|

시장보고서

상품코드

1850272

신경보철 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Neuroprosthetics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

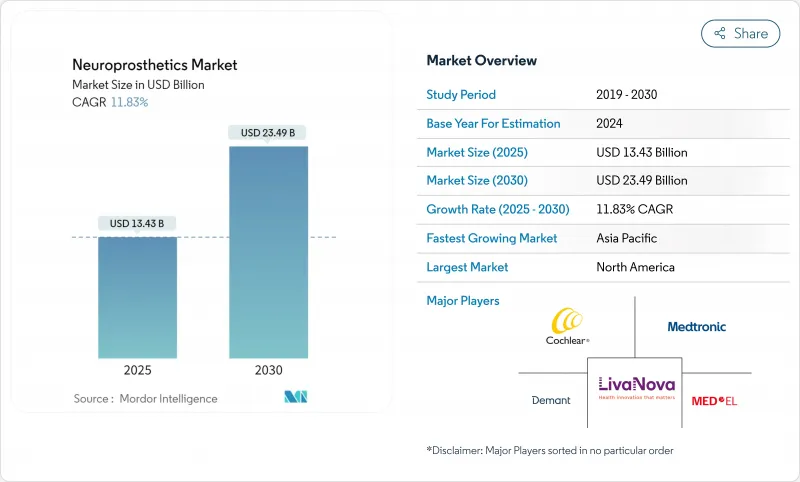

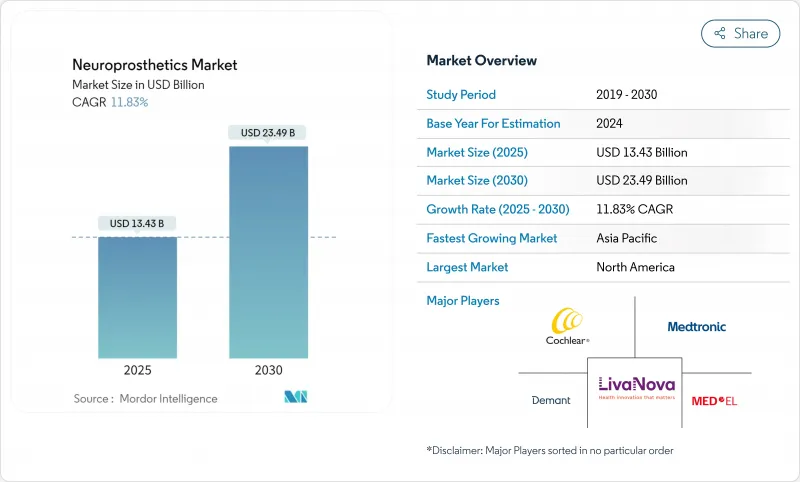

신경보철 시장은 2025년에 134억 3,000만 달러에 이를것으로 예측되며, 2030년에는 234억 9,000만 달러로 성장할 전망입니다.

이러한 급속한 확장은 개방형 자극 시스템에서 실시간으로 치료를 미세 조정하는 폐쇄형 적응 플랫폼으로의 전환을 반영합니다. 소형화된 전자기기, 유연한 생체재료, 기기 내 인공지능 알고리즘이 결합되어 이전 세대보다 수명이 길면서 수술 재수술률을 낮추는 내구성 있는 임플란트를 제공합니다. 2024년 이후 FDA 혁신 의료기기 지정이 증가하고, 신경조절 시술에 대한 메디케어 적용 범위가 확대되며, 운동·감각·정신과적 적응증 전반에 걸친 임상 증거가 축적되면서 시장 도입이 더욱 가속화되고 있습니다. 2023년 이후 연평균 14억 달러 규모의 벤처 캐피털 유입은 마비 및 중증 우울증 분야의 미충족 수요를 타깃으로 하는 혁신적인 뇌-컴퓨터 인터페이스 개발을 지속적으로 지원하며, 신경의학 보철 시장 전반의 장기적 수요를 강화하고 있습니다.

세계의 신경보철 시장 동향 및 인사이트

신경 질환 유병률 상승

65세 이상 인구에서 뇌졸중 및 파킨슨병 발병률이 지속적으로 증가함에 따라 다중 모드 신경보철 치료에 대한 수요가 지속되고 있습니다. 노화와 관련된 뇌졸중 및 파킨슨병 추세는 연간 환자 수를 증가시키며, 운동, 인지 및 감각 장애를 동시에 해결하는 다중 모드 신경보철 치료에 대한 지속적인 수요를 촉진합니다. 반응성 신경자극에 대한 6년간 추적 관찰 데이터는 치료 저항성 간질에서 발작 빈도가 중앙값 기준 82% 감소했음을 보여주며, 만성적 효능을 입증합니다. 건강경제 모델은 8년 이상의 기기 수명이 초기 비용 증가를 상쇄함을 보여주어, 신경보철 시장 전반에서 신경보철 장치를 최후의 수단이 아닌 일차적 치료 옵션으로 자리매김하게 합니다.

감각신경성 난청 발생률 증가

도시 소음 노출과 산업화로 인공와우 이식 수요가 가속화되는 가운데, 그래핀 전도체를 탑재한 차세대 양측 전극 배열은 잔존 청력을 보존하고 공간 음향 인지 능력을 향상시킵니다. 소아 조기 이식 프로그램은 개별 기기 업그레이드 주기를 연장하여 신경보철 시장 내 평생 가치 풀을 확대합니다. 스마트폰 연동 음향 처리 소프트웨어는 이제 개인 맞춤형 음향 프로필을 제공하여 프리미엄 인공와우 시스템을 차별화합니다.

이식 장치의 높은 구입 및 수술 비용

이식형 펄스 발생기 가격(24,000-60,000달러)과 100,000달러를 초과하는 시술 비용은 특히 신경외과 센터가 부족한 지역에서 접근성을 제한합니다. 전 세계적으로 다학제적 전문성을 갖춘 시설은 200곳에 불과하여, 새로운 임대 또는 위험 분담 결제 옵션이 확대되기 전까지 저소득 지역으로의 신경보철 시장 확산이 병목 현상을 겪고 있습니다.

부문 분석

폐쇄 루프 시스템은 생리학적 피드백을 포착하여 자극을 자동 조정하며, 2030년까지 연평균 12.31% 성장률을 기록할 전망입니다. 출력 장치는 성숙한 심부 뇌, 척수 및 인공 와우 프랜차이즈 덕분에 2024년 신경 보철 시장 점유율의 56.54%를 여전히 차지했습니다. 대뇌 피질 의도를 해독하는 입력 인터페이스는 이제 마비된 사용자를 외부 로봇 공학과 연결하여 신경 보철 시장의 접근 가능한 기반을 확대하고 있습니다. 지속적인 알고리즘 개선은 진료 방문을 줄이고 우수한 장기적 결과를 지원하여 적응형 플랫폼을 예측 기간 동안 전략적 성장 동력으로 만듭니다.

감지와 자극 기능을 단일 임플란트 내부에 통합한 양방향 설계는 이 분야가 통합 정밀의학 도구로 진화하고 있음을 보여줍니다. 메드트로닉의 인셉티브 척추 자극기와 같은 상용 제품은 실시간 복합 활동 전위 추적을 통해 개별화된 치료 창 내에서 진통 효과를 고정시킵니다. 병원 시스템이 재프로그래밍 작업량을 최소화하는 장치를 선호함에 따라 적응형 장치는 처방 목록 선호도를 얻으며 전체 신경보철 시장 확장에 미치는 영향력을 확대하고 있습니다.

이식형 하드웨어는 2024년 매출의 63.81%를 차지했으나, 제조사가 기존 기기에 머신러닝 분석을 추가함에 따라 AI 기반 소프트웨어 모듈은 연평균 12.84% 성장률을 보이고 있습니다. 외부 웨어러블 기기는 고대역폭 피질 기록을 처리하여 신호 정확도를 유지하면서도 이식 장치의 복잡성을 줄입니다. 예측 유지보수 대시보드는 배터리 소모 및 임피던스 드리프트를 경고하여 신경보철 시장 전반의 예정되지 않은 진료 예약을 감소시킵니다.

규제 프레임워크는 이제 고비용 수술 수정 없이도 시판 후 소프트웨어 업그레이드를 허용하여 제품 수명 주기를 연장합니다. NeuroPace의 클라우드 연계 발작 분석은 디지털 차별화 제품으로의 전환을 보여줍니다. 머신러닝 기반 의료 기기에 대한 FDA의 향후 지침은 신경보철 시장 내에서 소프트웨어 구독을 반복 수익 채널로 더욱 공고히 할 것입니다.

지역 분석

북미는 2024년 글로벌 매출의 43.56%를 차지했으며, 이는 기능적 신경외과 네트워크의 고밀도 분포, 폐쇄 루프 자극기에 대한 메디케어 지급 범위, 상용화 기간을 단축하는 FDA 혁신 의료기기(Breakthrough Device) 승인 경로 등에 힘입은 결과입니다. 미국 병원 그룹들은 현재 객관적인 이동성 또는 발작 감소 성과에 따라 지급 단계를 연계하는 위험 분담 계약을 협상 중이며, 이는 실제 임상 증거(RWE) 생성을 가속화하고 신경보철 시장 성장을 지속적으로 촉진하고 있습니다.

유럽은 사용자 안전을 강화하면서도 범지역적 CE 인증 시장 진입 경로를 유지하는 엄격한 의료기기 규정 기준을 적용합니다. 독일 등 국가들은 검증 가능한 삶의 질 향상을 제공하는 임플란트에 보상하는 보건기술평가(HTA) 필터를 적용하며, 이러한 증거 중심 접근법은 지속 가능한 채택 곡선을 조성합니다. EU 지원 호라이즌 유럽 컨소시엄은 생분해성 전극 및 적응형 피질 인터페이스에 투자하여 지역 내 혁신이 직접적으로 지역 신경보철 시장 파이프라인에 반영되도록 합니다.

아시아태평양 지역은 2030년까지 연평균 13.71% 성장률로 가장 빠르게 성장하는 클러스터로 전망됩니다. 중국 국가의약품감독관리국은 침습적 뇌-컴퓨터 인터페이스 이식에 대해 902달러의 보험급여 코드를 시범 운영 중이며, 공업정보화부는 신경 인터페이스를 전략적 신흥 산업으로 지정했습니다. 일본과 한국은 첨단 반도체 공급망을 활용해 비용 효율적인 임플란트 제조를 실현하는 반면, 인도는 1선 도시를 넘어 장치 접근성을 확대하는 신경 재활 센터를 확장 중입니다. 이러한 움직임들은 10년 말까지 보다 민주화된 신경보철 시장 환경을 조성할 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 신경계 질환의 유병률 상승

- 감각신경성 난청 발생률 상승

- 기술 소형화 및 생체재료 발전

- 신경조절 임플란트에 대한 보험 적용 확대

- 임상 파이프라인 진입 중인 바이오하이브리드 신경 인터페이스

- 인간-기계 증강을 위한 군사 및 우주 기관 자금 지원

- 시장 성장 억제요인

- 임플란트의 높은 구입 및 수술 비용

- 약리학적/물리적 재활 대체 수단의 가용성

- 전문 기능신경외과 인력 부족

- 선택적 인지 능력 향상에 대한 윤리적·규제적 장벽

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(가치, 2021-2030년)

- 유형별

- 입력 신경보철

- 출력 신경보철

- 폐쇄 루프/적응형 신경보철

- 컴포넌트별

- 이식형

- 외부 착용형

- 소프트웨어 및 알고리즘

- 기술별

- 뇌심부자극요법(DBS)

- 척수자극요법(SCS)

- 미주신경자극(VNS)

- 피질 및 말초 신경 자극

- 용도별

- 운동장애(파킨슨병, 본태성 진전 등)

- 감각 상실(청각, 시각)

- 인지 및 정신질환(알츠하이머병, 우울증, PTSD)

- 만성 통증과 간질

- 최종 사용자별

- 병원

- 전문의 및 재활 클리닉

- 재택 케어 및 외래 진료

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- Boston Scientific Corporation

- Cochlear Limited

- Demant A/S

- LivaNova PLC

- MED-EL Medical Electronics

- Medtronic PLC

- Sonova Holding AG

- Second Sight Medical Products

- Cyberonics Inc.(VNS Therapy)

- BrainGate Company

- Nevro Corp.

- Synchron Inc.

- Neuralink Corporation

- Blackrock Neurotech

- Pixium Vision SA

- Axonics Modulation Technologies

- BlueWind Medical

- MicroTransponder Inc.

- NeuroPace Inc.

제7장 시장 기회와 장래의 전망

HBR 25.11.19The Neuroprosthetics market stands at USD 13.43 billion in 2025 and is projected to reach USD 23.49 billion by 2030, reflecting an 11.83% CAGR.

This swift expansion mirrors the transition from open-loop stimulation systems to closed-loop adaptive platforms that fine-tune therapy in real time. Miniaturized electronics, flexible biomaterials, and on-device artificial-intelligence algorithms now merge to deliver durable implants that outlast earlier generations while lowering surgical revision rates. Heightened FDA Breakthrough Device designations since 2024, broader Medicare coverage for neuromodulation procedures, and growing clinical evidence across motor, sensory, and psychiatric indications further unlock adoption. Venture capital inflows, averaging USD 1.4 billion per year since 2023, continue to fund novel brain-computer interfaces that target unmet needs in paralysis and severe depression, strengthening long-term demand across the Neuroprosthetics market.

Global Neuroprosthetics Market Trends and Insights

Rising Prevalence of Neurological Disorders

Stroke and Parkinson's incidence continues to rise among populations over 65, prompting sustained demand for multimodal neuroprosthetic therapies . Age-linked stroke and Parkinson's disease trends raise annual caseloads and prompt sustained demand for multi-modal neuroprosthetic therapies that address motor, cognitive, and sensory deficits concurrently. Six-year follow-up data on responsive neurostimulation show an 82% median seizure cut in treatment-resistant epilepsy, underscoring chronic efficacy. Health-economic models demonstrate that device longevity beyond eight years offsets higher up-front expenses, positioning neuroprosthetics as first-line rather than last-resort options across the Neuroprosthetics market.

Escalating Incidence of Sensorineural Hearing Loss

Urban noise exposure and industrialization accelerate cochlear-implant uptake, while next-generation bilateral electrode arrays equipped with graphene conductors preserve residual hearing and improve spatial sound perception . Pediatric early-implant programs lengthen individual device-upgrade cycles, expanding the lifetime value pool within the Neuroprosthetics market. Smartphone-linked sound-processing software now personalizes acoustic profiles, differentiating premium cochlear systems.

High Acquisition and Surgical Costs of Implants

Implantable pulse generators priced USD 24,000-60,000 and procedure bills surpassing USD 100,000 restrict access, especially where neurosurgical centers remain sparse. Only 200 facilities worldwide host the multidisciplinary expertise required, bottlenecking diffusion of the Neuroprosthetics market into lower-income regions until novel leasing or risk-sharing payment options scale.

Other drivers and restraints analyzed in the detailed report include:

- Technological Miniaturization and Biomaterial Advances

- Expanding Reimbursement for Neuromodulation Implants

- Availability of Pharmacological / Physical Rehabilitation Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Closed-loop systems capture physiological feedback to auto-adjust stimulation, driving a 12.31% CAGR through 2030. Output devices still controlled 56.54% of the Neuroprosthetics market in 2024 thanks to mature deep brain, spinal cord, and cochlear franchises. Input interfaces that decode cortical intent now bridge paralyzed users to external robotics, widening the Neuroprosthetics market addressable base. Continuous algorithm refinement reduces clinic visits and supports superior long-term outcomes, making adaptive platforms the strategic growth engine over the forecast window.

Bidirectional designs that merge sensing and stimulation inside one implant underscore the sector's evolution toward integrated precision-medicine tools. Commercial launches such as Medtronic's Inceptiv spinal stimulator showcase real-time compound-action-potential tracking that locks analgesia within individualized therapeutic windows . As hospital systems favor devices that minimize re-programming workloads, adaptive units gain formulary preference, amplifying their influence on overall Neuroprosthetics market expansion.

Implantable hardware captured 63.81% revenue in 2024, yet AI-driven software modules are growing at 12.84% CAGR as manufacturers layer machine-learning analytics atop legacy devices. External wearables process high-bandwidth cortical recordings, reducing implant complexity while sustaining signal fidelity. Predictive-maintenance dashboards flag battery depletion and impedance drift, lowering unscheduled clinic appointments across the Neuroprosthetics market.

Regulatory frameworks now permit post-market software upgrades outside costly surgical revisions, extending product life cycles. NeuroPace's cloud-linked seizure analytics illustrate the pivot toward digitally differentiated offerings; incoming FDA guidance on machine-learning-enabled medical devices should further cement software subscriptions as recurring revenue channels within the Neuroprosthetics market.

The Neuroprosthetics Market Report Segments the Industry Into by Type (Output Neuroprosthetics, and More), by Component (Implantable Device, and More), by Technique (Deep Brain Stimulation, and More), by Application (Motor Disorders, and More), End User (Hospitals, and More) and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America delivered 43.56% of 2024 global revenue, supported by dense functional-neurosurgery networks, Medicare payment coverage for closed-loop stimulators, and FDA Breakthrough Device pathways that shorten commercialization time. United States hospital groups now negotiate risk-share contracts that tie payment tranches to objective mobility or seizure-reduction milestones, accelerating real-world evidence generation and fueling continued Neuroprosthetics market growth.

Europe follows with stringent Medical Device Regulation standards that reinforce user safety while preserving a pan-regional CE-mark route to market. Countries such as Germany apply health-technology-assessment filters that reward implants delivering verifiable quality-of-life gains; this evidence-centric stance nurtures sustainable adoption curves. EU-funded Horizon Europe consortia invest in biodegradable electrodes and adaptive cortical interfaces, ensuring indigenous innovations feed directly into regional Neuroprosthetics market pipelines.

Asia-Pacific is the fastest-growing cluster, projected at 13.71% CAGR through 2030. China's National Medical Products Administration is piloting USD 902 reimbursement codes for invasive brain-computer-interface placements, while the Ministry of Industry and Information Technology lists neural interfaces as a strategic emerging industry. Japan and South Korea translate advanced semiconductor supply chains into cost-efficient implant manufacturing, whereas India scales neuro-rehabilitation centers that extend device access beyond Tier-1 cities. Together these moves support a more democratized Neuroprosthetics market landscape by decade's end.

- Abbott Laboratories

- Boston Scientific

- Cochlear

- Demant

- LivaNova

- MED-EL

- Medtronic

- Sonova

- Second Sight Medical Products

- Cyberonics Inc. (VNS Therapy)

- BrainGate Company

- Nevro

- Synchron

- Neuralink Corporation

- Blackrock Neurotech

- Pixium Vision SA

- Axonics Modulation Technologies

- BlueWind Medical

- MicroTransponder Inc.

- NeuroPace

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of neurological disorders

- 4.2.2 Escalating incidence of sensorineural hearing loss

- 4.2.3 Technological miniaturisation & biomaterial advances

- 4.2.4 Expanding reimbursement for neuromodulation implants

- 4.2.5 Bio-hybrid neural interfaces entering clinical pipelines

- 4.2.6 Military & space-agency funding for human-machine augmentation

- 4.3 Market Restraints

- 4.3.1 High acquisition & surgical costs of implants

- 4.3.2 Availability of pharmacological / physical rehabilitation alternatives

- 4.3.3 Shortage of specialised functional-neurosurgery talent

- 4.3.4 Ethical & regulatory hurdles around elective cognitive enhancement

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, 2021-2030)

- 5.1 By Type

- 5.1.1 Input Neuroprosthetics

- 5.1.2 Output Neuroprosthetics

- 5.1.3 Closed-loop/Adaptive Neuroprosthetics

- 5.2 By Component

- 5.2.1 Implantable Device

- 5.2.2 External Wearable Unit

- 5.2.3 Software & Algorithms

- 5.3 By Technique

- 5.3.1 Deep Brain Stimulation (DBS)

- 5.3.2 Spinal Cord Stimulation (SCS)

- 5.3.3 Vagus Nerve Stimulation (VNS)

- 5.3.4 Cortical & Peripheral Nerve Stimulation

- 5.4 By Application

- 5.4.1 Motor Disorders (Parkinson's, Essential Tremor, etc.)

- 5.4.2 Sensory Loss (Auditory, Visual)

- 5.4.3 Cognitive & Psychiatric Conditions (Alzheimer's, Depression, PTSD)

- 5.4.4 Chronic Pain & Epilepsy

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Specialty & Rehabilitation Clinics

- 5.5.3 Home-care & Ambulatory Settings

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global overview, Market overview, Core segments, Financials, Strategic information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Boston Scientific Corporation

- 6.3.3 Cochlear Limited

- 6.3.4 Demant A/S

- 6.3.5 LivaNova PLC

- 6.3.6 MED-EL Medical Electronics

- 6.3.7 Medtronic PLC

- 6.3.8 Sonova Holding AG

- 6.3.9 Second Sight Medical Products

- 6.3.10 Cyberonics Inc. (VNS Therapy)

- 6.3.11 BrainGate Company

- 6.3.12 Nevro Corp.

- 6.3.13 Synchron Inc.

- 6.3.14 Neuralink Corporation

- 6.3.15 Blackrock Neurotech

- 6.3.16 Pixium Vision SA

- 6.3.17 Axonics Modulation Technologies

- 6.3.18 BlueWind Medical

- 6.3.19 MicroTransponder Inc.

- 6.3.20 NeuroPace Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment