|

시장보고서

상품코드

1850962

전문 서비스 자동화 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Professional Services Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

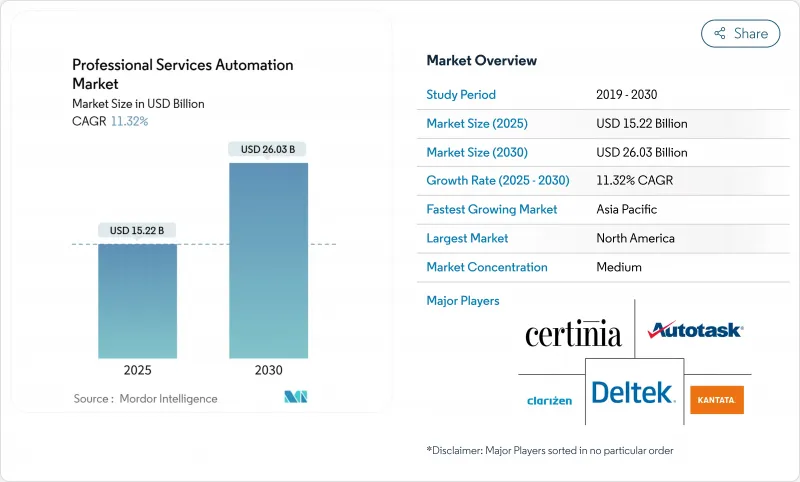

전문 서비스 자동화 시장 규모는 2025년에 152억 2,000만 달러, 예측 기간(2025-2030년)의 CAGR은 11.32%를 나타내고, 2030년에는 260억 3,000만 달러에 달할 것으로 예측됩니다.

클라우드 퍼스트의 변화, AI 주도 워크플로우 오케스트레이션, 프로젝트와 캐쉬의 통합적인 시각화의 필요성이 이러한 확대를 지원하고 있습니다. 기업은 인력 배치, 마진 관리, 고객 성과에 대한 지침이 되는 예측 분석을 통합하려고 경쟁하고 있으며, 성과 기반 청구 모델은 보다 풍부한 성능 측정 기능에 박차를 가하고 있습니다. 2024년 클라우드 도입률은 69.3%로, 확장 가능한 구독 기반 딜리버리가 현재 대부분의 신규 도입을 지원하고 있음을 증명하고, 월말 마감 전에 가동 리스크를 표면화시키는 AI 모듈이 의사결정 사이클을 가속시킵니다. 인재 부족이 계속되는 가운데, 벤더는 로우 코드 구성, 모범 사례 템플릿의 내장, 복잡한 롤아웃의 위험을 경감하는 긴밀한 ERP/CRM 커넥터에 의해 차별화를 도모하고 있습니다. 경쟁 우위는 플랫폼의 폭에 달려 있습니다. 프로젝트 관리, 리소싱, 송장 작성 및 분석을 하나의 작업 공간으로 통합한 제품군은 더 많은 시트 수를 얻고 수익 확대를 촉진합니다.

세계의 전문 서비스 자동화 시장 동향과 통찰

중소기업에서 클라우드 PSA 채택

중소기업은 전문 서비스 자동화 시장에서 가장 역동적인 성장을 추진하고 있습니다. 이는 공공 부문의 디지털화 보조금과 간단한 SaaS 온보딩이 역사적인 인프라 장애물을 제거했기 때문입니다. 싱가포르의 Productivity Solutions Grant는 구독 요금의 최대 50%를 환불하여 영세 기업이 이전에 세계 컨설팅 회사만 사용할 수 있는 기능을 제공합니다. 또한 구독 가격은 선행 투자인 CAPEX를 관리 가능한 OPEX로 변환하여 공급업체가 기능을 가속화하는 데 필요한 자금을 정기적으로 확보할 수 있도록 합니다. 자나 스몰 파이낸스 은행은 UiPath의 자동화 스위트를 도입한 후 턴어라운드 시간을 65-70% 단축했습니다. 이러한 결과는 10명 규모의 기업에서도 엔터프라이즈급 오케스트레이션이 가능하며 전문 서비스 부문에서 경쟁의 공정성을 재구성할 수 있음을 입증합니다.

리소스 및 마진의 실시간 시각화 추진

거시경제 변동성은 분기별 검토가 아니라 실시간으로 가동률 격차와 마진 누출을 밝혀야 합니다. BeyondTrust는 Certinia PSA를 채택하고 세밀한 기술 매트릭스와 라이브 피드백 루프를 결합하여 리소스 사용률을 20% 향상시켰습니다. 대시보드는 과도한 엔지니어 할당 및 이정표 자금 부족을 밝혀 수익성을 저하시키기 전에 비용 초과를 억제합니다. 시간대에 걸쳐 작업하는 프로젝트 팀이 늘어나는 동안 즉시 차이가 경고되므로 관리자는 납기를 초과하지 않고 작업 순서를 변경할 수 있습니다. 임베디드 AI 시뮬레이터는 인적 자원 조달 시나리오를 압력 테스트하여 요율 카드 할인 및 범위 변경으로 인해 예상 대략적인 이익률을 저하시키지 않습니다.

멀티 테넌트 클라우드의 데이터 프라이버시 우려

GDPR(EU 개인정보보호규정)은 엄격한 거주와 동의 규칙을 부과하여 고객 기록, 프로젝트 노트 및 직원 타임시트를 다루는 공유 테넌트 아키텍처의 검토를 강화하고 있습니다. 현재 규제 대상 권고 사례는 암호화 키, 지역별 페일오버 및 감사 대응 로깅을 규정하는 데이터 처리 추가 조항을 협상하고 있습니다. 하이퍼스케일 클라우드는 SOC2나 ISO-27001 인증을 받았지만, 싱글 테넌트나 EU의 소블린 존을 선호하는 고객도 있어 순수한 클라우드로의 전환이 늦어져 단기적으로는 전문 서비스 자동화 시장의 보급에 약간 영향을 주고 있습니다.

부문 분석

2024년 전문 서비스 자동화 시장 규모의 69.3%를 클라우드 배포가 차지하고, 2030년까지의 CAGR은 13.2%를 보일 것으로 예측됩니다. 자동 패치 적용, 탄력적인 컴퓨팅 및 구독 가격은 분산 워크 포스의 현실과 CAPEX를 OPEX로 이동시키는 CFO의 요구에 부합합니다. On-Premise PSA는 방화벽 뒷면에 데이터를 저장해야 하는 엄격한 규제 영역에서 살아나고 있지만, 이러한 분야에서도 클라우드에서의 하이브리드 인접 분석 또는 모바일 타임 캡처가 지원을 받고 있습니다. 플랫폼 공급업체는 AWS 및 Microsoft와의 제휴를 강화하고 세계 가용 영역 및 공유 AI 가속기를 활용합니다. 이러한 움직임은 구현 주기를 몇 분기에서 몇 주로 단축시켜 대응 가능한 전문 서비스 자동화 시장을 확대시킵니다.

한때 영구 라이선스에 의존했던 전통적인 공급업체는 이제 단계적 마이그레이션 툴킷을 만들고 데이터 마이그레이션 유틸리티와 다운타임을 제한하는 이중 실행 옵션을 제공합니다. 클라우드에서 태어난 신흥 진출기업은 제로 풋 프린트의 도입, 소비 기반의 과금, 전임의 IT 서포트가 없는 팀에 적합한 제품 내 워크스루를 약속하는 것으로, 이 관성을 이용하고 있습니다. 그 결과, 클라우드 PSA의 채택은 레거시 툴을 구축할 뿐만 아니라, 신흥 경제권에서 처음으로 PSA를 구입하는 계기가 되어, 전문 서비스 자동화 시장의 밑단을 넓히게 됩니다.

2024년 매출은 솔루션 부문이 61.6%를 차지했지만, 서비스 부문은 13.7%의 연평균 복합 성장률(CAGR)로 확대되고 있으며, 프로세스 재구성, 데이터 정리 및 사용자 인에이블먼트를 필요로 하는 기업 전체의 롤아웃이 증가하고 있음을 반영합니다. 새로운 AI 모듈과 ERP 커넥터가 도입될 때마다 설정, 통합 및 거버넌스 프레임워크가 다운스트림에 필요하지만 고객은 이 레이어를 자체 관리하는 대역폭이 부족한 경우가 많습니다. 따라서 시스템 통합사업자는 로드맵 개발, 역할 기반 대시보드 설정, 단계적 컷오버 제작 등 프리미엄 컨설팅 수익을 얻고 있습니다.

도입의 성공은 행동변형에 달려 있기 때문에 체인지관리의 스페셜리스트는 커뮤니케이션, 롤플레이 세션, KPI 대시보드를 지휘해, 도입 후의 기세를 지속시킵니다. Thirdera와 같은 공급업체는 ServiceNow 고객을 위한 Workflow Data Fabric 가속기를 제공하여 빠르게 움직였습니다. 서비스의 호전은 평균 계약 금액을 증가시키고, 경상적인 확대 예약을 지원하고, 전문 서비스 자동화 시장에서 벤더와 고객의 장기적인 관계를 견고하게 만듭니다.

전문 서비스 자동화 시장은 배포 유형(클라우드 및 On-Premise), 구성 요소(솔루션 및 서비스), 기업 규모(대기업 및 중소기업), 최종 사용자 업계(IT 및 통신, BFSI 등), 기능 모듈(프로젝트 및 리소스 관리, 송장 및 송장 작성 등), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 2024년 전문 서비스 자동화 시장 규모의 38.06%를 차지했으며 성숙한 IT 컨설팅 생태계, 서벤스 옥슬리 법규, 초기 AI 파일럿 예산이 그 요인이 되고 있습니다. 본사에 가깝기 때문에 많은 공급업체는 피드백 루프 및 디자인 파트너와의 관계를 활용하여 기능 개발을 가속화하고 있습니다. 조기 도입 기업은 현재 부서별 파일럿에서 전사적 통합으로 진행되어 이용률 최적화, 고급 수익성 모델링, AI에 의한 제안서 작성에 주력하고 있습니다. 시장의 포화가 대수의 성장을 억제하고 있는 것, 애널리틱스, 모바일 경비, 인재 마켓플레이스에의 크로스셀이 수익의 성장을 지지하고 있습니다.

아시아태평양은 정부 보조금, 임금 상승 압력, 활기찬 SaaS 개발자 기반에 의해 지원되며 CAGR로 가장 빠른 14.5%로 성장을 지속하고 있습니다. 일본에서는 2024년에 전자계약에 관한 문의가 157% 급증하여 디지털화의 기세가 퍼지고 있음을 나타냅니다. 인도의 SaaS 기업은 2028년까지 세계 점유율 8%를 목표로 내걸고 있으며, PSA 기능의 구매자와 구축자 모두의 역할을 담당하고 있습니다. 싱가포르의 Productivity Solutions Grant와 호주 AI 생산성에 중점을 두어 이 지역의 파이프라인을 더욱 활성화시킵니다. 벤더는 세금, 컴플라이언스, 언어 팩을 현지화하여 이러한 다양한 미시적 시장을 통합하고 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정)에 대한 우려가 있는 것, 꾸준히 도입이 진행되고 있습니다. 많은 자문 프랙티스는 프라이빗 클라우드 또는 EU 소블린에서의 도입을 진행하고 있으며, 조달의 허들이 클리어 되면, 판매는 장기화하는 것, 거래 규모는 확대됩니다. Workday 영국의 5억 5,000만 파운드 투자에는 AWS 지역 리전과 견습 프로그램이 포함되어 데이터 거주 우려와 인력 부족을 완화하고 있습니다. ESG 보고서의 의무화는 탄소 임팩트와 다양성 메트릭스를 포착하는 PSA의 기능 강화의 기폭제가 되어, 전문 서비스 자동화 시장을 규제 준수의 인에이블러로서 자리매김하고 있습니다. 한편 중동 및 아프리카에서는 스마트시티 건설 및 인프라 정비 등 대규모 프로젝트 감독에 PSA가 도입되기 시작했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 중소기업에서 클라우드 PSA 도입

- 실시간 리소스와 마진의 가시성을 추진

- ERP/CRM 통합의 기세

- 성과 기반 서비스 모델로의 전환

- AI를 활용한 예측 인력 배치 분석

- 시장 성장 억제요인

- 멀티 테넌트 클라우드의 데이터 프라이버시 우려

- 레거시 스택과의 통합 복잡성

- PSA 스킬을 가진 구현 인재의 부족

- 벤더 통합과 락인 리스크

- 업계 밸류체인 분석

- 규제 상황

- 기술의 전망

- 업계의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 거시 경제 요인이 시장에 미치는 영향

제5장 시장 규모와 성장 예측(가치관)

- 전개 유형별

- 클라우드

- On-Premise

- 컴포넌트별

- 솔루션

- 서비스

- 기업 규모별

- 대기업

- 중소기업

- 최종 사용자 업계별

- IT 및 통신

- BFSI

- 아키텍처, 엔지니어링, 건설

- 헬스케어

- 법률 서비스

- 컨설팅 및 권고

- 기타 최종 사용자 산업

- 기능 모듈별

- 프로젝트 및 리소스 관리

- 청구와 청구서 발행

- 시간과 경비의 추적

- 비즈니스 분석 및 보고서

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 싱가포르

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Autotask Corporation(Datto)

- Kantata (Mavenlink + Kimble Apps)

- Clarizen Inc.

- Deltek Inc.

- Certinia(FinancialForce.com, Inc.)

- Infor Inc.

- Oracle NetSuite OpenAir

- Upland Software(Tenrox)

- Projector PSA Inc.

- Replicon Inc.

- Unanet Technologies

- Adobe Workfront

- ConnectWise PSA

- BigTime Software

- Planview(Changepoint)

- Avaza Ltd.

- Accelo Ltd.

- Wrike(Citrix)

- Hub Planner

- BQE Software(BQE CORE)

- Smartsheet(Resource Mgt)

- ServiceNow PSA

- Unit4 PSA

- Kimble(legacy)

- Workday PSA

- SAP Professional Services Cloud

제7장 시장 기회와 미래 동향

- 화이트 스페이스와 미충족 요구의 평가

The Professional Services Automation Market size is estimated at USD 15.22 billion in 2025, and is expected to reach USD 26.03 billion by 2030, at a CAGR of 11.32% during the forecast period (2025-2030).

Cloud-first transformation, AI-driven workflow orchestration, and the need for unified project-to-cash visibility anchor this expansion. Firms race to embed predictive analytics that guide staffing, margin management, and client outcomes, while outcome-based billing models spur richer performance measurement capabilities. A 69.3% cloud deployment footprint in 2024 proves that scalable, subscription-based delivery now underpins most new implementations, and AI modules that surface utilization risks before month-end close accelerate decision cycles. As talent shortages persist, vendors differentiate through low-code configuration, embedded best-practice templates, and tight ERP/CRM connectors that de-risk complex rollouts. Competitive advantage hinges on platform breadth: suites that combine project management, resourcing, billing, and analytics in one workspace capture larger seat counts and drive expansion revenue.

Global Professional Services Automation Market Trends and Insights

Cloud PSA Adoption Among SMEs

Small and medium enterprises propel the most dynamic growth in the professional services automation market as public-sector digitization grants and easy SaaS onboarding dismantle historical infrastructure hurdles. Singapore's Productivity Solutions Grant reimburses up to 50% of subscription fees, letting micro-firms access capabilities once reserved for global consultancies. A referral flywheel forms as early wins showcase productivity boosts, and subscription pricing converts upfront CAPEX into manageable OPEX, giving vendors recurring cash flows that fund feature velocity. Jana Small Finance Bank cut turnaround time by 65-70% after deploying UiPath's automation suite. Such results validate the thesis that even a 10-seat firm can wield enterprise-grade orchestration, reshaping competitive parity across professional services segments.

Drive for Real-Time Resource and Margin Visibility

Macroeconomic volatility forces firms to expose utilization gaps and margin leaks in real time rather than at quarterly review. BeyondTrust lifted resource utilization 20% after adopting Certinia PSA, pairing granular skills matrices with live feedback loops. Dashboards that surface over-allocated engineers or under-funded milestones curb cost overruns before they erode profitability. As more project teams work across time zones, instantaneous variance alerts allow managers to re-sequence tasks without breaching delivery windows. Embedded AI simulators pressure-test resourcing scenarios, ensuring that rate-card discounts or scope changes do not dilute forecasted gross margin.

Data-Privacy Concerns in Multi-Tenant Clouds

GDPR imposes strict residency and consent rules that intensify scrutiny of shared-tenant architectures handling client records, project notes, and employee timesheets. Regulated advisory practices now negotiate data-processing addendums that stipulate encryption keys, regional failover, and audit-ready logging. While hyperscale clouds boast SOC 2 and ISO-27001 attestations, some clients still prefer single-tenant or EU sovereign zones, delaying pure-cloud migrations and marginally dampening professional services automation market adoption in the short term.

Other drivers and restraints analyzed in the detailed report include:

- ERP/CRM Integration Momentum

- AI-Driven Predictive Staffing Analytics

- Integration Complexity with Legacy Stacks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments represented 69.3% of the professional services automation market size in 2024 and are slated to grow at 13.2% CAGR to 2030, reflecting a decisive pivot from on-premise custom builds. Automatic patching, elastic compute, and subscription pricing align with distributed workforce realities and CFO mandates to shift CAPEX to OPEX. On-premise PSA persists in highly regulated niches that mandate behind-firewall data residency, but even there, hybrid adjacency-analytics or mobile time capture in the cloud-gains traction. Platform vendors deepen alliances with AWS and Microsoft to tap global availability zones and shared AI accelerators. These moves compress implementation cycles from quarters to weeks, broadening the total addressable professional services automation market.

Traditional vendors that once relied on perpetual licenses now craft phased migration toolkits, offering data migration utilities and dual-running options that limit downtime. Emerging entrants born in the cloud exploit this inertia by promising zero-footprint deployment, consumption-based billing, and in-product walk-throughs suited to teams without dedicated IT support. As a result, cloud PSA adoption not only displaces legacy tools but can also catalyze first-time PSA buyers in emerging economies, extending the professional services automation market footprint.

While Solutions retained 61.6% revenue in 2024, the Services segment is expanding at 13.7% CAGR, mirroring the rise in enterprise-wide rollouts that demand process re-engineering, data cleanup, and user enablement. Every new AI module or ERP connector creates a downstream need for configuration, integration, and governance frameworks, and customers often lack the bandwidth to manage this layer themselves. Systems integrators, therefore, carve premium consulting revenue, shaping roadmaps, configuring role-based dashboards, and staging phased cut-overs.

Because successful adoption hinges on behavior change, change-management specialists orchestrate communications, role-play sessions, and KPI dashboards that sustain momentum post go-live. Vendors such as Thirdera became early movers, delivering Workflow Data Fabric accelerators for ServiceNow customers. The services upturn bolsters average contract value and underpins recurring expansion bookings, solidifying long-term vendor-client relationships within the professional services automation market.

Professional Services Automation Market is Segmented by Deployment Type (Cloud and On-Premise), Component (Solutions and Services), Enterprise Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (IT and Telecom, BFSI, and More), Functionality Module (Project and Resource Management, Billing and Invoicing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 38.06% of the professional services automation market size in 2024, anchored by mature IT consulting ecosystems, Sarbanes-Oxley controls, and early AI pilot budgets. Headquarters proximity grants many vendors live feedback loops and design-partner engagements that accelerate feature rollouts. Early adopters now progress from departmental pilots to enterprise-wide consolidations, focusing on utilization optimization, advanced profitability modeling, and AI-assisted proposal generation. Although saturation tempers volume growth, cross-selling into analytics, mobile expense, and talent marketplaces sustains revenue lift.

Asia-Pacific is on track for the fastest 14.5% CAGR, backed by government grants, rising wage pressure, and a vibrant SaaS developer base. Japan saw a 157% spike in electronic contract inquiries in 2024, signaling widespread digitization momentum. India's SaaS firms target an 8% global share by 2028, translating into dual-role participation as both buyers and builders of PSA capabilities. Singapore's Productivity Solutions Grant and Australia's focus on AI productivity further energize the regional pipeline. Vendors localize tax, compliance, and language packs to capture these diverse micro-markets.

Europe offers steady uptake tempered by GDPR anxieties. Many advisory practices pursue private-cloud or EU-sovereign deployments, elongating sales but enlarging deal size once procurement hurdles clear. Workday's GBP 550 million UK investment includes local AWS regions and apprenticeship programs, easing data-residency fears and talent shortages. ESG reporting mandates also catalyze PSA enhancements that capture carbon impact and diversity metrics, positioning the professional services automation market as an enabler of regulatory compliance. Meanwhile, the Middle East and Africa begin to deploy PSA for megaproject oversight-think smart-city builds and infrastructure rollouts-though connectivity gaps and scarce admin talent slow mass adoption.

- Autotask Corporation (Datto)

- Kantata (Mavenlink + Kimble Apps)

- Clarizen Inc.

- Deltek Inc.

- Certinia (FinancialForce.com, Inc.)

- Infor Inc.

- Oracle NetSuite OpenAir

- Upland Software (Tenrox)

- Projector PSA Inc.

- Replicon Inc.

- Unanet Technologies

- Adobe Workfront

- ConnectWise PSA

- BigTime Software

- Planview (Changepoint)

- Avaza Ltd.

- Accelo Ltd.

- Wrike (Citrix)

- Hub Planner

- BQE Software (BQE CORE)

- Smartsheet (Resource Mgt)

- ServiceNow PSA

- Unit4 PSA

- Kimble (legacy)

- Workday PSA

- SAP Professional Services Cloud

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud PSA adoption among SMEs

- 4.2.2 Drive for real-time resource and margin visibility

- 4.2.3 ERP/CRM integration momentum

- 4.2.4 Shift to outcome-based service models

- 4.2.5 AI-driven predictive staffing analytics

- 4.3 Market Restraints

- 4.3.1 Data-privacy concerns in multi-tenant clouds

- 4.3.2 Integration complexity with legacy stacks

- 4.3.3 Scarcity of PSA-skilled implementation talent

- 4.3.4 Vendor consolidation and lock-in risk

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Deployment Type

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.2 By Component

- 5.2.1 Solutions

- 5.2.2 Services

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-user Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Architecture, Engineering, and Construction

- 5.4.4 Healthcare

- 5.4.5 Legal Services

- 5.4.6 Consulting and Advisory

- 5.4.7 Other End-user Industries

- 5.5 By Functionality Module

- 5.5.1 Project and Resource Management

- 5.5.2 Billing and Invoicing

- 5.5.3 Time and Expense Tracking

- 5.5.4 Business Analytics and Reporting

- 5.5.5 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Malaysia

- 5.6.4.6 Singapore

- 5.6.4.7 Australia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Egypt

- 5.6.5.2.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Autotask Corporation (Datto)

- 6.4.2 Kantata (Mavenlink + Kimble Apps)

- 6.4.3 Clarizen Inc.

- 6.4.4 Deltek Inc.

- 6.4.5 Certinia (FinancialForce.com, Inc.)

- 6.4.6 Infor Inc.

- 6.4.7 Oracle NetSuite OpenAir

- 6.4.8 Upland Software (Tenrox)

- 6.4.9 Projector PSA Inc.

- 6.4.10 Replicon Inc.

- 6.4.11 Unanet Technologies

- 6.4.12 Adobe Workfront

- 6.4.13 ConnectWise PSA

- 6.4.14 BigTime Software

- 6.4.15 Planview (Changepoint)

- 6.4.16 Avaza Ltd.

- 6.4.17 Accelo Ltd.

- 6.4.18 Wrike (Citrix)

- 6.4.19 Hub Planner

- 6.4.20 BQE Software (BQE CORE)

- 6.4.21 Smartsheet (Resource Mgt)

- 6.4.22 ServiceNow PSA

- 6.4.23 Unit4 PSA

- 6.4.24 Kimble (legacy)

- 6.4.25 Workday PSA

- 6.4.26 SAP Professional Services Cloud

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment