|

시장보고서

상품코드

1850947

항공기 프로펠러 시스템 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Aircraft Propeller Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

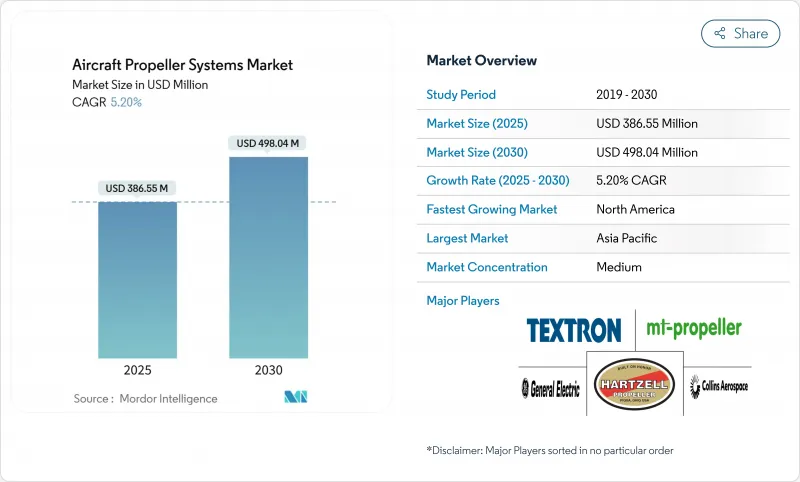

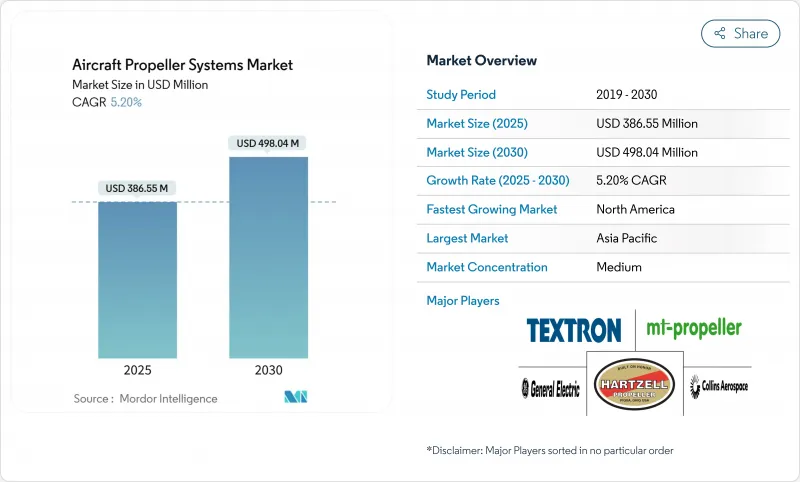

항공기 프로펠러 시스템 시장은 2025년에는 3억 8,655만 달러, 2030년에는 4억 9,804만 달러에 이를 것으로 예측됩니다.

이 꾸준한 확대는 노후화된 피스톤 및 터보프롭 항공기(대부분은 1970-1990년에 제조된 것)의 대체를 세계적으로 추진하고 있는 것이 배경에 있습니다. 운항회사는 현대의 소음 및 배출 규정을 준수하고 복합재 블레이드를 채택함으로써 연료 소비를 8-15% 삭감하는 최신 프로펠러 솔루션을 우선하고 있습니다. 복합재의 보급, 디지털 제어의 통합, 전기 및 하이브리드 실증기의 등장은 경쟁 전략의 형태를 계속 바꾸고 있습니다. 북미의 장점은 항공기 증가와 훈련 수요가 가속화되는 아시아태평양과의 경쟁 격화에 직면하고 있습니다. 한편 항공우주급 탄소섬유 공급체인이 불안정해져 조달과 제조 혁신이 촉구되는 가운데 기존 기업은 입증된 인증 전문지식을 활용해 포지션을 지킵니다.

세계 항공기 프로펠러 시스템 시장 동향 및 통찰

노후화된 피스톤 및 터보프롭 기계의 대체가 OEM 수요를 가속

1970년부터 1990년 사이에 제조된 항공기의 노후화로 인해 항공기 프로펠러 시스템 시장에 대규모 교환 풀이 형성되었습니다. 북미만으로도 11만기 이상의 단발 피스톤이 평균 40년 이상 사용되고 있으며, 운항회사는 기존 알루미늄 블레이드의 부식에 의한 오버홀 비용의 상승에 직면하고 있습니다. 공항의 소음 규제가 엄격해짐에 따라, 소유자는 더 조용한 출발을 위해 시미터 프로파일의 블레이드와 정교한 팁 모양을 결합한 최신 프로펠러로 향하고 있습니다. 업그레이드 투자 회수는 연료 사용량 감소와 점검 간격 연장으로 3-5년에 걸쳐 달성되며, 비행 스쿨이나 전세 항공편 운항사가 연간 800시간 이상 이용하도록 장려하고 있습니다. 저소음 항공기에 대한 착륙료 감액과 같은 규제 인센티브는 비즈니스 사례를 더욱 강화합니다. 이러한 함대 갱신의 기세는 OEM 생산 라인을 유지하고, 개조 수요를 증가시켜, 항공기 프로펠러 시스템 시장을 구조적으로 지원합니다.

알루미늄에서 첨단 복합재 블레이드로 보편적인 시프트가 성능 기준을 변경

복합재 블레이드는 최대 20%의 경량화를 달성하여 유도 항력을 줄이는 긴 스팬과 높은 종횡비를 가능하게 합니다. 허니컴 코어에 탄소 에폭시를 적층함으로써 단조 알루미늄은 실현 불가능한 복잡한 첨단 스위프와 가변 코드 설계를 지원하여 순항 단계에서의 연료 절약을 실현합니다. 자동화된 섬유 배치와 같은 제조의 진보는 스크랩을 줄이고, 재현성을 향상시키고, 사이클 타임을 단축하며, 프로펠러 제조를 보다 광범위한 항공우주 복합재의 워크플로우에 맞춥니다. 오퍼레이터는 또한 염해나 열대 기후에서도 도장 시스템을 무상으로 유지해, 오버홀까지의 기간을 40-60% 연장하는 이 재료의 내식성도 높게 평가했습니다. 항공사가 환경, 사회 및 거버넌스 목표를 통합하고 보다 가볍고 조용한 추진 컴포넌트를 선호하게 되면 항공기 프로펠러 시스템 시장은 혜택을 받아 프리미엄 비즈니스 에비에이션 틈새 이외에도 복합재의 채택을 가속시킵니다.

항공우주 등급 탄소섬유 공급 체인의 박멸 및 가격 변동성

비행 하드웨어용으로 인증된 PAN계 고탄성률 섬유를 공급하고 있는 제조업체는 단 한 줌으로, 그 대부분은 와이드 바디의 기체 계약에 큰 쉐어를 나누고 있습니다. 에너지 가격 상승과 무역 혼란은 즉시 프리프레그 비용에 반영되어 블레이드 가격 설정을 두 자리 상승시킵니다. 소규모 프로펠러 제조업체는 장기 계약을 헤지하는 구매력이 없기 때문에 마진을 압축하는 스팟 시장의 노출에 직면하고 있습니다. 또한 리드타임의 불확실성도 OEM의 생산계획 담당자를 끌어들여 운전자금을 구속하는 재고를 많이 갖도록 촉구하고 있습니다. 따라서 항공기 프로펠러 시스템 시장에서는 공급 부족으로 납품이 지연되면 주문 흐름에 편차가 발생합니다.

부문 분석

파일럿이 상승, 순항, 하강의 각 단계에서 효율을 추구하기 위해, 2024년의 매출 점유율은 가변 피치 유닛이 57.88%를 차지했습니다. 가변 피치 설계 항공기 프로펠러 시스템 시장 규모는 제어 가능한 추력 솔루션에 대한 OEM 수요에 따라 증가할 것으로 예측됩니다. 고정 피치 프로펠러는 CAGR 6.89%로 성장을 이끌고 있는데, 이것은 UAV 플릿의 확대와 전기 항공기 개발자가 요구하는 간편성의 이점이 원동력이 되고 있습니다. 하이브리드 실증기에서의 역회전 컨피규레이션의 채택 확대가 제품 개발을 뒷받침하고 있습니다. 동시에 비용에 민감한 운영자는 유지 보수 터치 포인트를 최소화하는 표준화 된 고정 피치 교체를 환영합니다.

블레이드는 2024년 항공기 프로펠러 시스템 시장 규모의 51.25%를 차지하며 복잡한 복합재 레이업, 가공, 밸런싱을 반영하며 특수 장비가 필요합니다. 복합재료의 보급은 지속적인 비용과 무게 감소를 촉진합니다. 제어 및 거버너 시스템은 디지털 전자기기, 센서, 소프트웨어가 예지 보전 및 원격 건강 모니터링 기능을 개방하고 운행 비용의 직접 절약을 함대 소유자에게 제공하기 때문에 CAGR 6.47%로 성장합니다.

전자 거버너는 현재 엔진 FADEC 유닛과 원활하게 통합되어 다양한 출력 설정에서 최적의 프로펠러 회전 속도를 보장하며 데이터 구동형 유지 보수 스케줄링을 지원합니다. 공급업체는 소프트웨어 업데이트 및 성능 분석을 수익화하고 지속적인 수익원을 확대하고 있습니다.

지역 분석

북미는 2024년에 32.91%의 매출 점유율을 차지했으며 20만대 이상의 등록 일반 항공기와 지역 공급망을 지원하는 프로펠러 OEM 본사에 의해 지원됩니다. 활기찬 복고풍 문화와 엄격한 군사 조달 파이프라인은 블레이드, 허브, 디지털 컨트롤러에 대한 수요를 유지하고 있습니다. 규제당국은 소음과 배출가스의 컴플라이언스를 중시하고 업그레이드의 안정된 흐름을 확보하고 있습니다.

아시아태평양은 중국, 인도, 일본, 동남아시아 국가들이 조종사 훈련, 지역 노선, UAV 용도를 확대함에 따라 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 7.80%로 성장할 전망입니다. ANA 홀딩스의 145억 달러의 수주 포트폴리오에 77대의 신형기가 등장한 것은 지역 운항을 위한 고효율 프로펠러를 지지하는 능력 증강을 강조하고 있습니다. 현지의 복합재 제조 능력이 성숙해, 수입품과의 리드 타임 격차가 축소합니다.

유럽은 레거시 OEM, 까다로운 환경 목표, 차세대 로터 크래프트 개발을 가속화하는 깨끗한 비행과 같은 프로그램 하에서 강력한 R&D 자금 덕분에 상당한 점유율을 유지하고 있습니다. 오퍼레이터는 인구밀집지역에서 보다 조용한 진입 프로파일이 가능한 복합재 블레이드를 요구하고, 군용 사용자는 엄격한 기후에 적응한 해상 순찰 솔루션을 요구하고 있습니다. 동유럽 항공사들도 기존 플랫폼을 위한 비용 효율적인 고정 피치 업그레이드에 투자하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 노후화된 피스톤기 및 터보프롭기의 대체

- 알루미늄 블레이드에서 고급 복합재 블레이드로의 전면적 전환

- 고효율 역회전 프로펠러를 필요로 하는 하이브리드 전기 추진 실증기

- 라이프 사이클 비용 절감 프로그램에 의해 애프터마켓용 복합 블레이드의 판매가 가속

- 디지털 관리자와 블레이드 헬스 센서의 통합

- 민간 및 정부에 의한 무인 항공기 미션의 폭발적인 증가

- 시장 성장 억제요인

- 항공우주 등급의 탄소섬유 공급 체인의 타이트함과 가격 변동

- 길고 비용이 많이 드는 규제 인증 사이클

- 복합재 프로펠러의 높은 초기 비용

- 기존 기업에 유리한 고도로 통합된 엔진-에어프레임 제휴

- 밸류체인 분석

- 규제 전망

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 프로펠러유형별

- 고정 피치

- 가변 피치

- 가변 피치 프로펠러

- 정속 프로펠러

- 풀 페더링 프로펠러

- 기타

- 컴포넌트별

- 블레이드

- 허브 어셈블리

- 스피너와 액세서리

- 제어 및 조속 시스템

- 칼날의 재질별

- 알루미늄

- 복합

- 목재

- 엔진 유형별

- 피스톤 엔진 항공기

- 터보프롭기

- 전기/하이브리드 추진 항공기

- 항공기유형별

- 상업용

- 군

- 수송 및 해상 순찰

- 연습기

- 무인 항공기(UAV)

- 일반항공

- 단발 피스톤

- 멀티 엔진 피스톤

- 경스포츠기

- 최종 사용자별

- OEM

- 애프터마켓

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 프랑스

- 독일

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Collins Aerospace(RTX Corporation)

- Dowty Propellers(General Electric Company)

- McCauley Propeller Systems(Textron Inc.)

- Hartzell Propeller Inc.

- MT-Propeller Entwicklung GmbH

- Safran SA

- Sensenich Propeller Manufacturing Co., Inc.

- Aerosila R&P Enterprise OJSC

- Airmaster Propellers

- GSC Systems Ltd.

- Jabiru Aircraft Pty Ltd.

- Hercules Propellers Ltd.

- FP-Propeller Srl

- DUC HELICES

- Catto Propellers

- Warp Drive Incorporated

- Ivoprop Corporation

- Helix Carbon GmbH

제7장 시장 기회와 장래의 전망

SHW 25.11.11The aircraft propeller systems market stands at USD 386.55 million in 2025 and is forecasted to reach a market size of USD 498.04 million by 2030, reflecting a 5.20% CAGR.

This steady expansion is anchored in the global push to replace aging piston and turboprop aircraft, many of which were produced between 1970 and 1990. Operators prioritize modern propeller solutions that comply with contemporary noise and emission regulations and reduce fuel burn by 8-15% by adopting composite blades. Composite penetration, digital control integration, and the rise of electric and hybrid demonstrators continue to reshape competitive strategies. North American dominance faces intensifying competition from Asia-Pacific, where fleet additions and training demand accelerate. Meanwhile, incumbents leverage proven certification expertise to defend positions, even as supply-chain volatility for aerospace-grade carbon fiber prompts innovation in sourcing and manufacturing.

Global Aircraft Propeller Systems Market Trends and Insights

Replacement of Aging Piston and Turboprop Fleets Accelerates OEM Demand

Ageing aircraft built between 1970 and 1990 create a sizeable replacement pool for the aircraft propeller system market. Over 110,000 single-engine pistons in North America alone now average more than 40 years in service, and operators face rising corrosion-related overhaul costs on legacy aluminium blades. Stricter airport noise rules push owners toward modern propellers that combine scimitar-profile blades with refined tip geometry for quieter departures. Upgrade payback is achieved in three to five years through lower fuel use and extended inspection intervals, encouraging flight schools and charter operators to utilize more than 800 hours annually. Regulatory incentives such as reduced landing fees for low-noise aircraft further strengthen the business case. This fleet-renewal momentum sustains OEM production lines and lifts retrofit demand, adding structural support to the aircraft propeller systems market.

Universal Shift from Aluminum to Advanced Composite Blades Transforms Performance Standards

Composite blades achieve weight reductions of up to 20%, permitting longer spans and higher aspect ratios that cut induced drag. Carbon-epoxy lay-up over honeycomb cores supports complex swept tips and variable chord designs that are not feasible in forged aluminium, delivering measurable cruise-phase fuel savings. Manufacturing advances such as automated fibre placement lower scrap, improve repeatability, and shorten cycle time, aligning propeller production with broader aerospace composite workflows. Operators also value the material's corrosion immunity, which keeps paint systems intact in saline or tropical climates and extends time between overhauls by 40-60%. The aircraft propeller systems market benefits as airlines integrate environmental, social, and governance targets, favoring lighter, quieter propulsion components, accelerating composite adoption beyond premium business-aviation niches.

Supply-Chain Tightness and Price Volatility for Aerospace-Grade Carbon Fibre

Only a handful of producers supply PAN-based high-modulus fibres certified for flight hardware, and many allocate a large share to wide-body fuselage contracts. Any surge in energy prices or trade disruptions immediately flows through to prepreg cost, lifting blade pricing by double-digit percentages. Small propeller manufacturers lack the purchasing clout to hedge long contracts, so they face spot-market exposure that compresses margins. Lead-time uncertainty also frustrates OEM production planners, prompting them to hold thicker inventories that tie up working capital. Therefore, the aircraft propeller systems market sees uneven order flow when supply shortages delay deliveries.

Other drivers and restraints analyzed in the detailed report include:

- Hybrid-Electric Demonstrators Requiring High-Efficiency Contra-Rotating Propellers

- Lifecycle-Cost Reduction Programs Accelerating Aftermarket Composite Blade Sales

- Lengthy and Expensive Regulatory Certification Cycles Discourage Innovation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Variable-pitch units held a 57.88% revenue share in 2024 as pilots sought efficiency across climb, cruise, and descent. The aircraft propeller systems market size for variable-pitch designs is projected to rise in line with OEM demand for controllable thrust solutions. Fixed-pitch propellers lead growth at a 6.89% CAGR, powered by the expanding UAV fleet and the simplicity benefits electric aircraft developers seek. The growing adoption of contra-rotating configurations in hybrid demonstrators amplifies product development. At the same time, cost-sensitive operators welcome standardized fixed-pitch replacements that minimize maintenance touchpoints.

Blades contributed 51.25% of the aircraft propeller systems market size in 2024, reflecting complex composite layup, machining, and balancing that demand specialized equipment. Composite penetration drives continual cost and weight reductions. Control and governor systems advance at a 6.47% CAGR as digital electronics, sensors, and software unlock predictive maintenance and remote health monitoring capabilities that deliver direct operating-cost savings to fleet owners.

Electronic governors now integrate seamlessly with engine FADEC units, ensuring optimal propeller RPM under varying power settings and supporting data-driven maintenance scheduling. Suppliers monetise software updates and performance analytics, expanding recurring revenue streams.

The Aircraft Propeller Systems Market Report is Segmented by Propeller Type (Fixed-Pitch and Variable-Pitch), Component (Blades, Hub Assembly, and More), Blade Material (Aluminum, and More), Engine Type (Piston Engine, and More), Aircraft Type (Commercial, and More), End-User (OEM and Aftermarket), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held a 32.91% revenue share in 2024, buoyed by more than 200,000 registered general aviation aircraft and propeller OEM headquarters that anchor the regional supply chain. A vibrant retrofit culture and rigorous military procurement pipelines maintain demand for blades, hubs, and digital controls. Regulators emphasise noise and emissions compliance, ensuring a steady flow of upgrade activity.

Asia-Pacific registers the fastest 7.80% CAGR through 2030 as China, India, Japan, and Southeast Asian nations expand pilot training, regional routes, and UAV applications. The arrival of 77 new aircraft in ANA Holdings' USD 14.5 billion order portfolio underscores capacity additions favouring high-efficiency propellers for regional operations. Local composite fabrication capability matures, narrowing lead-time gaps versus imports.

Europe maintains a substantial share thanks to legacy OEMs, stringent environmental targets, and strong R&D funding under programs such as Clean Aviation, which accelerate next-generation rotorcraft development. Operators demand composite blades capable of quieter approach profiles in densely populated regions, while military users seek maritime patrol solutions adapted to harsh climates. Eastern European fleets likewise invest in cost-effective fixed-pitch upgrades for legacy platforms.

- Collins Aerospace (RTX Corporation)

- Dowty Propellers (General Electric Company)

- McCauley Propeller Systems (Textron Inc.)

- Hartzell Propeller Inc.

- MT-Propeller Entwicklung GmbH

- Safran S.A.

- Sensenich Propeller Manufacturing Co., Inc.

- Aerosila R&P Enterprise OJSC

- Airmaster Propellers

- GSC Systems Ltd.

- Jabiru Aircraft Pty Ltd.

- Hercules Propellers Ltd.

- FP-Propeller Srl

- DUC HELICES

- Catto Propellers

- Warp Drive Incorporated

- Ivoprop Corporation

- Helix Carbon GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Replacement of aging piston and turboprop fleets

- 4.2.2 Universal shift from aluminum to advanced composite blades

- 4.2.3 Hybrid-electric demonstrators requiring high-efficiency contra-rotating propellers

- 4.2.4 Lifecycle-cost reduction programs accelerating aftermarket composite blade sales

- 4.2.5 Digital governors and blade-health sensors integration

- 4.2.6 Explosive growth of civil and governmental UAV missions

- 4.3 Market Restraints

- 4.3.1 Supply-chain tightness and price volatility for aerospace-grade carbon fiber

- 4.3.2 Lengthy and expensive regulatory certification cycles

- 4.3.3 High up-front cost of composite propellers

- 4.3.4 Highly consolidated engine-airframer alliances giving incumbents advantage

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Propeller Type

- 5.1.1 Fixed-Pitch

- 5.1.2 Variable-Pitch

- 5.1.2.1 Controllable Pitch Propeller

- 5.1.2.2 Constant Speed Propeller

- 5.1.2.3 Full Feathering Propeller

- 5.1.2.4 Others

- 5.2 By Component

- 5.2.1 Blades

- 5.2.2 Hub Assembly

- 5.2.3 Spinner and Accessories

- 5.2.4 Control and Governor System

- 5.3 By Blade Material

- 5.3.1 Aluminum

- 5.3.2 Composite

- 5.3.3 Wood

- 5.4 By Engine Type

- 5.4.1 Piston Engine Aircraft

- 5.4.2 Turboprop Aircraft

- 5.4.3 Electric/Hybrid Propulsion Aircraft

- 5.5 By Aircraft Type

- 5.5.1 Commercial

- 5.5.2 Military

- 5.5.2.1 Transport and Maritime Patrol

- 5.5.2.2 Trainer Aircraft

- 5.5.2.3 Unmanned Aerial Vehicles (UAVs)

- 5.5.3 General Aviation

- 5.5.3.1 Single-Engine Piston

- 5.5.3.2 Multi-Engine Piston

- 5.5.3.3 Light-Sport Aircraft

- 5.6 By End-User

- 5.6.1 Original Equipment Manufacturer (OEM)

- 5.6.2 Aftermarket

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 United Kingdom

- 5.7.2.2 France

- 5.7.2.3 Germany

- 5.7.2.4 Italy

- 5.7.2.5 Russia

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 South Korea

- 5.7.3.5 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Saudi Arabia

- 5.7.5.1.2 United Arab Emirates

- 5.7.5.1.3 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Collins Aerospace (RTX Corporation)

- 6.4.2 Dowty Propellers (General Electric Company)

- 6.4.3 McCauley Propeller Systems (Textron Inc.)

- 6.4.4 Hartzell Propeller Inc.

- 6.4.5 MT-Propeller Entwicklung GmbH

- 6.4.6 Safran S.A.

- 6.4.7 Sensenich Propeller Manufacturing Co., Inc.

- 6.4.8 Aerosila R&P Enterprise OJSC

- 6.4.9 Airmaster Propellers

- 6.4.10 GSC Systems Ltd.

- 6.4.11 Jabiru Aircraft Pty Ltd.

- 6.4.12 Hercules Propellers Ltd.

- 6.4.13 FP-Propeller Srl

- 6.4.14 DUC HELICES

- 6.4.15 Catto Propellers

- 6.4.16 Warp Drive Incorporated

- 6.4.17 Ivoprop Corporation

- 6.4.18 Helix Carbon GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment