|

시장보고서

상품코드

1850316

데이터 준비 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Data Preparation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

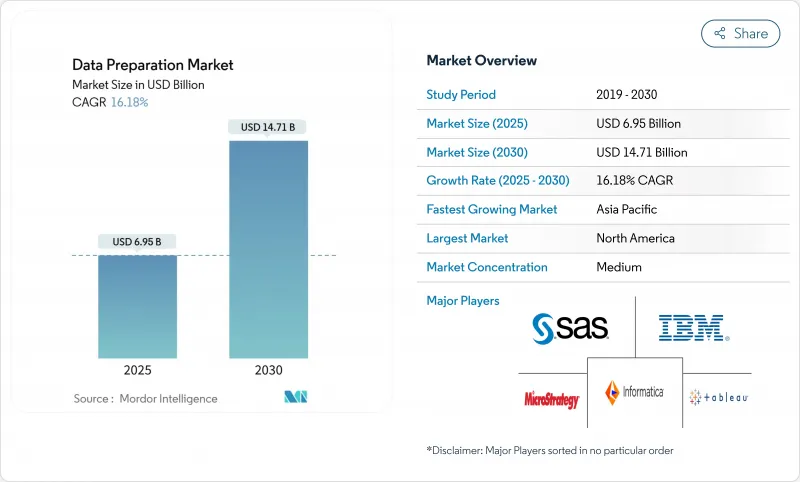

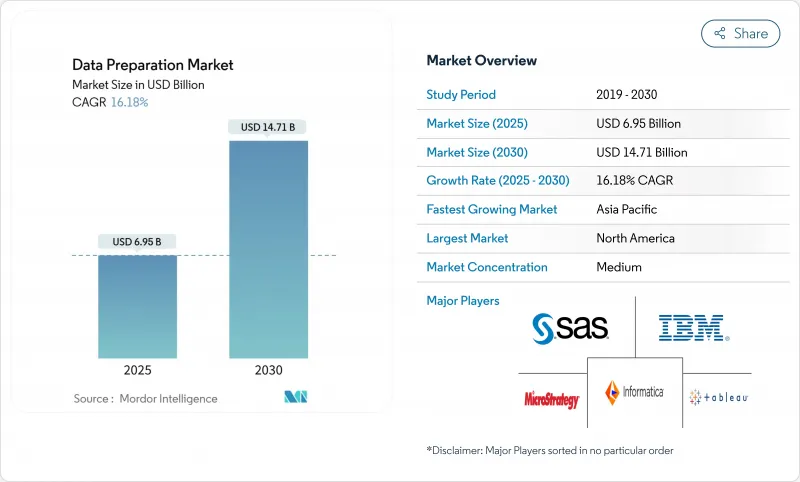

데이터 준비 시장 규모는 2025년에 69억 5,000만 달러, 2030년에는 147억 1,000만 달러에 이르고, CAGR 16.2%를 나타낼 것으로 예측됩니다.

이 확장은 기업이 일상적인 워크플로우에 생성형 AI를 통합함으로써 AI 대응 인프라가 급증하고 있음을 반영합니다. 데이터 거버넌스 프로그램은 2023년에는 60%였지만, 현재는 71% 조직에서 도입되어 체계적인 데이터 준비 도구에 대한 지출을 강화하고 있습니다. On-Premise 솔루션이 2024년 매출의 65.7%를 차지한 반면, 클라우드 도입은 CAGR 17.8%로 가장 빠르게 확대되고 있습니다. 이는 2025년 7월에 시행된 베트남 데이터 법과 같이 국경을 넘는 전송을 제한하는 주권 클라우드 규제에 의해 형성된 패턴입니다. 2024년 매출 점유율은 대기업이 68.9%를 차지했지만, 로우코드 애널리틱스와 소비 기반 가격 설정이 진입 장벽을 낮추기 때문에 중소기업이 CAGR 18.1%로 가장 기세를 보이고 있습니다. 데이터 분석 모듈은 2024년 매출의 24.3%를 차지했습니다. 그러나 EU의 기업 지속가능성 보고 지령에서 태어난 온실가스 보고 의무에 힘입어 거버넌스 중심의 솔루션이 CAGR 17.3%로 가장 빠르게 성장하고 있습니다. IT 및 통신은 2024년에 22.8%의 수직 점유율로 최대가 되었지만, 헬스케어 및 생명과학는 AI가 진단, 환자 워크플로우, 생명과학의 연구개발에 진입함에 따라 2030년까지 16.8%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 지역별로는 북미가 2024년 매출에서 37.1%를 차지해 선두에 올랐지만, 아시아태평양은 데이터센터용량의 확대에 힘입어 17.5%의 연평균 복합 성장률(CAGR)로 다른 사람을 능가할 것으로 보입니다.

세계의 데이터 준비 시장 동향과 인사이트

로우코드/노코드 셀프서비스 분석 툴로의 이동 가속

저 코드 인터페이스는 비즈니스 전문가가 스크립트가 아닌 드래그 앤 드롭 설계로 파이프라인을 구축할 수 있게 함으로써 데이터 준비 시장을 재정의합니다. Google Cloud의 BigQuery 데이터 준비는 이러한 추세를 보여주며 자연 언어 프롬프트에서 데이터를 정리, 프로파일링 및 변환하는 AI 지침을 제공합니다. 이 접근법은 누락된 데이터 엔지니어에 대한 의존도를 줄이고, 개발 주기를 단축하며, 분석의 전달을 도메인 전문 지식과 연계시킵니다. GenAI를 활용한 확장 기능은 급속히 보급되고 있어 업계 예측에서는 2026년까지 거의 모든 BI 플랫폼에 GenAI가 포함된다고 합니다. 그러나 대중적인 시민들이 구축한 흐름을 기업의 품질과 보안 표준과 정합시키기 위해서는 거버넌스의 철저가 필요합니다.

중소기업 분석팀에서 클라우드 도입 급증

중소기업은 2025년까지 60% 기업이 AI 언어 모델 도입을 계획하고 있는 아시아태평양 수요 증가를 견인하고 있습니다. 클라우드의 탄력성과 소비 가격으로 중소기업은 자본 지출을 피하면서 고급 데이터 준비 기능을 활용할 수 있습니다. 영국의 조사에 따르면 현재 빅데이터 분석을 활용하고 있는 중소기업은 전체의 1% 미만이며, 비용과 복잡성의 장애물이 낮아짐에 따라 비즈니스가 진전되고 있는 것으로 나타났습니다. 그러나 기술 부족은 여전히 계속되고 있으며 관리 서비스 제공업체는 파이프라인 설정 및 특히 데이터 현지화에 대한 새로운 규칙 준수를 강화하기 위해 진입하고 있습니다.

복잡한 데이터 거버넌스 구성의 기술 부족

CIO의 3분의 1 가까이 데이터 관리의 복잡성을 심각한 장애로 꼽고 있으며, 거버넌스의 전문가 부족으로 확장 가능한 파이프라인 배포가 지연됩니다. 이 과제는 캘리포니아의 기후 변화 정보 공개 규칙과 같은 범위 1-3의 배출량을 자동으로 파악할 의무가 있는 법률이 있는 경우에 더욱 심각해집니다. 신흥 시장에서는 학술 프로그램이 늦어져 인력 부족이 심각해지고 있으며, 도입 예산을 부풀리는 외부 컨설턴트와 매니지드 서비스 계약으로의 전환이 진행되고 있습니다.

부문 분석

On-Premise 플랫폼 데이터 준비 시장 규모는 2024년 45억 7,000만 달러에 달했고, 데이터 준비 시장 점유율은 65.7% 베트남 데이터 법과 인도의 디지털 개인 데이터 보호 규칙은 기밀 기록을 국경 내에 유지하는 온프레임 및 주권 클라우드 모델을 강화했습니다. 클라우드 서비스의 규모는 작고 중소기업과 디지털 네이티브 기업이 민첩성을 우선하기 때문에 2030년까지 17.8%의 성장이 예측되고 있습니다. 북미에서는 규제 데이터용 로컬 클러스터와 저위험 워크로드용 하이퍼스케일 저장소를 융합시킨 하이브리드 블루프린트가 주류가 되고 있습니다. 클라우드 제공업체는 지역 전용 인스턴스와 암호화된 키 컨트롤로 컴플라이언스에 대한 우려를 없애고 소규모 도시가 광섬유에 직접 연결할 수 있게 됨에 따라 기존 기술 기반 외에도 채택을 확대하고 있습니다.

안정적인 ETL 배치와 예측 가능한 풍부한 작업은 라이선스 감가 상각을 위해 On-Premise 상태이지만, 폭발적인 AI 추론과 시민 개발자 샌드박스는 종량 과금제 클라우드로 이동합니다. 다국적 기업의 절반 이상이 2029년까지 소블린 클라우드 인스턴스를 실행할 것으로 예상되고 있으며, 프라이빗, 퍼블릭, 에지 노드에 걸친 원활한 정책 구현에 대한 수요가 탄생하고 있습니다. 공급업체는 현재 기초에 관계없이 데이터 품질 규칙과 연계 그래프를 전파하는 통일된 제어 평면을 강조하고 있습니다.

대기업의 2024년 매출은 47억 9,000만 달러로, 데이터 준비 시장의 68.9%에 해당했습니다. 대기업은 카탈로그, 계보 및 관측 가능성을 기존 데이터 패브릭에 통합하는 플랫폼 번들을 선호하고 사용합니다. 반대로, 중소기업은 21억 6,000만 달러의 공헌을 하고 있지만, CAGR 18.1%로 다른 코호트를 상회해, 중소기업용 솔루션의 데이터 준비 시장 규모는 2030년까지 56억 달러에 달할 것으로 예상되고 있습니다. 소비 과금과 자동 스키마 감지는 자본 장애를 줄여 지역 소매업체, Fintech, SaaS 신흥 기업이 기존 기업과 동등해질 수 있도록 합니다.

Small Business Institute Journal의 조사에 따르면 미국 중소기업의 70%는 애널리틱스의 가치를 인정하고 있지만 엔드 투 엔드 파이프라인을 실행할 수 있는 인재를 사내에 가지고 있는 것은 소수파입니다. 저가형 클라우드 워크벤치와 관리형 서비스 에코시스템이 격차를 메우는 반면, 업계 단체는 시민 이용을 가속화하는 모듈식 교육을 제공합니다. 새로운 AI-act 의무에 대응하는 정책 프레임워크의 개발에는 과제가 남아 있으며, 컴플라이언스 오버레이를 전문으로 하는 채널 파트너에 문이 열려 있습니다.

데이터 준비 시장 보고서는 배포(On-Premise 및 클라우드), 기업 규모(중소기업(SME) 및 대기업), 솔루션 유형(데이터 인제스트, 데이터 카탈로그링 등), 최종 사용자 가상(은행, 금융서비스 및 보험(BFSI), 의료 및 생명 과학 등) 및 지역별로 분류됩니다.

지역 분석

북미의 2024년 지출액은 25억 8,000만 달러로 데이터 준비 시장 점유율의 37.1%를 차지했습니다. 캘리포니아의 기후 정보 공개법은 매출 10억 달러 이상의 기업에 범위 1-3 배출량의 공표를 의무화하고 있으며, 이 대륙 전체에서 거버넌스 툴 수요를 강화하고 있습니다. 미국 이외의 장소에 본사를 두면서 미국에서 활동하는 다국적 기업은 국경을 넘어 영향력을 확대하기 위해 여전히 보고해야 합니다. 캐나다는 법안 C-27의 소비자 프라이버시 보호법을 통해 병렬 프레임워크를 진행하고 있으며, 멕시코는 데이터 현지화를 제안하고 국경을 넘어서는 마키라도라 공급망을 위한 하이브리드 클라우드 청사진을 촉구하고 있습니다. 이 지역 투자의 초점은 초기 캡처 기능에서 운영 노력을 줄이는 고급 관측 가능성과 자동화 된 복구로 옮겨졌습니다.

아시아태평양은 가장 빠르게 성장하고 있으며, 퍼블릭 클라우드 성장이 다른 지역을 넘어 매년 17.5% 확대되고 있습니다. 중국의 83% GenAI 도입은 적극적인 파이프라인 근대화에 나타나고 있으며, 한국과 일본은 의료기록의 디지털화와 스마트 팩토리 프로그램에 국가 AI 자금을 할당하고 있습니다. 베트남 데이터 법과 인도의 DPDP 규칙은 다국적 스택에서 데이터 레지던시 계층을 유발하여 On-Premise 에지 배포를 증가시키고 통합 정책 엔진 수요를 자극합니다. 호주 기업은 데이터 준비의 업스트림 단계에서 실시간 비정상 감지를 필요로 하는 새로운 중요 인프라 보안 의무에 직면하고 있습니다. 한편, 싱가포르의 IMDA 보조금은 중소기업을 클라우드 서비스로 밀어 올려 이 지역의 대중시장 기세를 강화하고 있습니다.

유럽에서는 ESG 지령이 '보고서 대응' 파이프라인 투자를 촉진하고 10%대 중반의 꾸준한 성장을 기록하고 있습니다. EU의 기업 지속가능성 보고 지침은 약 5만 개 기업에 일관된 분류법을 사용하여 온실가스 측정 기준을 기록하는 것을 강제하고, 데이터 카탈로그와 품질 도구를 경영진의 의제로 밀어 올렸습니다. 독일과 프랑스가 지출을 이끌고 있지만, 이탈리아와 스페인에서는 부흥 회복 기금(Recovery and Resilience Facility)의 보조금이 디지털 전환 프로젝트를 맡고 있으며 그 기세는 가속화되고 있습니다. EU의 AI 방법은 투명성, 바이어스 모니터링 및 인간 모니터링 로그를 요구하며, 에지 노드와 하이퍼스케일러 영역에 걸쳐 안전한 연계 아카이브가 필요합니다. 동유럽 국가들은 시민 데이터를 국내에 유지하기 위해 로컬 클라우드의 능력을 강화하고 지역 통신 사업자와 세계 하이퍼스케일러와의 파트너십을 장려하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 로우 코드/노코드의 셀프 서비스 분석 툴로의 이행을 가속

- 중소기업 분석팀의 클라우드 도입 급증

- 데이터 준비 워크플로우에 GenAI 코파일럿 통합

- 벤더가 데이터 준비 모듈을 보다 광범위한 데이터 패브릭 스위트에 번들

- 도메인 특화형 「수직 AI」데이터 준비 파이프라인의 급속한 증가

- On-Premise/하이브리드의 회귀를 촉진하는 주권 클라우드 규칙

- 시장 성장 억제요인

- 복잡한 데이터 거버넌스 구성에 관한 스킬 갭

- 멀티클라우드 데이터 파이프라인의 총소유비용 상승

- 신흥 시장에서의 데이터 주권에 관한 벌칙 강화

- 탄소발자국의 할당이, 계산 부하가 높은 준비 작업 방해

- 밸류체인 분석

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 거시 경제 동향이 시장에 미치는 영향 평가

제5장 시장 규모와 성장 예측

- 배포별

- On-Premise

- 클라우드

- 기업 규모별

- 중소기업

- 대기업

- 솔루션 유형별

- 데이터 수집

- 데이터 카탈로그화

- 데이터 품질

- 데이터 거버넌스

- 데이터 정리

- 데이터 보강

- 최종 사용자별

- BFSI

- 헬스케어 및 생명과학

- 소매업 및 전자상거래

- 제조 및 산업

- IT 및 통신

- 정부 및 공공 부문

- 기타(에너지, 교육, 미디어)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Alteryx Inc.

- Informatica LLC

- IBM Corporation

- Microsoft Corporation

- Tableau Software LLC(Salesforce)

- SAP SE

- SAS Institute Inc.

- QlikTech International AB

- TIBCO Software Inc.

- Talend SA

- Oracle Corporation

- Trifacta Inc.(Google)

- Databricks Inc.

- Snowflake Inc.

- Dataiku SAS

- MicroStrategy Inc.

- RapidMiner Inc.

- Paxata Inc.(DataRobot)

- Unifi Software Inc.

- Denodo Technologies Inc.

제7장 시장 기회와 향후 전망

KTH 25.11.10The data preparation market size stands at USD 6.95 billion in 2025 and is projected to reach USD 14.71 billion by 2030, expanding at a 16.2% CAGR.

This expansion mirrors the surge in AI-ready infrastructure as enterprises embed generative AI into day-to-day workflows; adoption has reached 83% of organizations in China and full production roll-outs in 24% of United States companies. Proliferating data-governance programs, now present in 71% of organizations compared with 60% in 2023, reinforce spending on systematic data preparation tools. Deployment choices continue to diverge: on-premises solutions controlled 65.7% of 2024 revenue, while cloud deployments are scaling fastest at 17.8% CAGR, a pattern shaped by sovereign-cloud regulations such as Vietnam's Data Law, effective July 2025, that restrict cross-border transfers. Large enterprises held 68.9% revenue share in 2024, yet small and medium enterprises (SMEs) show the strongest momentum at 18.1% CAGR as low-code analytics and consumption-based pricing lower entry barriers. Data-ingestion modules retained the top 24.3% slice of 2024 revenue; however, governance-centric solutions are rising fastest at 17.3% CAGR, pushed by greenhouse-gas-reporting mandates emerging from the EU Corporate Sustainability Reporting Directive. IT and telecommunications contributed the largest 22.8% vertical share in 2024, while healthcare and life sciences climbed at a 16.8% CAGR through 2030 as AI enters diagnosis, patient-workflow and life-science research and development. Regionally, North America led with 37.1% revenue in 2024, yet Asia-Pacific will outpace all others at 17.5% CAGR, underpinned by expanding data-center capacity-12,206 MW active and 14,338 MW in development. Mergers and acquisitions activity signals intensifying competition: Salesforce agreed to purchase Informatica for USD 8 billion in May 2025, and Alteryx was taken private for USD 4.4 billion in March 2024.

Global Data Preparation Market Trends and Insights

Accelerated Shift to Low-/No-Code Self-Service Analytics Tools

Low-code interfaces are redefining the data preparation market by enabling business specialists to build pipelines via drag-and-drop designs rather than scripts. Google Cloud's BigQuery data preparation illustrates the trend, offering AI guidance that cleans, profiles and transforms data with natural-language prompts. The approach reduces reliance on scarce data engineers, shortens development cycles and aligns analytics delivery with domain expertise. GenAI-powered augmentation is spreading quickly; industry forecasts suggest nearly all BI platforms will embed GenAI by 2026. Adoption, however, requires diligent governance to keep proliferating citizen-built flows aligned with enterprise quality and security standards.

Surging Cloud Adoption Among SME Analytics Teams

SMEs are scaling cloud-native pipelines to close capability gaps with larger rivals, driving incremental demand across Asia-Pacific where 60% of firms plan AI language-model implementation by 2025. Cloud elasticity and consumption pricing let smaller firms avoid capital expenses while accessing advanced data-prep functions. UK research shows sub-1% of SMEs exploit big-data analytics today, underscoring runway as cost and complexity hurdles fall. Yet skills shortages persist; managed service providers are stepping in to configure pipelines and enforce compliance, particularly around emerging data-localization rules.

Skills Gap for Complex Data-Governance Configuration

Nearly one-third of CIOs cite data-management complexity as a critical obstacle, and shortages of governance specialists delay the rollout of scalable pipelines. The challenge intensifies where legislation such as California's climate-disclosure rule mandates automated capture of Scope 1-3 emissions. Emerging markets face deeper shortages as academic programs lag, pushing firms toward external consultants and managed-service contracts that inflate deployment budgets.

Other drivers and restraints analyzed in the detailed report include:

- Integration of GenAI Copilots Inside Data-Prep Workflows

- Vendor Bundling of Data-Prep Modules into Broader Data-Fabric Suites

- Steep Total Cost of Ownership for Multi-Cloud Data Pipelines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The data preparation market size for on-premises platforms totaled USD 4.57 billion in 2024, translating to 65.7% data preparation market share, a reflection of enterprise demand for direct control amid tougher localization rules. Vietnam's Data Law and India's Digital Personal Data Protection Rules reinforce on-prem and sovereign-cloud models that keep sensitive records within national borders. Cloud services, though smaller, are projected to compound at 17.8% through 2030 as SMEs and digitally native units prioritize agility. In North America, hybrid blueprints predominate, fusing local clusters for regulated data with hyperscale reservoirs for lower-risk workloads. Cloud providers respond with dedicated regional instances and encrypted-key control to offset compliance fears, widening adoption beyond traditional tech hubs as smaller cities gain direct-connect fiber.

The economic calculus hinges on workload variability: steady ETL batches and predictable enrichment jobs remain on-prem due to licensing amortization, while bursty AI inference and citizen-developer sandboxes migrate to pay-as-you-go clouds. Over half of multinationals are expected to run sovereign-cloud instances by 2029, creating demand for seamless policy enforcement across private, public and edge nodes. Vendors now emphasize unified control planes that propagate data-quality rules and lineage graphs no matter the substrate.

Large corporations generated USD 4.79 billion revenue in 2024, equal to 68.9% of the data preparation market, supported by dedicated governance teams and global footprints. Their spend skew favors platform bundles that integrate catalog, lineage and observability into existing data fabrics. Conversely, SMEs contributed USD 2.16 billion yet will outgrow other cohorts at 18.1% CAGR, lifting the data preparation market size for SME solutions to a projected USD 5.6 billion by 2030. Consumption billing and automated schema-detection reduce capital obstacles, enabling regional retailers, fintechs and SaaS start-ups to achieve parity with incumbents.

A Small Business Institute Journal survey shows 70% of U.S. SMEs acknowledge analytics value, but only a minority has in-house talent to execute end-to-end pipelines. Low-code cloud workbenches and managed-service ecosystems fill gaps, while industry associations offer modular training to accelerate citizen usage. Challenges persist in developing policy frameworks that map to emerging AI-act obligations, creating openings for channel partners specializing in compliance overlays.

The Data Preparation Market Report is Segmented by Deployment (On-Premises and Cloud), Enterprise Size (Small and Medium Enterprises (SMEs) and Large Enterprises), Solution Type (Data Ingestion, Data Cataloging, and More), End-User Vertical (BFSI, Healthcare and Life Sciences, and More), and Geography.

Geography Analysis

North America's USD 2.58 billion spend in 2024 reflected 37.1% data preparation market share, an outcome of early AI experimentation and dense vendor ecosystems. California's climate-disclosure statute compels companies above USD 1 billion revenue to publish Scope 1-3 emissions, reinforcing governance-tool demand across the continent. Multinationals headquartered elsewhere yet active in the United States must still report, extending influence beyond borders. Canada advances parallel frameworks through Bill C-27's Consumer Privacy Protection Act, while Mexico's data-localization proposals are prompting hybrid-cloud blueprints for cross-border maquiladora supply chains. The region's investment focus has pivoted from initial ingestion capabilities to advanced observability and automated remediation that reduce operational toil.

Asia-Pacific is the fastest climber, expanding 17.5% annually as public-cloud growth surpasses other regions. China's 83% GenAI adoption manifests in aggressive pipeline modernization, while South Korea and Japan allocate national AI funds to health-record digitization and smart-factory programs. Vietnam's Data Law and India's DPDP Rules trigger data-residency layers within multinational stacks, increasing on-prem edge deployments and stimulating demand for integrated policy engines. Australian enterprises face new Critical Infrastructure Security obligations that require real-time anomaly detection in upstream data-prep stages. Meanwhile, Singapore's IMDA grants push SMEs to cloud services, reinforcing the region's mass-market momentum.

Europe posts steady mid-teens growth as ESG mandates drive "report-ready" pipeline investments. The EU Corporate Sustainability Reporting Directive forces roughly 50,000 firms to log greenhouse-gas metrics using consistent taxonomies, elevating data catalog and quality tooling to the executive agenda. Germany and France lead spend, though momentum accelerates in Italy and Spain as Recovery and Resilience Facility grants underwrite digital-transition projects. The EU AI Act requires transparency, bias monitoring and human-oversight logs, deepening the need for secure lineage archives that span edge nodes and hyperscaler zones. Eastern European states ramp local-cloud capacity to keep citizen data domestic, encouraging partnerships between regional telcos and global hyperscalers.

- Alteryx Inc.

- Informatica LLC

- IBM Corporation

- Microsoft Corporation

- Tableau Software LLC (Salesforce)

- SAP SE

- SAS Institute Inc.

- QlikTech International AB

- TIBCO Software Inc.

- Talend SA

- Oracle Corporation

- Trifacta Inc. (Google)

- Databricks Inc.

- Snowflake Inc.

- Dataiku SAS

- MicroStrategy Inc.

- RapidMiner Inc.

- Paxata Inc. (DataRobot)

- Unifi Software Inc.

- Denodo Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated shift to low-/no-code self-service analytics tools

- 4.2.2 Surging cloud adoption among SME analytics teams

- 4.2.3 Integration of GenAI copilots inside data-prep workflows

- 4.2.4 Vendor bundling of data-prep modules into broader data-fabric suites

- 4.2.5 Rapid rise of domain-specific 'vertical AI' data-prep pipelines

- 4.2.6 Sovereign-cloud rules fuelling on-prem / hybrid repatriation

- 4.3 Market Restraints

- 4.3.1 Skills gap for complex data-governance configuration

- 4.3.2 Steep total cost of ownership for multi-cloud data-pipelines

- 4.3.3 Escalating data-sovereignty penalties in emerging markets

- 4.3.4 Carbon-footprint quotas pushing back on compute-heavy prep jobs

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-premises

- 5.1.2 Cloud

- 5.2 By Enterprise Size

- 5.2.1 Small and Medium Enterprises (SMEs)

- 5.2.2 Large Enterprises

- 5.3 By Solution Type

- 5.3.1 Data Ingestion

- 5.3.2 Data Cataloging

- 5.3.3 Data Quality

- 5.3.4 Data Governance

- 5.3.5 Data Wrangling

- 5.3.6 Data Enrichment

- 5.4 By End-user Vertical

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Retail and e-Commerce

- 5.4.4 Manufacturing and Industrial

- 5.4.5 IT and Telecommunications

- 5.4.6 Government and Public Sector

- 5.4.7 Others (Energy, Education, Media)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alteryx Inc.

- 6.4.2 Informatica LLC

- 6.4.3 IBM Corporation

- 6.4.4 Microsoft Corporation

- 6.4.5 Tableau Software LLC (Salesforce)

- 6.4.6 SAP SE

- 6.4.7 SAS Institute Inc.

- 6.4.8 QlikTech International AB

- 6.4.9 TIBCO Software Inc.

- 6.4.10 Talend SA

- 6.4.11 Oracle Corporation

- 6.4.12 Trifacta Inc. (Google)

- 6.4.13 Databricks Inc.

- 6.4.14 Snowflake Inc.

- 6.4.15 Dataiku SAS

- 6.4.16 MicroStrategy Inc.

- 6.4.17 RapidMiner Inc.

- 6.4.18 Paxata Inc. (DataRobot)

- 6.4.19 Unifi Software Inc.

- 6.4.20 Denodo Technologies Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment