|

시장보고서

상품코드

1910450

파이로젠 시험 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Global Pyrogen Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

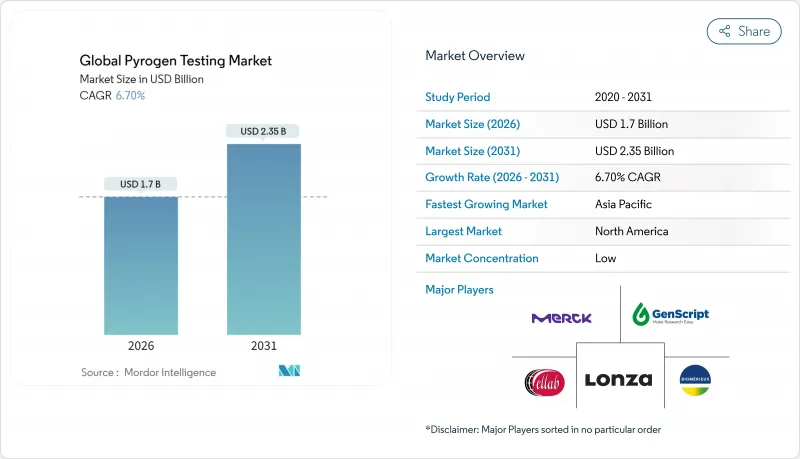

2026년 파이로젠 시험 시장 규모는 17억 달러로 추정되며, 2025년 15억 9,000만 달러에서 성장하여, 2031년에는 23억 5,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지는 CAGR 6.7%로 성장할 전망입니다.

지속적인 성장은 생물학적 제제의 생산 증가, 재조합 분석에 대한 강력한 규제 지원, 품질 관리(QC) 서비스의 아웃소싱으로의 광범위한 전환으로 발생됩니다. 기업은 수동 개입을 줄이고 오류를 줄여 제품 출시를 가속화하기 위해 자동화를 채택합니다. 규제 당국은 투구게 개체군을 보호하면서 공급의 연속성을 보장하기 위해 동물을 사용하지 않는 시험을 승인합니다. 아시아태평양의 제조업체는 고처리량 능력을 추가하여 새로운 수요의 창출을 도모하고 있습니다. 한편 북미는 QC 연구소의 최대 설치 기반을 유지하고 있습니다. 지속적인 백신 자금 조달, 확대하는 세포 및 유전자 치료 파이프라인, 비용 효율적인 마이크로플루이딕스 키트가 파이로젠 시험 시장의 장기적인 확대를 뒷받침하고 있습니다.

세계의 파이로젠 시험 시장의 동향 및 전망

생물학적 및 바이오시밀러 파이프라인의 급속한 성장

2024년 생물학적 제제의 제조 능력은 1,650만 리터를 돌파하였으며, 거의 대부분의 신규 플랜트는 일회용 시스템용으로 가동을 개시하였습니다. 이로 인해 품질 관리 사이클의 빈도 증가가 요구됩니다. 고분자 의약품은 엔도톡신 이외의 발열 경로를 활성화시킬 수 있으며, 기업은 LAL 분석 이외에 단핵구 기반 검사법을 병용하는 경향이 있습니다. 세포 및 유전자 치료 후보품에 관한 FDA의 개정 가이던스에서는 재료 매개 파이로젠 시험이 지정되어, 품질 관리 연구소 내의 검사 메뉴가 확대되고 있습니다. 바이오시밀러 개발 기업은 참조 로트를 여러 사이트에 복제하기 때문에 각 배치의 릴리스 시에 파이로젠 클리어런스가 요구되는 배치 릴리스 이벤트가 증가하고 있습니다. 유럽에서는 2026년까지 토끼를 이용한 시험을 MAT(단핵구 활성화 분석)로 대체하도록 의무화되면서 다양한 분석에 대한 수요를 더욱 밀어 올리고 있습니다. 종합적으로 볼 때, 생물학적 기세는 파이로젠 시험 시장에 지속적인 볼륨 성장을 가져올 전망입니다.

위탁개발생산의 아웃소싱 확대

세계의 CDMO(위탁개발생산)는 다국적 제약기업용으로 증가하는 충전, 포장 공정 및 최종 릴리스 분석을 처리하고 있습니다. IQVIA, 써모피셔, 우시앱텍과 같은 주요 기업들은 파이로젠 테스트를 통합 서비스 계약에 통합하여 장비 가동률 안정화와 자동화 설비 업그레이드 자금을 도모하고 있습니다. 찰스리버의 Nexus 플랫폼(1회당 120검체 처리 가능)은 단독 사내 벤치에서는 실현할 수 없는 처리량 경제성을 외부 위탁 허브가 어떻게 활용하고 있는지를 보여줍니다. 아시아의 CDMO는 임금의 이점을 통해 이러한 효율성을 더욱 높여 재조합 분석 및 MAT(단핵구 활성화 분석) 능력에 재투자할 수 있습니다. 이는 지속가능성 목표를 추구하는 서유럽의 고객층에 대응하고 있습니다. 그 결과, 아웃소싱은 파이로젠 시험 시장의 세계적인 확대를 촉진하는 동시에 스폰서의 단가 비용을 압축합니다.

투구게 추출액의 공급 불안정성

야생 대서양투구게의 채취 할당량은 여전히 적은 상황임에도 불구하고 실제 채취량은 항상 할당량을 상회하고 있으며, 보전상의 우려가 높아지고 있습니다. 갑작스런 채취 규제 강화는 LAL 시약의 공급을 정체시키고 백신 공급망을 위협할 수 있습니다. 소규모 바이오텍 기업은 가격 급등의 영향에 가장 먼저 노출되며 대량 계약을 맺는 대기업과의 비용 격차가 확대됩니다. 비정상적인 날씨와 서식지 상실은 여러 시즌에 걸쳐 위험을 초래할 수 있으며, 허리케인 1개만으로 델라웨어만 해안에 있는 수많은 사육 게가 멸종될 수 있습니다. 이러한 리스크는 rFC(재조합 인자 C)로의 포트폴리오 이행을 가속화하지만, 단기적으로는 불확실성을 증대시켜, 파이로젠 시험 시장의 성장을 억제하는 요인이 될 수 있습니다.

부문 분석

계측기기는 2031년까지 연평균 복합 성장률(CAGR) 7.86%를 기록할 전망으로 전체 제품 라인 중 가장 높은 성장을 보이고 있습니다. 이 성장은 제약 업계의 데이터 무결성 확보와 인력 감축 추진에 의해 뒷받침되며 자동 감사 추적을 생성하는 폐쇄 시스템 리더가 선호되고 있습니다. 카트리지식 유닛은 시약 팩을 통합하여 희석 오차를 줄이고 분석자의 작업 시간을 85% 줄입니다. 키트 및 시약은 2025년 매출의 44.08%를 차지하였으며 이는 공급업체의 수익성을 지원하는 소모품 모델이 지속되고 있음을 보여줍니다. CDMO가 턴키 제공에 서비스 대가형 엔도톡신 패널을 추가함에 따라 서비스 분야는 꾸준히 성장하고 있습니다.

바코드 추적 기능이 있는 휴대용 분광광도계는 현장에서 릴리스가 가능하여 로트 처리 시간을 최대 6시간 단축할 수 있습니다. 마이크로유체 키트는 기존의 튜브비로 용해액을 95% 절감했으며, 이 재료 효율은 지속가능성 부문에서 높은 평가를 받고 있습니다. 최종 사용자는 자본 비용이 급증하고 있음에도 불구하고 새로운 리더의 도입 예산을 결정하는 주된 이유로 검증을 용이하게 하고 샘플 처리 능력을 향상시키는 점을 들고 있습니다. 이러한 추세가 결합되어 업그레이드 사이클이 강화되고 도입 범위가 확대되어 파이로젠 시험 시장의 기세가 지속되고 있습니다.

지역별 분석

북미는 2025년 매출액의 42.05%를 차지하였고 FDA에 의한 rFC의 신속한 승인과 바이오텍 기업 본사의 밀집이 성장에 기여했습니다. 이 지역은 자동화 보급의 성숙도와 확립된 시험문화의 혜택을 받는 한편, 높은 기저효과로 인해 성장률은 둔화 추세에 있습니다. 반면 아시아태평양은 8.18%의 연평균 복합 성장률(CAGR)로 확대될 것으로 전망됩니다. 중국과 인도에서 시행되는 바이오 의약품 메가플랜트의 건설이 성장의 기반입니다. 인도의 생산연동형 인센티브와 중국의 성 수준의 보조금에 의한 까다로운 지원이 최첨단 품질관리(QC)실에 대한 자금 조달을 뒷받침해 시약 수요의 증가로 이어지고 있습니다.

유럽은 안정적인 성장을 유지하고 있으며 대체 어세이의 조기 도입과 EDQM(유럽의약품품질위원회)의 크로스보더 기준이 원동력이 되고 있습니다. 엄격한 동물복지법에 의해 타지역보다 조기에 MAT(단핵구 활성화 분석)와 rFC(재조합 인자 C)의 검증을 추진하고 있습니다. 브렉시트(영국의 EU 탈퇴)에 의해 행정 수속이 증가했지만, 무역에 실질적인 지장은 없으며, 영국과 EU의 어세이 제조업체는 상호 인증을 유지하고 있습니다. 지역적 다양화가 함께 세계 수요의 균형을 맞추고, 파이로젠 시험 시장 전체의 회복력을 강화하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 바이오로직 및 바이오시밀러 파이프라인의 급속한 성장

- 위탁개발생산의 아웃소싱의 확대

- 규제 당국의 재조합 인자 C(rFC) 분석 승인

- 환경 보호를 배경으로 한 동물 유래 성분 미사용 엔도톡신 검출법으로의 이행

- 마이크로플루이딕스 기술에 기반한 신속한 파이로젠 검출 플랫폼

- 백신, 세포 및 유전자 치료의 제조량 급증

- 억제요인

- 투구게 용해액의 공급 변동성

- 기존 품질 관리 프로토콜을 rFC로 전환할 때 발생하는 불확실성

- 연구소 간 차이나는 단핵구 활성화 분석 결과

- 자동 엔도톡신 분석기의 높은 초기 비용

- 가치 및 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측(금액)

- 제품별

- 키트 및 시약

- 서비스

- 기기

- 시험 유형별

- LAL 시험

- 토끼 파이로젠 시험

- 단핵구 활성화 분석

- 기타 시험 유형별

- 최종 사용자별

- 제약 및 생명공학 기업

- 의료기기 제조업체

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 점유율 분석

- 기업 프로파일

- Associates of Cape Cod Inc.

- bioMerieux SA

- Charles River Laboratories Inc.

- Ellab A/S

- GenScript Biotech

- Lonza Group

- Merck KGaA

- Thermo Fisher Scientific Inc.

- Fujifilm Wako Pure Chemical Corp.

- WuXi AppTec

- Eurofins Scientific

- Microcoat Biotechnologie GmbH

- Sotera Health(Nelson Labs)

- Sanquin

- Seikagaku Corporation

- Hyglos GmbH

- Toxin Technology Inc.

- Labor Dr. Merk & Kollegen

- Endosafe(Charles River)

제7장 시장 기회 및 미래 전망

CSM 26.02.04Pyrogen testing market size in 2026 is estimated at USD 1.7 billion, growing from 2025 value of USD 1.59 billion with 2031 projections showing USD 2.35 billion, growing at 6.7% CAGR over 2026-2031.

Sustained growth is shaped by rising biologics production, strong regulatory backing for recombinant assays, and a broad move toward outsourcing quality-control (QC) services. Companies adopt automation to cut manual intervention, reduce errors, and release products faster. Regulatory agencies are approving animal-free tests to protect horseshoe crab populations while securing supply continuity. Asia-Pacific manufacturers add high-throughput capacity, creating new demand pockets even as North America maintains the largest installed base of QC laboratories. Sustained vaccine funding, expanding cell- and gene-therapy pipelines, and cost-efficient microfluidic kits all reinforce the long-term expansion of the pyrogen testing market.

Global Pyrogen Testing Market Trends and Insights

Rapid Growth of Biologics & Biosimilars Pipeline

Biologic manufacturing capacity topped 16.5 million L in 2024, and new plants now open almost entirely with single-use systems requiring more frequent QC cycles. Large-molecule drugs can activate pyrogenic pathways beyond endotoxins, prompting firms to layer monocyte-based methods on top of LAL assays. Updated FDA guidance for cell- and gene-therapy candidates calls for material-mediated pyrogen checks, broadening test menus inside QC labs . Biosimilar sponsors replicate reference lots across many sites, multiplying batch release events that each demand pyrogen clearance. Europe's mandate to replace rabbit tests with MAT by 2026 further lifts demand for diversified assays. Altogether, biologics momentum injects consistent volume growth into the pyrogen testing market.

Expansion of Contract Research & Manufacturing Outsourcing

Global CDMOs handle rising volumes of fill-finish and final-release analytics for multinational drug makers. Leaders such as IQVIA, Thermo Fisher, and WuXi AppTec bundle pyrogen testing into integrated service contracts, which stabilizes instrumentation utilization and funds automation upgrades. Charles River's Nexus platform, capable of 120 samples per run, illustrates how outsourced hubs exploit throughput economics that single in-house benches cannot match. Asian CDMOs compound these efficiencies with wage advantages, enabling reinvestment in recombinant assays and MAT capacity to serve Western clientele pursuing sustainability goals. Consequently, outsourcing magnifies the global reach of the pyrogen testing market while compressing unit costs for sponsors.

Horseshoe-Crab Lysate Supply Volatility

Wild harvest quotas for Atlantic Limulus remain tight, yet real extraction volumes routinely over-shoot, raising conservation alarms. Any sudden clampdown could stall LAL reagent deliveries and jeopardize vaccine supply chains. Small-cap biotech firms face price spikes first, widening cost differentials versus larger peers with volume contracts. Severe weather events or habitat loss pose multi-season threats, and a single hurricane can wipe out thousands of breeding crabs along Delaware Bay. Such exposure accelerates portfolio shifts to rFC but adds near-term uncertainty that can temper growth in the pyrogen testing market.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Endorsement of Recombinant Factor C Assays

- Conservation-Driven Shift to Animal-Free Endotoxin Detection

- Microfluidic-Based Rapid Pyrogen Detection Platforms

- Surge in Vaccine & Cell-/Gene-Therapy Manufacturing Volumes

- Uncertainty During rFC Transition for Legacy QC Protocols

- Inter-Lab Variability of Monocyte Activation Test Results

- High Upfront Cost of Automated Endotoxin Analyzers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Instruments captured are on track to log an 7.86% CAGR to 2031, the fastest among all product lines. Their rise rests on pharma's push for data integrity and lean staffing, which favors closed-system readers that generate automatic audit trails. Cartridge-based units integrate reagent packs, alleviating dilution errors and trimming analyst time by 85%. Kits & Reagents still contributed 44.08% of 2025 revenues, underscoring the recurring consumables model that underwrites vendor profitability. The services slice grows steadily as CDMOs add fee-for-service endotoxin panels to turnkey offerings.

Portable spectrophotometers with barcode tracking now enable on-floor release, allowing facilities to shorten lot disposition by as much as six hours. Microfluidic kits use 95% less lysate than traditional tubes, a material efficiency welcomed by sustainability teams. End-users cite easier validation and higher sample throughput as core reasons to budget for new readers despite elevated capital prices. Combined, these preferences reinforce the upgrade cycle and widen adoption, sustaining momentum in the pyrogen testing market.

The Pyrogen Testing Market Report Segments the Industry Into by Product (Kits and Reagents, Services, Instruments), by Test Type (LAL Tests, Rabbit Pyrogen Test, Monocyte Activation Test, Other Test Types), by End User (Pharmaceutical and Biotechnology Companies, Medical Device Companies, Other End Users), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 42.05% of 2025 revenues, helped by the FDA's speedy acceptance of rFC and a dense cluster of biotech HQs. The region benefits from mature automation penetration and entrenched test culture but faces slower percentage growth due to its high base. Asia-Pacific, by contrast, is set to expand at an 8.18% CAGR, underpinned by Chinese and Indian build-outs of biologics mega-plants. Generous incentives from India's Production Linked scheme and China's provincial grants fund state-of-the-art QC labs, lifting reagent pull-through.

Europe holds steady growth, supported by early alternative-assay adoption and cross-border standards from EDQM. Stringent animal-welfare laws push firms to validate MAT and rFC earlier than peers elsewhere. Brexit added administrative filings but did not materially deter trade, with UK-EU assay producers retaining reciprocal certifications. Collectively, geographic diversification balances global demand and cements resilience across the pyrogen testing market.

- Associates of Cape Cod Inc.

- bioMerieux

- Charles River

- Ellab

- GenScript Biotech

- Lonza Group

- Merck

- Thermo Fisher Scientific

- Fujifilm Wako Pure Chemical Corp.

- WuXi App Tec

- Eurofins

- Microcoat Biotechnologie

- Sotera Health (Nelson Labs)

- Sanquin

- Seikagaku

- Hyglos GmbH

- Toxin Technology Inc.

- Labor Dr. Merk & Kollegen

- Endosafe (Charles River)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid growth of biologics & biosimilars pipeline

- 4.2.2 Expansion of contract research & manufacturing outsourcing

- 4.2.3 Regulatory endorsement of recombinant Factor C (rFC) assays

- 4.2.4 Conservation-driven shift to animal-free endotoxin detection

- 4.2.5 Microfluidic-based rapid pyrogen detection platforms

- 4.2.6 Surge in vaccine & cell-/gene-therapy manufacturing volumes

- 4.3 Market Restraints

- 4.3.1 Horseshoe-crab lysate supply volatility

- 4.3.2 Uncertainty during rFC transition for legacy QC protocols

- 4.3.3 Inter-lab variability of Monocyte Activation Test results

- 4.3.4 High upfront cost of automated endotoxin analyzers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD mn)

- 5.1 By Product

- 5.1.1 Kits and Reagents

- 5.1.2 Services

- 5.1.3 Instruments

- 5.2 By Test Type

- 5.2.1 LAL Tests

- 5.2.2 Rabbit Pyrogen Test

- 5.2.3 Monocyte Activation Test

- 5.2.4 Other Test Types

- 5.3 By End User

- 5.3.1 Pharmaceutical & Biotechnology Companies

- 5.3.2 Medical Device Companies

- 5.3.3 Other End Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Share Analysis

- 6.2 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.2.1 Associates of Cape Cod Inc.

- 6.2.2 bioMerieux SA

- 6.2.3 Charles River Laboratories Inc.

- 6.2.4 Ellab A/S

- 6.2.5 GenScript Biotech

- 6.2.6 Lonza Group

- 6.2.7 Merck KGaA

- 6.2.8 Thermo Fisher Scientific Inc.

- 6.2.9 Fujifilm Wako Pure Chemical Corp.

- 6.2.10 WuXi AppTec

- 6.2.11 Eurofins Scientific

- 6.2.12 Microcoat Biotechnologie GmbH

- 6.2.13 Sotera Health (Nelson Labs)

- 6.2.14 Sanquin

- 6.2.15 Seikagaku Corporation

- 6.2.16 Hyglos GmbH

- 6.2.17 Toxin Technology Inc.

- 6.2.18 Labor Dr. Merk & Kollegen

- 6.2.19 Endosafe (Charles River)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment