|

시장보고서

상품코드

1850958

클라우드 매니지드 서비스 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Cloud Managed Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

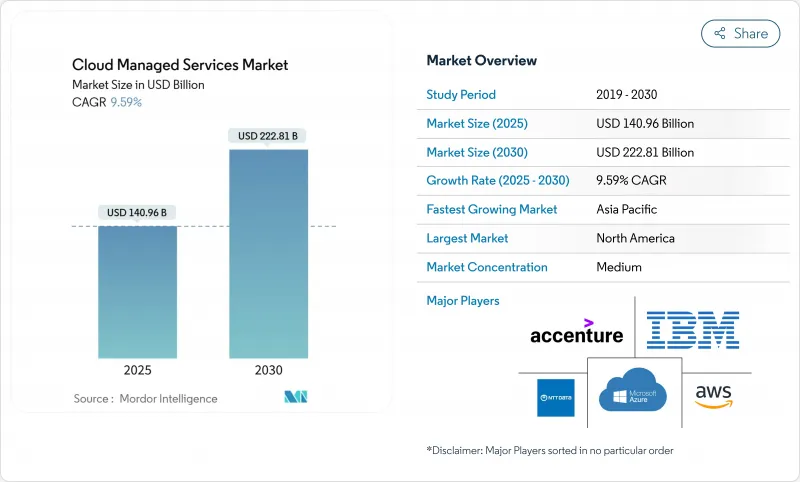

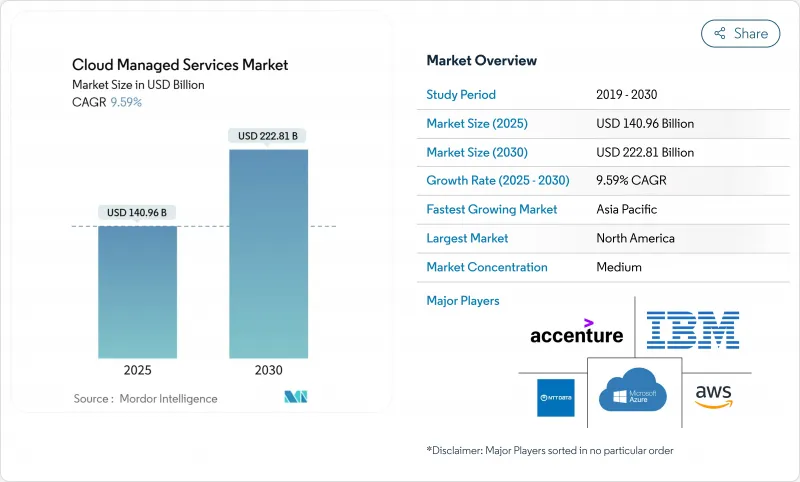

클라우드 매니지드 서비스 시장 규모는 2025년에 1,409억 6,000만 달러, 2030년에는 2,228억 1,000만 달러로 성장할 것으로 예측됩니다.

기업은 자산 편중의 인프라 소유에서 민첩성을 높이고, 현금을 창출하고, 혁신주기를 단축하는 종량 과금 운영 모델로 계속 전환하고 있습니다. 멀티클라우드 난립과 사이버 보안 위협이 사내 IT 팀을 피곤하게 하는 동안 수요는 급증합니다. 금융 서비스의 디지털 지침, AI 주도 워크로드, 지속가능성 목표는 전문가의 외부 관리 필요성을 높이고 있습니다. 북미가 지출의 대부분을 차지하고 있지만, 아시아태평양은 미개척의 기반이 많아, 클라우드를 추진하는 정책 환경이 갖추어져 있기 때문에 가장 급속하게 확대하고 있는 지역이 되고 있습니다. 경쟁은 단순한 비용 결정이 아니라 자동화, 컴플라이언스 깊이, 수직 전문 지식을 축으로 점점 치열해지고 있습니다.

세계 클라우드 매니지드 서비스 시장 동향과 통찰

BFSI의 디지털 퍼스트가 아웃소싱을 강화

은행과 보험 회사는 현재 매니지드 클라우드 서비스를 현대화 로드맵의 핵심으로 삼고 있습니다. 2024년 4월, 타타 컨설턴시 서비스는 AWS와의 제휴를 확대하고 은행 등급 클라우드 현대화 패턴에 대해 2만 5,000명의 엔지니어를 육성할 것을 약속했습니다. 금융기관은 생성형 AI를 통합하고, 컴플라이언스 체크를 자동화하고, 제품 릴리스 사이클을 단축하기 위한 유일한 현실적인 루트로 외부 파트너를 포착하고 있습니다. 하이브리드 설정을 통해 차세대 핵심 시스템을 레거시 플랫폼과 공존할 수 있어 운영 위험을 줄일 수 있습니다. 아시아태평양의 은행에서는 고객 경험 향상이 가장 중요한 과제가 되고 있으며, 클라우드 근대화를 위한 예산 배분이 비용 절감 목표를 상회하고 있습니다.

기업의 멀티클라우드와 하이브리드 복잡성 급증

하이브리드 클라우드나 멀티 클라우드의 도입은 주류가 되고 있지만, 크로스 플랫폼 오케스트레이션을 사내에서 다루는 기업은 적습니다. VMware 보고서에 따르면 회사의 고객 중 93%는 하이브리드 아키텍처를 장기적으로 유지하려는 의도를 보여줍니다. Nutanix의 조사에 따르면 기업의 95%는 2024년에 보안을 개선하고 혁신을 가속화하기 위해 클라우드 간에 용도를 마이그레이션합니다. 그 결과 클라우드 전체의 통합 가시화, 워크로드의 자동 배치, 비용 거버넌스를 실현하는 파트너의 요구가 급증하고 있습니다.

근본적인 데이터 침해에 대한 불안과 위협의 진화

영국의 조사에 따르면 많은 중소기업들은 유연성과 비용면에서의 이점을 인정했음에도 불구하고 보안 격차가 있다는 사실을 알고 있기 때문에 클라우드 마이그레이션을 늦추고 있습니다. 컴플라이언스 감사 및 고객의 신뢰가 심해지면서 엄격한 인증 및 사고 대응 지표를 제시할 수 없는 공급자와의 계약 주기가 장기화되고 있습니다.

부문 분석

매니지드 인프라 서비스는 계속 프로비저닝의 기반을 제공하고 2024년 매출의 37.5%를 차지합니다. 그러나 Managed Security Services는 기업이 지속적인 위협 조사, 제로 트러스트 구현 및 컴플라이언스 보고서 작성을 선호하기 때문에 CAGR 10.7%로 성장을 가속화하고 있습니다. 따라서 관리 보안 시장 세분화 시장 규모는 대부분의 다른 부문을 초과합니다. 매일 수십억 건의 이벤트를 분석하는 바이킹 클라우드 플랫폼 등 AI를 활용한 보안 운영 센터는 체류 시간 단축과 상관관계 자동화를 통해 공급자의 우위성을 강화합니다. 네트워크, 용도, 백업 및 재해 복구 서비스는 계속 견고하며 복잡한 현대화 프로젝트와 레거시 지원을 채널링하고 있습니다.

공급자가 보안을 인프라 및 네트워크 모니터링에 번들로 통합함으로써 통합 플랫폼이 구축되고 스위칭 비용이 증가합니다. 엔터프라이즈 바이어는 통합 대시보드, 일관된 SLA, 멀티클라우드 에스테이트에 걸친 싱글 페인 거버넌스 등 독립된 포인트 솔루션으로는 대응할 수 없는 기능을 높이 평가했습니다.

퍼블릭 클라우드 옵션은 하이퍼스케일 가용 영역과 풍부한 네이티브 도구를 지원하며 2024년에는 52%의 점유율을 유지합니다. 그러나 하이브리드 모델은 고객이 대기 시간 제어, 데이터 레지던시 및 비용 최적화의 이점을 요구하기 때문에 CAGR 11.5%로 가속화되었습니다. 노무라 종합연구소에서 AWS Outposts를 이용함으로써, 일본은 소블린 규제를 충족시키기 위해 AWS 서비스를 On-Premise환경에서 운영할 수 있습니다. Equinix Japan과 Sakura Internet Partnership은 AI 워크로드를 위한 공동 위치와 GPU 지원 서비스가 공공 경제성과 개인 제어를 어떻게 융합하는지를 보여줍니다. 프라이빗 클라우드의 성장은 초저 지연 시간과 틈새 규제 케이스로 제한되며 완만한 것에 머물러 있습니다.

관리 서비스 공급업체는 현재 공용, 개인 및 에지 실적에서 일관된 정책 엔진, 비용 대시보드 및 관측 가능성을 제공함으로써 차별화를 도모하고 있습니다. 가동 시간과 데이터 위치가 까다로운 고객은 공급자가 하이브리드 통합에 익숙하다는 것을 구매의 전제조건으로 삼고 있습니다.

클라우드 매니지드 서비스 시장은 서비스 유형별(매니지드 인프라 서비스, 매니지드 네트워크 서비스 등), 배포 유형별(퍼블릭 클라우드, 프라이빗 클라우드, 하이브리드 클라우드), 기업 규모별(대기업, 중소기업), 최종 사용자 산업별(은행, 금융서비스 및 보험(BFSI), IT 및 텔레콤, 소매 및 E-Commerce 등), 지역별로 분류. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미가 가장 큰 지출국으로 계속 2024년 클라우드 매니지드 서비스 시장에서 37.3%의 점유율을 유지하고 있습니다. 조기 도입, 성숙한 파트너 생태계, 활발한 벤처 자금 조달 장면은 최적화, AI 운영 및 규정 준수 자동화에 대한 수요를 지원합니다. 미국 기업은 성과 기반 계약을 선호하고 캐나다 기업은 국경을 넘어서는 근접성을 활용해 두 지역 간의 회복력을 높입니다. 멕시코 제조는 Industry 4.0 프로그램을 지원하기 위해 Managed Edge Gateway를 통합합니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 9.3%로 성장을 지속하고, 정부가 디지털화를 조성하며 광대역 액세스가 확대됩니다. Huawei Cloud 파트너 네트워크는 현재 45,000개 이상의 기업을 대상으로 12,000개의 마켓플레이스를 제공합니다. 인도의 IT 메이저가 세계 서비스 수출을 위해 기존 부동산을 개편합니다. 한국의 5G 백본은 엣지를 많이 사용하는 워크로드를 가속시킵니다. 호주는 고립되어 있기 때문에 세계 리소스와 원활하게 상호 연결되는 로컬 관리 노드에 대한 수요가 증가하고 있으며, 오픈 텍스트는 2025년에 이 분야에 엄청난 투자를 하고 있습니다.

유럽의 규제 모자이크는 데이터 레지던시와 지속가능성 증명에 대한 공급자의 차별화를 촉진합니다. 독일의 중견 제조업은 Industrie 4.0을 위해 매니지드 서비스를 활용하고 프랑스와 이탈리아의 퍼블릭 클라우드 투자는 국가 AI 전략 하에서 증가하고 있습니다. 영국의 금융 기관은 PRA의 기대에 부응하기 위해 통합 위협 관리 제품군을 위탁합니다. 이 지역의 녹색 거래 및 CSRD 보고서는 투명성이 높은 배출량 측정 기준을 갖지 않는 공급자에 대한 수요를 감소시킵니다. Microsoft의 100% 재생에너지로 데이터센터를 제공하는 약속은 조달 의사 결정에 영향을 미칩니다.

남미와 중동 및 아프리카는 관리 서비스가 현지의 제한된 인프라를 피할 수 있는 아직 시작되었지만 미래성이 높은 지역입니다. Expereo는 기업이 지리적으로 분산된 운영에서 일관된 용도 성능을 제공하기 위해 SD-WAN과 SASE에 대한 지출을 늘리고 있다고 지적합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- BFSI의 디지털 퍼스트의 대처가 매니지드 클라우드의 아웃소싱을 가속

- 기업에서의 멀티클라우드와 하이브리드의 복잡성의 급증

- 사이버 리스크와 컴플라이언스가 증가함에 따라 24시간 관리형 보안 강화

- CIO 예산에 대한 비용 최적화 압력(운영 비용 대 설비 투자)

- FinOps의 도입에 의해 계속적인 클라우드 코스트 거버넌스의 새로운 수요 창출

- 지속가능성과 그린클라우드의 의무화에 의해 프로바이더의 선택이 변화

- 시장 성장 억제요인

- 데이터 유출에 대한 불안은 뿌리 깊고, 위협의 정세는 변화하고 있다

- 벤더 락인의 위험에 의해 대규모 워크로드의 이행이 지연된다

- 공인 클라우드 아키텍트 인재의 세계 부족

- 분산된 데이터 주권법은 컴플라이언스 비용을 증대시킨다

- 가치/공급망 분석

- 규제 상황

- 기술 전망(엣지, 5G, Gen-AI Ops)

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 서비스 유형별

- 매니지드 인프라 서비스

- 매니지드 네트워크 서비스

- 매니지드 시큐리티 서비스

- 매니지드 용도 서비스

- 기타 서비스 유형

- 전개 모델별

- 퍼블릭 클라우드

- 프라이빗 클라우드

- 하이브리드 클라우드

- 기업 규모별

- 대기업

- 중소기업

- 최종 사용자 업계별

- BFSI

- IT 및 통신

- 소매업 및 전자상거래

- 헬스케어 및 생명과학

- 제조업

- 정부 및 공공 부문

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amazon Web Services(AWS)

- Microsoft Corp.(Azure Managed Services)

- International Business Machines Corp.(IBM)

- Accenture plc

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Ericsson

- Fujitsu Ltd.

- NEC Corp.

- NTT DATA Corp.

- DXC Technology Co.

- Lumen Technologies, Inc.

- Rackspace Technology, Inc.

- Tata Consultancy Services Ltd.

- Wipro Ltd.

- HCLTech

- Capgemini SE

- Cognizant Technology Solutions

- Infosys Ltd.

- Atos SE

제7장 시장 기회와 장래의 전망

SHW 25.11.11The cloud managed services market size reaches USD 140.96 billion in 2025 and is set to grow to USD 222.81 billion by 2030, reflecting a 9.59% CAGR.

Enterprises continue moving from asset-heavy infrastructure ownership to pay-as-you-go operating models that improve agility, free cash and shorten innovation cycles. Demand rises sharply as multi-cloud sprawl and cybersecurity threats strain in-house IT teams. Financial-services digital mandates, AI-driven workloads and sustainability targets intensify the need for expert external management. North America holds the lion's share of spending, yet Asia Pacific's large untapped base and pro-cloud policy environment make it the fastest-expanding region. Competition increasingly revolves around automation, compliance depth and vertical expertise rather than simple cost arbitrage.

Global Cloud Managed Services Market Trends and Insights

BFSI Digital-First Mandates Intensify Outsourcing

Banks and insurers now place managed cloud services at the core of their modernization roadmaps. In April 2024 Tata Consultancy Services expanded its AWS alliance, pledging to train 25,000 engineers on bank-grade cloud modernization patterns. Institutions view external partners as the only realistic route to embed generative-AI, automate compliance checks and shorten product release cycles. Hybrid set-ups allow next-generation core systems to coexist with legacy platforms, lowering operational risk. Asia-Pacific banks stand out: budget allocations for cloud modernization now outweigh cost-cutting targets as customer-experience gains become paramount.

Surge in Multi-Cloud and Hybrid Complexity Among Enterprises

Hybrid and multi-cloud adoption has become mainstream, yet few firms can master cross-platform orchestration internally. VMware reports that 93% of its customers intend to keep hybrid architectures long term.Nutanix finds that 95% of enterprises shifted applications between clouds in 2024 to improve security or speed innovation. The result is a booming need for partners who deliver unified visibility, automated workload placement, and cost governance across cloud estates.

Persistent Data-Breach Anxiety and Evolving Threat Landscape

UK research shows many SMEs still delay cloud migration because of perceived security gaps, even though they acknowledge benefits in flexibility and cost. Compliance audits and customer trust weigh heavily, lengthening deal cycles for providers that cannot produce rigorous certifications and incident-response metrics.

Other drivers and restraints analyzed in the detailed report include:

- Heightened Cyber-Risk and Compliance Push 24/7 Managed Security

- Cost-Optimization Pressure on CIO Budgets (Op-Ex vs Cap-Ex)

- Vendor Lock-In Risks Slow Large-Scale Workload Migration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Managed infrastructure services continue to deliver foundational provisioning, capturing 37.5% of 2024 revenue. Yet managed security services grow faster at 10.7% CAGR as firms prioritize continuous threat hunting, zero-trust enforcement and compliance reporting. The cloud managed services market size for managed security will therefore outpace most other segments. AI-driven security operations centers, such as VikingCloud's platform that analyzes billions of events daily, strengthen provider advantage by shortening dwell time and automating correlation. Network, application, backup and disaster-recovery services remain steady, channeling complex modernization projects and legacy support.

Second-order effects ripple across the cloud managed services industry as providers bundle security with infrastructure and network oversight, creating integrated platforms that raise switching costs. Enterprise buyers value unified dashboards, consistent SLAs and single-pane governance across multi-cloud estates features that independent point solutions struggle to match.

The public-cloud option retains 52% cloud managed services market share in 2024, anchored by hyperscale availability zones and rich native tooling. The hybrid model, however, accelerates at 11.5% CAGR as clients seek latency control, data residency and cost optimization advantages. Use of AWS Outposts by Nomura Research Institute lets Japanese banks run AWS services on-premises to satisfy sovereignty rules. Equinix Japan's partnership with Sakura Internet illustrates how co-location and GPU-ready services blend public economics with private control for AI workloads. Private-cloud growth remains modest, reserved for ultra-low-latency or niche regulatory cases.

Managed-service vendors now differentiate by offering consistent policy engines, cost dashboards and observability across public, private and edge footprints. Clients with strict uptime or data-location mandates increasingly treat provider proficiency in hybrid integration as a purchase prerequisite.

Cloud Managed Services Market is Segmented by Service Type (Managed Infrastructure Services, Managed Network Services, and More), Deployment Type (Public Cloud, Private Cloud, Hybrid Cloud), Enterprise Size (Large Enterprise and SMEs), End User Industry (BFSI, IT and Telecom, Retail and E-Commerce, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America remains the largest spender, retaining 37.3% share of the cloud managed services market in 2024. Early adoption, mature partner ecosystems and a robust venture funding scene sustain demand for optimization, AI operations and compliance automation. US enterprises favor outcome-based contracts, while Canadian firms leverage cross-border proximity for dual-region resilience. Mexican manufacturers integrate managed edge gateways to underpin Industry 4.0 programs.

Asia Pacific records the fastest 9.3% CAGR through 2030 as governments subsidize digitization and broadband access widens. Huawei Cloud's partner network now counts more than 45,000 firms and 12,000 marketplace offers, linking finance, telecom and AI start-ups across the region. India's IT majors revamp legacy estates for global service exports. Japan's high trust threshold spurs demand for hybrid setups backed by local data centers, while South Korea's 5G backbone accelerates edge-heavy workloads. Australia's isolation intensifies calls for local managed nodes that interconnect seamlessly with global resources, an area where OpenText is investing heavily in 2025.

Europe's regulatory mosaic drives provider differentiation on data-residency and sustainability credentials. Germany's Mittelstand manufacturers tap managed services for Industrie 4.0, while French and Italian public-cloud spend rises under national AI strategies. UK financial institutions commission integrated threat-management suites to align with PRA expectations. The region's Green Deal and CSRD reporting dampen demand for providers without transparent emissions metrics; Microsoft's pledge to power data centers with 100% renewable energy influences sourcing decisions.

South America and the Middle East and Africa represent nascent yet high-potential territories where managed services circumvent limited local infrastructure. Expereo notes businesses boosting spending on SD-WAN and SASE to deliver consistent application performance across geographically dispersed operations.

- Amazon Web Services (AWS)

- Microsoft Corp. (Azure Managed Services)

- International Business Machines Corp. (IBM)

- Accenture plc

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- Ericsson

- Fujitsu Ltd.

- NEC Corp.

- NTT DATA Corp.

- DXC Technology Co.

- Lumen Technologies, Inc.

- Rackspace Technology, Inc.

- Tata Consultancy Services Ltd.

- Wipro Ltd.

- HCLTech

- Capgemini SE

- Cognizant Technology Solutions

- Infosys Ltd.

- Atos SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 BFSI digital-first initiatives accelerate managed-cloud outsourcing

- 4.2.2 Surge in multi-cloud and hybrid complexity among enterprises

- 4.2.3 Heightened cyber-risk and compliance push 24/7 managed security

- 4.2.4 Cost-optimization pressure on CIO budgets (Op-Ex vs Cap-Ex)

- 4.2.5 FinOps adoption creates new demand for continuous cloud cost governance

- 4.2.6 Sustainability and green-cloud mandates reshape provider selection

- 4.3 Market Restraints

- 4.3.1 Persistent data-breach anxiety and evolving threat landscape

- 4.3.2 Vendor lock-in risks slow large-scale workload migration

- 4.3.3 Global shortage of certified cloud-architect talent

- 4.3.4 Fragmented data-sovereignty laws inflate compliance cost

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (Edge, 5G, Gen-AI Ops)

- 4.7 Porters Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Managed Infrastructure Services

- 5.1.2 Managed Network Services

- 5.1.3 Managed Security Services

- 5.1.4 Managed Application Services

- 5.1.5 Other Service Type

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid Cloud

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 BFSI

- 5.4.2 IT and Telecom

- 5.4.3 Retail and E-Commerce

- 5.4.4 Healthcare and Life Sciences

- 5.4.5 Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Other End-Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services (AWS)

- 6.4.2 Microsoft Corp. (Azure Managed Services)

- 6.4.3 International Business Machines Corp. (IBM)

- 6.4.4 Accenture plc

- 6.4.5 Cisco Systems, Inc.

- 6.4.6 Huawei Technologies Co., Ltd.

- 6.4.7 Ericsson

- 6.4.8 Fujitsu Ltd.

- 6.4.9 NEC Corp.

- 6.4.10 NTT DATA Corp.

- 6.4.11 DXC Technology Co.

- 6.4.12 Lumen Technologies, Inc.

- 6.4.13 Rackspace Technology, Inc.

- 6.4.14 Tata Consultancy Services Ltd.

- 6.4.15 Wipro Ltd.

- 6.4.16 HCLTech

- 6.4.17 Capgemini SE

- 6.4.18 Cognizant Technology Solutions

- 6.4.19 Infosys Ltd.

- 6.4.20 Atos SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment