|

시장보고서

상품코드

1850329

G단백질 결합 수용체 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global G-Protein Coupled Receptors (GPCR) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

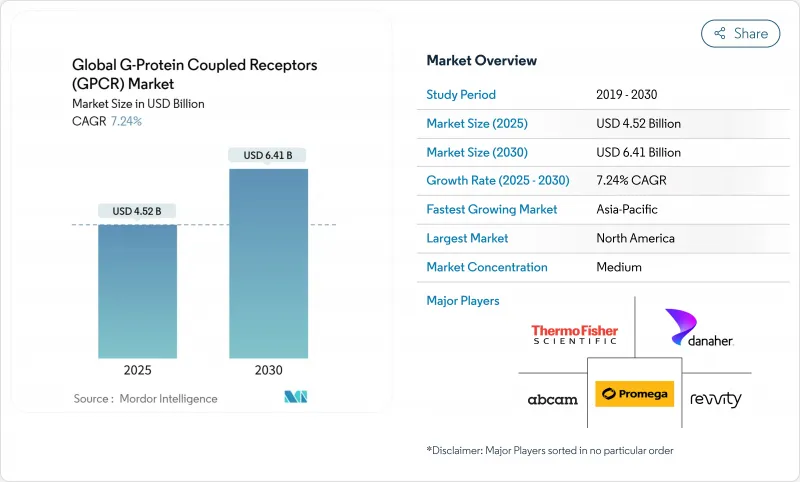

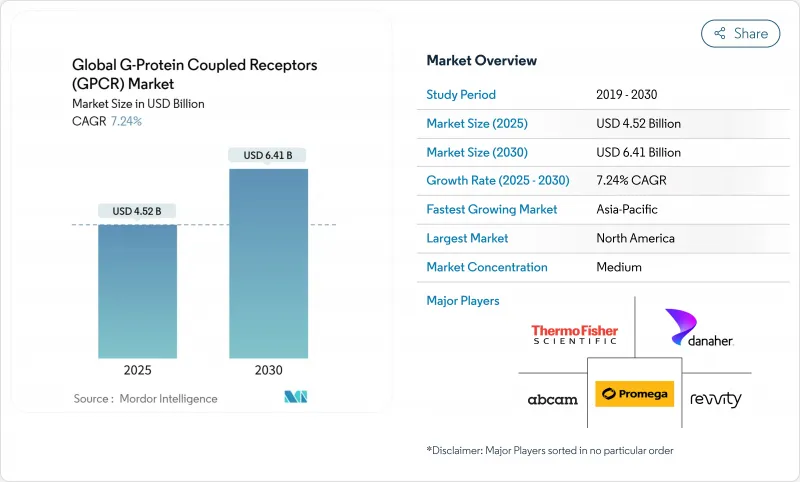

G단백질 결합 수용체 시장 규모는 2025년에 45억 2,000만 달러로, 2030년에는 64억 1,000만 달러에 달할 것으로 예상되어 CAGR 7.24%를 나타낼 전망입니다.

AlphaFold2 모델을 기반으로 한 구조 유도 설계의 채용이 증가하고 대응 가능한 수용체 영역이 확대되는 반면, 경구 저분자 GLP-1 프로그램은 벤처 기업의 자금 조달 기세를 유지하고 새로운 제휴 구조를 촉매하고 있습니다. 북미 스폰서가 계속 신청 건수를 독점하고 있지만, 각국 정부가 심사 기준을 갖추어 트랜스레이셔널 인프라에 조성금을 내고 있기 때문에 아시아태평양의 실험실이 가장 급속히 규모를 확대하고 있습니다. 암 영역이 최대의 치료 실적을 유지하고 있지만, 알로스테릭 디스커버리의 돌파구를 배경으로 심혈관계 프로젝트가 가장 급 가속하고 있습니다. 전반적으로 G단백질 결합 수용체 시장은 모듈형 플랫폼의 혁신, 경쟁 격화 완화, 퍼스트 인 클래스 타겟 풀의 확대로부터 혜택을 누리고 있습니다.

세계의 G단백질 결합 수용체 시장 동향과 인사이트

GPCR 분석에서 HTS 플랫폼 채택 급증

높은 처리량 스크리닝 장비는 동위 원소의 취급을 필요로하지 않는 스폰서가보다 신속하고 라벨없는 리드 아웃을 요구하기 때문에 수동 방사성 리간드 방법을 대체합니다. 생물 발광 공명 에너지 이동 센서는 실시간으로 컨포메이션 변화를 포착하여 감도를 더욱 향상시키고, 임피던스 기반 마이크로 전극 어레이는 패치 클램프 데이터와 0.85의 상관 관계를 갖는 전기 생리학적 반응의 비침습적 프록시를 제공합니다. 공급업체의 로드맵은 미량 분배를 위한 로봇 공학과 리간드 히트를 자동으로 순위화하는 클라우드 분석을 통합합니다. 이러한 진보가 결합되어 G단백질 결합 수용체 시장은 정밀 약리학 프로젝트를 위한 비옥한 토양으로 강화되고 있습니다.

GPCR을 표적으로 하는 창약 지출 증가

G단백질 결합 수용체는 승인 약물의 36%를 지원하지만, 수용체 아형의 4분의 3은 아직 시판되지 않았기 때문에 지속적인 R&D 할당을 촉진하고 있습니다. 당뇨병 치료제와 비만 치료제만으로도 2024년 매출액이 300억 달러 가까이에 이르러 상업적인 업사이드가 검증되어 경구 저분자 GLP-1, 아밀린, 이중 차단제 후보에 예산이 돌았습니다. 스트럭처 세라퓨틱스는 2b 단계의 GLP-1 및 GIPR 프로그램에 8억 8,350만 달러의 현금을 투입하고 있으며, 그 규모를 이야기하고 있습니다. 노보 노르디스크와 세프테르나와의 제휴는 경구 비만 치료제로서 최대 22억 달러로 평가되고 있습니다. 이러한 자금의 흐름은 당분간 파이프라인을 지지하고 G단백질 결합 수용체 시장을 주요 제약회사의 전략적 우선순위로 확고히 하고 있습니다.

GPCR의 정제 및 안정성 문제

멤브레인 단백질은 지질 이중 막에서 꺼내지면 원래의 형태를 잃어 결정학과 생물 물리학 분석을 복잡하게합니다. 세정제에 의한 가용화는 종종 안정화 지질을 제거하기 때문에 네이티브 나노디스크를 보유하는 스티렌-말레산 공중합체의 채용을 촉진하고 있습니다. 최근의 기술 혁신은 Ga 모방 펩티드를 크로마토그래피 수지에 결합시켜, 분취 스케일에서 활성 수용체의 태그가 없는 단리를 가능하게 하였습니다. 그럼에도 불구하고 GPCR의 하위 유형별로 맞춤형 열 안정화 사이클이 필요하기 때문에 플랫폼 표준화가 지연되고 G단백질 결합 수용체 시장의 단기 효율 향상에는 이어지지 않습니다.

부문 분석

시약 및 키트는 GPCR 탐색 워크플로의 백본을 제공하여 2024년 G단백질 결합 수용체 시장 점유율의 36.44%를 차지했습니다. 이는 버퍼, 리간드, 검출 화학물질에 대한 보편적인 수요를 반영합니다. 자동 리퀴드 핸들러, 포토닉 리더 및 임피던스 모듈은 플랫폼 카테고리를 구성하며 소형화 및 클라우드 링크 애널리틱스 덕분에 CAGR 8.92%로 상승하고 있습니다. AI 알고리즘과 광학 센서의 융합을 통해 단일 워크스테이션에서 엔드 투 엔드 히트 트리어지가 가능하며 리드 타임이 단축되고 중견기업도 쉽게 액세스할 수 있습니다.

의약품 스폰서가 자체 셀 뱅크와 분석 라이브러리를 보유한 CRO에 높은 컨텐츠 스크리닝을 위탁함에 따라 서비스 계약이 확대되고 있습니다. 예를 들어, Eurofins CEREP는 20년 동안 수용체 약리학의 노하우와 고밀도 스크리닝 라인을 결합하여 고객의 프로그램 일정을 단축하고 있습니다. 하이브리드 서비스는 시약, 플레이트 및 분석 라이선스를 구독 모델로 번들하여 실험실이 자본 지출을 프로젝트 이정표에 맞출 수 있도록 합니다. 그 결과 플랫폼과 서비스 생태계는 G단백질 결합 수용체 시장의 가치 전환을 지원합니다.

세포내 칼슘 동원 키트는 클래스 A 수용체 프로그램의 역사적 역할을 반영하여 2024년 매출을 28.71%로 견인했습니다. 한편, cAMP 검출 키트의 CAGR은 9.01%로 예측되고 있으며, 이는 생세포 중의 사이클릭 AMP를 나노몰 이하의 감도로 정량하는 NanoLuc 바이너리 기술에 지지되고 있습니다. 라디오 리간드와 GTPYS 법은 방사성 동위 원소 폐기물에 관한 규제 압력이 더 넓은 범위에서의 흡수를 억제하고있는 것, 직교 확인을 위해 견뎌냅니다.

B-아레스틴 바이오센서는 심대사계 안전성 프로파일링에 관여하는 경로 때문에 계속 보급되어 라벨이 없는 임피던스 플레이트는 형광 태그 없이 형태학적 변화를 기록하게 되었습니다. ThermoBRET 프로토콜은 표지 리간드를 제거하여 내열성 평가를 더욱 간소화하고 리드 최적화 시 소모품 비용을 절감합니다. 이러한 기술을 종합하면 G단백질 결합 수용체 시장에서 이용 가능한 기능 레퍼토리가 확대될 것입니다.

지역 분석

북미는 보스턴, 샌프란시스코, 샌디에고의 클러스터가 벤처 캐피탈, 인공지능 인력, 머신러닝에 의한 증거 패키지를 명확히 하는 FDA 지침을 결집해 2024년 매출의 37.43%를 차지했습니다. 국내 기존 기업은 매년 장비 업그레이드를 반복적으로 출시하고 있으며 사용자는 파괴적인 자본주기 없이 기존 실험실을 개조할 수 있습니다. 구조 생물학에 대한 수년간의 NIH의 자금 제공 흐름은 G단백질 결합 수용체 시장에서 이 지역의 우위를 더욱 강력하게 하고 있습니다.

유럽은 뛰어난 학술과 규제의 현실주의가 균형있게 혼합되어 있습니다. EMA에 의한 폐동맥 고혈압 치료제 Winrevair와 과활동 방광 치료제 Obgemsa의 승인은 2024년에 새로운 GPCR 치료제의 승인 경로를 확인했습니다. 바젤 대학과 같은 대륙의 연구 기관은 원자 분해능으로 수용체의 운동을 추적하는 GPS-NMR과 같은 엔벨로프 기술을 추진하고 있습니다. 이러한 요인들이 결합되어 G단백질 결합 수용체 시장의 유럽에서 견조한 성장 프로파일이 성장하고 있습니다.

2030년까지 연평균 복합 성장률(CAGR)이 8.85%로 예측되는 아시아태평양은 바이오테크놀러지의 자립을 강화하고 승인 스케줄을 조화시키려는 정부의 협조적인 움직임으로부터 혜택을 받고 있습니다. PCO371과 같은 세포내 활성화제의 발견은 이 지역의 창의 궁리를 나타내는 것으로, 전신성 부작용을 경감한 경구 투여 가능한 약제가 유망시되고 있습니다. 중국과 한국은 펩티드 치료제의 제조 능력을 확대하고 있으며, 벤처펀드는 다국적기업과 공동투자하여 지역의 시험시설을 가속화하고 있습니다. 라틴아메리카, 중동, 아프리카의 신흥국은 아직 규모는 작지만 기술이전협정을 통해 임상 인프라를 증강하고 있으며 G단백질 결합 수용체 시장에 미래의 공헌국으로 자리매김하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- GPCR 분석에서 HTS 플랫폼 채택 급증

- GPCR을 표적으로 한 창약 지출 증가

- 만성 질환 및 대사성 질환의 부담 증대

- 생물학적 제제와 알로스테릭 모듈레이터의 확대

- AI를 활용한 구조 유도 GPCR 모델링

- 경구 소분자 GLP-1 작용제의 VC 붐

- 시장 성장 억제요인

- GPCR의 정제와 안정성의 과제

- 시그널 바이어스의 복잡성이 어세이 설계를 방해

- 고급 분석 플랫폼의 고비용

- IP 클러스터링은 운용의 자유도를 제한

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 강도

제5장 시장 규모와 성장 예측

- 구성 요소별

- 시약 및 키트

- 세포주

- 분석 플랫폼

- 검출기기

- 서비스

- 어세이 유형별

- 칼슘 농도 검출 분석법

- 방사성 리간드 결합 및 GTP-S 분석

- cAMP 및 cGMP 분석

- B-아레스틴 기능 분석

- 리포터 유전자 분석

- 라벨 프리 임피던스 분석

- 기타 어세이 유형

- 치유 영역별

- 심혈관계

- 중추신경계

- 종양학

- 대사 장애

- 호흡기 질환

- 기타 치료 영역

- 최종 사용자별

- 제약 및 바이오테크놀러지 기업

- 계약 연구 기관(CRO)

- 학술 및 연구 기관

- 진단 실험실

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 경쟁 벤치마킹

- 시장 점유율 분석

- 기업 프로파일

- Abcam plc

- Addex Therapeutics Ltd.

- Becton, Dickinson and Company

- BioInvenu Inc.

- Bio-Rad Laboratories Inc.

- BMG Labtech GmbH

- Charles River Laboratories

- Cisbio

- Corning Incorporated

- Danaher Corporation

- Enzo Biochem Inc.

- Eurofins Scientific SE(DiscoverX)

- Evotec SE

- HD Biosciences Co., Ltd.

- ION Biosciences

- Luminex Corporation

- Merck KGaA

- Promega Corporation

- Reaction Biology Corp.

- Revvity Inc

- Structure Therapeutics Inc.

- Thermo Fisher Scientific Inc.

제7장 시장 기회와 향후 전망

KTH 25.11.10The G-protein coupled receptors market size stands at USD 4.52 billion in 2025 and is forecast to reach USD 6.41 billion by 2030, expanding at a 7.24% CAGR as artificial-intelligence tools replace legacy radioligand screens in early discovery workflows.

Increasing adoption of structure-guided design based on AlphaFold2 models is broadening the addressable receptor universe, while oral small-molecule GLP-1 programs sustain venture funding momentum and catalyze new partnership structures. North American sponsors continue to dominate filings, yet Asia Pacific laboratories are scaling fastest as governments align review standards and subsidize translational infrastructure. Oncology keeps the largest therapeutic footprint, but cardiovascular projects post the sharpest acceleration on the back of allosteric discovery breakthroughs. Overall, the G-protein coupled receptors market is benefiting from modular platform innovation, moderated competitive intensity and a widening pool of first-in-class targets.

Global G-Protein Coupled Receptors (GPCR) Market Trends and Insights

Surging Adoption of HTS Platforms for GPCR Assays

High-throughput screening instruments are replacing manual radioligand methods as sponsors demand faster, label-free read-outs that eliminate isotope handling. Bioluminescence resonance energy transfer sensors further improve sensitivity by capturing conformational shifts in real time, and impedance-based microelectrode arrays provide a non-invasive proxy for electrophysiological responses with 0.85 correlation to patch-clamp data. Vendor roadmaps integrate robotics for micro-volume dispensing and cloud analytics that rank ligand hits automatically. Together, these advances reinforce the G-protein coupled receptors market as a fertile ground for precision pharmacology projects.

Growing Drug-Discovery Spend Targeting GPCRs

G protein-coupled receptors (GPCRs) underpin 36% of approved medicines, yet three-quarters of receptor subtypes still lack marketed drugs, prompting sustained R&D allocations. Diabetes and obesity agents alone delivered nearly USD 30 billion in 2024 sales, validating the commercial upside and steering budgets toward oral small-molecule GLP-1, amylin and dual-agonist candidates. Structure Therapeutics illustrates the scale, carrying USD 883.5 million in cash earmarked for Phase 2b GLP-1 and GIPR programs. Licensing deals echo investor confidence, with Novo Nordisk's collaboration with Septerna valued at up to USD 2.2 billion for oral obesity pills. Such capital flows underpin the near-term pipeline and solidify the G-protein coupled receptors market as a strategic priority for big pharma.

Purification & Stability Challenges of GPCRs

Membrane proteins lose native conformation once removed from lipid bilayers, complicating crystallography and biophysical assays. Detergent solubilization often strips stabilizing lipids, prompting adoption of styrene-maleic-acid copolymers that preserve native nanodiscs. Recent innovations attach Ga-mimetic peptides to chromatography resin, enabling tag-free isolation of active receptors at preparative scale. Nevertheless, each GPCR subtype demands bespoke thermostabilization cycles, delaying platform standardization and tempering near-term efficiency gains in the G-protein coupled receptors market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Burden of Chronic & Metabolic Diseases

- Expansion of Biologics & Allosteric Modulators

- Signal-Bias Complexity Hampers Assay Design

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents and kits provided the backbone of GPCR discovery workflows and represented 36.44% of G-protein coupled receptors market share in 2024, reflecting universal demand for buffers, ligands and detection chemistries. Automated liquid handlers, photonic readers and impedance modules constitute the platform category, which is climbing at an 8.92% CAGR thanks to miniaturization and cloud-linked analytics. The convergence of AI algorithms with optical sensors now supports end-to-end hit triaging inside a single workstation, accelerating time-to-lead and widening access for mid-tier firms.

Service contracts are expanding as drug sponsors outsource high-content screens to CROs that maintain proprietary cell banks and assay libraries. Eurofins CEREP, for example, couples 20 years of receptor pharmacology know-how with high-density screening lines to shorten client program timelines. Hybrid offerings bundle reagents, plates and analytics licences under subscription models, allowing labs to align capital outlay with project milestones. Consequently, platforms and service ecosystems anchor the value shift within the G-protein coupled receptors market.

Intracellular calcium mobilization kits led revenues at 28.71% in 2024, mirroring their historic role in class-A receptor programs. Yet cAMP detection formats are projected to register a 9.01% CAGR, underpinned by NanoLuc binary technologies that quantify cyclic-AMP in live cells with sub-nanomolar sensitivity. Radioligand and GTPYS methods endure for orthogonal confirmation, although regulatory pressure on radioisotope waste curbs broader uptake.

B-arrestin biosensors continue to gain currency for pathways implicated in cardiometabolic safety profiling, and label-free impedance plates now record morphological changes without fluorescent tags. ThermoBRET protocols further streamline thermostability assessments by eliminating labelled ligands, trimming consumable costs during lead optimization. Collectively, these technologies extend the functional repertoire available to the G-protein coupled receptors market.

The G-Protein Coupled Receptors Market Report is Segmented by Component(Reagents & Kits and More), Assay Type (Calcium Level Detection Assays and More), Therapeutic Area (Cardiovascular System and More), End-User (Pharmaceutical & Biotech Companies and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 37.43% of 2024 sales as Boston, San Francisco and San Diego clusters combined venture capital, AI talent and FDA guidance that clarifies machine-learning evidence packages. Domestic incumbents release iterative instrumentation upgrades annually, enabling users to retrofit established laboratories without disruptive capital cycles. Long-standing NIH funding streams for structural biology further solidify the region's dominance within the G-protein coupled receptors market.

Europe contributes a balanced mix of academic excellence and regulatory pragmatism. EMA endorsements of Winrevair for pulmonary arterial hypertension and Obgemsa for overactive bladder verified the approval pathway for novel GPCR therapies in 2024. Continental institutes such as the University of Basel are pushing envelope techniques like GPS-NMR to trace receptor motions at atomic resolution, insights that feed directly into ligand engineering cycles. Combined, these factors nurture a robust albeit steady growth profile across the European slice of the G-protein coupled receptors market.

Asia-Pacific, projected at an 8.85% CAGR through 2030, benefits from concerted governmental drives to bolster biotech self-reliance and harmonize approval timelines. Japan's discovery of intracellular-side activators such as PCO371 exemplifies the region's ingenuity, promising orally available agents with reduced systemic side-effects. China and South Korea are expanding manufacturing capacity for peptide therapeutics, while venture funds co-invest with multinationals to accelerate regional trial sites. Emerging economies in Latin America, the Middle East and Africa remain smaller but are ramping clinical infrastructure via technology-transfer agreements, positioning themselves as future contributors to the G-protein coupled receptors market.

- Abcam

- Addex Therapeutics

- Beckton Dickinson

- BioInvenu

- Bio-Rad Laboratories

- BMG Labtech GmbH

- Charles River

- Cisbio

- Corning

- Danaher

- Enzo Biochem

- Eurofins Scientific SE (DiscoverX)

- Evotec

- HD Biosciences

- ION Biosciences

- Luminex

- Merck

- Promega

- Reaction Biology Corp.

- Revvity Inc

- Structure Therapeutics Inc.

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging adoption of HTS platforms for GPCR assays

- 4.2.2 Growing drug-discovery spend targeting GPCRs

- 4.2.3 Rising burden of chronic & metabolic diseases

- 4.2.4 Expansion of biologics & allosteric modulators

- 4.2.5 AI-enabled structure-guided GPCR modeling

- 4.2.6 VC boom in oral small-molecule GLP-1 agonists

- 4.3 Market Restraints

- 4.3.1 Purification & stability challenges of GPCRs

- 4.3.2 Signal-bias complexity hampers assay design

- 4.3.3 High cost of advanced assay platforms

- 4.3.4 IP clustering limits freedom-to-operate

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Reagents & Kits

- 5.1.2 Cell Lines

- 5.1.3 Assay Platforms

- 5.1.4 Detection Instruments

- 5.1.5 Services

- 5.2 By Assay Type

- 5.2.1 Calcium Level Detection Assays

- 5.2.2 Radioligand Binding & GTP?S Assays

- 5.2.3 cAMP & cGMP Assays

- 5.2.4 B-Arrestin Functional Assays

- 5.2.5 Reporter Gene Assays

- 5.2.6 Label-free Impedance Assays

- 5.2.7 Other Assay Types

- 5.3 By Therapeutic Area

- 5.3.1 Cardiovascular System

- 5.3.2 Central Nervous System

- 5.3.3 Oncology

- 5.3.4 Metabolic Disorders

- 5.3.5 Respiratory Diseases

- 5.3.6 Other Therapeutic Areas

- 5.4 By End-User

- 5.4.1 Pharmaceutical & Biotech Companies

- 5.4.2 Contract Research Organizations (CROs)

- 5.4.3 Academic & Research Institutes

- 5.4.4 Diagnostic Laboratories

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Abcam plc

- 6.4.2 Addex Therapeutics Ltd.

- 6.4.3 Becton, Dickinson and Company

- 6.4.4 BioInvenu Inc.

- 6.4.5 Bio-Rad Laboratories Inc.

- 6.4.6 BMG Labtech GmbH

- 6.4.7 Charles River Laboratories

- 6.4.8 Cisbio

- 6.4.9 Corning Incorporated

- 6.4.10 Danaher Corporation

- 6.4.11 Enzo Biochem Inc.

- 6.4.12 Eurofins Scientific SE (DiscoverX)

- 6.4.13 Evotec SE

- 6.4.14 HD Biosciences Co., Ltd.

- 6.4.15 ION Biosciences

- 6.4.16 Luminex Corporation

- 6.4.17 Merck KGaA

- 6.4.18 Promega Corporation

- 6.4.19 Reaction Biology Corp.

- 6.4.20 Revvity Inc

- 6.4.21 Structure Therapeutics Inc.

- 6.4.22 Thermo Fisher Scientific Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment