|

시장보고서

상품코드

1850288

매시브 MIMO 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Massive MIMO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

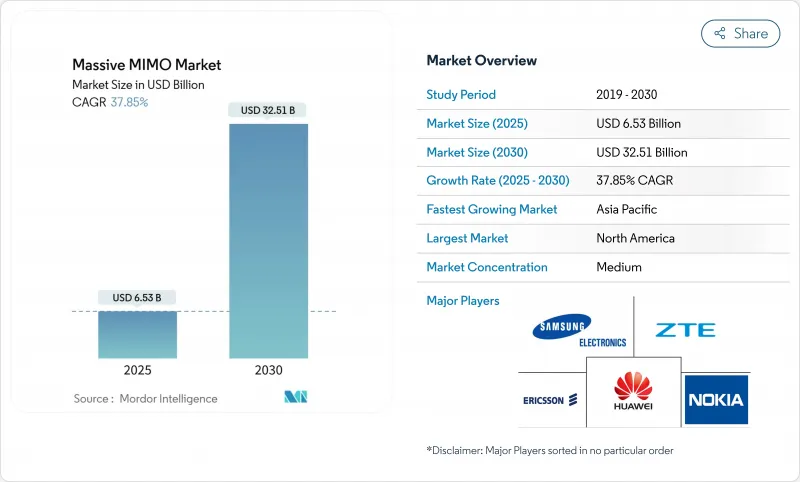

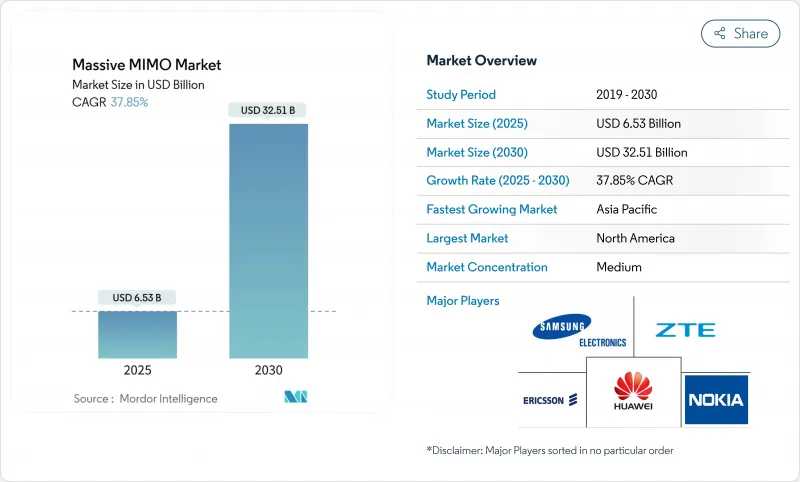

2025년 매시브 MIMO 시장은 65억 3,000만 달러, 2030년에는 325억 1,000만 달러로 확대될 것으로 예측됩니다.

이는 이 기술이 5G 배포에서 전략적으로 중요하다는 것을 뒷받침하는 37.85%의 연평균 복합 성장률(CAGR)을 반영합니다.

매시브 MIMO 시장은 2029년까지 전 세계적으로 83억 5G 가입을 향한 설치 기반, 사설 5G 네트워크 채택 확대, 멀티벤더 에코시스템을 촉진하는 오픈 RAN 아키텍처에 대한 정책적 지원을 통해 더욱 기세를 얻고 있습니다. 하드웨어 공급업체는 128T128R 및 512T512R의 고차원 어레이로 전환하여 사이트당 처리량을 높이고 운영자는 네이티브 에너지 절약 소프트웨어를 넷 제로 목표를 달성하기 위해 도입했습니다. 산업용 IoT 및 고정 무선 액세스 이용 사례가 늘어나면 사이트 수요가 증가하고 예측 기간 동안에도 이 기술이 네트워크 고밀도화 전략의 핵심이 되는 것이 확실해집니다.

세계 대규모 MIMO - 시장 동향과 통찰

모바일 데이터 트래픽 및 장치 밀도 급증

중국에서는 2030년까지 모바일 데이터 트래픽이 4배가 될 것으로 예상되고 있으며, 기존의 셀 분할 전략에서는 비용 효율적으로 관리할 수 없는 밀도 수준이 만들어졌습니다. 고정 무선 액세스 회선은 2024년의 1억 6,000만 회선에서 2030년에는 3억 5,000만 회선으로 증가할 것으로 예측되며, 그 80%는 매시브 MIMO무선 어레이, ZTE를 중심으로 하는 5G-Advanced 네트워크에 의해 서비스됩니다. 산업용 IoT는 추가 부하가 되고 중국은 2027년까지 10,000개의 무선 대응 공장을 목표로 하고 있으며, 각각 네트워크 용량에 엄격한 성능 제약을 부과하고 있습니다. 주요 시장에서 5G의 보급률이 75.9%를 넘으면 셀 엣지에서의 혼잡이 격화되고 일관된 사용자 경험을 유지하기 위해서는 빔포밍이 필수적입니다. 따라서 매시브 MIMO 시장은 트래픽 증가와 직접적으로 일치하며, 사업자는 이에 비례하여 사이트를 확장하지 않고 처리량의 요구를 충족시킬 수 있습니다.

5G NR(서브 6GHz 및 mm 파)의 급속한 세계 개발

에릭슨에 따르면 5G의 단독 계약 수는 2024년 말까지 세계에서 12억에 달하고 2030년에는 36억에 이를 것으로 예측되고 있습니다. 중국은 2025년까지 450만 곳의 5G 기지국을 신설할 계획으로 새로운 기지국의 디폴트 안테나 시스템으로서 매시브 MIMO를 의무화하고 있습니다. 에릭슨에 따르면 2025년에 에릭슨, NBN Co, 퀄컴이 고급 빔포밍에 의존하는 14km의 기가비트 링크를 입증함으로써 mmWave의 경제성이 개선되었습니다. 프라이빗 5G는 2024년에 RAN의 수익이 40% 이상 증가하고 간섭 관리된 무선은 보증된 서비스 수준 계약에 필수적입니다.

RF 프론트엔드의 높은 단가와 전력 소비

질화갈륨 웨이퍼의 생산량의 98%를 차지하고 있으며, 고차 어레이에 필수적인 RF 프론트엔드 모듈공급 안정성과 가격에 대한 우려가 높아지고 있습니다. 컴포넌트 제조업체인 Qorvo는 휴대전화 수요의 연화에 따라 2025년 3분기 매출이 12.4% 감소했습니다. AI를 활용한 절전 알고리즘은 무선의 에너지 소비를 최대 80%까지 줄일 수 있지만 실리콘을 추가해야 하기 때문에 수량이 확대될 때까지 부품 비용이 상승합니다. 미국 국방부는 국내 갈륨 가공 파일럿 사업에 자금을 제공하고 있지만, 상업 생산량은 2027년 이후로 어긋나고, 사업자는 외환 변동이나 수출 규제에 노출되게 됩니다. 이러한 요인은 비용에 민감한 지역에서의 당면 채택을 억제하고 업그레이드의 선행을 촉진합니다.

부문 분석

5G NR Sub-6GHz 기술은 전파 특성이 광역 커버리지와 실내 침투를 지원하고 초기 5G 출시의 기본 옵션이기 때문에 2024년 매출은 58%를 차지했습니다. 이 부문은 여러 지역에서 미드밴드 할당이 조화됨에 따라 장치의 생태계가 간소화되고 무선 비용이 절감되었습니다. 대조적으로 5G NR mmWave는 현재 프리미엄 이용 사례만을 차지하고 있지만 CAGR은 39.8%를 고정 무선 액세스 및 경기장의 핫스팟에서의 이용이 가속되고 있음을 나타냅니다. mmWave의 매시브 MIMO 시장 규모는 사업자가 호주 14km 지역 링크의 성공을 재현하고 도시 이외의 광대역에서 고주파 경제성이 입증됨에 따라 크게 확대될 것으로 예측됩니다.

그럼에도 불구하고, 서브 6 레이어는 여전히 제어 플레인의 앵커링에 필수적이며, 통신 사업자는 커버리지와 용량을 양립시키는 균형 잡힌 주파수 전략을 취할 수 있습니다. 릴라이언스 지오(Reliance Jio)의 AirFiber 평가판에서 mmWave FWA는 섬유에 비해 마지막 마일의 배포 시간을 단축하고 있습니다. 일본의 프라이빗 5G 면허 상황은 여전히 Sub-6이 유리하지만, 창고에서의 초기 mmWave 프로젝트는 향후 다양화를 시사하고 있습니다. 디바이스 비용이 낮아지고 5G-Advanced에서 전파 강화가 성숙하면 mmWave의 점유율이 상승하고 2030년까지 매시브 MIMO 시장 매출에서 차지하는 비율이 높아질 것입니다.

64T64R 패널은 높은 셀 에지 처리량과 관리하기 쉬운 무게와 전력 소비의 균형을 맞추어 2024년에 39%의 수량 점유율을 차지했습니다. 사업자는 밀집한 메트로 매크로 사이트를 업그레이드할 때 설치에 필요한 구조 보강이 최소한이기 때문에 이 형식을 선호하고 사용하고 있습니다. 128T128R 이상의 클래스는 공급업체가 방열판 효율을 개선하고 AI 도구가 빔 교정 오버헤드를 줄이면서 41.2%의 연평균 복합 성장률(CAGR)로 전환할 것으로 보입니다. 조지아 공과대학의 조사에서는 27-41GHz대에서 상당한 소자수를 지원하는 리시버 아키텍처가 실증되어 초대규모 어레이의 실용성이 나타났습니다.

용도이 XR 및 산업용 로봇으로 전환함에 따라 일관된 멀티 기가비트 처리량에 대한 수요가 증가하고 통신 사업자는 256개 요소의 프로토타입을 테스트하게 됩니다. 128T128R 시스템의 매시브 MIMO 시장 규모는 2030년까지 119억 달러에 이르렀으며 전체 매출의 36.6%에 해당할 것으로 예측됩니다. 퀄컴의 4096 소자 Giga-MIMO 컨셉은 스텝 기능에 의한 용량 향상의 길을 보여줍니다. 가까운 미래에 32T32R 어레이는 타워 적재량 제한으로 더 무거운 패널을 사용할 수 없는 지역 및 비용에 중점을 둔 배치에 대응하여 다층 시장 구조를 유지합니다.

대규모 MINO 시장 보고서는 기술별(LTE(4G), 5G NR Sub-6GHz, 기타), 안테나 유형별(16T16R, 32T32R, 기타), 배포 유형별(집중형(C-RAN), 분산형 RAN, 기타), 아키텍처별(시분할 듀플렉스(TDD), 주파수 분할 듀플렉스(FDD), 기타), 최종 사용자용도별(모바일 네트워크 사업자, 기업, 사설망, 기타), 지역별로 분류됩니다.

지역 분석

북미는 적극적인 C-band 전개, 기업용 FWA 채택, Open RAN에 대한 호의적인 정책을 배경으로 2024년 세계 수익의 40%를 창출. Verizon은 2025년에 175억-185억 달러의 자본 지출을 계획하고 있으며, 가입자 1인당 처리량 경쟁력을 유지하는 64T64R 섹터 업그레이드에 상당한 비율을 갖고 있습니다. 캐나다의 TELUS는 삼성과 제휴하여 최초의 가상화 RAN을 전국 전개합니다. 70/80/90GHz 밴드 백홀과 37GHz 밴드 공유에 대한 FCC 개혁은 지역 광대역을 위한 mm 파 비즈니스 케이스를 더욱 확대합니다.

중국이 2025년 3월까지 440만 곳의 5G 사이트를 돌파하고 연내에 450만 곳의 기지국을 추가할 것을 약속했기 때문에 아시아태평양은 2030년까지의 CAGR이 37.89%로 예측되어 가장 급성장하고 있는 지역입니다. 인도는 2024년 후반에 전국적인 5G 커버리지를 달성했으며, 릴라이언스 지오가 액티브 셀의 85%를 담당하고 있기 때문에 32T32R 및 64T64R 라디오의 대규모 조달 루트가 형성되고 있습니다. Bharat 6G와 같은 정부 프로그램은 토착 R&D를 중시하고 지역 벤더 점유율을 재편할 수 있습니다. 중국 연통(차이나 유니콤)은 2025년 말까지 300개 도시를 커버하는 5G-Advanced를 발표해 안테나 주문량을 더욱 증가시킵니다.

유럽에서는 사업자가 자본 효율성과 벤더 다양화를 둘러싼 규제 모니터링을 양립시키면서 신중한 확대를 보여주고 있습니다. 삼성과 O2 텔레포니카는 2024년에 64T64R 라디오를 사용한 독일 최초의 상용 vRAN 사이트를 가동하여 분해 스택 테스트에 대한 시장 의욕을 보였습니다. 에릭슨과 MasOrange는 스페인에서 개방형 프로그래머블 네트워크를 시연했으며 원시 용량보다 자동화와 에너지 최적화에 중점을 둡니다. 프랑스와 이탈리아의 주파수 경매에서는 3.4-3.8GHz의 연속 블록이 유리해져 TDD의 우위성이 강해졌습니다. 따라서 유럽의 매시브 MIMO 시장은 와트당 성능과 공급망의 탄력성을 중시하고 완만하면서도 견고한 성장을 지원하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 모바일 데이터 트래픽과 디바이스 밀도 급증

- 5G NR(서브 6GHz 및 mmWave)의 급속한 세계 전개

- 빔포밍의 효율화에 의한 오퍼레이터의 CAPEX 삭감

- 멀티 벤더 mMIMO를 가능하게 하는 Open-RAN 촉매

- AI 지원에 의한 셀 엣지 빔 최적화

- 시장 성장 억제요인

- RF 프론트엔드의 높은 단가 및 전력 소비

- 복잡한 사이트 레벨 배포 및 유지 보수

- 반도체 등급의 질화갈륨(GaN) 공급 위험

- 전자파 노출과 도시 실적 반대

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 기술별

- LTE(4G)

- 5G NR 서브 6GHz

- 5G NR mm 파

- 안테나 유형별

- 16T16R

- 32T32R

- 64T64R

- 128T128R 이상

- 전개 유형별

- 집중형(C-RAN)

- 분산 RAN

- 오픈 RAN

- 아키텍처별

- 시분할 듀플렉스(TDD)

- 주파수 분할 듀플렉스(FDD)

- 하이브리드 듀플렉스

- 최종 사용자용도별

- 모바일 네트워크 사업자

- 기업과 사설망

- 공공 안전과 방어

- 고정 무선 액세스(FWA)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Samsung Electronics

- Ericsson

- Huawei

- Nokia

- ZTE

- Qualcomm

- Intel

- Texas Instruments

- Qorvo

- NEC

- Fujitsu

- CommScope

- Airspan Networks

- Mavenir

- Parallel Wireless

- Keysight Technologies

- Rohde and Schwarz

- Viavi Solutions

- Analog Devices

- Renesas

제7장 시장 기회와 장래의 전망

SHW 25.11.11The massive MIMO market stood at USD 6.53 billion in 2025 and is projected to expand to USD 32.51 billion by 2030, reflecting a vigorous 37.85% CAGR that confirms the technology's strategic importance for 5G roll-outs.Steady operator migration from broad-coverage roll-outs toward capacity-oriented urban deployments is amplifying demand, because beamforming increases spectral efficiency and lifts average revenue per user.

The massive MIMO market receives additional momentum from an installed base headed toward 8.3 billion global 5G subscriptions by 2029, greater adoption of private 5G networks, and policy support for Open RAN architectures that encourage multi-vendor ecosystems. Hardware vendors are also moving to higher-order 128T128R and 512T512R arrays, which multiply throughput per site, while operators deploy AI-native energy-saving software to meet net-zero goals. Emerging industrial IoT and fixed-wireless-access use cases add incremental site demand, ensuring that the technology remains the backbone of network densification strategies over the forecast period.

Global Massive MIMO Market Trends and Insights

Surging Mobile-Data Traffic and Device Density

China expects mobile data traffic to quadruple by 2030, creating density levels that legacy cell-splitting strategies cannot manage cost-effectively. Fixed-wireless-access lines are forecast to climb from 160 million in 2024 to 350 million by 2030, with 80% serviced by 5 G-Advanced networks anchored by massive MIMO radio arrays, ZTE. Industrial IoT adds further load; China targets 10,000 wireless-enabled factories by 2027, each placing tight performance constraints on network capacity. As 5G penetration exceeds 75.9% in leading markets, congestion at the cell edge intensifies, making beamforming vital for sustaining a consistent user experience. The massive MIMO market, therefore, aligns directly with traffic growth, positioning operators to meet throughput needs without proportional site expansion.

Rapid Global Roll-out of 5G NR (Sub-6 GHz and mmWave)

Standalone 5G subscriptions reached 1.2 billion worldwide by end-2024 and are forecast to touch 3.6 billion by 2030, according to Ericsson. China plans to add 4.5 million new 5G base stations by 2025, mandating massive MIMO as the default antenna system for fresh sites. India achieved nationwide 5G coverage by October 2024, accelerating demand for high-order arrays during back-haul upgrades. mmWave economics improved in 2025 when Ericsson, NBN Co, and Qualcomm demonstrated 14 km gigabit links that rely on advanced beamforming, according to Ericsson. Private 5G saw over 40% RAN revenue growth in 2024, and interference-managed radios are indispensable for guaranteed service-level agreements.

High Unit Cost and Power-Consumption of RF Front-end

China controls 98% of gallium nitride wafer output, raising supply-security and pricing concerns for RF front-end modules essential in high-order arrays. Component maker Qorvo recorded a 12.4% sales decline in Q3 2025 as handset demand softened, hinting that vendor margins already feel pressure from cost-push inflation. AI-enabled power-saving algorithms can trim radio energy draw by up to 80%, but they require additional silicon, raising bill-of-materials until volume scales. The U.S. Defense Department has funded domestic gallium processing pilots, yet commercial volumes will lag beyond 2027, leaving operators exposed to currency swings and export controls. These factors restrain near-term adoption in cost-sensitive geographies and encourage deferred upgrades.

Other drivers and restraints analyzed in the detailed report include:

- Operator CAPEX Savings via Beamforming Efficiency

- Open RAN Catalysts Enabling Multi-vendor Massive MIMO

- Complex Site-level Deployment and Maintenance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

5G NR Sub-6 GHz technology commanded 58% revenue in 2024 because its propagation traits support wide-area coverage and indoor penetration, making it the default option for early 5G launches. The segment benefited from harmonized mid-band allocations across several regions, which streamlined device ecosystems and reduced radio costs. In contrast, 5G NR mmWave occupies only premium use cases today, but its 39.8% CAGR indicates accelerating take-up in fixed wireless access and stadium hotspots. The massive MIMO market size for mmWave is projected to widen significantly as operators replicate the 14 km rural link success in Australia, proving high-frequency economics for non-urban broadband.

The Sub-6 layer nevertheless remains essential for control-plane anchoring, giving carriers a balanced spectrum strategy that marries coverage and capacity. Reliance Jio's AirFiber trials show mmWave FWA cutting last-mile rollout times compared with fiber. Japan's private 5G licensing landscape still favors Sub-6, but early mmWave projects in warehouses hint at forthcoming diversification. Once device costs fall and propagation enhancements mature under 5G-Advanced, the mmWave share should climb, contributing a rising portion of the massive MIMO market revenue through 2030.

64T64R panels held 39% volume share in 2024 by balancing high cell-edge throughput with manageable weight and power draw. Operators favor this format when upgrading macro sites in dense metros because installation requires minimal structural reinforcement. The 128T128R and larger class will register a 41.2% CAGR as vendors improve heat-sink efficiency and as AI tools mitigate beam calibration overhead. Research at Georgia Tech demonstrates receiver architectures that support substantial element counts across 27-41 GHz bands, signaling practical viability for extremely large-scale arrays.

As applications migrate toward XR and industrial robotics, demand for consistent multi-gigabit throughput climbs, prompting carriers to test 256-element prototypes. The massive MIMO market size for 128T128R systems is projected to reach USD 11.9 billion by 2030, equal to 36.6% of overall sales. Qualcomm's 4,096-element Giga-MIMO concept underlines the runway for step-function capacity gains, although commercial adoption is likely after 2028 when power-amplifier efficiency improves. Near-term, 32T32R arrays still serve rural and cost-sensitive deployments where tower loading limits preclude heavier panels, preserving a multi-tier market structure.

Massive MINO Market Report is Segmented by Technology (LTE (4G), 5G NR Sub-6 GHz, and More), Antenna Type (16T16R, 32T32R, and More), Deployment Type (Centralised (C-RAN), Distributed RAN, and More), Architecture (Time-Division Duplex (TDD), Frequency-Division Duplex (FDD), and More), End-User Application (Mobile Network Operators, Enterprises and Private Networks, and More), and Geography.

Geography Analysis

North America generated 40% of global revenue in 2024 on the back of aggressive C-band roll-outs, enterprise FWA adoption, and favorable policy toward Open RAN. Verizon plans USD 17.5-18.5 billion in 2025 capital outlays, a sizable share earmarked for 64T64R sector upgrades that keep per-subscriber throughput competitive. Canada's TELUS is partnering with Samsung to deploy the first nationwide virtualized RAN, underscoring regional appetite for software-defined radios. FCC reforms around 70/80/90 GHz backhaul and 37 GHz sharing further broaden mmWave business cases for rural broadband.

Asia Pacific is the fastest-growing territory, forecast at 37.89% CAGR to 2030 as China surpasses 4.4 million 5G sites by March 2025 and commits to 4.5 million additional base stations within the year. India reached nationwide 5G coverage in late 2024, with Reliance Jio responsible for 85% of active cells, creating a sizable procurement funnel for 32T32R and 64T64R radios. Government programs such as Bharat 6G emphasize indigenous R&D, potentially reshaping regional vendor shares. China Unicom's 5G-Advanced coverage across 300 cities by end-2025 further raises antenna order volumes, providing economies of scale that exert downward price pressure globally.

Europe shows measured expansion as operators juggle capital efficiency and regulatory scrutiny over vendor diversification. Samsung and O2 Telefonica activated Germany's first commercial vRAN site with 64T64R radios in 2024, signaling market willingness to test disaggregated stacks. Ericsson and MasOrange demonstrated an open programmable network in Spain, focusing on automation and energy optimization rather than raw capacity. Spectrum auctions in France and Italy favored contiguous 3.4-3.8 GHz blocks, reinforcing TDD dominance. The European massive MIMO market therefore emphasizes performance per watt and supply-chain resilience, supporting gradual but firm growth.

- Samsung Electronics

- Ericsson

- Huawei

- Nokia

- ZTE

- Qualcomm

- Intel

- Texas Instruments

- Qorvo

- NEC

- Fujitsu

- CommScope

- Airspan Networks

- Mavenir

- Parallel Wireless

- Keysight Technologies

- Rohde and Schwarz

- Viavi Solutions

- Analog Devices

- Renesas

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging mobile-data traffic and device density

- 4.2.2 Rapid global roll-out of 5G NR (Sub-6 GHz and mmWave)

- 4.2.3 Operator CAPEX savings via beam-forming efficiency

- 4.2.4 Open-RAN catalysts enabling multi-vendor mMIMO

- 4.2.5 AI-assisted cell-edge beam-optimization

- 4.3 Market Restraints

- 4.3.1 High unit cost and power-consumption of RF front-end

- 4.3.2 Complex site-level deployment and maintenance

- 4.3.3 Semiconductor-grade gallium nitride (GaN) supply risk

- 4.3.4 EMF-exposure and urban footprint opposition

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 LTE (4G)

- 5.1.2 5G NR Sub-6 GHz

- 5.1.3 5G NR mmWave

- 5.2 By Antenna Type

- 5.2.1 16T16R

- 5.2.2 32T32R

- 5.2.3 64T64R

- 5.2.4 128T128R and Above

- 5.3 By Deployment Type

- 5.3.1 Centralised (C-RAN)

- 5.3.2 Distributed RAN

- 5.3.3 Open RAN

- 5.4 By Architecture

- 5.4.1 Time-Division Duplex (TDD)

- 5.4.2 Frequency-Division Duplex (FDD)

- 5.4.3 Hybrid Duplex

- 5.5 By End-user Application

- 5.5.1 Mobile Network Operators

- 5.5.2 Enterprises and Private Networks

- 5.5.3 Public Safety and Defence

- 5.5.4 Fixed Wireless Access (FWA)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 UAE

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Samsung Electronics

- 6.4.2 Ericsson

- 6.4.3 Huawei

- 6.4.4 Nokia

- 6.4.5 ZTE

- 6.4.6 Qualcomm

- 6.4.7 Intel

- 6.4.8 Texas Instruments

- 6.4.9 Qorvo

- 6.4.10 NEC

- 6.4.11 Fujitsu

- 6.4.12 CommScope

- 6.4.13 Airspan Networks

- 6.4.14 Mavenir

- 6.4.15 Parallel Wireless

- 6.4.16 Keysight Technologies

- 6.4.17 Rohde and Schwarz

- 6.4.18 Viavi Solutions

- 6.4.19 Analog Devices

- 6.4.20 Renesas

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment