|

시장보고서

상품코드

1850253

포그 네트워킹 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Fog Networking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

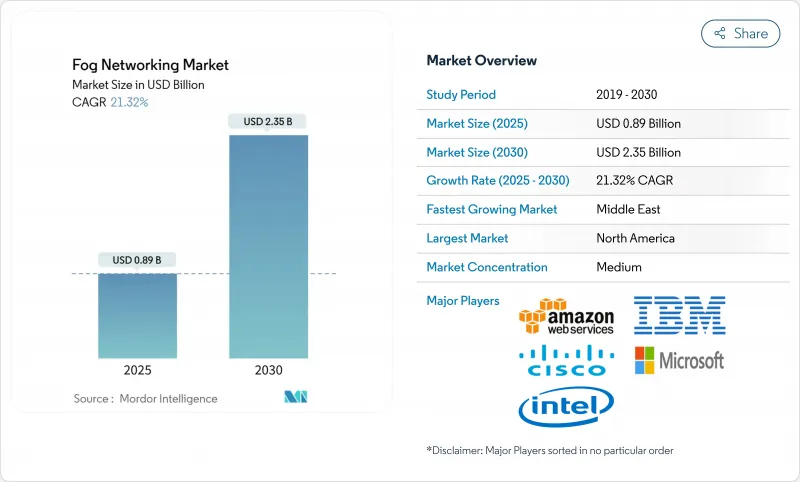

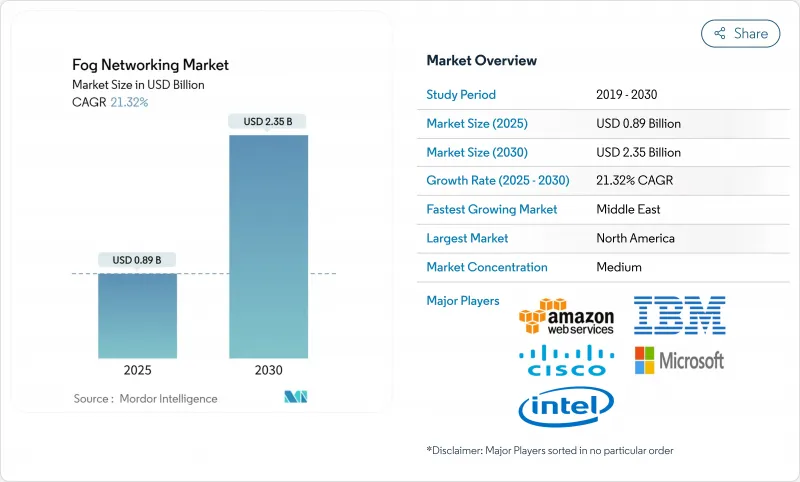

포그 네트워킹 시장 규모는 2025년에 8억 9,000만 달러로 평가되었고, 2030년에는 23억 5,000만 달러에 이를 것으로 예측되며, CAGR은 21.32%를 나타낼 전망입니다.

하드웨어 게이트웨이와 엣지 서버가 현재 대부분의 전개를 주도하는 가운데, 기업들이 장치 근처에서 실시간 데이터 처리를 추구함에 따라 소프트웨어 정의 오케스트레이션 및 보안 계층이 주목받고 있습니다. 5G와 Wi-Fi 7의 신속한 보급, IoT 센서 가격 하락, 강화된 데이터 주권 규제는 로컬 컴퓨팅의 비즈니스 사례를 더욱 공고히 합니다. 벤더들은 마이크로 데이터 센터 폼 팩터에 인공지능 가속기를 계속 통합하여 자율주행차, 정밀 제조, 핵심 건강 모니터링을 위한 저지연 분석을 가능하게 합니다. 보안 복잡성과 분산된 오케스트레이션 스택이 단기 도입을 제한하지만, 엣지 연결성과 국가 디지털 전환 프로그램에 대한 지속적인 투자가 포그 네트워킹 시장의 장기적 확장을 뒷받침합니다.

세계의 포그 네트워킹 시장 동향 및 인사이트

실시간 분석 수요 증가

제조 기업들은 10밀리초 이내에 반응해야 하는 예측 유지보수 모델을 실행하기 위해 포그 게이트웨이를 도입하고 있습니다. 메르세데스-벤츠 공장은 생산 엣지에 임베디드 머신러닝을 적용해 차량 테스트 시간 예측 정확도를 82.88%까지 끌어올렸습니다. 클라우드에서 현장 포그 노드로 원격의료 워크로드를 전환한 병원들은 지연 시간을 100밀리초에서 5밀리초로 단축하고 공격 표면을 35% 감소시켰다. 유사한 지연 시간 개선 효과는 자동화 창고 로봇, 교통 신호 최적화, 첨단 운전자 보조 시스템의 기반이 됩니다. 경제적 인센티브는 속도 그 이상으로 확장됩니다. 에너지 효율성 연구에 따르면 중앙 집중식 처리 대비 전력 사용량이 25-30% 낮아져 자본 지출 정당성을 강화합니다.

저가 IoT 센서의 보급

5달러 미만의 산업용 등급 센서로 이제 공장 현장과 도시 인프라 전반에 걸쳐 지속적인 자산 모니터링이 가능해졌습니다. 산업 인터넷 컨소시엄(IIC)은 비용 효율적인 센서 통합을 주요 엣지 컴퓨팅 촉매제로 강조합니다. NIST(미국국립표준기술연구소)의 IoT 자문위원회 역시 분산형 아키텍처를 국가 핵심 인프라 복원력에 필수적이라고 분류합니다. 저렴한 센서는 스마트 그리드, 건물 에너지 관리, 누수 감지를 위한 실시간 최적화 루프에 데이터를 공급하며, 포그 노드에 내장된 로컬 분석 역량에 대한 수요를 높입니다.

보안 공격 측면 복잡성

모든 분산 노드는 의료 및 제조 운영자가 HIPAA(건강보험이동성 및 책임법) 및 GDPR(일반개인정보보호법) 규정에 따라 보호해야 하는 새로운 취약점을 도입합니다. 유럽방위청(EDA)의 CLAUDIA 프로젝트는 전술적 엣지 보안 프레임워크를 다루지만, 사고 대응은 여전히 분산된 상태입니다. 운영 기술(OT) 환경에서 침해는 물리적 안전을 위협하므로, 포그 클러스터 전반에 걸친 제로 트러스트 아키텍처와 런타임 무결성 모니터링에 대한 투자가 필수적입니다.

부문 분석

온프레미스 노드는 2024년 포그 네트워킹 시장 점유율의 46%를 차지했으며, 이는 의료, 금융, 국방 분야의 엄격한 데이터 현지화 의무를 반영합니다. 결정론적 지연 시간과 규제 통제를 중시하는 산업들은 컴퓨팅 자산을 보안 시설 내 또는 생산 라인 내부에서 운영합니다. 지멘스와 마이크로소프트의 하이브리드 아키텍처는 온프레미스 산업용 엣지 런타임과 Azure 기반 분석을 결합하여 유연한 감독에 대한 수요를 강조합니다.

호스팅형 포그 서비스(Fog-as-a-Service)는 관리형 서비스 제공업체들이 라이프사이클 지원, 위협 모니터링, 용량 최적화 서비스를 번들로 제공함에 따라 26%의 연평균 성장률(CAGR)로 가장 빠르게 성장하고 있습니다. 자체 IT 역량이 부족한 중소 제조업체 및 유통업체가 가장 큰 혜택을 보며, 전문 하드웨어 구매나 운영 없이도 고급 AI를 활용할 수 있습니다. 통신사와 하이퍼스케일 클라우드 기업이 현장 컴퓨팅으로 서비스 범위를 확장함에 따라 호스팅 서비스의 포그 네트워킹 시장 규모는 2025년부터 2030년 사이 3배 성장할 전망입니다.

포그 네트워킹 시장은 구성요소(하드웨어, 소프트웨어, 서비스), 전개 모델(온프레미스, 호스팅/관리, 하이브리드), 최종 사용자용도(스마트 미터, 스마트 미터 외 등), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 기업 디지털화 예산, 성숙한 5G 커버리지, 지원적 규제 명확성에 힘입어 2024년 매출의 37%를 차지하며 선두를 달렸다. 미국 스타트업 생태계에는 현재까지 111억 달러를 조달한 203개 엣지 컴퓨팅 기업이 포진해 있다(Tracxn 기준). 캐나다는 규모는 작지만 활기찬 클러스터로, 2024년 투자 감소에도 불구하고 2억 1,400만 달러의 자금을 유치했습니다.

유럽은 데이터 주권을 강조하는 GDPR과 디지털 시장법(Digital Markets Act)의 영향으로 뒤를 이었습니다. 통신 인프라 의존성에 대한 의회 논의는 자국산 포그 스택(fog stack) 투자를 강화하고 있습니다(Europarl). 유럽의 산업적 전통은 자동차 및 중장비 분야의 도입을 뒷받침하며, EU 지원 시범 사업에 따르면 2021년부터 2027년까지 설치 기반 성장률이 두 배로 증가할 것으로 나타났습니다.

중동은 사우디아라비아와 UAE의 스마트시티 메가프로젝트가 초당 분석이 필요한 수천 개의 도로변 센서와 감시 카메라를 배치하며 27%의 연평균 성장률(CAGR)을 기록했습니다. 국가 AI 전략은 주권적 데이터 처리를 우선시하여 지역 데이터센터 및 포그 게이트웨이 구축을 촉진하고 있습니다. 아시아태평양 전역에서 중국의 산업용 IoT 정책, 일본의 로봇 기술 리더십, 인도의 5G 확장은 상당한 수요를 창출하고 있습니다. 설치 인건비 절감으로 투자 수익률이 더욱 개선되어 2차 제조 허브 전반에 걸쳐 도입이 가속화될 전망입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 실시간 분석 수요 증가

- 저비용 IoT 센서 보급

- 5G와 Wi-Fi 7 고밀도화

- OpenFog/ETSI MEC 표준 채택

- 엣지 AI 가속기 출하량 급증

- 국가 데이터 주권 의무

- 시장 성장 억제요인

- 보안 공격 표면의 복잡성

- 분산된 오케스트레이션 스택

- 기존 OT 사이트의 자본 지출 부담

- 제한된 포그 인재 풀

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 라이벌 관계의 격렬

- 기술 로드맵

제5장 시장 규모와 성장 예측

- 컴포넌트별

- 하드웨어

- 포그 게이트웨이

- 엣지 서버 및 마이크로 DC

- IoT 칩셋 및 가속기

- 소프트웨어 및 서비스

- 포그 관리 플랫폼

- 보안 및 오케스트레이션

- 하드웨어

- 전개 모델별

- 온프레미스

- 호스트/관리

- 하이브리드

- 최종 사용자용도별

- 스마트 미터

- 빌딩 및 홈 자동화

- 스마트 매뉴팩처링

- 커넥티드 헬스케어

- 커넥티드 차량

- 기타(석유 및 가스, 소매 등)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amazon Web Services

- Cisco Systems

- Dell Technologies

- IBM

- Intel

- Microsoft

- Nebbiolo Technologies

- Nokia

- Qualcomm

- Tata Consultancy Services

- Advantech

- HPE

- Huawei

- Arm

- Schneider Electric

- Bosch .IO

- GE Digital

- Saguna Networks

- ClearBlade

- FogHorn(Google)

- EdgeIQ

- Vapor IO

- Fastly

- Equinix Metal

제7장 시장 기회와 장래의 전망

HBR 25.11.17The fog networking market size is estimated at USD 0.89 billion in 2025 and is forecast to reach USD 2.35 billion by 2030, advancing at a 21.32% CAGR.

Hardware gateways and edge servers currently anchor most deployments, while software-defined orchestration and security layers gain traction as enterprises seek real-time data processing close to devices. Rapid 5G and Wi-Fi 7 rollouts, falling IoT sensor prices, and stricter data-sovereignty mandates reinforce the business case for localized computing. Vendors continue integrating artificial-intelligence accelerators into micro-data-center form factors, enabling low-latency analytics for autonomous vehicles, precision manufacturing, and critical health monitoring. Although security complexity and fragmented orchestration stacks temper near-term uptake, sustained investment in edge connectivity and national digital-transformation programs underpins long-term expansion of the fog networking market

Global Fog Networking Market Trends and Insights

Expanding Real-Time Analytics Demand

Manufacturing organizations deploy fog gateways to run predictive-maintenance models that must respond in less than 10 milliseconds. A Mercedes-Benz plant recorded 82.88% accuracy in forecasting vehicle-test times by applying embedded machine learning at the production edge. Hospitals that shift telemedicine workloads from cloud to on-site fog nodes have cut latency from 100 milliseconds to 5 milliseconds and reduced the attack surface by 35%. Similar latency gains underpin automated warehouse robotics, traffic-signal optimization, and advanced driver-assistance systems. The economic incentive extends beyond speed: energy-efficiency studies show 25-30% lower power use versus centralized processing, reinforcing capital-spending justification.

Proliferation of Low-Cost IoT Sensors

Industrial-grade sensors priced below USD 5 now enable continuous asset monitoring across shop floors and city infrastructure. The Industrial Internet Consortium stresses cost-effective sensor integration as a primary edge-computing catalyst. NIST's IoT Advisory Board likewise classifies distributed architectures as essential for national critical-infrastructure resilience NIST. Cheap sensors feed real-time optimization loops for smart grids, building-energy management, and leakage detection, elevating demand for local analytics capacity embedded in fog nodes.

Security Attack-Surface Complexity

Every distributed node introduces new vulnerabilities that healthcare and manufacturing operators must secure in line with HIPAA and GDPR provisions. The European Defence Agency's CLAUDIA project addresses tactical-edge security frameworks, yet incident-response remains fragmented. In operational-technology environments, breaches risk physical safety, compelling investment in zero-trust architectures and runtime-integrity monitoring across fog clusters.

Other drivers and restraints analyzed in the detailed report include:

- 5G & Wi-Fi 7 Densification

- Edge AI Accelerator Shipments Surge

- Fragmented Orchestration Stacks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premisess nodes accounted for 46% of the 2024 fog networking market share, mirroring strict data-localization mandates in healthcare, finance, and defense. Industries valuing deterministic latency and regulatory control keep compute assets within secured facilities or even inside production lines. Siemens and Microsoft's hybrid architecture combineson-premiseses Industrial Edge runtimes with Azure-based analytics, underscoring demand for flexible oversight.

Hosted fog-as-a-service grows fastest at 26% CAGR as managed-service providers bundle lifecycle support, threat-monitoring, and capacity right-sizing. Smaller manufacturers and retailers lacking in-house IT benefit most, accessing advanced AI without purchasing or operating specialized hardware. The fog networking market size for hosted services is projected to triple between 2025 and 2030 as telcos and hyperscale clouds extend service catalogues to field-level computing.

Fog Networking Market is Segmented by Component (Hardware, Software, Service), Deployment Model (On-Premise, Hosted/Managed, and Hybrid), End-User Application (Smart Metering, Smart Metering and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 37% of 2024 revenue, propelled by enterprise digitization budgets, mature 5G coverage, and supportive regulatory clarity. United States start-up ecosystems host 203 edge-computing firms that raised USD 11.1 billion to date Tracxn. Canada's smaller yet vibrant cluster recorded USD 214 million in funding despite a 2024 pullback.

Europe follows, shaped by GDPR and the Digital Markets Act that stress data sovereignty. Parliament debates on communications-infrastructure dependence reinforce investment in indigenous fog stacks Europarl. The continent's industrial pedigree underpins adoption in automotive and heavy machinery; EU-funded pilots show far-edge compute nodes doubling installed-base growth from 2021 to 2027.

The Middle East posts a 27% CAGR as smart-city megaprojects in Saudi Arabia and the UAE deploy thousands of roadside sensors and surveillance cameras requiring sub-second analytics. National AI strategies privilege sovereign data processing, catalysing regional data-center and fog-gateway rollouts Across APAC, China's industrial-IoT policy, Japan's robotics leadership, and India's 5G expansion foster sizeable demand. Lower installation labour costs further improve return on investment, accelerating adoption across tier-2 manufacturing hubs.

- Amazon Web Services

- Cisco Systems

- Dell Technologies

- IBM

- Intel

- Microsoft

- Nebbiolo Technologies

- Nokia

- Qualcomm

- Tata Consultancy Services

- Advantech

- HPE

- Huawei

- Arm

- Schneider Electric

- Bosch .IO

- GE Digital

- Saguna Networks

- ClearBlade

- FogHorn (Google)

- EdgeIQ

- Vapor IO

- Fastly

- Equinix Metal

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding real-time analytics demand

- 4.2.2 Proliferation of low-cost IoT sensors

- 4.2.3 5G and Wi-Fi 7 densification

- 4.2.4 OpenFog/ETSI MEC standard adoption

- 4.2.5 Edge AI accelerator shipments surge

- 4.2.6 National data-sovereignty mandates

- 4.3 Market Restraints

- 4.3.1 Security attack-surface complexity

- 4.3.2 Fragmented orchestration stacks

- 4.3.3 CAPEX burden on brownfield OT sites

- 4.3.4 Limited fog talent pool

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Technology Roadmap

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component (Value, USD)

- 5.1.1 Hardware

- 5.1.1.1 Fog gateways

- 5.1.1.2 Edge servers and micro-DCs

- 5.1.1.3 IoT chipsets and accelerators

- 5.1.2 Software and Services

- 5.1.2.1 Fog management platform

- 5.1.2.2 Security and orchestration

- 5.1.1 Hardware

- 5.2 By Deployment Model (Value, USD)

- 5.2.1 On-premise

- 5.2.2 Hosted/Managed

- 5.2.3 Hybrid

- 5.3 By End-user Application (Value, USD)

- 5.3.1 Smart Metering

- 5.3.2 Building and Home Automation

- 5.3.3 Smart Manufacturing

- 5.3.4 Connected Healthcare

- 5.3.5 Connected Vehicle

- 5.3.6 Others (Oil and Gas, Retail, etc.)

- 5.4 By Geography (Value, USD)

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Israel

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Turkey

- 5.4.5.5 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amazon Web Services

- 6.4.2 Cisco Systems

- 6.4.3 Dell Technologies

- 6.4.4 IBM

- 6.4.5 Intel

- 6.4.6 Microsoft

- 6.4.7 Nebbiolo Technologies

- 6.4.8 Nokia

- 6.4.9 Qualcomm

- 6.4.10 Tata Consultancy Services

- 6.4.11 Advantech

- 6.4.12 HPE

- 6.4.13 Huawei

- 6.4.14 Arm

- 6.4.15 Schneider Electric

- 6.4.16 Bosch .IO

- 6.4.17 GE Digital

- 6.4.18 Saguna Networks

- 6.4.19 ClearBlade

- 6.4.20 FogHorn (Google)

- 6.4.21 EdgeIQ

- 6.4.22 Vapor IO

- 6.4.23 Fastly

- 6.4.24 Equinix Metal

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment