|

시장보고서

상품코드

1850258

가상화 보안 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Virtualization Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

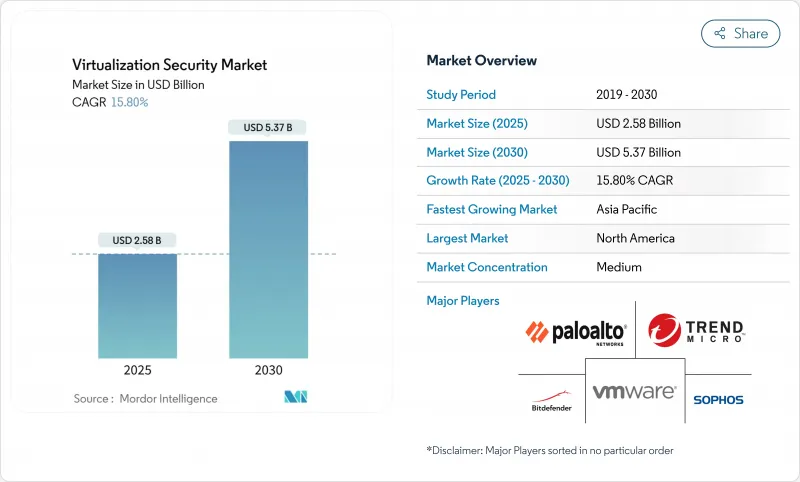

가상화 보안 시장 규모는 2025년에 25억 8,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 15.80%로 성장할 전망이며, 2030년에는 53억 7,000만 달러에 달할 것으로 예측됩니다.

하이브리드 클라우드 및 멀티클라우드 전개, 공급업체 플랫폼 통합, 기밀 컴퓨팅 채택 증가로 확장 가능한 제어에 대한 수요가 높은 수준으로 추세되고 있습니다. Broadcom의 VMware와의 통합은 번들로 구성된 프라이빗 클라우드 구독이 수익과 마진을 모두 향상시키는 방법을 보여주며 기업이 통합된 스택을 선호한다는 것을 뒷받침합니다. 동시에, AI를 활용한 공격 표면의 발견은 마이크로 세분화을 옵션 애드온에서 기본 요건으로 밀어 올립니다. 인텔 VT-rp와 같은 하드웨어 지원 방위는 위협의 주체가 하이퍼바이저의 메모리 변환 경로를 타겟팅하기 때문에 실리콘 혁신이 가상화 보안 시장에서 필수적인 계층이 되고 있음을 보여줍니다.

세계의 가상화 보안 시장 동향 및 인사이트

하이브리드 및 멀티클라우드 채택 급증

Broadcom은 2024년 VMware Cloud Foundation의 매출을 215억 달러로 인상했으며, 고객이 프라이빗 클라우드와 퍼블릭 클라우드에 걸쳐 단일 컨트롤 플레인을 요구하고 있음을 입증했습니다. 워크로드가 환경 간에 홉되면서 동서양의 가시성은 경계 방어만큼 중요해집니다. Azure Confidential VM은 원활한 마이그레이션을 가능하게 하면서 신뢰할 수 있는 실행 환경이 사용 중인 암호화를 유지하는 방법을 보여줍니다. 정책은 각 서브넷이 아니라 각 워크로드를 따라야하기 때문에 아이덴티티 중심 모델과 제로 트러스트 모델은 전통적인 경계 구역화를 대체합니다. 또한 종량 과금제 때문에 예산에 핍박한 경우에도 근대화 프로젝트를 정체시키지 않습니다.

엄격한 데이터 보호 규정(GDPR(EU 개인정보보호규정), CCPA, DPDPA)

인도의 새로운 DPDPA 규칙은 가상화 설계도에 통합되어야 하는 명확한 목적 제한과 국경을 넘어서는 이전 제한을 의무화합니다. 말레이시아와 베트남에서도 비슷한 의무가 있으며 감사 추적과 암호화 키의 거버넌스가 필요합니다. 헬스케어 시스템은 HIPAA를 준수하는 가상 작업 공간을 채택하여 ePHI를 개인 장치에 반입하지 않도록 하는 동시에 원격지의 임상의가 안전하게 작업할 수 있도록 하고 있습니다. 컴플라이언스 위반에 대한 처벌이 라이선스 비용을 초과하기 때문에 가상화 보안 시장은 프라이버시 바이 디자인 원칙을 모든 릴리스에 통합합니다.

전문적인 보안 어플라이언스의 높은 초기 비용

KubeVirt와 OpenShift는 전통적인 vSphere 라이선스를 대체하는 비용 효율적인 옵션으로 평가되었습니다. 설문 조사에 따르면 중소기업의 78%가 가상 서버용 안티바이러스를 도입하지 않았으며 48%는 예산 제한을 위해 적절한 방화벽을 도입하지 않았다고 합니다. 트러스트된 칩 공급 중단은 어플라이언스 비용을 증가시키고 새로 고침 사이클을 지연시킵니다.

부문 분석

2024년 가상화 보안 시장 점유율의 64.2%는 솔루션입니다. Palo Alto Networks의 차세대 보안 ARR은 34% 증가한 48억 달러에 이르렀으며 플랫폼화가 구매자의 공감을 불러일으키고 있음을 분명히 보여줍니다. 복잡한 하이브리드 설계에는 타사 전문 지식이 필요하기 때문에 서비스도 이 기세를 재현하여 CAGR 19.1%로 성장하고 있습니다. 포티넷과 같은 공급업체는 Lacework와 같은 인수 회사를 단일 패브릭에 통합하여 도구의 난립을 억제하고 고객을 더 긴 계약에 묶습니다. 따라서 시장 세분화 시장 규모는 CNAPP, 마이크로 세분화 및 제로 트러스트 네트워크 액세스를 단일 라이선스로 결합한 통합 제품으로 편향됩니다.

중소기업은 어플라이언스의 초기 비용과 직원 부담을 없애고 액세스를 민주화하는 SaaS 소비 패턴에서 이익을 얻고 있습니다. 결과적으로 서비스 제공업체는 기성품 구축 설계도와 월별 구독 가격으로 느린 보급이 있는 이 계층을 대상으로 합니다.

하드웨어 및 서버 가상화는 VM 분리에 있어서 기본적인 역할로 2024년 46.3%의 점유율을 유지했습니다. Intel VT-rp는 실리콘 레이어에서의 하드닝을 보여주고, 페이징 구조의 변조를 방해하며, 하이퍼바이저의 신뢰 경계를 강화합니다. Cisco Hypershield와 같은 AI 네이티브 패브릭은 분산 포드 전체에 커널 수준 정책 시행을 통합하기 때문입니다. 네트워크 계층의 가상화 보안 시장 규모는 OT 공장이 센서와 PLC를 가상화하고 결정론적이지만 안전한 트래픽 흐름을 필요로 할 때 더욱 확대됩니다.

가상화 보안 시장은 컴포넌트별(솔루션 및 서비스), 가상화 계층별(하드웨어 및 서버 가상화, 애플리케이션 가상화 등), 전개 모드별(온프레미스, 프라이빗 클라우드 등), 최종 사용자 산업별(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 의료 및 생명 과학 등), 조직 규모별(대기업 및 중소기업), 지역별로 구분됩니다.

지역 분석

북미는 2024년 매출의 35.26%를 차지했으며, 제로 트러스트의 조기 도입과 HIPAA나 CCPA와 같은 엄격한 분야별 의무에 지지되고 있습니다. 벤더는 미국에 연구개발 및 채널 에코시스템을 집중시켜 피드백 사이클의 단축과 기능 제공의 신속화를 도모하고 있습니다.

아시아태평양은 2030년까지 매년 18.1% 성장이 전망되는 고속 엔진입니다. 인도의 DPDPA와 말레이시아의 엄격한 데이터 담당자 의무로 인해 중견기업도 감사 대응 가상화 스택을 채택하게 됩니다. 중국, 베트남 및 태국의 제조 클러스터는 현장 워크로드를 가상화하고 엣지 보안 출하를 촉진합니다.

유럽은 GDPR(EU 개인정보보호규정) 하에서 꾸준한 페이스를 유지하고 있습니다. 슈렘스 II 판결은 데이터 전송 조건을 충족시키기 위한 기밀 컴퓨팅 인증에 대한 관심을 높입니다. 한편, GCC 국가들은 석유에서 얻은 예산을 스마트시티와 전자정부 프로젝트에 돌려보내 안전한 가상화 클라우드에 의존하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 하이브리드 클라우드 및 멀티 클라우드의 도입 급증

- 엄격한 데이터 보호 규정(GDPR(EU 개인정보보호규정), CCPA, DPDPA)

- 에지 데이터센터에서 VM 및 컨테이너 워크로드의 폭발적인 증가

- 하이퍼바이저 라이선스 인플레이션이 오픈소스 하이퍼바이저 추진

- AI에 의한 공격 대상 영역의 검출이 마이크로 세분화 수요 상승 초래

- 기밀 컴퓨팅의 증명이 조달 기준으로

- 시장 성장 억제요인

- 특수 보안 기기의 높은 초기 비용

- 숙련된 가상 보안 엔지니어의 부족

- VM의 확산에 의해 제로 트러스트 적용 복잡화 초래

- 양자 대응 암호화 프리미엄이 구입 사이클 지연 초래

- 업계 밸류체인 분석

- 규제 상황

- 기술의 전망

- 업계의 매력-Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 거시 경제 요인이 시장에 미치는 영향

제5장 시장 규모 및 성장 예측(가치)

- 컴포넌트별

- 솔루션

- 서비스

- 가상화 계층별

- 하드웨어 및 서버 가상화

- 애플리케이션 가상화

- 네트워크와 SD-WAN 가상화

- 스토리지 가상화

- 전개 모드별

- 온프레미스

- 프라이빗 클라우드

- 퍼블릭 클라우드

- 하이브리드 클라우드

- 최종 사용자 업계별

- IT 및 통신

- BFSI

- 헬스케어 및 생명과학

- 정부 및 방위

- 소매업 및 전자상거래

- 제조업

- 기타 최종 사용자 산업

- 조직 규모별

- 대기업

- 중소기업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 싱가포르

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- VMware Inc.(Broadcom Inc.)

- Trend Micro Inc.

- Sophos Ltd.

- Bitdefender LLC

- Palo Alto Networks Inc.

- Fortinet Inc.

- Check Point Software Technologies Ltd.

- Cisco Systems Inc.

- Juniper Networks Inc.

- Kaspersky Lab

- McAfee LLC

- IBM Corporation

- Microsoft Corporation

- Citrix Systems Inc.

- Red Hat Inc.

- Nutanix Inc.

- Parallels International GmbH

- Sangfor Technologies Inc.

- Guardicore(Akamai Technologies)

- Illumio Inc.

- Acronis International GmbH

- Symantec Enterprise Division(Broadcom)

- Hillstone Networks

- Radware Ltd.

- Tenable Holdings Inc.

제7장 시장 기회 및 미래 동향

- 화이트 스페이스 및 미충족 요구의 평가

The Virtualization Security Market size is estimated at USD 2.58 billion in 2025, and is expected to reach USD 5.37 billion by 2030, at a CAGR of 15.80% during the forecast period (2025-2030).

Rising hybrid and multi-cloud rollouts, vendor platform consolidation, and confidential-computing adoption keep demand for scalable controls high. Broadcom's integration of VMware illustrates how bundled private-cloud subscriptions can lift both revenue and margins, underscoring enterprises' preference for unified stacks. At the same time, AI-driven attack-surface discovery pushes micro-segmentation from an optional add-on to a baseline requirement. Hardware-assisted defenses, such as Intel VT-rp, show that silicon innovation is now an essential layer in the virtualization security market as threat actors target hypervisor memory translation paths.

Global Virtualization Security Market Trends and Insights

Hybrid and Multi-Cloud Adoption Surge

Broadcom lifted VMware Cloud Foundation revenue to USD 21.5 billion in fiscal 2024, proving that customers want a single control plane across private and public clouds. As workloads hop among environments, east-west visibility becomes as critical as perimeter defense. Azure Confidential VMs show how trusted execution environments can preserve encryption in use while enabling seamless migration. Identity-centric and zero-trust models now replace traditional perimeter zoning because policies have to follow each workload, not each subnet. Pay-as-you-go consumption also keeps enterprises from stalling modernization projects when budgets tighten.

Strict Data-Protection Regulations (GDPR, CCPA, DPDPA)

India's new DPDPA rules mandate explicit purpose limitation and cross-border transfer restrictions that must be embedded into virtualization blueprints. Similar mandates in Malaysia and Vietnam drive demand for built-in audit trails and encryption key governance. Healthcare systems adopt HIPAA-compliant virtual workspaces, keeping ePHI off personal devices while allowing remote clinicians to work securely. Penalties for non-compliance now outweigh license fees, so the virtualization security market embeds privacy-by-design principles into every release.

High Up-Front Cost of Specialized Security Appliances

KubeVirt and OpenShift are evaluated as cost-effective alternatives to traditional vSphere licenses, especially after Broadcom's pricing changes. Surveys show 78% of small businesses lack antivirus for virtual servers, while 48% run without proper firewalls due to budget limits. Trusted-chip supply disruptions inflate appliance costs, delaying refresh cycles.

Other drivers and restraints analyzed in the detailed report include:

- Explosive VM and Container Workload Growth in Edge Data-Centers

- AI-Driven Attack-Surface Discovery Boosting Micro-Segmentation Demand

- Shortage of Skilled Virtual-Security Engineers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for 64.2% of the virtualization security market share in 2024 as enterprises gravitated toward integrated suites rather than piecemeal tools. Palo Alto Networks' Next-Generation Security ARR climbed 34% to USD 4.8 billion, a clear indicator that platformization resonates with buyers. Services replicate this momentum, growing at 19.1% CAGR because intricate hybrid designs require third-party expertise. Vendors like Fortinet fold acquisitions such as Lacework into a single fabric, shrinking tool sprawl, and locking customers into longer contracts. The virtualization security market size is, therefore, skewing toward bundled offerings that combine CNAPP, micro-segmentation, and zero-trust network access in one license.

Smaller enterprises benefit from SaaS consumption patterns that remove up-front appliance costs and staffing burdens, democratizing access. As a result, service providers target this under-penetrated tier with off-the-shelf deployment blueprints and monthly subscription pricing.

Hardware/Server Virtualization retained a 46.3% share in 2024 owing to its foundational role in VM isolation. Intel VT-rp exemplifies hardening at the silicon layer, obstructing paging structure tampering and reinforcing hypervisor trust boundaries. Yet, Network and SD-WAN Virtualization will outpace all layers, registering an 18.3% CAGR as AI-native fabrics like Cisco Hypershield embed kernel-level policy enforcement across distributed pods. The virtualization security market size for network layers will widen further when OT factories virtualize sensors and PLCs, requiring deterministic but secure traffic flows.

Virtualization Security Market is Segmented by Component (Solutions and Services), Virtualization Layer (Hardware/Server Virtualization, Application Virtualization, and More), Deployment Mode (On-Premise, Private Cloud, and More), End-User Industry (IT and Telecom, BFSI, Healthcare and Life Sciences, and More), Organization Size (Large Enterprises and Small and Medium Enterprises), and Geography.

Geography Analysis

North America contributed 35.26% of revenue in 2024, sustained by early zero-trust adoption and strict sectoral mandates such as HIPAA and CCPA. Vendors concentrate R&D and channel ecosystems in the United States, shortening feedback cycles and quickening feature delivery.

Asia-Pacific is the high-velocity engine, set to grow 18.1% annually through 2030. India's DPDPA and Malaysia's stricter data officer obligations nudge even midsize firms to adopt audit-ready virtualization stacks. Manufacturing clusters across China, Vietnam, and Thailand virtualize shop-floor workloads, driving edge-security shipments.

Europe keeps a steady pace under GDPR. The Schrems II ruling amplifies interest in confidential-computing attestation to satisfy data transfer conditions. Meanwhile, GCC nations channel oil-windfall budgets into smart-city and e-government projects that rely on secure virtualized clouds, creating a nascent but strategic opportunity for specialists.

- VMware Inc. (Broadcom Inc.)

- Trend Micro Inc.

- Sophos Ltd.

- Bitdefender LLC

- Palo Alto Networks Inc.

- Fortinet Inc.

- Check Point Software Technologies Ltd.

- Cisco Systems Inc.

- Juniper Networks Inc.

- Kaspersky Lab

- McAfee LLC

- IBM Corporation

- Microsoft Corporation

- Citrix Systems Inc.

- Red Hat Inc.

- Nutanix Inc.

- Parallels International GmbH

- Sangfor Technologies Inc.

- Guardicore (Akamai Technologies)

- Illumio Inc.

- Acronis International GmbH

- Symantec Enterprise Division (Broadcom)

- Hillstone Networks

- Radware Ltd.

- Tenable Holdings Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hybrid and multi-cloud adoption surge

- 4.2.2 Strict data-protection regulations (GDPR, CCPA, DPDPA)

- 4.2.3 Explosive VM and container workload growth in edge data centers

- 4.2.4 Hypervisor licence inflation pushing open-source hypervisors

- 4.2.5 AI-driven attack-surface discovery boosting micro-segmentation demand

- 4.2.6 Confidential-computing attestation becoming a procurement criterion

- 4.3 Market Restraints

- 4.3.1 High up-front cost of specialised security appliances

- 4.3.2 Shortage of skilled virtual-security engineers

- 4.3.3 VM sprawl complicating zero-trust enforcement

- 4.3.4 Quantum-ready encryption premiums delaying purchase cycles

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Virtualization Layer

- 5.2.1 Hardware/Server Virtualization

- 5.2.2 Application Virtualization

- 5.2.3 Network and SD-WAN Virtualization

- 5.2.4 Storage Virtualization

- 5.3 By Deployment Mode

- 5.3.1 On-Premise

- 5.3.2 Private Cloud

- 5.3.3 Public Cloud

- 5.3.4 Hybrid Cloud

- 5.4 By End-user Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Government and Defense

- 5.4.5 Retail and E-Commerce

- 5.4.6 Manufacturing

- 5.4.7 Other End-user Industries

- 5.5 By Organization Size

- 5.5.1 Large Enterprises

- 5.5.2 Small and Medium Enterprises (SMEs)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Malaysia

- 5.6.4.6 Singapore

- 5.6.4.7 Australia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 VMware Inc. (Broadcom Inc.)

- 6.4.2 Trend Micro Inc.

- 6.4.3 Sophos Ltd.

- 6.4.4 Bitdefender LLC

- 6.4.5 Palo Alto Networks Inc.

- 6.4.6 Fortinet Inc.

- 6.4.7 Check Point Software Technologies Ltd.

- 6.4.8 Cisco Systems Inc.

- 6.4.9 Juniper Networks Inc.

- 6.4.10 Kaspersky Lab

- 6.4.11 McAfee LLC

- 6.4.12 IBM Corporation

- 6.4.13 Microsoft Corporation

- 6.4.14 Citrix Systems Inc.

- 6.4.15 Red Hat Inc.

- 6.4.16 Nutanix Inc.

- 6.4.17 Parallels International GmbH

- 6.4.18 Sangfor Technologies Inc.

- 6.4.19 Guardicore (Akamai Technologies)

- 6.4.20 Illumio Inc.

- 6.4.21 Acronis International GmbH

- 6.4.22 Symantec Enterprise Division (Broadcom)

- 6.4.23 Hillstone Networks

- 6.4.24 Radware Ltd.

- 6.4.25 Tenable Holdings Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment