|

시장보고서

상품코드

1850952

지오텍스타일 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Geotextile - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

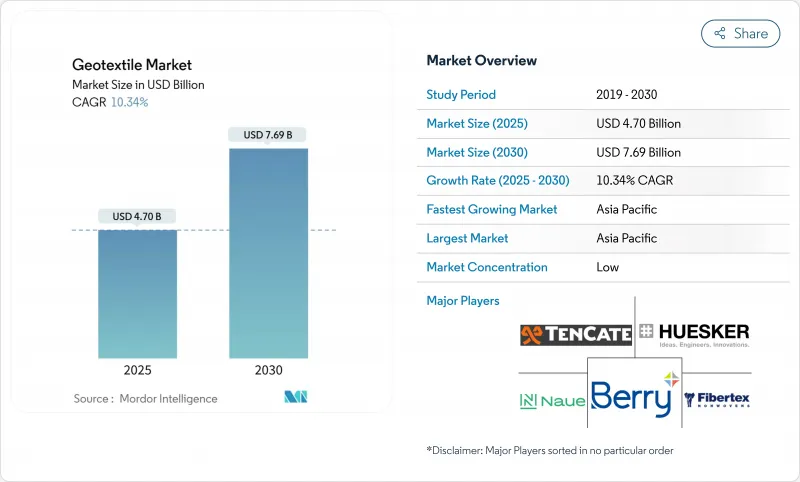

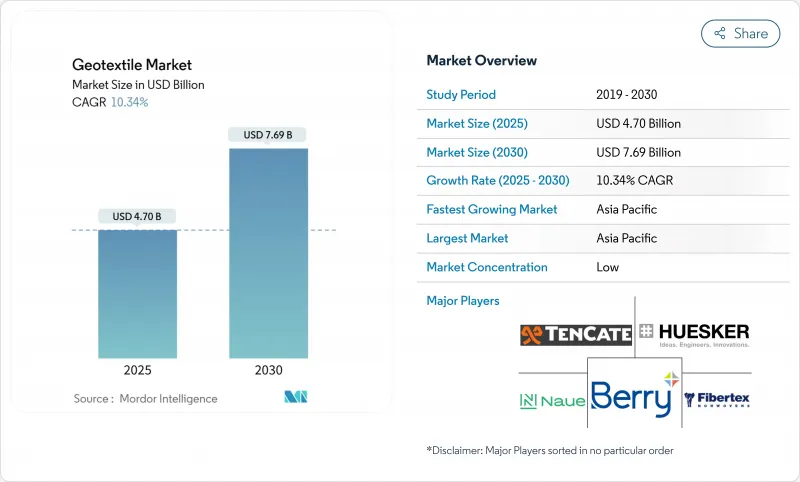

지오텍스타일 시장 규모는 2025년에 47억 달러, 2030년에는 76억 9,000만 달러에 이르고, 이 기간의 CAGR은 10.34%를 나타낼 전망입니다.

지오텍스타일 산업은 토목공학, 환경관리, 자원효율의 교차로에 점점 위치하고 있습니다. 인플레이션 조정 후에도 새로운 도로, 철도 부설 및 치수 시스템에 대한 절대적인 지출은 대응 가능한 시장을 이전 예측보다 빠르게 확장하고 있으며 공급업체에게는 지속적인 조달 파이프라인을 의미합니다. 이와 병행하여, 제조업체 각 사는 처리능력이 높은 라인에 대한 투자를 추진하고 있어, 이것은 수요의 탄력성이 단기적인 원재료의 변동을 능가한다는 자신감의 드러나고 있습니다. 최근의 계약 체결에서 새롭게 추찰되는 것은 공공 기관이 성능에 근거한 사양과 재활용 콘텐츠 조항을 묶어, 지오텍스타일이 순수한 기술 항목이 아니고, 지속가능성 목표의 대용품이 되고 있다고 하는 것입니다.

세계 지오텍스타일 시장 동향과 통찰

건설 섹터의 확대가 지오텍 스타일의 채택을 뒷받침

교통 예산의 지속적인 성장으로 지오텍 스타일 사양이 고속도로 계약 옵션에서 표준 사양으로 전환하고 있습니다. 연방 도로 관리국의 실제 데이터에 따르면, 미국의 새로운 고속도로 프로젝트의 78%는 이미 적어도 하나의 지오텍스타일 레이어를 통합했으며, 동국의 엔지니어는 서브베이스 양의 최대 1/5 절약을 보고했습니다. 이 패턴은 철도에서도 마찬가지이며, 미국 토목 학회(American Society of Civil Engineers)의 논문에서는 분리 패브릭을 사용했을 경우 밸러스트의 안정성이 2자리수 향상하는 것으로 보고되었습니다. 지오텍스타일이 설계의 일부가 되면 재료의 양을 모델링하기 쉬워지기 때문입니다.

광업 부문의 통합은 경영의 지속가능성을 향상

칠레, 호주, 남아프리카의 구리와 리튬 생산자는 침투를 제한하고 담수의 취수를 줄이기 위해 미광 저장 시설에 지오텍 스타일을 내장하고 있습니다. 운영자는 현재 댐 통합 대시보드에 실시간 데이터를 제공하는 센서 가능 부직포 층을 지정하고 있으며, 이 기능은 검사 사이클을 단축하고 점점 더 엄격해지는 정보 공개 규칙을 충족합니다. 업계가 더 높은 사양의 제품을 시험적으로 도입하는 데 적극적인 것은 상품 가격 변동보다는 컴플라이언스 리스크가 조달 우선순위를 형성하고 있음을 보여줍니다. 부차적인 효과로서, 주요 광산 집적지 근처에 현지 제조 유닛이 설립되어 지오텍스타일 업계에 분산형 공급 모델이 출현하고 있음을 시사하고 있습니다.

프로파일렌 가격 변동이 마진 안정을 위협

폴리프로필렌 원료의 계약 가격은 연간 2자리 변동을 나타내며 생산자 마진을 압박하며 고정 가격 입찰을 복잡하게 합니다. 헤지 능력이 제한된 소규모 공장은 판매 주문 생산 모델로 이동하고 비용 변동을 하류로 전가하고 있지만 구매자가 리드 타임의 확실성을 우선시하므로 시장 점유율이 떨어질 위험이 있습니다. 파급효과로서 고밀도 폴리에틸렌과 같은 대체 폴리머가 봉쇄 용도로 점유율을 확대하고 있는데, 이는 기술적 우위성에 의한 것이 아니라 투입 비용이 보다 예측하기 쉽기 때문입니다. 새로운 추론은 조달 담당자가 가격 위험의 균형을 맞추기 위해 단일 단량체가 아닌 폴리머 바구니에 계약을 할당 할 수 있다는 것입니다.

부문 분석

2024년 지오텍스타일 시장 점유율은 폴리프로필렌 부문이 57.30%로 최대를 차지했으며, 이 소재 시장 규모는 2030년까지 연평균 복합 성장률(CAGR) 11.30%로 상승할 것으로 예측됩니다. 지오텍스타일의 인기는 내화학성과 양호한 강도 대 중량비에 기인합니다. 이 특성은 최근 고온 및 자외선에 노출된 실험실에서의 노화시험에서 확인되었으며, 사양 기준을 초과하는 인장 강도가 유지되는 것으로 나타났습니다. 기계 리사이클에 적합한 안정제 패키지가 이미 시판되고 있기 때문에 순환형 디자인으로의 이행이 진행됨에 따라, 폴리프로필렌의 리드는 더욱 견고한 것이 될 것이라는 것이 새로운 추론입니다.

폴리에스테르는 보강 매트의 높은 인장 탄성률이 평가되어 큰 점유율을 차지하고 있지만, rPET공급이 제한되어 있기 때문에 그 점유율은 낮습니다. 공급망의 스트레스는 성능과 조달 위험의 균형을 유지하면서 버진 폴리에스테르와 바이오 유래 섬유를 혼합하는 블렌드로의 다양화를 촉진하고 있습니다. 폴리에틸렌은 탄성률보다 내응력 균열성이 중시되는 화학물질 봉쇄의 틈새를 타겟으로 판매량의 8분의 1 근처를 차지하고 있습니다. 나머지를 차지하는 것은 신흥의 천연 폴리머와 생분해성 폴리머로, 비용은 높은 것, 내용 연수 후의 제거가 곤란한 섬세한 생태계에서의 구입 주문을 확보하고 있습니다. 논리적 추론에서는 내구성이 있는 합성수지층과 생분해성의 희생층을 조합한 이중소재 사양이 중가격대에서의 새로운 채택의 길을 열 수 있습니다.

직물 지오텍스타일은 도로의 서브 베이스에 있어서의 우수한 하중 분산성이 원동력이 되어, 2024년에는 45% 시장 점유율을 차지했습니다. 공공기관이 설계 수명의 길이를 선호하기 때문에 시장 규모는 꾸준히 확대될 것으로 예측됩니다. 새로운 셔틀 룸의 구성은 생산 폭을 확대하여 시공의 중복과 노동 시간을 줄였습니다. 현재의 추론에서는 종래는 부직포가 주류였던 용도에서도, 롤 폭이 넓어진 것으로 코스트·베네핏 분석이 직물에 기울어질 가능성이 있습니다.

부직포 지오텍스타일은 CAGR 11.50%로 급성장하여 빗물 여과 시스템에의 통합이 진행되고 있습니다. 니들 펀치 유형은 투수성을 희생하지 않고 차압 침하에 대응하고, 일단 철도 밸러스트 하에서의 사용이 제한된 성능 갭을 메웁니다. 니트 직물은 지오그리드-지오텍스타일 복합재료를 위한 초고강도를 제공하며, 방향성 보강이 중요합니다. 제조업체 각 사는 니트층을 부직포 필터와 조합해 다층 라미네이트로 하는 것으로, 1회의 시공으로 3개의 기능을 실현하는 어프로치를 취하고 있습니다. 이 추세는 구매자가 가까운 미래에 "패브릭"이 아니라 "시스템"을 지정할 가능성을 시사하며 시장 통계를 집계하는 방법이 변경됨을 의미합니다.

지역 분석

2024년 지오텍스타일 시장 점유율은 아시아태평양이 39.5%로 최고입니다. 중국은 적극적인 인프라 확장과 보다 엄격한 환경 규제를 양립시켜, 이 지역 수요의 대부분을 창출하고 있습니다. 인도는 4분의 1을 차지하며 2025년 4월에 예정된 품질관리령의 혜택을 받고 있습니다. 품질관리령은 기본적인 기술기준을 끌어올릴 것으로 기대되고 있으며, 일본, 한국, 호주는 복합지오텍스타일에 의존하는 경우가 많은 지진과 사이클론에 강한 고도의 설계를 전개하고 있습니다. 나머지는 동남아시아로, 관민 파트너십이 최초 채택의 계기가 되고 있습니다. 국내 생산능력 증강에 따라 아시아태평양은 10년 후까지는 순수입국에서 균형무역권으로 전환할 것이라는 새로운 추론입니다.

북미는 BABA 규칙에 따라 2025년 3월부터 연방 정부가 자금을 제공하는 프로젝트의 국내 제조가 의무화되는 미국이 지배적입니다. 캐나다는 이 지역의 파이의 5분의 1을 차지하고, 지오텍 스타일을 한랭 지역의 도로 및 채광 용도로 활용하고 있습니다. 한편 멕시코는 니어쇼어링 코리도를 따라 공업단지 건설로 점유율을 늘리고 있습니다. 멕시코에서는 센서가 내장된 섬유를 채택하는 것이 가장 많으며, 이는 디지털 인프라 전략이 프리미엄 제품 수요로 이어지고 있음을 보여줍니다. 새로운 추론으로는 미국 고속도로의 재허가 사이클은 여러 해에 걸친 조달 전망을 고정하여 공장이 세계 평균보다 높은 가동률로 조업할 수 있도록 하고 있다는 것입니다.

유럽은 총 매출액에 크게 기여하고 있으며, 독일, 프랑스, 영국은 재활용 및 저탄소 지오텍 스타일을 선호하는 엄격한 배출 프로토콜을 통해 이러한 기여에 큰 역할을 하고 있습니다. 남유럽에서는 가뭄 회복력으로 이어지는 사방 프로젝트에 주력하고, 동유럽에서는 EU의 결속 자금을 철도와 도로 복구에 충당하고 있습니다. 시오엔산업 등의 제조업체는 순환 경제 성과를 공표하고 있어 브랜드의 차별화가 코스트로부터 지속가능성의 지표로 이행하고 있는 것을 시사하고 있습니다. 경제 상황이 호전되면 미뤄졌던 정비 적체(backlog)가 해소되면서 2차 수요 급증을 촉발할 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 건설 업계에서 지오텍 스타일의 사용 증가

- 광업 활동에서 지오텍 스타일의 사용 증가

- 환경 보호를 위한 엄격한 규제 틀

- 유럽 매립지령에 있어서의 복토층의 의무화가 지오신세틱 라이너의 보급을 촉진

- 사우디아라비아의 NEOM과 기가 프로젝트가 GCC 지역의 사막 토양 안정화 솔루션을 추진

- 시장 성장 억제요인

- 휘발성 프로파일렌 계약 가격

- rPET 할당으로부터 음료 포장까지의 폴리에스테르 공급의 박박

- 신흥국에서의 설계 시공의 도입을 저해하는 엔지니어링 스킬의 갭

- 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 소재별

- 폴리프로필렌

- 폴리에스테르

- 폴리에틸렌

- 기타 재료

- 원단 유형별

- 직조

- 부직포

- 니트

- 기능별

- 분리

- 배수

- 여과

- 강화

- 보호

- 용도별

- 도로 건설과 포장 보수

- 침식

- 배수

- 철도 공사

- 농업

- 기타 용도(채굴 작업, 해안 및 수로의 보호 등)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 태국

- 말레이시아

- 인도네시아

- 베트남

- 기타 아시아

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 튀르키예

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 남아프리카

- 나이지리아

- 이집트

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- ACE Geosynthetics

- AFITEXINOV

- AGRU America Inc.

- Asahi Kasei Advance Corporation

- Berry Global Inc.

- Carthage Mills

- CMC

- Fibertex Nonwovens A/S

- Freudenberg Performance Materials

- HUESKER International

- Industrial Fabrics, Inc.

- KayTech

- Mattex Geosynthetics

- Naue GmbH & Co. KG

- Officine Maccaferri Spa

- Owens Corning

- Solmax

- TenCate Geosynthetics

- Thrace Group

- TYPAR Geosynthetics

제7장 시장 기회와 장래의 전망

SHW 25.11.11The geotextiles market size is estimated at USD 4.70 billion in 2025 and is forecast to climb to USD 7.69 billion by 2030, reflecting a CAGR of 10.34% over the period.

The strong expansion is rooted in the material's ability to boost infrastructure resilience while supporting circular-economy targets, so the geotextiles industry increasingly sits at the intersection of civil engineering, environmental stewardship and resource efficiency. Even after adjusting for inflation, the absolute spending on new roads, railbeds and flood-control systems is widening the addressable market faster than previously projected, implying sustained procurement pipelines for suppliers. In parallel, manufacturer investments in higher-throughput lines signal confidence that demand elasticity outweighs short-term raw-material volatility. A fresh inference from recent contract awards is that public agencies now bundle performance-based specifications with recycled-content clauses, effectively making geotextiles a proxy for sustainability goals instead of a purely technical item.

Global Geotextile Market Trends and Insights

Construction Sector Expansion Fuels Geotextile Adoption

Persistent growth in transportation budgets is pushing geotextile specifications from optional to standard practice on highway contracts. Field data from the Federal Highway Administration show that 78% of new U.S. highway projects already integrate at least one geotextile layer, and agency engineers report aggregate savings of up to one-fifth on sub-base volumes. The pattern is similar in rail, where American Society of Civil Engineers papers document a two-digit improvement in ballast stability when separation fabrics are used. A fresh inference is that cost predictability, not just headline savings, is driving faster contractor uptake because material quantities become easier to model once geotextiles are part of the design.

Mining Sector Integration Enhances Operational Sustainability

Copper and lithium producers in Chile, Australia and South Africa are embedding geotextiles into tailings-storage facilities to limit seepage and reduce freshwater withdrawals. Operators now specify sensor-ready non-woven layers that feed real-time data into dam-integrity dashboards, a capability that shortens inspection cycles and satisfies increasingly stringent disclosure rules. The industry's willingness to pilot higher-spec products indicates that compliance risk, rather than commodity price swings, is shaping procurement priorities. An observed secondary effect is the creation of local fabrication units near major mine clusters, hinting at an emerging decentralised supply model for the geotextiles industry.

Propylene Price Volatility Threatens Margin Stability

Contract prices for polypropylene feedstock have shown double-digit intra-year swings, compressing producer margins and complicating fixed-price bids. Smaller mills with limited hedging capacity are shifting toward make-to-order models, which pass cost volatility downstream but risk eroding market share when buyers prioritise lead-time certainty. The ripple effect is that alternative polymers such as high-density polyethylene are gaining incremental share in containment applications, not due to technical superiority but because of more predictable input costs. One fresh inference is that procurement officers may start indexing contracts to polymer baskets rather than single monomers to balance price risk.

Other drivers and restraints analyzed in the detailed report include:

- Environmental Regulations Drive Material Innovation

- European Landfill Directive Elevates Geosynthetic Demand

- Engineering Skills Gap Hampers Technical Implementation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The polypropylene segment accounts for the largest geotextiles market share at 57.30% in 2024, with the market size in this material forecast to climb at an 11.30% CAGR through 2030. Its popularity stems from chemical resistance and a favourable strength-to-weight ratio, attributes recently confirmed by laboratory aging tests under elevated temperature and ultraviolet exposure that showed retained tensile strength above specification thresholds. A fresh inference is that the ongoing shift to circular design will further cement polypropylene's lead, because stabiliser packages compatible with mechanical recycling are already commercially available.

Polyester holds a significant share prized for high tensile modulus in reinforcement mats but held back by constrained rPET supply. Supply-chain stress is encouraging diversification into blends that mix virgin polyester with bio-sourced fibres, balancing performance and procurement risk. Polyethylene captures close to one-eighth of volume, targeting chemical-containment niches where stress-crack resistance matters more than modulus. Emerging natural and biodegradable polymers make up the balance and, though costlier, secure purchase orders in sensitive ecosystems where removal after service life is difficult. The logical inference is that dual-material specifications, combining a durable synthetic layer with a biodegradable sacrificial layer, could open new mid-price adoption avenues.

Woven geotextiles command a 45% market share in 2024, driven by superior load-distribution in road sub-bases. Their market size is expected to expand steadily as public agencies prioritise long design lives. New shuttle-loom configurations have increased productive width, lowering installation overlaps and labour hours. A current inference is that the wider rolls may tilt cost-benefit analyses in favour of woven fabrics even in applications traditionally dominated by non-wovens.

Non-woven geotextiles grow faster, at an 11.50% CAGR, and increasingly integrate into stormwater filtration systems. Needle-punched variants address differential settlement without sacrificing permeability, bridging a performance gap that once limited use beneath rail ballast. Knitted fabrics, supply ultra-high strength for geogrid-geotextile composites where directional reinforcement is prized. Manufacturers are bundling knitted layers with non-woven filters into multi-layer laminates, an approach that delivers three functions in one installation step. That trend implies buyers may soon specify "systems" rather than "fabrics", altering how market statistics are compiled.

The Geotextiles Market Report Segments the Industry by Material (Polypropylene, Polyester, and More), Fabric Type (Woven, Non-Woven, and Knitted), Function (Separation, Drainage, and More), Application (Road Construction and Pavement Repair, Erosion, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific leads with a 39.5% geotextiles market share in 2024. China generates significant of regional demand, marrying aggressive infrastructure expansion with stricter environmental codes. India contributes one-quarter and benefits from its Quality Control Order scheduled for April 2025, which is expected to raise baseline technical standardsJapan, South Korea, and Australia collectively contribute a significant portion to the regional expenditure, deploying sophisticated earthquake- and cyclone-resilient designs that often rely on composite geotextiles. The remainder rests with Southeast Asia, where public-private partnerships are catalysing first-time adoption. An emerging inference is that domestic capacity additions will convert Asia-Pacific from a net importer to a balanced trade zone by decade-end.

North America, dominated by the United States, where BABA rules require domestic manufacture for federally funded projects from March 2025. Canada holds one-fifth of the regional pie, leveraging geotextiles for cold-region roads and mining applications, while Mexico's share grows with industrial-park construction along the near-shoring corridor. Adoption of sensor-embedded fabrics is highest here, an indicator that digital infrastructure strategies are translating into premium product demand. A fresh inference is that U.S. highway re-authorisation cycles lock in multi-year procurement visibility, allowing mills to operate at higher utilisation rates than global averages.

Europe contributes significantly to total sales, with Germany, France, and the UK playing a major role in this contribution, propelled by stringent emissions protocols that favour recycled and low-carbon geotextiles. Southern Europe focuses on erosion-control projects linked to drought resilience, while Eastern states channel EU cohesion funds into rail and road rehabilitation. Manufacturers such as Sioen Industries publicise circular-economy achievements, suggesting brand differentiation is shifting from cost to sustainability metrics. The inference is that once economic conditions improve, deferred maintenance backlogs could trigger a second-wave demand surge.

- ACE Geosynthetics

- AFITEXINOV

- AGRU America Inc.

- Asahi Kasei Advance Corporation

- Berry Global Inc.

- Carthage Mills

- CMC

- Fibertex Nonwovens A/S

- Freudenberg Performance Materials

- HUESKER International

- Industrial Fabrics, Inc.

- KayTech

- Mattex Geosynthetics

- Naue GmbH & Co. KG

- Officine Maccaferri Spa

- Owens Corning

- Solmax

- TenCate Geosynthetics

- Thrace Group

- TYPAR Geosynthetics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Usage of Geotextiles in Construction Industry

- 4.2.2 Increase Usage of Geotextiles in Mining Activities

- 4.2.3 Stringent Regulatory Framework for Environmental Protection

- 4.2.4 Mandatory Capping Layers in Europe Landfill Directive Boosting Geosynthetic Liners

- 4.2.5 Saudi NEOM and Giga-Projects Driving Desert Soil-Stabilisation Solutions in GCC region

- 4.3 Market Restraints

- 4.3.1 Volatile Propylene Contract Prices

- 4.3.2 Polyester Supply Tightness from rPET Allocation to Beverage Packaging

- 4.3.3 Engineering-Skills Gap Curtailing Design-Build Adoption in Emerging Economies

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material

- 5.1.1 Polypropylene

- 5.1.2 Polyester

- 5.1.3 Polyethylene

- 5.1.4 Other Materials

- 5.2 By Fabric Type

- 5.2.1 Woven

- 5.2.2 Non-woven

- 5.2.3 Knitted

- 5.3 By Function

- 5.3.1 Separation

- 5.3.2 Drainage

- 5.3.3 Filtration

- 5.3.4 Reinforcement

- 5.3.5 Protection

- 5.4 By Application

- 5.4.1 Road Construction and Pavement Repair

- 5.4.2 Erosion

- 5.4.3 Drainage

- 5.4.4 Railworks

- 5.4.5 Agriculture

- 5.4.6 Other Applications (Mining Operations, Coastal and Waterway Protection,etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Thailand

- 5.5.1.6 Malaysia

- 5.5.1.7 Indonesia

- 5.5.1.8 Vietnam

- 5.5.1.9 Rest of Asia

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordics

- 5.5.3.7 Russia

- 5.5.3.8 Turkey

- 5.5.3.9 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 South Africa

- 5.5.5.5 Nigeria

- 5.5.5.6 Egypt

- 5.5.5.7 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ACE Geosynthetics

- 6.4.2 AFITEXINOV

- 6.4.3 AGRU America Inc.

- 6.4.4 Asahi Kasei Advance Corporation

- 6.4.5 Berry Global Inc.

- 6.4.6 Carthage Mills

- 6.4.7 CMC

- 6.4.8 Fibertex Nonwovens A/S

- 6.4.9 Freudenberg Performance Materials

- 6.4.10 HUESKER International

- 6.4.11 Industrial Fabrics, Inc.

- 6.4.12 KayTech

- 6.4.13 Mattex Geosynthetics

- 6.4.14 Naue GmbH & Co. KG

- 6.4.15 Officine Maccaferri Spa

- 6.4.16 Owens Corning

- 6.4.17 Solmax

- 6.4.18 TenCate Geosynthetics

- 6.4.19 Thrace Group

- 6.4.20 TYPAR Geosynthetics

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Rising Awareness about Water Conservation in the Manufacturing Sector