|

시장보고서

상품코드

1939697

유방 임플란트 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Breast Implants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

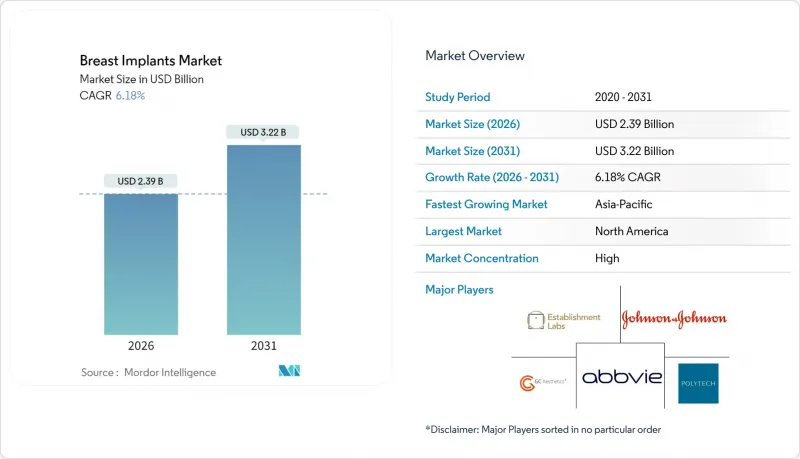

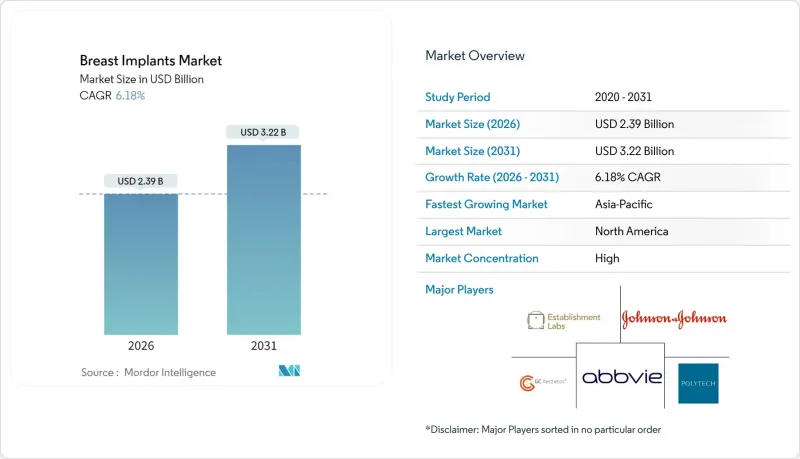

유방 임플란트 시장은 2025년에 22억 5,000만 달러로 평가되며, 2026년 23억 9,000만 달러에서 2031년까지 32억 2,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 6.18%로 예상됩니다.

이러한 확대는 유방 절제술 후 재건 수술 증가, 미용 목적의 유방 확대 수술에 대한 사회적 수용성 확대, 그리고 빠른 제품 혁신과 함께 이루어지고 있습니다. 실리콘 임플란트가 여전히 전체 수요의 대부분을 차지하고 있지만, 구조화된 식염수 임플란트는 실리콘과 유사한 촉감을 제공하면서 조용한 파열에 대한 우려를 해소할 수 있다는 장점으로 인해 점점 더 많은 인기를 얻고 있습니다. 지역별로는 아시아태평양이 의료관광 거점 확대, 중산층 소비 확대, 신규 승인 건수 급증 등을 배경으로 가장 빠른 성장세를 보이고 있습니다. 한편, 북미는 성숙한 상환제도와 높은 수준의 외과의사 전문성을 바탕으로 선도적인 지위를 유지하고 있습니다. 지정학적 혼란이 가중되면서 원자재 취약성이 노출됨에 따라 각 제조업체들은 연간 매출의 3-5%를 공급망 탄력성 강화, 계약 유연성 확보, 이중 소싱 전략에 투입한다는 방침을 세우고 있습니다.

세계 유방 임플란트 시장 동향과 인사이트

높은 유방암 발병률

미국내 신규 침윤성 암 진단 건수는 2025년 31만 6,950건에 달할 것으로 예상되며, 2024년 대비 2% 증가할 것으로 전망됩니다. 이는 지속적인 재건 수요를 지원합니다. 인종 및 사회경제적 격차는 여전히 존재하며, 백인 환자의 재건 수술률은 약 67%인 반면 흑인 여성은 54%에 불과한 것으로 나타났습니다. 이는 접근 장벽이 해소되면 미개발 성장 여지가 있다는 것을 보여줍니다. 재수술 위험이 18% 더 높음에도 불구하고 즉각적인 재건 수술의 인기가 높아지는 이유는 환자들이 전반적인 회복 기간 단축을 중요하게 생각하기 때문입니다. 북미의 보험 적용 의무화로 인해 본인 부담금이 더욱 낮아져 수술 건수가 증가하고 있습니다.

유방 수술 수요 급증

소비자의 취향은 자연스러운 가슴의 미학을 재현하는 '감지할 수 없는' 가슴성형술로 옮겨가고 있습니다. 모티바의 부드러운 실크 쉘과 그에 상응하는 첨단 텍스처는 피막 수축의 발생률을 감소시켜 외과 의사들의 지지를 받고 있습니다. 동시에, 피부 조임 기술의 향상에 힘입어 2024년 미국의 유방 거상술 시행 빈도는 6% 증가했습니다. 임플란트 라인업을 이러한 동향(볼륨, 프로젝션, 촉감의 현실감 균형)에 맞춘 클리닉은 소비자의 선택적 지출을 확보할 수 있습니다.

수술 후 합병증과 위험

세계에서 보고된 BIA-ALCL 확진 사례는 1,290건이며, 대부분 텍스처드 쉘과 연관성이 있는 것으로 알려져 있습니다. 2024년, FDA는 박스형 경고문과 환자 체크리스트 의무화, 컴플라이언스 비용 상승, 리스크에 대한 투명성 논의가 촉진되었습니다. 매끄러운 표면의 임플란트 및 나노 텍스처링 기술은 이러한 우려를 해결하고 있지만, 소송의 추세로 인해 외과 의사의 보험료가 상승하고 있으며, 미국 일부 주에서는 2024년에 전년 대비 15%의 상승을 보였습니다.

엄격한 규제와 지방 이식의 대안

유럽 의료기기 규정(MDR) 전환에 따라 2027년까지 재인증이 의무화되어 감사 비용 증가와 인증기관의 승인을 받지 못하면 구식 기기의 판매 지연이 발생합니다. 동시에 합성 물질을 우려하는 환자들을 끌어들이는 하이브리드 지방이식 기술이 등장하고 있습니다. 이에 반해 의료기기 제조업체들은 임플란트와 무세포 진피 매트릭스(ADM)를 결합하여 연조직의 발판 형성을 지원하는 제품을 제공합니다. 자가조직이식술과 경쟁하는 것이 아니라 보완적인 대안으로 자리매김하고 있습니다.

부문 분석

2025년 기준 실리콘 임플란트는 유방 임플란트 시장의 86.62% 점유율을 유지하고 있으며, 응집성 겔에 의한 안정성과 연조직에 대한 적합성을 높이 평가받고 있습니다. 실리콘 제품의 유방 보형물 시장 규모는 계속 확대될 것으로 예상되며, 구조화 식염수 보형물의 CAGR 7.34%는 채택이 가속화되고 있음을 보여줍니다. 구조화된 임플란트는 MRI 검사가 필요하지 않아 안전성을 중시하는 소비자들에게 선호되고 있으며, 수술 중 충전 조정을 통해 대칭성을 미세 조정할 수 있습니다. 모양 기억력과 낮은 누출 위험으로 지지받는 구미베어형 코히시브 임플란트에 비해, 구조화된 식염수 임플란트는 파열시 가시성으로 인해 재수술 후보자들로부터 지지를 받고 있습니다.

실리콘 임플란트 제조업체들은 제품 수명 기간 중 캡슐 수축 및 파열시 교체를 보장하는 연장 보증을 제공합니다. 환자의 해부학적 구조에 3D 이미지를 겹쳐서 보여주는 디지털 유방 사이저는 수술 전 계획을 개선하고, 유방 보형물 시장에서 식염수 시장의 성장세에도 불구하고 실리콘 제품의 기존 우위를 더욱 강화합니다.

2025년 기준 원형 보형물이 유방 보형물 시장 규모의 82.88%를 차지하고 있지만, 해부학적 형태의 유닛은 원형의 11.3% 대비 3.4%로 현저히 낮은 피막 수축률로 인해 더욱 빠른 성장이 예상됩니다. 낮은 상부 돌출을 선호하는 동아시아 및 유럽 환자들은 눈물방울 모양을 선호하는 경향이 있습니다. 2025년에 출시된 매끄러운 표면의 해부학 모델은 ALCL 위험과 관련된 과도한 거칠기 없이 포켓 위치를 안정화시키는 레이저 에칭 공정을 통해 기존의 회전 문제를 해결했습니다.

하이브리드 젤 필링의 특허기술은 형상 유지를 위한 경질 베이스층과 촉감을 높이는 연질 외층이라는 이중 점도 구조를 융합한 기술입니다. 이를 통해 해부학적 임플란트는 촉감의 현실감에서 원형과 경쟁할 수 있게 되었습니다. 홍보 캠페인은 이러한 혁신성을 강조하여 외과 의사의 채용을 촉진하고 해부학 카테고리로 시장 점유율을 확대하기 위해 노력하고 있습니다.

지역별 분석

북미는 2025년에도 유방 임플란트 시장에서 40.68%의 점유율을 유지했습니다. 2024년 9월 미국 식품의약국(FDA)의 승인을 받은 모티바 스무스실크는 미국 최초의 비텍스처드 나노 표면 임플란트로 도입되어 디바이스 선택 경쟁이 치열해지고 있습니다. 규제 개정으로 모든 임플란트에 블랙박스 경고가 의무화되고, 환자 의사결정 체크리스트의 도입이 요구되고 있습니다. 이로 인해 정보에 입각한 선택이 촉진되는 반면, 의료 서비스 프로바이더의 업무 부담은 가중되고 있습니다. 미국 외과의사들은 지역적 미적 이상을 반영하여 유럽 동료들에 비해 높은 프로젝션 임플란트를 선택하는 경향이 두드러집니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 7.48%로 가장 빠르게 성장할 것으로 예측됩니다. 의료관광 루트를 통해 수술 후 스파 케어와 함께 저렴한 가격의 가슴성형 수술을 받기 위해 매년 수천 명의 환자들이 태국과 한국으로 유입되고 있습니다. 중국 국가약품감독관리국(NMPA)의 2024년 말 모티바인 임플란트 승인(중국내 10년 만의 유방 임플란트 승인)은 민간 클리닉 네트워크의 잠재적 수요를 이끌어 낼 것으로 예측됩니다. 호주에서 진행된 PCL(폴리카프로락톤) 스캐폴드 기반 완전 흡수성 임플란트 임상시험에서 12개월 경과 시점에 심각한 합병증이 전혀 보고되지 않아 실리콘 임플란트의 지위를 뒤흔들 수 있는 대체품이 개발 파이프라인에 있다는 것을 보여주었습니다. 인도네시아에서는 전문의 부족으로 인해 해외 의료 관광이 여전히 활발히 이루어지고 있으며, 국제 클리닉 체인이 채우려는 지역적 서비스 능력의 격차를 강조하고 있습니다.

유럽은 전 세계 판매의 상당 부분을 차지하는 반면, 더 엄격한 규제에 직면해 있습니다. 의료기기 규정(MDR)에 따라 2027년까지 유방 임플란트 재인증이 의무화되어 있는 가운데, GC에스테틱은 2022년 첫 MDR 승인 임플란트를 출시하여 이 목표를 조기에 달성했다(gcaesthetics.com). 영국에서는 2024년 5,202건의 미용 유방 수술이 시행되어 거시경제적 역풍에도 불구하고 미용 수요가 6% 증가했습니다. 텍스처 임플란트 리콜의 영향은 여전히 남아 있으며, 외과 의사들은 매끄러운 또는 미세한 텍스처의 대체품으로 눈을 돌리고 있습니다. 한편, 독일과 프랑스의 보험사들은 즉각적인 재건을 동반한 예방적 유방절제술에 대한 보험 적용을 확대하여 재건수술 건수 증가를 지원하고 있습니다.

남미와 중동 및 아프리카(MEA)는 전략적으로 유망한 시장으로 큰 점유율을 차지하고 있습니다. 브라질은 세계에서 1인당 가슴성형 수술률이 가장 높은 국가 중 하나이며, 현지 제조업체들은 점유율을 유지하기 위해 공격적인 가격정책을 펼치고 있습니다. 걸프협력회의(GCC) 회원국에서는 두바이와 도하에 위치한 고급 의료관광 시설들이 북미에 가지 않고도 미국 FDA 승인을 받은 임플란트를 원하는 부유층 외국인들을 끌어들이고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 동향

KSA 26.03.06The breast implants market was valued at USD 2.25 billion in 2025 and estimated to grow from USD 2.39 billion in 2026 to reach USD 3.22 billion by 2031, at a CAGR of 6.18% during the forecast period (2026-2031).

The expansion reflects a combination of rising post-mastectomy reconstruction volumes, wider social acceptance of cosmetic augmentation, and rapid product innovation. Silicone devices continue to dominate overall unit demand, but structured saline implants are gaining momentum because they eliminate silent-rupture concerns while offering a silicone-like feel. Across regions, Asia Pacific is the fastest-growing arena, powered by medical-tourism hubs, accelerating middle-class spending, and a surge of new approvals, whereas North America preserves its leadership position through mature reimbursement pathways and advanced surgeon expertise. Heightened geopolitical disruptions have exposed raw-material vulnerabilities, prompting manufacturers to earmark 3-5% of annual revenue for supply-chain resiliency, contract flexibility, and dual-sourcing strategies.

Global Breast Implants Market Trends and Insights

High burden of breast cancer

New invasive cancer diagnoses in the United States are expected to reach 316,950 in 2025, a 2% increase from 2024, reinforcing sustained reconstruction demand. Racial and socioeconomic disparities persist-White patients undergo reconstruction at nearly 67% versus 54% for Black women, highlighting untapped growth if access barriers are resolved. Immediate reconstruction enjoys growing popularity despite an 18% higher risk of reoperation, because patients value shorter overall recovery. Insurance mandates in North America further lower out-of-pocket costs, elevating procedure volumes.

Surge in demand for breast surgery

Consumer preference has shifted toward "undetectable" augmentations that mirror natural breast aesthetics. Motiva's SmoothSilk shell and similarly advanced textures reduce capsular-contracture incidence, capturing surgeon endorsement. Simultaneously, breast-lift frequencies rose 6% in the United States during 2024, supported by better skin-tightening technology. Clinics that align implant portfolios with these trends-balancing volume, projection, and tactile authenticity-stand to capture discretionary consumer spend.

Post-procedure complications and risks

Global reporting registers 1,290 confirmed BIA-ALCL cases, mostly linked to textured shells. In 2024 the FDA mandated boxed warnings and patient checklists, elevating compliance costs yet encouraging transparent risk discussion. Smooth-surface implants and nano-texturing techniques address these concerns, but litigation trends elevate surgeon insurance premiums; in some U.S. states premiums rose 15% year-over-year in 2024.

Stringent regulations & fat-grafting alternatives

The European MDR transition compels recertification by 2027, adding audit fees and delaying legacy device sales unless notified-body sign-off is obtained. Concurrently, hybrid fat-transfer techniques lure patients wary of synthetic materials. Device makers counter by bundling implants with acellular dermal matrices (ADM) that support soft-tissue scaffolding, positioning implants as complementary rather than competing with autologous options.

Other drivers and restraints analyzed in the detailed report include:

- Technological advancement in breast implants

- Rise in medical tourism

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone implants retained an 86.62% share of the breast implant market in 2025, favored for their cohesive-gel stability and soft-tissue mimicry. The breast implant market size for silicone lines will continue to expand; however, structured saline's 7.34% CAGR indicates accelerating uptake. Structured devices avoid MRI monitoring, appeal to safety-conscious consumers, and allow intra-operative fill adjustment to refine symmetry. Gummy-bear cohesive implants still appeal through shape memory and lower leak risk, but structured saline's transparent rupture profile garners support among revision-surgery candidates.

Silicone implant manufacturers respond with warranty extensions covering capsule contracture and rupture replacement for the implant's lifetime. Digital breast sizers that overlay 3-D imaging onto patient anatomy improve pre-procedure planning, further reinforcing silicone incumbency despite saline's momentum in the breast implant market.

Round implants owned 82.88% of the breast implants market size in 2025, yet anatomical units will grow more rapidly due to a significantly lower capsular-contracture rate of 3.4% vs. 11.3% for rounds. East-Asian and European patients, who often prefer modest upper-pole projection, gravitate toward teardrop geometrics. Smooth-surface anatomical models launched in 2025 tackle historical rotation concerns, aided by laser-etched texturing that stabilizes pocket positioning without aggressive roughness linked to ALCL risk.

Hybrid gel-fill patents blend dual-viscosity layers-a firmer base for shape and a softer outer layer for palpability-allowing anatomical implants to compete with rounds on tactile authenticity. Promotional campaigns highlight these innovations, propelling surgeon adoption and nudging market share toward anatomical categories.

Breast Implant Market Report is Segmented by Product Type (Silicone Implants, Cohesive Gel Implants, and More), Shape (Round and Anatomical), Application (Reconstructive Surgery and Cosmetic Surgery), End-User (Hospitals, and More), and Geography (North America, Europe, and More). The Market and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained a 40.68% share of the breast implants market in 2025. The FDA's September 2024 approval of Motiva SmoothSilk introduced the first non-textured nano-surface implant in the United States, intensifying device choice competition. Regulatory updates impose black-box warnings on all implants and require patient decision checklists, fostering informed choice yet adding administrative overhead for providers. U.S. surgeons exhibit distinctive practice patterns, often selecting higher-projection implants relative to their European peers, reflecting regional aesthetic ideals.

Asia Pacific is forecast to be the fastest-growing region at a 7.48% CAGR to 2031. Medical-tourism corridors funnel thousands of patients annually into Thailand and South Korea for cut-price augmentations bundled with post-operative spa care. China's NMPA authorization of Motiva implants in late 2024-China's first breast-implant clearance in a decade-unleashes pent-up demand among private-clinic networks. Australia's clinical trials of PCL scaffold-based, fully resorbable implants reported zero major complications at 12-month follow-up, indicating a pipeline of alternatives that could eventually disrupt silicone incumbency. In Indonesia, outbound medical tourism remains prevalent because of limited specialist availability, revealing regional service-capacity gaps that international clinic chains aim to fill.

Europe accounts for a substantial slice of global sales but confronts stricter regulation. The Medical Device Regulation (MDR) compels breast-implant recertification by 2027, and GC Aesthetics met the milestone early by launching the first MDR-approved implant in 2022 gcaesthetics.com. The U.K. tallied 5,202 cosmetic breast procedures in 2024, representing a 6% increase in aesthetic demand despite macroeconomic headwinds. Textured-implant recall aftermath lingers, nudging surgeons toward smooth or micro-textured alternatives. Meanwhile, insurers in Germany and France expanding reimbursement for prophylactic mastectomy with immediate reconstruction support reconstructive volume growth.

South America and the Middle East & Africa (MEA) collectively capture a significant slice and hold strategic promise. Brazil hosts one of the highest per-capita augmentation rates worldwide, and local manufacturers aggressively price to maintain share. In the Gulf Cooperation Council (GCC) states, premium medical-tourism complexes in Dubai and Doha attract affluent expatriates seeking U.S.-FDA-approved implants without traveling to North America.

- Abbvie

- Anita Dr. Helbig GmbH

- Bimini Health Tech

- Cereplas SAS

- Establishment Labs

- GC Aesthetics

- Groupe Sebbin

- HansBiomed Co. Ltd.

- Johnson & Johnson

- Laboratoires Expanscience

- Pofam Poznan Sp.z.o.o

- Polytech Health & Aesthetics

- Shanghai Kangning Medical Device Co.

- Silimed Industria de Implantes Ltda.

- Wanhe Plastic Materials Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Burden of Breast Cancer

- 4.2.2 Surge in Demand for Breast Surgery

- 4.2.3 Technological Advancement in Breast Implants

- 4.2.4 3-D Imaging & Simulation Tools Raising Patient Conversion Rates

- 4.2.5 Rise in Medical Tourism for Breast Surgeries in Different Countries Coupled with Increased Awareness and Acceptance for Breast Surgery

- 4.2.6 Accelerating the Adoption of Advanced Implants and Direct-to-consumer Marketing Influencing Demand

- 4.3 Market Restraints

- 4.3.1 Post Complications and Risks Associated with Breast Implant

- 4.3.2 Supply Shortages for Medical Grade Material

- 4.3.3 Stringent Regulations and Availability of Alternatives

- 4.3.4 Rise in Product-Liability Insurance Premiums for Surgeons

- 4.4 Supply Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Product Type

- 5.1.1 Silicone Implants

- 5.1.2 Cohesive Gel (Form-Stable) Implants

- 5.1.3 Saline Implants

- 5.1.4 Structured Saline Implants

- 5.1.5 Hydrogel & Other Fillers

- 5.2 By Shape

- 5.2.1 Round

- 5.2.2 Anatomical (Teardrop)

- 5.3 By Application

- 5.3.1 Reconstructive Surgery

- 5.3.2 Cosmetic (Augmentation) Surgery

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Cosmetology Clinics & Medical Spas

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 AbbVie Inc. (Allergan Aesthetics)

- 6.3.2 Anita Dr. Helbig GmbH

- 6.3.3 Bimini Health Tech

- 6.3.4 Cereplas SAS

- 6.3.5 Establishment Labs S.A.

- 6.3.6 GC Aesthetics

- 6.3.7 Groupe Sebbin SAS

- 6.3.8 HansBiomed Co. Ltd.

- 6.3.9 Johnson & Johnson

- 6.3.10 Laboratories Arion

- 6.3.11 Pofam Poznan Sp.z.o.o

- 6.3.12 Polytech Health & Aesthetics GmbH

- 6.3.13 Shanghai Kangning Medical Device Co.

- 6.3.14 Silimed Industria de Implantes Ltda.

- 6.3.15 Wanhe Plastic Materials Co.

7 Market Opportunities and Future Trends

- 7.1 Market Opportunities & Future Outlook

- 7.2 White-Space and Unmet-Need Assessment