|

시장보고서

상품코드

1850248

네트워크 트래픽 분석 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Network Traffic Analysis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

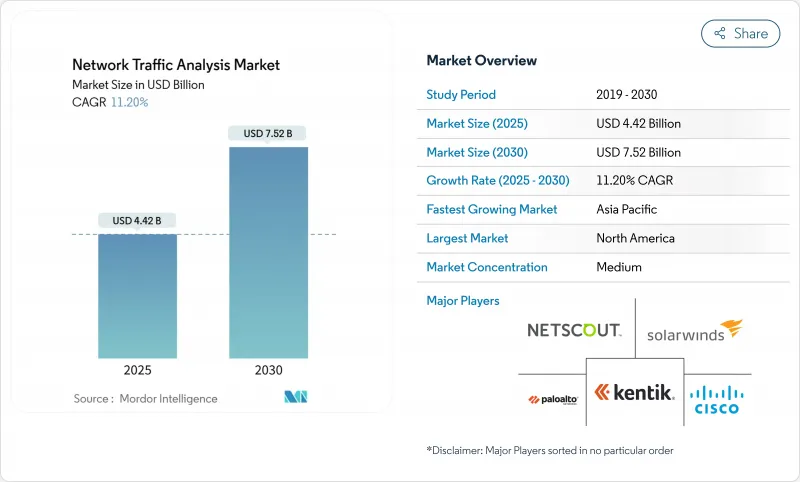

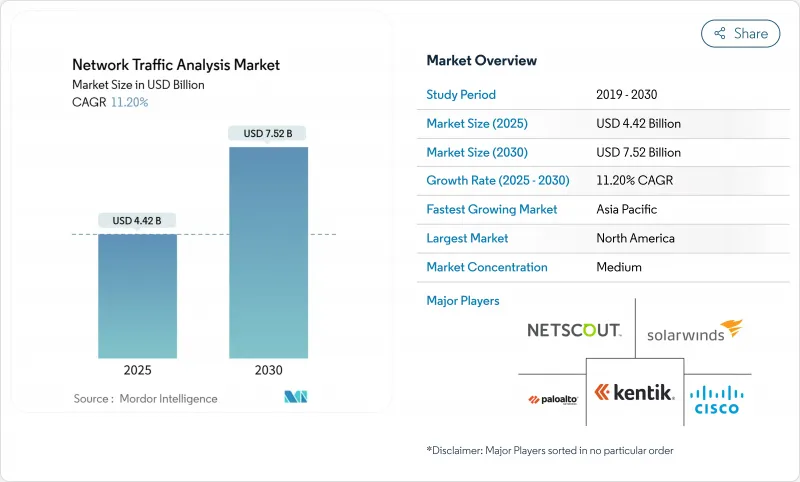

네트워크 트래픽 분석 시장 규모는 2025년에 44억 2,000만 달러로 평가되었고, 예측 기간(2025-2030년)의 CAGR은 11.20%를 나타낼 전망이며, 2030년에는 75억 2,000만 달러에 달할 전망입니다.

성장은 제로 트러스트 프로그램, 5G 도입, 클라우드 네이티브 워크로드가 기존 경계를 모호하게 만들면서 보안 커뮤니티가 경계 방어에서 심층 트래픽 가시성으로 전환한 것을 반영합니다. 기업들은 네트워크 텔레메트리를 하이브리드 환경에서 측면 이동, 암호화된 위협, 성능 병목 현상을 발견할 수 있는 유일한 신뢰할 수 있는 정보원으로 보고 있습니다. 보안 팀이 포인트 도구를 통합하는 가운데 AI 기반 분석과 지속적 패킷 캡처를 결합한 벤더들이 시장 점유율을 확대하고 있으며, 관리형 탐지 및 대응(MDR) 서비스는 소규모 IT 부서의 기술 격차를 해소하고 있습니다. 동시에 플랫폼 제공업체들은 TLS 1.3 채택과 마이크로서비스 확산에 대응하기 위해 암호화 트래픽 분석 및 동서 방향 검사 기능을 통합하기 위해 경쟁하고 있습니다.

세계의 네트워크 트래픽 분석 시장 동향 및 인사이트

최신 보안 스택의 핵심으로 NTA 출현

고도화된 지속적 위협(APT)의 70%는 주로 세분화된 트래픽 분석을 통해 탐지 가능한 측면 이동에 의존합니다. 이로 인해 보안 팀은 NTA를 선택적 도구에서 핵심 통제 수단으로 격상시키고 있습니다. 패킷 분석을 SIEM 및 XDR과 긴밀히 연동하면 사일로화된 도구 대비 탐지 소요 시간을 최대 30% 단축할 수 있습니다. 통합 텔레메트리는 상관 작업 부하를 40-50% 줄여, 부족한 분석 인력이 데이터 정리보다 트리아지에 집중할 수 있게 합니다. 오픈 API와 클라우드 규모 데이터 레이크를 제공하는 벤더들은 이제 많은 제로 트러스트 프로그램의 기반이 되어, NTA를 엔드포인트, 신원, 클라우드 방어의 기반 구조로 자리매김하고 있습니다. 그 결과, 플랫폼 중심 구매 행태가 독립형 프로브에서 통합 SaaS 분석으로 예산을 이동시키고 있습니다.

확장되는 네트워크 대역폭과 5G 도입이 가시성 격차를 발생

5G로의 전환은 초고밀도 셀, 분산된 사용자 평면 기능, 멀티액세스 엣지 컴퓨팅을 도입하여 기존 탭 및 스팬 포트를 압도합니다. 미국 내 사설 5G 지출만 2027년까지 37억 달러에 달할 것으로 예상되지만, 대부분의 기존 모니터링 스택은 컨테이너화된 트래픽을 수집하거나 밀리초 단위 이상 현상을 탐지할 수 없습니다. 서비스 제공업체들은 네트워크 슬라이싱과 인라인 위협 탐지를 결합하기 위해 보안 전문업체와 협력하고 있습니다(T-Mobile의 Prisma SASE 번들이 대표적인 사례). 사물인터넷(IoT)의 확산은 시그니처 기반 도구가 다양한 기기 행동에 취약해 분석 엔진에 부담을 가중시키며, 행동 및 머신러닝 중심 모델에 대한 수요를 촉진하고 있습니다.

위협의 급속한 진화와 도구를 앞지르는 암호화

TLS 1.3은 웹 트래픽의 95%를 암호화하고 핸드셰이크 메타데이터를 숨겨 기존 DPI를 무력화합니다. Encrypted ClientHello 및 0-RTT 재개와 같은 기능은 벤더들이 타이밍, 시퀀스 길이, 트래픽 형태에 의존하는 사이드 채널 추론으로 전환하도록 강요합니다. 다중 인스턴스 암호화 트래픽 트랜스포머 같은 연구용 프로토타입은 99% 분류 정확도를 달성했으나, 대부분의 IT 팀이 보유하지 못한 GPU급 성능과 데이터 과학 전문 인력이 필요합니다. 소규모 공급업체들은 R&D 비용 부담으로 어려움을 겪으며, 잠재적 이탈 또는 인수 가능성을 초래합니다.

부문 분석

클라우드 전개는 2024년 매출의 51.2%를 차지하며, 자본 지출(CapEx)을 운영 지출(OpEx)로 전환하는 탄력적인 SaaS 분석에 대한 선호도를 강조합니다. 하이브리드 모델은 성장의 선두주자로, 기업들이 기존 데이터 센터를 AWS, Azure 또는 GCP 환경과 통합함에 따라 2030년까지 연평균 13.7%의 성장률을 기록할 전망입니다. 이러한 조합은 클라우드의 민첩성을 유지하면서 데이터 거주 규정 준수를 보장합니다. Zscaler의 트래픽 캡처 서비스는 클라우드 플랫폼이 온프레미스 캡처 어플라이언스를 포화시키지 않고도 원시 트래픽을 분석 파이프라인으로 내보낼 수 있는 방법을 보여줍니다.

하이브리드 아키텍처를 도입한 기업들은 하드웨어 교체 비용이 감소하고 신규 검사 기능의 출시 속도가 빨라졌다고 보고합니다. 이는 업그레이드가 중앙에서 전개되기 때문입니다. 온프레미스 프로브는 에어갭 환경이나 규제가 엄격한 업종에서 여전히 사용되지만, 규제가 클라우드 인증 프레임워크를 수용함에 따라 네트워크 트래픽 분석 시장에서의 점유율은 꾸준히 감소하고 있습니다. 결과적으로 하이브리드 도입은 기업급 도구가 부족했던 신생 중견 기업으로의 네트워크 트래픽 분석 시장 확장을 촉진합니다.

솔루션(어플라이언스, 가상 센서, SaaS 콘솔)은 2024년 네트워크 트래픽 분석 시장 규모의 62.4%를 차지했습니다. 그러나 기업들이 모니터링 및 사고 대응을 아웃소싱함에 따라 서비스 부문은 연평균 14.5% 성장률을 보이고 있습니다. OPSWAT의 InQuest 인수는 벤더들이 연방 부문 요구를 충족하기 위해 관리형 서비스에 심층 파일 검사 및 위협 인텔리전스를 결합하는 방식을 보여줍니다.

관리형 서비스 채택은 분석가 부족과 제품 복잡성에 대한 실용적 대응입니다. 공급업체는 24/7 커버리지, 선별된 위협 피드, 자동화된 격리 기능을 제공하여 자원 제약 기업들의 도입을 촉진합니다. 하드웨어 센서는 FPGA 가속이 가상 어플라이언스를 여전히 능가하는 100Gbps 이상 백본에서 여전히 유효합니다. 그럼에도 벤더들은 해당 센서를 클라우드 분석에 데이터를 공급하는 포워더로 점점 더 포지셔닝하고 있습니다.

네트워크 트래픽 분석 시장은 전개(온프레미스, 클라우드 기반, 하이브리드), 구성 요소(솔루션 및 서비스), 조직 규모(대규모 및 중소기업), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), IT 및 통신 등), 지역별로 구분됩니다. 시장 규모 및 예측은 위의 모든 부문에 대해 금액(단위 : 백만 달러)으로 제공됩니다.

지역별 분석

북미는 엄격한 개인정보 보호법, 조기 제로트러스트 도입, 높은 사이버보안 예산 덕분에 2024년 매출의 34.06%를 차지했습니다. JP모건의 AI 기반 사기 방지 시스템은 위협 식별 속도를 300배 가속화하고 연간 2억 달러를 절감하는 패킷 기반 분석에 대한 지역적 수요를 보여줍니다. 주 정부 역시 관측 가능성을 적극 도입하고 있습니다. 인디애나주는 멀티클라우드 인프라 전반에 트래픽 분석을 전개한 후 시민 서비스를 개선했습니다.

아시아태평양 지역은 연평균 성장률(CAGR) 14.3%로 고성장 엔진입니다. 중국, 인도, 한국의 대규모 5G 구축과 스마트시티 투자, 증가하는 랜섬웨어 사건이 NTA 도입을 촉진합니다. 중국의 사이버보안법, 호주의 중요 인프라 보호법 등 현지 규제로 트래픽 로깅 및 이상 탐지가 의무화됩니다. 사설 셀룰러 네트워크로 생산 현장을 디지털화하는 제조업체들은 OT와 IT 융합을 보호하기 위한 세분화된 모니터링이 필요합니다.

유럽은 GDPR의 침해 통보 의무와 알고리즘 투명성을 요구하는 신생 AI 법규로 인해 견고한 수요를 유지하고 있습니다. 주권 클라우드 이니셔티브는 패킷이 지역 내에 머물도록 하이브리드 전개를 촉진하여, 세분화된 데이터 거주지 제어 기능을 제공하는 벤더들에게 유리합니다. 라틴 아메리카와 중동 및 아프리카는 아직 초기 단계이지만 유망합니다. 브라질 은행, 사우디 스마트 시티 프로젝트, 남아프리카 통신사들은 더 엄격한 사이버 규제를 예상하며 AI 기반 NTA를 시범 운영 중입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 현대 보안 스택의 핵심으로 부상하는 NTA

- 네트워크 대역폭의 확대와 5G의 전개에 의해 가시성 격차 발생

- 클라우드 및 하이브리드 아키텍처로 전환으로 클라우드 네이티브 NTA 수요 촉진

- 암호화 트래픽에 대한 머신러닝 기반 검사 요구사항

- 제로 트러스트 환경에서의 동서 방향 트래픽 확산

- SOC 통합이 NTA/NDR 통합 추진

- 시장 성장 억제요인

- 도구 개발 속도를 앞지르는 위협 및 암호화 기술의 급속한 진화

- 숙련된 분석가 부족 및 솔루션의 높은 복잡성

- 심층 패킷 검사를 제한하는 데이터 개인정보 보호 규정

- 엔드포인트/XDR 도구로 예산 재분배

- 업계 밸류체인 분석

- 규제 상황

- 기술의 전망

- 업계의 매력 - Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 거시 경제 요인이 시장에 미치는 영향

제5장 시장 규모와 성장 예측(가치관)

- 전개별

- 온프레미스

- 클라우드 기반

- 하이브리드

- 컴포넌트별

- 솔루션

- 하드웨어 어플라이언스

- 가상 어플라이언스

- SaaS 플랫폼

- 서비스

- 전문 서비스

- 관리형 서비스

- 솔루션

- 조직 규모별

- 대기업

- 중소기업

- 최종 사용자 업계별

- BFSI

- IT 및 통신

- 정부 및 방위

- 에너지 및 유틸리티

- 소매업 및 전자상거래

- 헬스케어 및 생명과학

- 제조업

- 기타 최종 사용자 업계

- 용도별

- 보안 및 위협 감지

- 성능 모니터링 및 최적화

- 규정 준수 및 정책 시행

- 용량 계획 및 예측

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 싱가포르

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- NETSCOUT Systems Inc.

- Cisco Systems Inc.

- Palo Alto Networks Inc.

- SolarWinds Corporation

- Kentik Technologies Inc.

- Dynatrace LLC

- ExtraHop Networks Inc.

- Flowmon Networks AS(Progress)

- GreyCortex sro

- Genie Networks Ltd.

- ManageEngine(Zoho Corp.)

- Plixer LLC

- Nagios Enterprises LLC

- Gigamon Inc.

- Corelight Inc.

- Vectra AI Inc.

- Ixia(Keysight Technologies Inc.)

- Riverbed Technology LLC

- Nozomi Networks Inc.

- Nokia Corporation

제7장 시장 기회와 미래 동향

- 화이트 스페이스와 미충족 요구의 평가

The Network Traffic Analysis Market size is estimated at USD 4.42 billion in 2025, and is expected to reach USD 7.52 billion by 2030, at a CAGR of 11.20% during the forecast period (2025-2030).

Growth reflects the security community's pivot from perimeter defenses to deep traffic visibility as zero-trust programs, 5G rollouts, and cloud-native workloads muddy traditional boundaries. Enterprises see network telemetry as the single source of truth that can uncover lateral movement, encrypted threats, and performance bottlenecks in a hybrid world. Vendors that marry AI-driven analytics with continuous packet capture are winning mindshare as security teams consolidate point tools, while managed detection and response (MDR) services temper the skills gap in small IT shops. At the same time, platform providers are racing to embed encrypted traffic analytics and east-west inspection to keep pace with TLS 1.3 adoption and microservices proliferation.

Global Network Traffic Analysis Market Trends and Insights

Emergence of NTA as Cornerstone in Modern Security Stacks

Seventy percent of advanced persistent threats rely on lateral movement, detectable primarily through granular traffic analytics, prompting security teams to elevate NTA from a nice-to-have tool to a foundational control. Tightly coupling packet analytics with SIEM and XDR cuts mean time to detect by up to 30% relative to siloed tools. Unified telemetry also trims correlation workloads 40-50%, freeing scarce analysts to focus on triage rather than data wrangling. Vendors that deliver open APIs and cloud-scale data lakes now underpin many zero-trust programs, positioning NTA as the fabric that underlies endpoint, identity, and cloud defenses. As a result, platform-first buying behavior is shifting budget from stand-alone probes toward integrated SaaS analytics.

Expanding Network Bandwidth and 5G Rollouts Create Visibility Gaps

The jump to 5G introduces ultra-dense cells, distributed user-plane functions, and multi-access edge computing that overwhelm classic taps and span ports. Private 5G outlays in the United States alone are expected to hit USD 3.7 billion by 2027, yet most existing monitoring stacks cannot ingest containerized traffic or detect millisecond-scale anomalies. Service providers partner with security specialists-T-Mobile's Prisma SASE bundle is a notable example-to pair network slicing with inline threat detection. IoT proliferation further stresses analytics engines because signature-based tools falter against diverse device behaviors, fueling demand for behavior and ML-centric models.

Rapid Evolution of Threats and Encryption Outpacing Tooling

TLS 1.3 encrypts 95% of web traffic and conceals handshake metadata, thwarting legacy DPI. Features such as Encrypted ClientHello and 0-RTT resumption force vendors to pivot toward side-channel inference that relies on timing, sequence lengths, and traffic morphologies. Research prototypes like multi-instance encrypted traffic transformers hit 99% classification accuracy but demand GPU-class horsepower and data science talent that most IT teams lack. Smaller suppliers struggle with R&D costs, creating potential attrition or acquisition.

Other drivers and restraints analyzed in the detailed report include:

- Migration to Cloud and Hybrid Architectures Boosts Demand for Cloud-Native NTA

- Zero-Trust East-West Traffic Proliferation

- Shortage of Skilled Analysts and High Solution Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments controlled 51.2% of 2024 revenue, underscoring preference for elastic SaaS analytics that shift capex to opex. The hybrid model is the growth pacesetter, registering a 13.7% CAGR through 2030 as enterprises knit legacy data centers with AWS, Azure, or GCP estates. That blend ensures compliance with data-residency rules while sustaining cloud agility. Zscaler's Traffic Capture service showcases how cloud platforms can export raw traffic to analytics pipelines without saturating on-premises capture appliances.

Enterprises adopting hybrid architectures report lower hardware refresh spend and faster rollout of new inspection features because upgrades are deployed centrally. On-premises probes persist in air-gapped or highly regulated verticals, yet their share of the network traffic analysis market steadily recedes as regulations embrace cloud certification frameworks. Hybrid adoption consequently propels overall network traffic analysis market expansion into greenfield midsize companies that lacked enterprise-class tooling.

Solutions-appliances, virtual sensors, and SaaS consoles-represented 62.4% of the network traffic analysis market size in 2024. However, services are scaling at 14.5% CAGR as organizations offload monitoring and incident response. OPSWAT's buyout of InQuest illustrates how vendors bundle Deep File Inspection and threat intel with managed offerings to address federal-sector needs.

Managed service uptake is a pragmatic response to analyst scarcity and product complexity. Providers supply 24/7 coverage, curated threat feeds, and automated containment, boosting adoption among resource-constrained firms. Hardware sensors retain relevance in 100 Gbps-plus backbones where FPGA acceleration still outperforms virtual appliances. Even so, vendors increasingly position those sensors as data forwarders feeding cloud analytics.

Network Traffic Analysis Market is Segmented by Deployment (On-Premise, Cloud-Based, and Hybrid), Component (Solutions and Services), Organization Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (BFSI, IT and Telecom, and More), and Geography. The Market Sizes and Forecasts are Provided in Value (in USD Million) for all the Above Segments.

Geography Analysis

North America contributed 34.06% of 2024 revenue thanks to strict privacy statutes, early zero-trust adoption, and high cybersecurity budgets. JPMorgan's AI-infused fraud system illustrates regional appetite for packet-driven analytics that accelerate threat identification 300-fold and save USD 200 million annually. State governments likewise embrace observability; Indiana improved citizen services after deploying traffic analytics across multi-cloud infrastructure.

Asia-Pacific is the high-growth engine with a 14.3% CAGR. Massive 5G rollouts in China, India, and South Korea, combined with smart-city investments and rising ransomware incidents, spur NTA adoption. Local regulations such as China's Cybersecurity Law and Australia's Critical Infrastructure Act compel traffic logging and anomaly detection. Manufacturers digitizing shop floors with private cellular networks need granular monitoring to secure OT and IT convergence.

Europe maintains robust demand owing to GDPR's breach notification requirements and emerging AI legislation that mandates algorithmic transparency. Sovereign-cloud initiatives push hybrid deployments so packets stay in-region, benefitting vendors that provide fine-grained data-residency controls. Latin America and the Middle East and Africa remain nascent but promising: Brazilian banks, Saudi smart-city projects, and South African telcos are piloting AI-fueled NTA in anticipation of stricter cyber mandates.

- NETSCOUT Systems Inc.

- Cisco Systems Inc.

- Palo Alto Networks Inc.

- SolarWinds Corporation

- Kentik Technologies Inc.

- Dynatrace LLC

- ExtraHop Networks Inc.

- Flowmon Networks A.S. (Progress)

- GreyCortex s.r.o.

- Genie Networks Ltd.

- ManageEngine (Zoho Corp.)

- Plixer LLC

- Nagios Enterprises LLC

- Gigamon Inc.

- Corelight Inc.

- Vectra AI Inc.

- Ixia (Keysight Technologies Inc.)

- Riverbed Technology LLC

- Nozomi Networks Inc.

- Nokia Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Emergence of NTA as cornerstone in modern security stacks

- 4.2.2 Expanding network bandwidth and 5G rollouts create visibility gaps

- 4.2.3 Migration to cloud and hybrid architectures boosts demand for cloud-native NTA

- 4.2.4 Encrypted traffic ML-based inspection requirements

- 4.2.5 Zero-trust east-west traffic proliferation

- 4.2.6 SOC consolidation pushing NTA/NDR convergence

- 4.3 Market Restraints

- 4.3.1 Rapid evolution of threats and encryption outpacing tooling

- 4.3.2 Shortage of skilled analysts and high solution complexity

- 4.3.3 Data-privacy regulations restricting deep packet inspection

- 4.3.4 Budget reallocation toward endpoint/XDR tools

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Deployment

- 5.1.1 On-premise

- 5.1.2 Cloud-based

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Solutions

- 5.2.1.1 Hardware Appliances

- 5.2.1.2 Virtual Appliances

- 5.2.1.3 SaaS Platform

- 5.2.2 Services

- 5.2.2.1 Professional Services

- 5.2.2.2 Managed Services

- 5.2.1 Solutions

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 IT and Telecom

- 5.4.3 Government and Defense

- 5.4.4 Energy and Utilities

- 5.4.5 Retail and E-commerce

- 5.4.6 Healthcare and Life Sciences

- 5.4.7 Manufacturing

- 5.4.8 Other End-user Industries

- 5.5 By Application

- 5.5.1 Security and Threat Detection

- 5.5.2 Performance Monitoring and Optimization

- 5.5.3 Compliance and Policy Enforcement

- 5.5.4 Capacity Planning and Forecasting

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Malaysia

- 5.6.4.6 Singapore

- 5.6.4.7 Australia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 NETSCOUT Systems Inc.

- 6.4.2 Cisco Systems Inc.

- 6.4.3 Palo Alto Networks Inc.

- 6.4.4 SolarWinds Corporation

- 6.4.5 Kentik Technologies Inc.

- 6.4.6 Dynatrace LLC

- 6.4.7 ExtraHop Networks Inc.

- 6.4.8 Flowmon Networks A.S. (Progress)

- 6.4.9 GreyCortex s.r.o.

- 6.4.10 Genie Networks Ltd.

- 6.4.11 ManageEngine (Zoho Corp.)

- 6.4.12 Plixer LLC

- 6.4.13 Nagios Enterprises LLC

- 6.4.14 Gigamon Inc.

- 6.4.15 Corelight Inc.

- 6.4.16 Vectra AI Inc.

- 6.4.17 Ixia (Keysight Technologies Inc.)

- 6.4.18 Riverbed Technology LLC

- 6.4.19 Nozomi Networks Inc.

- 6.4.20 Nokia Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment