|

시장보고서

상품코드

1850343

유럽의 당뇨병 치료제 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Europe Diabetes Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

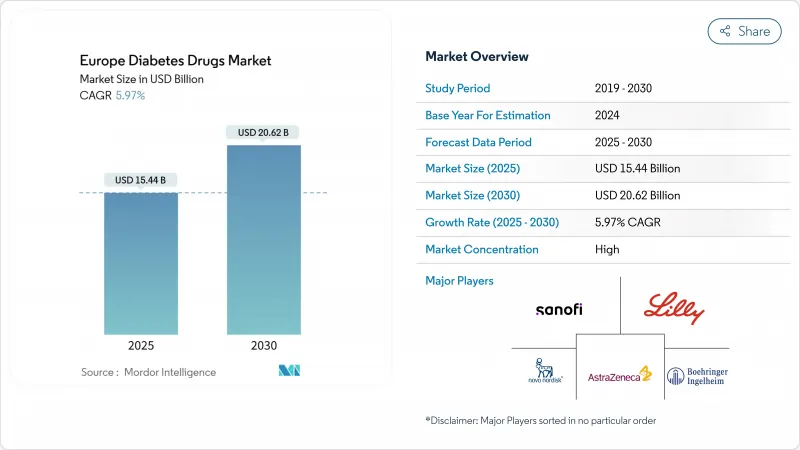

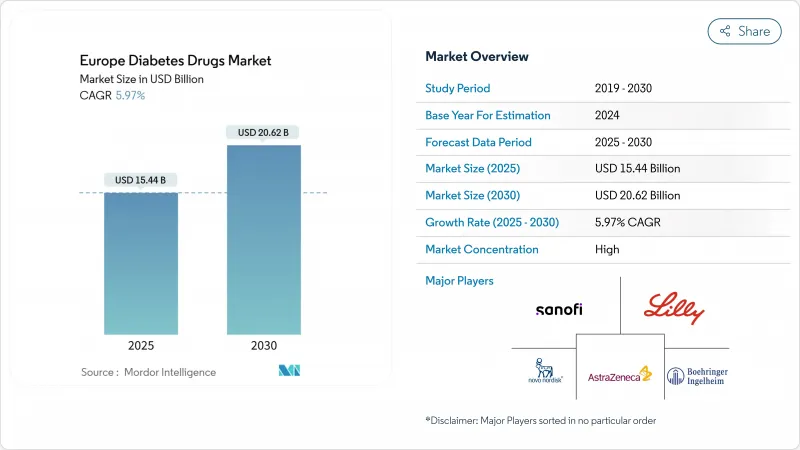

유럽 당뇨병 치료제 시장의 2025년 시장 규모는 154억 4,000만 달러, 예측 기간 중 CAGR은 5.97%를 나타내고, 2030년에는 206억 2,000만 달러에 이를 것으로 예측됩니다.

특히, 두 적응증 모두에 대응하는 GLP-1 수용체 작용제의 폭넓은 보급으로 비만과 당뇨병의 치료가 융합됨에 따라 수요가 확대되고 있습니다. 경구 항 당뇨병 약물은 SGLT-2 억제제와 경구 GLP-1 정제의 출현으로 치료 믹스를 지배하고 가장 빠르게 성장하는 클래스입니다. 조기 개입 프로그램에 의해 대응 가능한 환자층이 확대되고 있으며, 특히 당뇨병 예비군에서는 스크리닝의 대처가 많은 의료 시스템에서 주류가 되고 있습니다. 바이오시밀러 인슐린의 가격 저하와 GLP-1공급 부족으로 인한 생산 병목 현상화에 의해 EU 레벨에서의 규제 협조가 요구되게 되어 공급의 안전성이 요구되고 있습니다. 디지털 전환은 온라인 채널로의 유통 이동을 가속화하고 의약품과 승인된 디지털 치료제를 결합한 하이브리드 치료 모델로의 길을 열고 있습니다.

유럽 당뇨병 치료제 시장 동향과 통찰

당뇨병의 높은 부담과 GLP-1 비만의 크로스 오버 수요 급증

당뇨병과 비만의 유병률 증가는 치료의 우선순위를 바꾸고 있으며, GLP-1 수용체 작용제는 이 이동의 중심에 위치합니다. 이탈리아의 2024년 GLP-1 치료제에 대한 지출은 260억 유로에 달했으며, 그리스에서는 82.5%의 사용량 급증을 기록했으며, GLP-1 치료제의 이중 적응의 매력이 더욱 강해졌습니다. 수요의 급증은 여러 회원국에서 공급 부족을 일으켰고, 벨기에는 처방을 일시적으로 제한하고 독일은 수출 규제를 고려하게 되었습니다. 유럽의약청(EEA)은 이에 대해 용량계획을 의무화하고 적응외사용의 경계를 명확히 함으로써 하나의 치료제 클래스가 어떻게 지역의 정책에 영향을 미칠 수 있는지를 나타냈습니다. 제약 제조업체는 스케일 업 프로젝트를 가속화하고 있지만, 지속적인 공급 제약은 수요 증가와 생산 능력 사이의 수년간의 균형 조정을 시사하고 있습니다. 치료 알고리즘이 체중과 심신의 결과를 통합하게 된 현재, GLP-1의 급증은 연구 개발의 초점을 다제 병용형 제제와 경구 전달 제형으로 향하게 하는 것으로 보입니다.

전자 처방전에 의한 디지털 치료 번들

독일의 DiGA 패스웨이에서는 53개의 디지털 치료제가 상환되어 당뇨병 치료제가 상당한 비율을 차지하고 있습니다. 2형 당뇨병 환자의 89%가 HbA1c 목표치 7% 미만을 달성하고 약물 사용량을 74% 삭감한 것이 1년간의 실임상시험에서 밝혀졌으며, 생활습관의 지도에 그치지 않는 임상적 가치가 실증되고 있습니다. 성능 기반 결제 모델은 측정 가능한 결과에 상환을 연결하여 개발자의 알고리즘과 사용자 인터페이스의 개선 의지를 자극합니다. 그러나 의사와의 인터뷰는 시간적 제약에서 디지털 리터러시 평가에 이르기까지 도입 장애물이 높다는 것을 강조하고 있으며, 워크플로우 통합이 보다 광범위한 도입 결정자가 될 수 있음을 시사합니다. 독일의 성공은 북유럽 시장과 서유럽에서의 복제에 박차를 가하고 있으며, 제약회사는 디지털 툴을 치료의 연속성을 향상시키는 보완적인 수익원으로 생각하게 되었습니다.

중국에 과도하게 의존하는 원료 공급망

COVID-19의 유행은 유럽이 중국의 원료 공장에 의존하고 있음을 드러냈습니다. 이 취약점은 공공 부문이 재 쇼어링을 부르고 있음에도 불구하고 여전히 해결되지 않았습니다. 높은 자본 비용, 전문가 인력 부족, 복잡한 규제가 현지 생산 확대를 방해합니다. 노보놀디스크가 덴마크에서 진행하고 있는 23억 달러의 확장은 2029년 이후 국내 생산능력을 추가할 예정이지만, 세마글루티드는 이 확장에서 제외된 채로 있습니다. 당분간 지정 학적 또는 유행성 관련 혼란이 있으면 일반 메트포르민과 인슐린 공급이 억제 될 수 있으며 의료 시스템은 응급 조달 프로토콜을 시작해야합니다.

부문 분석

경구 항당뇨병제는 2024년 유럽 당뇨병 치료제 시장 전체 매출의 66.34%를 차지하며, 이 부문은 2030년까지 연평균 복합 성장률(CAGR) 6.74%로 확대될 것으로 예측되며, 신규 SGLT-2 및 경구 GLP-1 제형의 견인역으로서 리더십을 유지합니다. 구강 치료제의 유럽 당뇨병 치료제 시장 규모는 편의성, 어드히어런스, 우수한 결과 데이터가 처방을 촉진하기 때문에 더욱 확대될 것으로 보입니다. GLP-1 아날로그 제제를 중심으로 하는 비인슐린 주사제는 여전히 2위 시장 규모를 유지하고 있지만, 각국의 규제 당국이 배급을 통해 계속 관리하고 있는 지속적인 공급 부족으로 인해 성장이 멈추고 있습니다. 인슐린의 매출은 바이오시밀러에 의한 침식의 압력하에 있지만, 주 1회 제제나 포도당 감수성 제제의 기술 혁신에 의해 2020년대 후반까지는 회복할 가능성이 있습니다. 또한, 틸제파티드와 같은 듀얼 효능제는 임상시험에서 HbA1c를 최대 2.06% 감소시키고 체중을 2자리 감소시켰습니다.

새로운 다중 작용제 및 포도당 반응성 인슐린 제형은 치료 히에랄 키를 재정의할 수 있습니다. 연구 중 카글리린타이드와 세마글루티드의 병용 요법은 12주 동안 14kg의 체중 감소와 1.8%의 HbA1c 감소를 달성하여 이용 가능한 대부분의 요법을 능가했습니다. 이러한 효과는 심혈관 사건과 신장 사건에서 비용 상쇄가 입증되면 지불자가 더 높은 정가에 관용할 수 있도록 촉구합니다. 한편, NNC2215와 같은 포도당 민감성 후보 약물은 치료 계속의 중요한 결정 요인인 저혈당 위험을 완화하는데 유망합니다. 전반적으로 R&D 파이프라인은 바이오시밀러가 레거시 분자를 장기적인 가격 부담에 노출하더라도 유럽의 당뇨병 치료제 시장이 혁신 집약적임을 시사합니다.

2형 당뇨병은 2024년 유럽 당뇨병 치료제 시장에서 지출의 90.01%를 차지하며, 이는 대륙 전체의 인구동태의 고령화와 라이프 스타일의 패턴을 반영하고 있습니다. 그러나 조기 발견 프로그램은 개입의 폭이 넓어져 저용량 요법이나 생활 습관과 관련된 치료가 지지되고 있기 때문에 당뇨병 예비군의 카테고리가 CAGR 7.44%로 보다 급속히 증가하고 있습니다. 예방에 관한 유럽 당뇨병 치료제 시장 규모 예측은 큰 여지를 보여줍니다. HbA1c와 신장의 연간 스크리닝 가이드라인 준수율은 일부 국가에서는 여전히 50% 미만이며, 준수율이 개선되면 성장 가능성이 있음을 시사합니다. 1형 당뇨병 시장 규모는 비교적 작지만, 폐쇄 루프 인슐린 전달로의 전환이 기술 주도로 진행되고 있으며, 필요한 투여량을 억제하고 장기적인 약량에 영향을 미칠 수 있습니다.

예방경제학은 정책 입안자들에게 설득력을 늘리고 있으며, 비용효과 분석은 약물 치료의 확대보다 자금이 제공된 디지털 코칭 플랫폼을 지지하고 있습니다. 2023년에 업데이트된 임상 가이드라인은 심신계에 대한 유익성이 입증된 GLP-1 및 SGLT-2 제형을 권장하고, 클래스 톱 분자로의 전환을 강화하고 있습니다. 이 변화는 다장기 보호 특성을 가진 약물의 프리미엄 가격을 지원하고 유럽 당뇨병 치료제 시장 전망 수익의 다양성을 지원합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 당뇨병과 GLP-1 비만의 크로스 오버 수요의 급증에 의한 부담 증가

- 전자 처방전에 의한 디지털 치료 번들

- EU 전체의 조기 CKD 스크리닝 가이드 라인

- 바이오시밀러 인슐린 가격 경쟁 물결

- 지불자에 의한 ESG 연동형 처방전 입찰

- 경구 저분자 인슐린의 돌파구

- 시장 성장 억제요인

- API 공급망의 중국에 대한 과도한 의존

- GLP-1 용량의 병목과 할당 상한

- SGLT2DKA의 안전성에 관한 경고의 상승

- 분산형 헬스케어 예산의 긴축 재정

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 약제 클래스별

- 인슐린

- 기초/장시간 작용형

- 볼러스/속효성

- 인간의 전통

- 바이오시밀러

- 경구 당뇨병약

- Biguanides

- SGLT-2 억제제

- DPP-4 억제제

- Sulfonylureas

- 비인슐린 주사제

- GLP-1 RA

- 아밀린 유사체

- 병용약

- 인슐린

- 당뇨병유형별

- 유형 1

- 유형 2

- 투여 경로별

- 오랄

- 피하 주사

- 흡입

- 이식형/경피형

- 유통 채널별

- 병원 약국

- 소매 약국

- 온라인 약국

- 지역

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Novo Nordisk A/S

- Sanofi

- Eli Lilly

- Boehringer Ingelheim

- AstraZeneca

- Merck & Co.

- Wockhardt

- Takeda

- Janssen(J&J)

- Astellas

- Novartis

- MannKind

- Viatris

- Recordati

- Servier

- Lupin

- Sun Pharma

제7장 시장 기회와 장래의 전망

SHW 25.11.11The Europe diabetes drugs market is valued at USD 15.44 billion in 2025 and is projected to reach USD 20.62 billion by 2030, reflecting a CAGR of 5.97% during the forecast period.

Demand is expanding as obesity and diabetes care converge, especially through the broad uptake of GLP-1 receptor agonists that serve both indications.Oral anti-diabetics dominate the treatment mix and are also the fastest-growing class, thanks to SGLT-2 inhibitors and the emergence of oral GLP-1 tablets. Early intervention programs are expanding the addressable patient base, most visibly in the pre-diabetes cohort where screening initiatives are now mainstream across many health systems. Supply security has come under scrutiny as biosimilar insulin erodes prices and GLP-1 shortages expose production bottlenecks, prompting regulatory coordination at EU level. Digital transformation is accelerating distribution shifts toward online channels and is paving the way for hybrid therapy models that pair medicines with approved digital therapeutics.

Europe Diabetes Drugs Market Trends and Insights

High Burden of Diabetes and GLP-1 Obesity Cross-over Demand Surge

Escalating prevalence of both diabetes and obesity is reshaping therapy priorities, and GLP-1 receptor agonists sit at the epicenter of this shift. Italy's 2024 spending on GLP-1 drugs reached EUR 26 billion, while Greece posted an 82.5% usage spike, reinforcing the medicines' dual-indication appeal. Surging demand triggered shortages across multiple member states, prompting Belgium to restrict prescriptions temporarily and Germany to weigh export curbs. The European Medicines Agency responded by mandating capacity plans and clarifying off-label use boundaries, demonstrating how one therapeutic class can influence regional policy. Pharma manufacturers are accelerating scale-up projects, yet persistent supply constraints hint at a multiyear balancing act between escalating demand and production capabilities. As treatment algorithms now integrate weight and cardio-renal outcomes, the GLP-1 surge will continue to redirect R&D focus toward multi-agonist and oral delivery formulations.

Digital-Therapeutic Bundling with E-Prescriptions

Germany's DiGA pathway reimburses 53 digital therapeutics, with diabetes applications making up a substantial share. One-year real-world studies show 89% of type 2 patients reached HbA1c targets below 7% and reduced medication use by 74%, underlining clinical value beyond lifestyle coaching. Performance-based payment models tie reimbursement to measurable outcomes, motivating developers to refine algorithms and user interfaces. Physician interviews, however, highlight onboarding hurdles ranging from time constraints to digital literacy assessments, suggesting that workflow integration will be decisive for broader adoption. Success in Germany is spurring replication across Nordic markets and Western Europe, and pharmaceutical firms increasingly view digital tools as complementary revenue streams that improve persistence on therapy.

API Supply-Chain Over-Reliance on China

The COVID-19 pandemic exposed Europe's dependence on Chinese active pharmaceutical ingredient plants, a vulnerability that remains unresolved despite public-sector calls for reshoring. High capital costs, specialist talent shortages, and complex regulation hamper local build-out. Novo Nordisk's USD 2.3 billion expansion in Denmark will add domestic capacity from 2029, yet semaglutide remains excluded from the build. In the interim, any disruption-geopolitical or pandemic-related-can curtail generic metformin or insulin supply, forcing health systems to activate emergency procurement protocols.

Other drivers and restraints analyzed in the detailed report include:

- EU-wide Early CKD Screening Guidelines

- Biosimilar Insulin Price-Competition Wave

- GLP-1 Capacity Bottlenecks & Allocation Caps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oral anti-diabetics captured 66.34% of total 2024 sales within the Europe diabetes drugs market, and this segment is forecast to expand at a 6.74% CAGR through 2030, maintaining its leadership as new SGLT-2 and oral GLP-1 agents gain traction. The Europe diabetes drugs market size for oral treatments is set to widen further as convenience, adherence, and superior outcome data drive prescribing. Non-insulin injectables, anchored by GLP-1 analogues, remain the second-largest class; however, their growth is capped by ongoing shortages that national regulators continue to manage through rationing. Insulin revenue is under pressure from biosimilar erosion, but innovation in once-weekly and glucose-sensitive preparations offers a potential rebound by the late 2020s. In addition, dual agonists such as tirzepatide demonstrated HbA1c reductions up to 2.06% and double-digit weight losses in clinical studies, signalling another wave of therapy upgrades.

Emerging multi-agonists and glucose-responsive insulins could redefine the therapeutic hierarchy. Investigational pairing of cagrilintide with semaglutide achieved 14 kg weight loss and 1.8% HbA1c decline over 12 weeks, outperforming most available regimens. Such efficacy encourages payer openness to higher list prices when demonstrable cost offsets in cardiovascular and renal events are evident. Meanwhile, glucose-sensitive candidates like NNC2215 show promise in mitigating hypoglycemia risk, a key determinant of therapy persistence. Overall, R&D pipelines suggest that the Europe diabetes drugs market will remain innovation-intensive, even as biosimilars put legacy molecules under long-term pricing strain.

Type 2 diabetes represents 90.01% of 2024 spending within the Europe diabetes drugs market, reflecting demographic aging and lifestyle patterns across the continent. Yet, the pre-diabetic category is rising faster, at a 7.44% CAGR, as early detection programs enlarge intervention windows and favor lower-dose or lifestyle-linked therapies. Europe diabetes drugs market size projections for prevention indicate significant headroom: guideline adherence to annual HbA1c and kidney screening remains below 50% in several countries, implying growth potential once compliance improves. Type 1 diabetes, while comparatively small, is experiencing technology-driven shifts toward closed-loop insulin delivery, which may curb dose requirements and influence long-term drug volumes.

Prevention economics has become more persuasive to policymakers, with cost-effectiveness analyses favoring funded digital coaching platforms ahead of pharmacologic escalation. Clinical guidelines updated in 2023 recommend GLP-1 and SGLT-2 agents where cardio-renal benefit is proven, reinforcing migration toward class-leading molecules. This shift supports premium pricing for drugs with multi-organ protection attributes, anchoring future revenue diversity for the Europe diabetes drugs market.

The Europe Diabetes Drugs Market Report is Segmented by Drug Class (Insulins [Basal/Long-acting and More], Oral Anti-Diabetics [Biguanides and More], Non-Insulin Injectable Drugs, Combination Drugs), Diabetes Type (Type-1 and Type-2), Rout of Administartion (Oral, Inhaled and More), Distribution Channel (Hospital Pharmacies, Retail Pharmacies and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Novo Nordisk

- Sanofi

- Eli Lilly and Company

- Boehringer Ingelheim

- AstraZeneca

- Merck

- Wockhardt

- Takeda Pharmaceuticals

- Janssen (J&J)

- Astellas Pharma

- Novartis

- MannKind

- Viatris

- Recordati

- Servier

- Lupin

- Sun Pharmaceuticals Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Burden of Diabetes and GLP-1 Obesity Cross-over Demand Surge

- 4.2.2 Digital-Therapeutic Bundling with E-prescriptions

- 4.2.3 EU-wide Early CKD Screening Guidelines

- 4.2.4 Biosimilar Insulin Price-Competition Wave

- 4.2.5 ESG-linked Formulary Tenders by Payers

- 4.2.6 Oral Small-molecule Insulin Breakthroughs

- 4.3 Market Restraints

- 4.3.1 API Supply-chain Over-reliance on China

- 4.3.2 GLP-1 Capacity Bottlenecks & Allocation Caps

- 4.3.3 Rising SGLT-2 DKA Safety Warnings

- 4.3.4 Decentralised Healthcare Budget Austerity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Drug Class

- 5.1.1 Insulins

- 5.1.1.1 Basal/Long-acting

- 5.1.1.2 Bolus/Fast-acting

- 5.1.1.3 Human traditional

- 5.1.1.4 Biosimilar

- 5.1.2 Oral Anti-diabetics

- 5.1.2.1 Biguanides

- 5.1.2.2 SGLT-2 inhibitors

- 5.1.2.3 DPP-4 inhibitors

- 5.1.2.4 Sulfonylureas

- 5.1.3 Non-Insulin Injectables

- 5.1.3.1 GLP-1 RAs

- 5.1.3.2 Amylin Analogues

- 5.1.4 Combination Drugs

- 5.1.1 Insulins

- 5.2 By Diabetes Type

- 5.2.1 Type-1

- 5.2.2 Type-2

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.2 Sub-cutaneous Injection

- 5.3.3 Inhaled

- 5.3.4 Implantable/Transdermal

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.5 Geography

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Novo Nordisk A/S

- 6.3.2 Sanofi

- 6.3.3 Eli Lilly

- 6.3.4 Boehringer Ingelheim

- 6.3.5 AstraZeneca

- 6.3.6 Merck & Co.

- 6.3.7 Wockhardt

- 6.3.8 Takeda

- 6.3.9 Janssen (J&J)

- 6.3.10 Astellas

- 6.3.11 Novartis

- 6.3.12 MannKind

- 6.3.13 Viatris

- 6.3.14 Recordati

- 6.3.15 Servier

- 6.3.16 Lupin

- 6.3.17 Sun Pharma

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment