|

시장보고서

상품코드

1850368

데이터 거버넌스 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Data Governance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

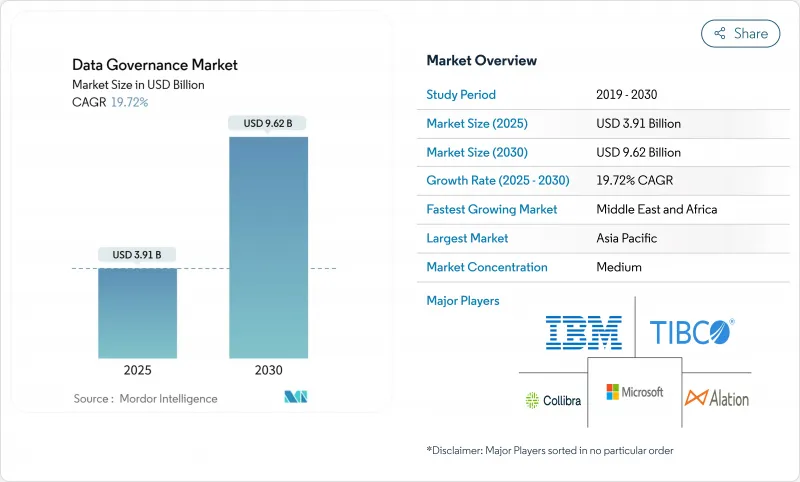

데이터 거버넌스 시장 규모는 2025년에 39억 1,000만 달러, 2030년에는 96억 2,000만 달러에 이르고, 예측기간동안 연평균 복합 성장률(CAGR) 19.72%로 성장할 것으로 예상됩니다.

급증의 배경에는 규제 강화, 클라우드 도입 가속, 신뢰성 높은 AI, 실시간 결제, 국경을 넘는 상거래에는 적절하게 관리되는 데이터가 필수적이라는 인식이 커지면서 뒷받침되고 있습니다. 금융기관, 의료 제공자 및 제조업체는 정보 유출에 대한 벌칙이 강화되고 비즈니스 모델이 데이터 수익화로 전환함에 따라 투자를 확대하고 있습니다. 공급업체는 분류 작업을 자동화하기 위해 계보 도구 및 카탈로그 도구에 AI를 통합하는 한편, 소블린 클라우드 및 하이브리드 아키텍처를 지원하는 배포 유연성을 강조합니다. 따라서 데이터 거버넌스 시장은 컴플라이언스에 특화된 포인트 솔루션에서 분산된 데이터 자산 전체의 품질, 보안 및 어카운빌리티를 오케스트레이션하는 통합 플랫폼으로 진화하고 있습니다.

세계 데이터 거버넌스 시장 동향과 통찰

설명 가능한 데이터 연계를 요구하는 EU AI 방법과 세계 AI 규정

2024년 8월에 발효된 EU AI법은 고위험 AI를 도입하는 기업에게 데이터의 기원, 변환, 품질 지표를 문서화할 것을 의무화하고 있습니다. 이에 실패하면 최고 3,982만 달러(세계 매출의 7%)의 벌금이 부과될 수 있기 때문에 기업은 엔드 투 엔드 데이터 흐름을 설명하는 고급 리니지 플랫폼을 도입할 필요가 있습니다. 공급업체는 모델 수준의 메타데이터를 기존 카탈로그 시스템과 통합하여 감사자가 교육 세트를 추적하고 바이어스를 감지할 수 있도록 합니다. 다국적 기업은 브라질과 캐나다에서도 유사한 규정을 마련하고 컴플라이언스가 세계 요구 사항이 될 것으로 예상했습니다. 이러한 압력은 데이터세트, 모델 및 비즈니스 성과를 단일 거버넌스 작업공간으로 연결하는 툴에 대한 수요를 높이고 있습니다. 그 결과 데이터 거버넌스 시장은 AI 감시와 기존의 스튜어드십 기능을 융합시킨 솔루션으로 전환하고 있습니다.

FedNow와 실시간 지불 레일 북미 BFSI로 서브 밀리 초 데이터 무결성을 강제로 실현

FedNow 서비스는 2023년 7월에 가동되었으며 현재는 은행 전체에서 24시간 365일 가동 중입니다. 밀리초 단위로 결제하려면 거래를 정체하지 않고 자금 세탁 방지 검사를 만족시키기 위해 원시 데이터 품질과 지속적인 계보가 필요합니다. 금융기관은 AI를 활용한 스크리닝과 인리치먼트 파이프라인을 도입하고, 이상이 있으면 즉시 경고를 발행합니다. 전통적인 일괄 지향 컴플라이언스 스택에서는 따라 잡지 못하기 때문에 은행은 메타 데이터 리포지토리를 현대화하고 제어 테스트를 자동화합니다. 이러한 움직임은 결제 워크 플로에 직접 규칙을 통합 할 수있는 클라우드 네이티브 거버넌스 공급업체의 구독 수익을 가속화합니다. 또한 리니지 툴을 메인프레임 코어에 뒷받침하는 것을 목적으로 한 컨설팅 계약에도 박차가 걸리고, 보다 광범위한 데이터 거버넌스 시장 중에서도 유리한 틈새 분야가 되고 있습니다.

엔터프라이즈 규모의 데이터 연계 도구의 높은 총 소유 비용

Tier 1 은행은 엔터프라이즈 리니지 플랫폼을 배포할 때 라이선스, 통합 및 하드웨어 리프레시를 위해 연간 수백만 달러의 지출에 어려움을 겪고 있습니다. 아르트 대학의 설문조사는 레거시 시스템과의 통합과 표준 부재로 인해 일정과 예산이 부풀어 오르는 것으로 확인되었습니다. 경비 절감을 위해 수작업 매핑에 의존하는 기관도 있으며, 본격적인 도입이 지연되고 있습니다. 벤더는 모듈 가격과 소비 기반의 클라우드 버전에서 지원하지만 스티커 충격은 데이터 거버넌스 시장 확대의 큰 브레이크가되었습니다.

부문 분석

소프트웨어 솔루션은 2024년 매출의 57.1%를 차지하며 정책 자동 적용, 메타데이터 획득, 계통 시각화 등의 기능으로 데이터 거버넌스 시장을 지원합니다. AI에 의한 분류와 이상 감지는 이제 기본 기능이며 기업이 EU의 AI법이나 FedNow 지령에 실시간으로 준거하는 데 도움이 되고 있습니다. 소프트웨어 데이터 거버넌스 시장 규모는 공급업체가 AI 파이프라인을 감사하는 모델 거버넌스 모듈을 통합함에 따라 확장될 것으로 예측됩니다.

구현, 교육 및 관리 운영을 포함한 서비스는 CAGR 23.4%로 확대될 것으로 예측됩니다. 인력 부족과 규제의 복잡화로 인해 기업은 프레임워크 설계와 일상적인 관리를 아웃소싱하는 경향이 있습니다. 관리형 서비스 제공업체는 데이터 품질과 동의 준수를 위한 SLA를 중복하여 세분화된 서비스 분야에서 차별화를 도모하고 있습니다.

서비스의 성장은 업계 특유의 권고 패키지에 의해 뒷받침됩니다. 은행 고객은 BCBS 239를 지원하는 수익 가속기를 요청하고, 건강 고객은 HIPAA 지원 템플릿을 요청합니다. 이러한 수직 맞춤화는 세계 시스템 통합사업자와 함께 부티크형 컨설턴트 회사에 여지가 있습니다. 결과적으로 데이터 거버넌스 시장은 순수한 라이선싱 모델에서 복잡한 경상 수익 스트림으로 계속 전환하고 있습니다.

금융서비스와 헬스케어 기업이 기밀기록의 로컬 관리를 고집하는 가운데 2024년 On-Premise 도입 점유율은 53.6%를 유지했습니다. 메인프레임과의 공존 및 규제 대상 워크로드는 기업의 SaaS로의 전환이 진행되고 있음에도 불구하고 데이터센터에 대한 선호를 강화하고 있습니다. On-Premise 솔루션의 데이터 거버넌스 시장 점유율은 클라우드 보안 인증이 확대됨에 따라 점차 감소할 것으로 예측됩니다.

클라우드 거버넌스 툴의 CAGR은 22.8%를 나타내고, 소블린 클라우드의 의무화와 원격 워크 규범이 그 원동력이 되고 있습니다. EDM Council의 CDMC와 같은 프레임워크는 감사인을 안심시키는 모범 사례를 제공합니다. 하이브리드 패턴이 지배적입니다 : 기밀성이 높은 골든 레코드는 On-Premise에 놓고 카탈로그 검색, 품질 규칙, 보고는 클라우드에서 실행됩니다. 공급업체는 사이트 간에 일관된 관리를 유지하는 크로스플레인 정책 오케스트레이션에서 경쟁하고 있습니다.

데이터 거버넌스 시장은 구성요소(소프트웨어, 서비스), 배포(클라우드, On-Premise), 조직 규모(대기업, 중소기업), 비즈니스 기능(IT 및 운영, 법률 및 규정 준수 등), 용도(컴플라이언스 관리, 위험 관리 등), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), IT 및 통신 등), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역 분석

북미는 성숙한 디지털 변혁에 대한 투자와 FedRAMP에 정합한 거버넌스를 중시하는 연방 엔터프라이즈 아키텍처 등의 프레임워크에 의해 지원되고 있으며, 2024년 매출은 35.6%를 차지했습니다. FedNow의 통합을 서두르는 금융 기관은 규제 기한이 지출을 촉진한다는 것을 보여줍니다. 미국 표준기술연구소에 의한 AI의 안전성에 관한 룰 만들기는 플랫폼 강화에 더욱 박차를 가하고 있습니다. 이 지역의 데이터 거버넌스 시장 규모는 스튜어드십 기능을 네이티브에 통합하는 컨설턴트와 하이퍼스케일 클라우드 프로바이더의 에코시스템이 밀집되어 있는 것이 장점이 되고 있습니다.

아시아는 CAGR 26.3%로 가장 빠르게 성장하는 지역입니다. 인도의 DPDP법은 데이터 흐름을 재구성하고 중국의 데이터 수출에 관한 네거티브 리스트 초안에서는 로컬 호스팅 요건이 강화되고 있습니다. 이러한 법령은 지역별 보존 정책을 시행할 수 있는 소블린 클라우드 카탈로그에 대한 투자를 촉진합니다. 일본과 한국은 기존의 법령을 세계 벤치마크에 맞추어 개량하여 국경을 넘은 연계를 강화하고 있습니다. 다국적 기업은 지역별 거버넌스 클러스터를 예산화하고 대응 가능한 데이터 거버넌스 시장을 확대합니다.

유럽은 GDPR(EU 개인정보보호규정)과 새롭게 제정된 EU AI법에 의해 큰 규모를 유지하고 있습니다. 유럽의 데이터 거버넌스 방법은 건강, 에너지 및 이동성 분야별 데이터 공간을 자극하고 상호 운용 가능한 메타데이터 표준에 대한 수요를 촉진합니다. 중동 및 아프리카는 성숙 곡선의 초기 단계에 있지만 스마트 시티 프로젝트와 걸프 협력 이사회의 데이터 주권 규칙에 따라 가속화되고 있습니다. 캐나다의 국가 로드맵은 35개의 표준화 격차를 지적하며 연방 정부가 자금을 제공하는 파일럿 사업을 촉구하고 있습니다. 이러한 역학이 결합되어 데이터 거버넌스 시장은 지리적으로 다양하면서도 규제 주도의 확대 경로를 형성하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- EU AI법과 설명 가능한 데이터 계통을 요구하는 세계 AI 규제

- FedNow와 실시간 결제 레일이 북미의 BFSI에서 밀리초 미만의 데이터 무결성을 강제

- 아시아태평양의 주권 클라우드 규제(인도의 DPDP법 등)에 의해 국내 데이터 카탈로그에 대한 투자가 가속

- 소매 미디어의 수익화에 의한 제품 마스터 데이터의 품질 향상

- 제조업 4.0에 있어서의 엣지 분석에는 니어 엣지 메타데이터 페더레이션이 필요

- 시장 성장 억제요인

- Tier 1 은행의 엔터프라이즈 규모의 데이터 리니지 툴의 고액의 총 소유 비용

- 인정 데이터 스튜어드와 DCAM 실천자의 인력 부족

- 방위기관에서 실시간 거버넌스를 제한하는 레거시 메인프레임의 상호 운용성 문제

- 규제 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력/소비자

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 컴포넌트별

- 소프트웨어

- 데이터 품질 및 프로파일링 툴

- 메타데이터 관리 및 데이터 카탈로그

- 마스터 데이터 관리

- 데이터 계통과 영향 분석

- 데이터 보안 및 프라이버시 거버넌스

- 서비스

- 전문 서비스

- 매니지드 서비스

- 소프트웨어

- 전개별

- 클라우드

- On-Premise

- 조직 규모별

- 대기업

- 중소기업

- 업무 기능별

- IT와 운영

- 법무 및 규정 준수

- 금융 및 위험

- 마케팅과 판매

- 인사

- 기타 기능

- 용도별

- 컴플라이언스 관리

- 리스크 관리

- 감사관리

- 인시던트 관리

- 데이터 품질 관리

- 기타 용도

- 최종 사용자 업계별

- BFSI

- IT 및 통신

- 헬스케어 및 생명과학

- 소매업 및 전자상거래

- 정부 및 방위

- 제조업

- 에너지 및 유틸리티

- 미디어 및 엔터테인먼트

- 기타 산업

- 지역별

- 북미

- 미국

- 캐나다

- 라틴아메리카

- 브라질

- 아르헨티나

- 칠레

- 멕시코

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 스웨덴

- 노르웨이

- 핀란드

- 덴마크

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 동남아시아

- 호주

- 뉴질랜드

- 기타 아시아태평양

- 중동

- GCC(사우디아라비아, UAE, 카타르)

- 튀르키예

- 이스라엘

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 케냐

- 기타 아프리카

- 북미

제6장 경쟁 구도

- Strategic Developments

- Vendor Positioning Analysis

- 기업 프로파일

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- Collibra NV

- Informatica Inc.

- Alation Inc.

- SAS Institute Inc.

- TIBCO Software Inc.

- Talend SA

- Varonis Systems Inc.

- Amazon Web Services

- Precisely LLC

- Ataccama Corp.

- Quest Software(erwin Data Intelligence)

- OneTrust LLC

- OpenText Corp.(incl. Micro Focus)

- ASG Technologies(Rocket Software)

- Snowflake Inc.

- Databricks Inc.

- Cloudera Inc.

- Alfresco Software Inc.

제7장 시장 기회와 장래의 전망

제8장 시장 기회와 장래의 전망

- 화이트 스페이스와 미충족 요구의 평가

The data governance market sized is estimated at USD3.91 billion in 2025 and is forecast to reach USD 9.62 billion by 2030, reflecting a 19.72% CAGR.

The surge is underpinned by stricter regulatory mandates, accelerating cloud adoption, and the growing realization that well-governed data is crucial for trustworthy AI, real-time payments, and cross-border commerce. Financial institutions, healthcare providers, and manufacturers are broadening investments as penalties for breaches escalate and as business models shift toward data monetization. Vendors are embedding AI into lineage and catalog tools to automate classification tasks, while buyers emphasize deployment flexibility that supports sovereign-cloud and hybrid architectures. The data governance market is therefore evolving from compliance-focused point solutions to integrated platforms that orchestrate quality, security, and accountability across dispersed data estates.

Global Data Governance Market Trends and Insights

EU AI Act and Global AI-Regulation Requiring Explainable Data Lineage

The EU AI Act, effective August 2024, obliges companies deploying high-risk AI to document data origins, transformations, and quality metrics. Failure can trigger fines up to USD 39.82 million or 7% of global turnover, pushing enterprises to adopt advanced lineage platforms that illustrate end-to-end data flows. Vendors are integrating model-level metadata with traditional catalog systems so that auditors can trace training sets and detect bias. Multinationals anticipate similar provisions in Brazil and Canada, turning compliance into a global requirement. These pressures elevate demand for tools that link datasets, models, and business outcomes in a single governance workspace. As a result, the data governance market is pivoting toward solutions that fuse AI oversight with conventional stewardship capabilities.

FedNow and Real-Time Payment Rails Forcing Sub-Millisecond Data Integrity in North-American BFSI

The FedNow Service went live in July 2023 and now operates 24/7 across participating banks. Sub-millisecond settlement demands pristine data quality and continuous lineage to satisfy anti-money-laundering checks without slowing transactions. Institutions are deploying AI-enabled screening and enrichment pipelines to flag anomalies instantly. Legacy batch-oriented compliance stacks cannot keep pace, so banks are modernizing metadata repositories and automating control tests. This driver accelerates subscription revenue for cloud-native governance vendors that can embed rules directly into payment workflows. It also spurs consulting engagements aimed at retrofitting lineage tools to mainframe cores, a lucrative niche within the wider data governance market.

High Total Cost of Ownership for Enterprise-Scale Data Lineage Tooling

Tier-1 banks grapple with multi-million-dollar annual outlays for licenses, integration, and hardware refresh when rolling out enterprise lineage platforms. An Aalto University study confirms that integration with legacy systems and the absence of standards inflate timelines and budgets. Some institutions resort to manual mapping to lower expenses, slowing full-fledged deployments. Vendors respond with modular pricing and consumption-based cloud editions, yet sticker shock remains a prominent brake on expansion within the data governance market.

Other drivers and restraints analyzed in the detailed report include:

- APAC Sovereign-Cloud Mandates Accelerating In-Country Data Catalog Investments

- Retail-Media Monetization Elevating Product-Master Data Quality Spend

- Talent Shortage of Certified Data Stewards and DCAM Practitioners

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software solutions accounted for 57.1% of revenue in 2024, anchoring the data governance market with capabilities that automate policy enforcement, metadata harvesting, and lineage visualization. AI-driven classification and anomaly detection are now baseline features, helping organizations comply with the EU AI Act and FedNow directives in real time. The data governance market size for software is projected to deepen as vendors embed model-governance modules that audit AI pipelines.

Services, encompassing implementation, training, and managed operations, are forecast to expand at 23.4% CAGR. Talent shortages and rising regulatory complexity push organizations to outsource framework design and day-to-day stewardship. Managed services providers are layering SLAs for data quality and consent compliance, differentiating themselves in a fragmented services arena.

Growth in services is also propelled by industry-specific advisory packages. Banking clients demand lineage accelerators pre-mapped to BCBS 239, while healthcare buyers request HIPAA-ready templates. This vertical tailoring leaves room for boutique consultancies alongside global system integrators. Consequently, the data governance market continues shifting from purely licensing models toward mixed recurring revenue streams.

On-premise deployments retained a 53.6% share in 2024 as financial services and healthcare firms insist on local control over sensitive records. Mainframe coexistence and regulated workloads reinforce datacenter preferences despite broader enterprise migration to SaaS. The data governance market share for on-premise solutions is expected to erode gradually as cloud security certifications widen.

Cloud governance tools are advancing at 22.8% CAGR, driven by sovereign-cloud mandates and remote-work norms. Frameworks such as the EDM Council's CDMC provide best practices that reassure auditors. Hybrid patterns dominate: sensitive golden records sit on-premise, while catalog search, quality rules, and reporting run in the cloud. Vendors compete on cross-plane policy orchestration that keeps controls consistent across locations, a capability now essential to win enterprise contracts.

Data Governance Market is Segmented by Component (Software, Services), Deployment (Cloud, On-Premise), Organization Size (Large Enterprises, Small and Medium Enterprises), Business Function (IT and Operations, Legal and Compliance, and More) Application (Compliance Management, Risk Management, and More), End-User Industry (BFSI, IT and Telecom, and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 35.6% revenue in 2024, supported by mature digital-transformation investments and frameworks such as the Federal Enterprise Architecture that emphasize FedRAMP-aligned governance. Financial institutions racing to integrate FedNow exemplify how regulatory deadlines catalyze spending. AI safety rule-making by the National Institute of Standards and Technology further spurs platform enhancements. The data governance market size in the region benefits from dense ecosystems of consultants and hyperscale cloud providers that embed stewardship capabilities natively.

Asia is the fastest-growing region at 26.3% CAGR. India's DPDP Act reshapes data flows, while China's draft negative list for data exports tightens local hosting requirements. These statutes propel investments in sovereign-cloud catalogs capable of enforcing locale-specific retention policies. Japan and South Korea refine existing directives to match global benchmarks, amplifying cross-border alignment. Multinationals now budget region-specific governance clusters, enlarging the addressable data governance market.

Europe retains significant scale through the GDPR and newly enacted EU AI Act. The European Data Governance Act stimulates sectoral data spaces in health, energy, and mobility, fostering demand for interoperable metadata standards . The Middle East and Africa are earlier in their maturity curve but are accelerating, driven by smart-city projects and Gulf Cooperation Council data-sovereignty rules. Canada's national roadmap pinpoints 35 standardization gaps, prompting federally funded pilots . Together, these dynamics produce a geographically diverse but regulatory-driven expansion path for the data governance market.

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- Collibra NV

- Informatica Inc.

- Alation Inc.

- SAS Institute Inc.

- TIBCO Software Inc.

- Talend SA

- Varonis Systems Inc.

- Amazon Web Services

- Precisely LLC

- Ataccama Corp.

- Quest Software (erwin Data Intelligence)

- OneTrust LLC

- OpenText Corp. (incl. Micro Focus)

- ASG Technologies (Rocket Software)

- Snowflake Inc.

- Databricks Inc.

- Cloudera Inc.

- Alfresco Software Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU AI Act and Global AI-Regulation Requiring Explainable Data Lineage

- 4.2.2 FedNow and Real-Time Payment Rails Forcing Sub-Millisecond Data Integrity in North-American BFSI

- 4.2.3 APAC Sovereign-Cloud Mandates (e.g., India DPDP Act) Accelerating In-Country Data Catalog Investments

- 4.2.4 Retail-Media Monetisation Elevating Product-Master Data Quality Spend

- 4.2.5 Edge Analytics in Manufacturing 4.0 Demands Near-Edge Metadata Federation

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership for Enterprise-Scale Data Lineage Tooling in Tier-1 Banks

- 4.3.2 Talent Shortage of Certified Data Stewards and DCAM Practitioners

- 4.3.3 Legacy Mainframe Interoperability Issues Limiting Real-Time Governance in Defense Agencies

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers / Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Data Quality and Profiling Tools

- 5.1.1.2 Metadata Management and Data Catalog

- 5.1.1.3 Master Data Management

- 5.1.1.4 Data Lineage and Impact Analysis

- 5.1.1.5 Data Security and Privacy Governance

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Software

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By Business Function

- 5.4.1 IT and Operations

- 5.4.2 Legal and Compliance

- 5.4.3 Finance and Risk

- 5.4.4 Marketing and Sales

- 5.4.5 Human Resources

- 5.4.6 Other Functions

- 5.5 By Application

- 5.5.1 Compliance Management

- 5.5.2 Risk Management

- 5.5.3 Audit Management

- 5.5.4 Incident Management

- 5.5.5 Data Quality Management

- 5.5.6 Other Applications

- 5.6 By End-user Industry

- 5.6.1 BFSI

- 5.6.2 IT and Telecom

- 5.6.3 Healthcare and Life Sciences

- 5.6.4 Retail and E-Commerce

- 5.6.5 Government and Defense

- 5.6.6 Manufacturing

- 5.6.7 Energy and Utilities

- 5.6.8 Media and Entertainment

- 5.6.9 Other Industries

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.2 Latin America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Chile

- 5.7.2.4 Mexico

- 5.7.2.5 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Sweden

- 5.7.3.7 Norway

- 5.7.3.8 Finland

- 5.7.3.9 Denmark

- 5.7.3.10 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Southeast Asia

- 5.7.4.6 Australia

- 5.7.4.7 New Zealand

- 5.7.4.8 Rest of Asia-Pacific

- 5.7.5 Middle East

- 5.7.5.1 GCC (Saudi Arabia, UAE, Qatar)

- 5.7.5.2 Turkey

- 5.7.5.3 Israel

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Nigeria

- 5.7.6.3 Kenya

- 5.7.6.4 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.3.1 IBM Corporation

- 6.3.2 Microsoft Corporation

- 6.3.3 Oracle Corporation

- 6.3.4 SAP SE

- 6.3.5 Collibra NV

- 6.3.6 Informatica Inc.

- 6.3.7 Alation Inc.

- 6.3.8 SAS Institute Inc.

- 6.3.9 TIBCO Software Inc.

- 6.3.10 Talend SA

- 6.3.11 Varonis Systems Inc.

- 6.3.12 Amazon Web Services

- 6.3.13 Precisely LLC

- 6.3.14 Ataccama Corp.

- 6.3.15 Quest Software (erwin Data Intelligence)

- 6.3.16 OneTrust LLC

- 6.3.17 OpenText Corp. (incl. Micro Focus)

- 6.3.18 ASG Technologies (Rocket Software)

- 6.3.19 Snowflake Inc.

- 6.3.20 Databricks Inc.

- 6.3.21 Cloudera Inc.

- 6.3.22 Alfresco Software Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.1.1 Databricks Inc.

- 7.1.2 Cloudera Inc.

- 7.1.3 Alfresco Software Inc.

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-Space and Unmet-Need Assessment