|

시장보고서

상품코드

1850319

스몰셀 네트워크 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Small Cell Networks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

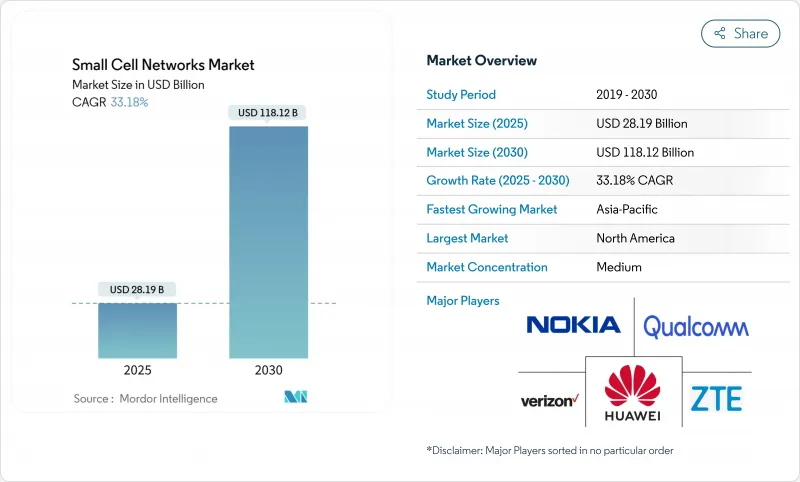

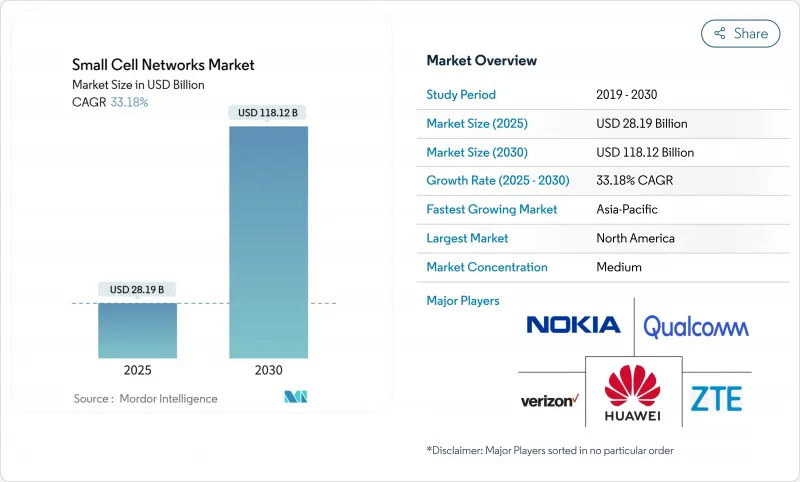

스몰셀 네트워크 시장의 2025년 시장 규모는 281억 9,000만 달러에 이르고, CAGR 33.18%로 견조하게 확대되며, 2030년에는 1,181억 2,000만 달러에 달할 것으로 예상되고 있습니다.

모바일 데이터량 증가, 고주파 5G 대역으로의 전환, 주파수 정책 지원으로 스몰셀은 틈새 솔루션에서 핵심 네트워크 자산으로 전환했습니다. mm파나 미드밴드 신호는 급속히 감쇠하므로, 특히 트래픽의 80% 이상이 실내에서 발생합니다. 공유 모델과 중립 호스트 모델의 초기 단계에서 성공으로 인해 소유 비용이 절감되는 반면, AI를 활용한 자체 최적화 기능은 기존의 분산형 안테나 시스템에 비해 에너지 사용량을 최대 45%까지 줄였습니다. 2026년 6월까지 완료되는 AWS-3 경매를 앞두고 기존 사업자가 규모의 우위성을 요구해 통합이 격화되고 있으며, 이 경매에서는 30억-45억 달러의 미드밴드 주파수대가 상업 이용될 것으로 예측되고 있습니다.

세계의 스몰셀 네트워크 시장 동향과 인사이트

5G 주파수 경매가 네트워크의 고밀도화를 가속

미드밴드 주파수 대역 할당은 5G에 필요한 스펙트럼의 헤드룸을 해제하고 있습니다. 독립적인 경제 모델링에 따르면 100MHz 증가할 때마다 GDP에 2,640억 달러가 추가됩니다. 곧 시작되는 AWS-3 판매는 이 효과를 더욱 강화할 것입니다. 허가가 빨라짐에 따라 미국의 허가주기는 수년에서 수개월로 단축되었으며, 사업자는 매크로 사이트에서 도시당 수천 개의 거리 노드까지 규모를 확장할 수 있게 되었습니다. mm파의 신호는 감쇠가 심하기 때문에 연속적인 커버리지를 실현하기 위해서는 기존 매크로셀의 최대 10배의 스몰셀이 필요해, 컴팩트한 무선기나 통합 안테나의 수주를 뒷받침하고 있습니다.

모바일 데이터 폭발이 보급 촉진

에릭슨에 따르면 연간 트래픽은 20% 증가하고 있으며, 5G는 2029년까지 75%의 비트를 전송한다고 합니다. UHD 비디오 스트리밍, XR 컨텐츠 및 클라우드 게임은 섹터화된 매크로에 부담을 주는 핫스팟 수요 프로파일을 생성합니다. 스몰셀 클러스터를 대상으로 함으로써 본격적인 오버레이 없이 현지화된 용량을 제공하며, 사업자는 사용자 경험을 유지하면서 설비 투자를 억제할 수 있습니다. 업계 단체는 향후 10년간 8배가 될 것으로 예상하고 있습니다.

규제 장애물이 보급 속도를 방해

연방 정부의 합리화 후에도 지역 규칙은 크게 다릅니다. 역사 지구는 종종 설계 심사를 부과하고, 승인을 12-24개월로 늘려, 건설 예산을 팽창시키고 있습니다. 미국에서는 현재 약 20개 주가 소규모 셀에 관한 법령을 정하고 있지만, 해석에 일관성이 없기 때문에 복수주를 건너는 건설이 복잡해지고 있습니다. 사업자는 폴탑의 인클로저를 표준화하고, 스트리트 패니처의 리스를 활용해 사이클을 단축하고 있지만, 마찰이 옥외 전개의 브레이크가 되고 있습니다.

부문 분석

펨토셀은 가정과 소규모 사무실을 위한 합리적인 가격을 반영하여 2024년 매출의 37%를 차지했습니다. 펨토셀은 약 60피트(약 1.6m) 이내에 최대 6명의 사용자를 수용할 수 있으므로 실내 스포트 개선에 이상적입니다. 그러나 마이크로셀은 CAGR 35.30%로 가장 급성장할 예정이며, 1,000피트(약 1,000m) 이내에 200명의 유저에게 서비스를 제공할 수 있기 때문에 밀집한 쇼핑가나 교통기관에 최적입니다. 통신 사업자가 이러한 노드를 엣지 컴퓨팅과 결합하고 지연에 민감한 이용 사례를 지원하기 때문에 마이크로셀 계층의 스몰셀 네트워크 시장 규모는 빠르게 확대될 것으로 예측됩니다. 무선 설계도 Open RAN 표준에 수렴하고 있어, 락 인을 저감해 혁신을 가속하는 멀티 벤더 에코시스템이 가능하게 됩니다.

피코셀의 호환성 업그레이드(중규모 장소에서는 750피트(약 3.5미터)를 커버)는 새로운 기업 계약의 잠금을 해제하고 있으며, 메트로셀은 보행자 수준에서 핸드오프를 원활하게 하기 위해 간선 도로를 따라 전개되고 있습니다. 실내 무선 도트 아키텍처는 120개의 운영자를 통과하여 최소한의 현장 장비로 매크로 패리티 속도를 실현합니다. 이러한 동향을 종합하면, 스몰셀 네트워크 시장이 단일 디바이스의 제안이 아니라 다층적인 생태계가 되고 있는 것을 알 수 있습니다.

스몰셀 네트워크 시장 보고서는 셀 유형(펨토셀, 피코셀, 마이크로셀, 메트로셀, 라디오 도트 시스템), 운영 환경(실내 및 실외), 최종 사용자 업계별(은행, 금융서비스 및 보험(BFSI), IT 및 텔레콤, 의료, 소매, 전력 및 에너지, 스마트 시티 및 정부), 지역별로 분류됩니다.

지역 분석

북미는 초기 C 밴드 경매와 연방 정부의 입지 개혁에 힘입어 2024년 매출의 35%를 차지했습니다. 미국에서만 2022년까지 45만 2,000개 이상의 야외 노드를 세고 메트로 코어를 넘어 확장하기 위해 5G Fund for Rural America를 통해 90억 달러를 투자하는 예산이 짜여졌습니다. 획기적인 140억 달러의 현대화 프로젝트는 레거시 기저대역을 개방형 아키텍처 무선으로 대체하여 공급업체의 다양성에 대한 경력 헌신을 보여줍니다.

아시아태평양의 CAGR은 38.49%로 예측되며 이 지역에서 가장 가파른 경사를 보입니다. 중국은 50만 개 이상의 5G 기지국을 배포하고 인도의 디지털 통신 정책은 전국적인 권리 장벽을 완화하고 있습니다. 이 지역의 모바일 생태계는 2023년 GDP에 8,800억 달러를 올리고 경제적 중요성을 강조했습니다. KT의 스마트 오피스용 라디오 도트 배포 등 실내 스몰셀 도입의 플래그십은 엔터프라이즈급 실내 커버리지의 비즈니스 사례를 입증하고 있습니다.

유럽은 지속가능성을 중시하고 현장 에너지를 최대 45% 줄이는 솔루션을 추구하고 있습니다. 국가 로드맵(독일의 5G 전략이 그 예)에서는 자율주행과 인더스트리 4.0을 지원하는 타이트 그리드 스몰셀이 우선되고 있습니다. 이 지역의 통신 사업자는 가로등에 소형 라디오를 내장하는 것을 일상적으로 실시했습니다. 런던이 있는 조종사에서는 웨스트민스터 전역에 80개의 셀을 추가했지만 시각적 영향은 최소한이었습니다.

중동 및 아프리카의 일부에서는 사우디아라비아가 매크로셀과 스몰셀 레이어를 결합한 멀티 벤더 프로그램을 실시하고 있는 것처럼 순례지와 스마트 시티의 회랑을 위해 5G의 확장을 진행하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 5G 주파수 경매와 네트워크 고밀도화의 의무화

- 모바일 데이터 및 동영상 트래픽의 폭발적인 증가

- 프라이빗 5G/LTE-A 네트워크에 대한 기업 수요

- 규제 당국 주도의 스펙트럼 공유와 CBRS 보급

- 중립 호스트와 공유 인프라 투자의 물결

- AI 구동형 자기 최적화 네트워크가 OPEX를 삭감

- 시장 성장 억제요인

- 복잡한 용지 취득과 지자체의 허가

- 백홀 파이버/전원 가용성의 갭

- 에너지 효율 컴플라이언스 비용 상승

- RF 프론트엔드 칩셋 수출 규제 및 공급 위험

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 투자·자금 조달 동향 분석

제5장 시장 규모와 성장 예측

- 세포 유형별

- 펨토셀

- 피코셀

- 마이크로셀

- 메트로셀

- 라디오 닷 시스템

- 운영 환경별

- 실내

- 옥외

- 최종 사용자별

- BFSI

- IT 및 통신

- 헬스케어

- 소매

- 전력 및 에너지

- 스마트시티 및 정부

- 지역별

- 북미

- 남미

- 유럽

- 아시아태평양

- 중동 및 아프리카

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Huawei Technologies Co. Ltd.

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- ZTE Corporation

- Samsung Electronics Co. Ltd.

- Cisco Systems Inc.

- CommScope Inc.(incl. Airvana)

- American Tower Corporation

- Qualcomm Technologies Inc.

- ATandT Inc.

- Verizon Communications Inc.

- Crown Castle International Corp.

- Airspan Networks Holdings Inc.

- Qucell Inc.

- Cirrus Core Networks

- Casa Systems Inc.

- Sercomm Corporation

- Baicells Technologies

- Comba Telecom Systems Holdings Ltd.

- IP.Access Ltd.

- Boingo Wireless Inc.

- Parallel Wireless Inc.

- JMA Wireless

- Corning Inc.(SpiderCloud)

제7장 시장 기회와 향후 전망

KTH 25.11.10The small cell networks market is valued at USD 28.19 billion in 2025 and is forecast to expand at a robust 33.18% CAGR, reaching USD 118.12 billion by 2030.

Rising mobile-data volumes, the transition to higher-frequency 5G bands, and supportive spectrum policies have moved small cells from niche solutions to core network assets. Carriers now treat densification as a necessity because millimeter-wave and mid-band signals attenuate rapidly, especially indoors, where more than 80% of traffic originates. Early wins with shared and neutral-host models are lowering ownership costs, while AI-enabled self-optimizing features are cutting energy use by up to 45% relative to traditional distributed antenna systems. Consolidation is intensifying as incumbents seek scale advantages ahead of the AWS-3 auction mandated for completion by June 2026, a sale projected to redirect USD 3 billion-4.5 billion of mid-band spectrum into commercial hands.

Global Small Cell Networks Market Trends and Insights

5G spectrum auctions accelerate network densification

Mid-band allocations are unlocking the spectral headroom needed for 5G. Independent economic modelling shows that every extra 100 MHz could add USD 264 billion to GDP. The forthcoming AWS-3 sale will reinforce this effect. Faster permitting has trimmed U.S. approval cycles from several years to months, enabling operators to scale from macro sites to thousands of street-level nodes per city. Because millimeter-wave signals decay sharply, achieving contiguous coverage can demand up to 10 times more small cells than legacy macrocells, driving orders for compact radios and integrated antennas.

Mobile-data explosion drives adoption

Annual traffic is rising 20%, and 5G will carry 75% of bits by 2029, according to Ericsson. Streaming UHD video, XR content, and cloud gaming create hotspot demand profiles that strain sectorized macros. Targeted clusters of small cells deliver localized capacity without full-scale overlays, enabling operators to throttle capex while preserving user experience. Deployments have already quadrupled over the past decade; industry associations expect an eight-fold increase in the next ten years.

Regulatory hurdles impede deployment velocity

Even after federal streamlining, local rules vary widely. Historic districts often impose design reviews, stretching approvals to 12-24 months and inflating construction budgets. Roughly 20 U.S. states now have small-cell statutes, yet inconsistent interpretation complicates multi-state builds. Operators are standardizing pole-top enclosures and leveraging street furniture leases to shorten cycles, but friction remains a brake on outdoor rollout.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise private networks create new growth vectors

- Neutral-host models transform deployment economics

- Semiconductor supply constraints threaten scaling

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Femtocells captured 37% of 2024 revenue, reflecting their affordability for homes and small offices. They handle up to six users within roughly 60 feet, making them the go-to for spot indoor remediation. Yet microcells are slated to grow fastest at 35.30% CAGR, benefiting from an ability to serve 200 users across 1,000 feet-ideal for dense shopping streets and transit stations. The small cell networks market size for the microcell tier is expected to expand swiftly as carriers combine these nodes with edge compute to support latency-sensitive use cases. Radio designs are also converging with Open RAN standards, enabling multi-vendor ecosystems that reduce lock-in and accelerate innovation.

Compatibility upgrades in picocells-covering 750 feet for mid-sized venues-are unlocking new enterprise contracts, while metrocells are rolling out along arterial roads to smooth hand-offs at pedestrian level. Indoor radio-dot architectures have passed 120 operators and deliver macro-parity speeds with minimal on-site equipment. Collectively, these trends underscore how the small cell networks market is becoming a multi-layered ecosystem rather than a single-device proposition.

The Small Cell Networks Market Report is Segmented by Cell Type (Femtocell, Picocell, Microcell, Metrocell, and Radio Dot Systems), Operating Environment (Indoor and Outdoor), End-User Vertical (BFSI, IT and Telecom, Healthcare, Retail, Power and Energy, and Smart City and Government), and Geography.

Geography Analysis

North America held 35% revenue in 2024, anchored by early C-band auctions and federal siting reforms. The United States alone counted more than 452,000 outdoor nodes by 2022 and is budgeted to invest USD 9 billion via the 5G Fund for Rural America to expand beyond metro cores. A landmark USD 14 billion modernization project is replacing legacy basebands with open-architecture radios, illustrating carrier commitment to vendor diversity.

Asia Pacific is projected to deliver a 38.49% CAGR, the steepest regional trajectory. China has deployed more than 500,000 5G base stations, and India's Digital Communications Policy is easing right-of-way barriers nationwide. The regional mobile ecosystem added USD 880 billion to GDP in 2023, underscoring economic stakes. Flagship indoor small-cell implementations-such as KT's Radio Dot roll-out for smart offices-demonstrate the business case for enterprise-grade indoor coverage.

Europe emphasizes sustainability, pursuing solutions that cut site energy by up to 45%. National roadmaps-Germany's 5G Strategy being an example-prioritize tight-grid small cells to support automated driving and Industry 4.0. Operators in the region routinely embed compact radios on streetlamps; one London pilot added 80 cells across Westminster with minimal visual impact.

The Middle East and parts of Africa are scaling 5G for pilgrimage sites and smart-city corridors, as seen in Saudi Arabia's multi-vendor program that combines macro and small-cell layers.

List of Companies Covered in this Report:

- Huawei Technologies Co. Ltd.

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- ZTE Corporation

- Samsung Electronics Co. Ltd.

- Cisco Systems Inc.

- CommScope Inc. (incl. Airvana)

- American Tower Corporation

- Qualcomm Technologies Inc.

- ATandT Inc.

- Verizon Communications Inc.

- Crown Castle International Corp.

- Airspan Networks Holdings Inc.

- Qucell Inc.

- Cirrus Core Networks

- Casa Systems Inc.

- Sercomm Corporation

- Baicells Technologies

- Comba Telecom Systems Holdings Ltd.

- IP.Access Ltd.

- Boingo Wireless Inc.

- Parallel Wireless Inc.

- JMA Wireless

- Corning Inc. (SpiderCloud)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G spectrum auctions and network densification mandates

- 4.2.2 Explosive mobile-data and video traffic growth

- 4.2.3 Enterprise demand for private 5G / LTE-A networks

- 4.2.4 Regulator-led spectrum-sharing and CBRS uptake

- 4.2.5 Neutral-host and shared-infrastructure investment wave

- 4.2.6 AI-driven self-optimising networks lowering OPEX

- 4.3 Market Restraints

- 4.3.1 Complex site-acquisition and municipal permitting

- 4.3.2 Backhaul fibre / power availability gaps

- 4.3.3 Rising energy-efficiency compliance costs

- 4.3.4 RF front-end chipset export controls and supply risk

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment and Funding Trends Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cell Type

- 5.1.1 Femtocell

- 5.1.2 Picocell

- 5.1.3 Microcell

- 5.1.4 Metrocell

- 5.1.5 Radio Dot Systems

- 5.2 By Operating Environment

- 5.2.1 Indoor

- 5.2.2 Outdoor

- 5.3 By End-user Vertical

- 5.3.1 BFSI

- 5.3.2 IT and Telecom

- 5.3.3 Healthcare

- 5.3.4 Retail

- 5.3.5 Power and Energy

- 5.3.6 Smart City and Government

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 South America

- 5.4.3 Europe

- 5.4.4 Asia-Pacific

- 5.4.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Huawei Technologies Co. Ltd.

- 6.4.2 Telefonaktiebolaget LM Ericsson

- 6.4.3 Nokia Corporation

- 6.4.4 ZTE Corporation

- 6.4.5 Samsung Electronics Co. Ltd.

- 6.4.6 Cisco Systems Inc.

- 6.4.7 CommScope Inc. (incl. Airvana)

- 6.4.8 American Tower Corporation

- 6.4.9 Qualcomm Technologies Inc.

- 6.4.10 ATandT Inc.

- 6.4.11 Verizon Communications Inc.

- 6.4.12 Crown Castle International Corp.

- 6.4.13 Airspan Networks Holdings Inc.

- 6.4.14 Qucell Inc.

- 6.4.15 Cirrus Core Networks

- 6.4.16 Casa Systems Inc.

- 6.4.17 Sercomm Corporation

- 6.4.18 Baicells Technologies

- 6.4.19 Comba Telecom Systems Holdings Ltd.

- 6.4.20 IP.Access Ltd.

- 6.4.21 Boingo Wireless Inc.

- 6.4.22 Parallel Wireless Inc.

- 6.4.23 JMA Wireless

- 6.4.24 Corning Inc. (SpiderCloud)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment