|

시장보고서

상품코드

1850974

앰비언트 조명 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Ambient Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

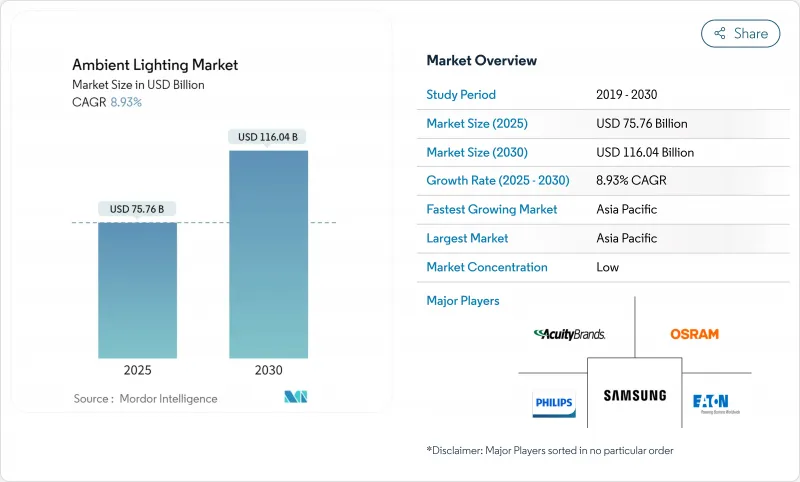

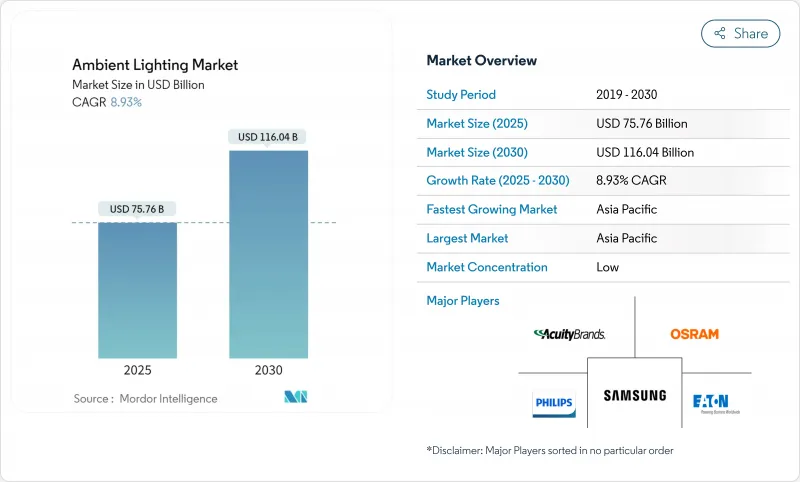

앰비언트 조명 시장은 2025년에 757억 6,000만 달러로 추정되고, 2030년에는 1,160억 4,000만 달러에 이를 전망이며, CAGR 8.93%로 성장할 것으로 예측됩니다.

성장은 세계적인 효율화의 의무화, LED의 급속한 보급, 조명을 보다 광범위한 스마트 빌딩 플랫폼과 연결시키는 커넥티드 시스템의 매력 확대에 지지되고 있습니다. LED 기반 제품은 이미 전반적인 조명 매출의 90%를 차지하고 있으며 밸류체인은 소프트웨어, 센서 및 서비스로 변화하고 있습니다. 아시아태평양은 세계 매출의 2분의 1 가까이를 차지하고 있으며, 도시화 계획이나 국가 자금에 의한 스마트 시티의 전개를 배경으로, 2자리수의 속도로 확대를 계속하고 있습니다. 제품 구성은 변화하고 있으며 램프와 조명기구가 여전히 주류이지만, 최종 사용자가 에너지 절약, 데이터, 생산성을 높이는 인간 중심의 기능을 요구하고 있기 때문에 제어기기가 전략적인 성장 엔진이 되고 있습니다.

세계의 앰비언트 조명 시장 동향 및 인사이트

EU와 호주에서 상업 시설 업그레이드를 가속화하는 LED 레트로핏 의무화

유럽연합(EU)의 에코디자인 지령(Ecodesign Directive)과 호주 국가건설기준(National Construction Code)과 같은 엄격한 정책 틀이 기존 램프의 단계적 폐지를 육박하고 있습니다. 현재는 투자 회수보다는 컴플라이언스가 전환점이 되고 있어 빌 소유자는 최저 효력의 임계치를 채우는 LED 기구를 채용하게 되어 있습니다. 상업용 분야만 봐도 업그레이드의 의무화 및 연결제어에 대한 수요가 높아짐에 따라 2024년 170억 7,000만 달러에서 2030년에는 273억 8,000만 달러로 급증할 것으로 예측됩니다. 공급업체는 다운타임과 인건비를 최소화하는 퀵 핏 램프, 드라이버리스 튜브 및 현장 프로그램 개조 키트를 지원합니다.

스마트 시티 투자가 아시아의 커넥티드 가로등 개보수 촉진

중국, 인도, 일본의 국가 스마트 시티 미션은 디지털 인프라의 핵심에 적응형 가로등을 설치하고 있습니다. 지자체는 기존의 고압 나트륨 기구를 5G 스몰셀, 대기질 센서, 교통 카메라를 호스팅할 수 있는 네트워크 LED로 대체하고 있습니다. Zigbee 및 BLE Mesh와 같은 무선 프로토콜은 새로운 케이블을 설치하지 않고도 확장성을 제공합니다. 개방형 API 노드를 제공하는 하드웨어 전문가는 도시가 조명을 보다 광범위한 IoT 서비스와 번들링하는 데 유리한 위치에 있습니다.

대규모 LED 스트립 도입에서 높은 돌입 전류 장애

멀티 스트링 스트립 시스템에서 수천 개의 드라이버가 동시에 전원을 켜면 유해한 전류 스파이크가 발생하여 차단기 트립이나 보증 클레임의 트리거가 발생할 수 있습니다. 소프트 스타트 전원 및 순차 컨트롤러는 위험을 줄이지만 비용은 증가합니다. 선형 조명이 수백 미터에 달하는 물류 허브에서는 신뢰성에 대한 우려로 인해 도입이 지연될 수 있습니다.

부문 분석

램프와 조명기구는 형광등과 할로겐에서 LED로의 대량 전환 덕분에 2024년에는 71%를 유지했으며, 계속 수익이 요구되고 있습니다. ENERGY STAR 규격의 조명기구는 백열등의 대체품보다 소비 전력이 90% 적고, 수명이 15배 길어 유지보수 예산과 카본 실적이 절감됩니다. 사무실, 가정 및 창고에서의 교환 활동은 단가가 하락하더라도 수요를 안정시키고 있습니다.

조명 제어는 시장의 가속 요인이며 연률 9.4%의 성장이 예측됩니다. 개방형 DALI 게이트웨이, 블루투스 LE 네트워크, 클라우드 대시보드는 에너지 관리에만 국한되지 않는 데이터 인사이트를 포함합니다. Signify의 보고서에 따르면 2024년에는 커넥티드 시스템과 서비스가 기업 매출의 30%를 차지하게 되어 소프트웨어 중심 제안에 대한 고객의 의욕이 높아지고 있음을 확인했습니다. 커넥티드 컨트롤의 앰비언트 조명 시장 규모는 건축 기준법이 거주자 센싱과 데이라이트 수확을 의무화함에 따라 확대됩니다.

개수 및 개축 프로젝트는 2024년 매출액의 63%를 창출했으며, 소유자가 낡은 집기의 엄청난 재고를 업그레이드했습니다. 미국 주택 리모델링 시장은 2022년에 6,000억 달러를 넘었으며, 지출의 34%가 조명을 포함한 에너지 관련 업그레이드로 흘렀습니다. 뉴욕지방법 97과 같은 시의 탄소 상한 규제가 긴급성을 높이고 있으며, 비효율 위반에는 2025년부터 벌금이 부과됩니다. 미국 일반 조달청의 지침은 LED 튜브, 복고풍 키트, 조명기구의 전면 교환이 승인된 경로로 꼽히고, 조명기구의 교환에 박차가 걸려 있습니다.

신축이 차지하는 비율은 작지만 CAGR 9.1%로 개수를 웃도는 것으로 보입니다. 건축가는 현재 WELL 및 LEED 크레딧을 획득하고 센서를 통합하며 시운전을 간소화하기 위해 설계 워크플로 초기에 조명을 프로그래밍하고 있습니다. 스마트 상업 캠퍼스는 네트워크 대응 기구를 기본 사양으로 하고, 복합 용도 타워, 데이터센터, 의료시설에 대한 앰비언트 조명 시장 침투를 촉진하고 있습니다. 신축 부동산에서의 앰비언트 조명 시장 규모의 확대는 하드웨어 및 소프트웨어의 번들 계약을 가능하게 하는 스케일 메리트에 의해서도 지원되고 있습니다.

지역 분석

아시아태평양은 2024년 매출의 46%를 차지했으며, 2030년까지 연평균 복합 성장률(CAGR) 12.8%로 성장할 전망입니다. 이는 효율적인 조명에 대한 국가 보조금, 광대한 주택 건설, LED 컴포넌트 생산의 세계 리더십이 원동력이 되고 있습니다. 중국은 제조 능력과 거대한 스마트 시티 조종사를 모두 이끌고 연결 가로등 수요를 지원합니다. 인도의 100개 도시 임무와 일본의 Society 5.0 비전은 제어, 센서, 플랫폼 통합을 위한 지역 파이프라인을 강화하고 있습니다.

북미는 성숙하지만 혁신 주도의 장소입니다. Signify의 2024년 데이터에 따르면 미국 매출은 22억 달러로 세계 매출의 약 3분의 1을 차지했습니다. 주택 리모델링은 계속 호조적이지만 COVID 후 사무실 다운 사이징으로 인해 일부 리노베이션 일정이 지연되었습니다. WELL과 LEED의 채택은 고급 장비 및 고급 제어를 정당화하는 인간 중심의 업그레이드 기세를 유지합니다.

유럽은 디자인 중심에서 규제가 많은 위치를 차지하고 있습니다. 에코디자인 지령은 상업 시설 전체의 LED화를 의무화하고 있으며, 이 지역은 시각적 쾌적성을 중시한 고연색 제품을 지지하고 있습니다. 독일과 프랑스의 자동차 제조업체는 앰비언트 패키지를 다운 레인지로 확장하여 부품 제조업체에게 비용 최적화된 RGB 모듈을 제공하도록 촉구하고 있습니다.

남미와 중동, 아프리카의 점유율은 작지만 건전한 성장을 이루고 있습니다. GCC의 접객시설 개조는 드라마틱한 분위기를 선호하며, 아프리카 인프라 계획은 스마트시티의 게이트웨이를 겸하는 효율적인 가로등에 공적 자금을 투입하고 있습니다. 앰비언트 조명 시장은 각국 정부가 그린 빌딩 기준을 적용하고 해외에서 직접 투자를 유치함으로써 장기적인 업사이드를 획득합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- LED 개수 의무화에 의해 EU 및 호주 상업 시설의 업그레이드 가속

- 아시아에서의 스마트 시티 투자가 커넥티드 가로등의 개수 추진

- 중급차용 OEM 주도형 앰비언트 패키지(아시아 및 유럽)

- WELL과 LEED v4 규격이 미국의 사무실에서 인간 중심 조명 추진

- 호스피탈리티 업계의 브랜드 재구축 사이클로 미적 분위기 예산 증가(만안 협력 회의 가맹국)

- 낮은 눈부심 조명기구를 필요로 하는 급속한 전자상거래 창고의 증축

- 시장 성장 억제요인

- 대규모 LED 스트립 전개에서 고돌입 전류 장해

- 단편화된 무선 프로토콜이 제어 시스템의 통합 비용 상승 초래

- COVID 후 사무실 축소 및 리노베이션 파이프라인 감소(북미 및 유럽)

- 희토류 원소 공급망 핍박에 의해 형광체 및 구동 장치 가격 상승

- 업계 생태계 분석

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제공별

- 램프 및 조명기구

- 백열 전구

- 할로겐 램프

- 형광등

- LED

- 조명 컨트롤

- 램프 및 조명기구

- 설치 단계별

- 신축

- 개수 및 개축

- 유형별

- 표면 실장 라이트

- 트랙라이트

- 스트립 라이트

- 매달린 빛

- 매립식 라이트

- 루멘 출력별

- 3,000 lm 미만(주택)

- 3,001-10,000 lm(상업)

- 10,000 lm 이상(산업 및 실외)

- 접속성별

- 유선(DALI, KNX)

- 무선(Zigbee, BLE Mesh, Thread)

- 최종 사용자별

- 주택

- 자동차

- 접객 및 소매

- 헬스케어

- 산업 및 물류

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 동남아시아

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Signify NV(Philips Lighting)

- Acuity Brands, Inc.

- ams OSRAM AG

- Hubbell Incorporated

- Eaton Corporation plc(Cooper Lighting)

- Cree Lighting(Savant Systems)

- Zumtobel Group

- GE Lighting, a Savant company

- Panasonic Life Solutions

- Wipro Lighting

- Samsung Electronics(LED Division)

- LG Innotek

- Bridgelux, Inc.

- Helvar Oy

- Dialight plc

- Fagerhult Group

- Legrand SA

- Lutron Electronics

- SPI Lighting

- Amerlux, LLC

제7장 시장 기회 및 향후 전망

AJY 25.11.19The ambient lighting market stands at USD 75.76 billion in 2025 and is forecast to reach USD 116.04 billion by 2030, advancing at an 8.93% CAGR.

Growth is anchored in global efficiency mandates, rapid LED penetration, and the widening appeal of connected systems that link lighting with broader smart-building platforms. LED-based products already account for 90% of total lighting sales, reshaping value chains toward software, sensors, and services. Asia Pacific owns nearly one-half of worldwide revenue and continues to expand at double-digit speed on the back of urbanization programs and state-funded smart-city rollouts. Product mix is shifting: lamps and luminaires still dominate, yet controls are now the strategic growth engine as end users seek energy savings, data, and human-centric functions that raise productivity.

Global Ambient Lighting Market Trends and Insights

LED retrofit mandates accelerating commercial upgrades in EU and Australia

Stringent policy frameworks such as the European Union Ecodesign Directive and Australia's National Construction Code are forcing the phase-out of legacy lamps. Compliance rather than payback is now the tipping point, pushing building owners to adopt LED fixtures that satisfy minimum efficacy thresholds. The commercial segment alone is projected to jump from USD 17.07 billion in 2024 to USD 27.38 billion by 2030 as mandated upgrades converge with rising demand for connected controls. Suppliers are responding with quick-fit lamps, driverless tubes, and field-programmed retrofit kits that minimize downtime and labor costs.

Smart-city investments driving connected street-light retrofits in Asia

National smart-city missions across China, India, and Japan place adaptive street lighting at the core of digital infrastructure. Municipalities are replacing conventional high-pressure sodium fixtures with networked LEDs that can host 5G small cells, air-quality sensors, and traffic cameras. Wireless protocols such as Zigbee and BLE Mesh offer scalability without trenching new cables, a decisive factor in dense urban cores. Hardware specialists that deliver open-API nodes are well-positioned as cities bundle lighting with broader IoT services.

High inrush-current failures in large-scale LED strip deployments

Multi-string strip systems can draw damaging current spikes when thousands of drivers power up simultaneously, triggering breaker trips and warranty claims. Soft-start power supplies and sequential controllers mitigate risk but add cost. Reliability concerns may delay rollouts in logistics hubs where linear lighting often spans hundreds of meters.

Other drivers and restraints analyzed in the detailed report include:

- OEM-triggered ambient packages in mid-segment autos

- WELL and LEED v4 standards pushing human-centric lighting in US offices

- Fragmented wireless protocols elevating control-system integration cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lamps and luminaires remain the revenue cornerstone, holding 71% in 2024 thanks to the mass conversion from fluorescent and halogen to LED. ENERGY STAR-rated fixtures consume 90% less power than incandescent alternatives and last 15 times longer, slashing maintenance budgets and carbon footprints. Replacement activity across offices, homes, and warehouses keeps demand stable even as unit prices fall.

Lighting controls are the market's accelerant, forecast to grow 9.4% annually. Open DALI gateways, Bluetooth LE networks, and cloud dashboards embed data insights that extend beyond energy management. Signify reports that connected systems and services delivered 30% of company sales in 2024, confirming rising customer appetite for software-centric propositions. The ambient lighting market size for connected controls is set to widen as building codes mandate occupancy sensing and daylight harvesting.

Retrofit and renovation projects generated 63% of 2024 revenue as owners upgraded vast stocks of outdated fixtures. The United States residential remodeling market surpassed USD 600 billion in 2022, with 34% of spend flowing into energy-related upgrades that include lighting. City carbon caps such as New York Local Law 97 amplify urgency, imposing fines starting in 2025 for inefficiency breaches. Guidance from the U.S. General Services Administration lists LED tubes, retrofit kits, or full luminaire swaps as approved pathways, fueling a deep replacement funnel.

New construction accounts for a smaller base but will outpace retrofits at 9.1% CAGR. Architects now program lighting early in design workflows to capture WELL and LEED credits, integrate sensors, and streamline commissioning. Smart commercial campuses specify network-ready fixtures as baseline, propelling ambient lighting market penetration in mixed-use towers, data centers, and healthcare facilities. Ambient lighting market size gains in new builds are also supported by economies of scale that allow bundled hardware-plus-software contracts.

The Ambient Lighting Market Report is Segmented by Offering (Lamps and Luminaires, and Lighting Controls), Installation Phase (New Construction, Retrofit and Renovation), Type (Surface-Mounted Light, Track Light, Sand More), Lumen Output (<=3 000 Lm (Residential), and More), Connectivity (Wired, and Wireless), End User (Residential, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific controls 46% of 2024 revenue and will grow at 12.8% CAGR through 2030, driven by state subsidies for efficient lighting, sprawling residential construction, and global leadership in LED component production. China spearheads both manufacturing prowess and giant smart-city pilots that anchor connected street-light demand. India's 100-city mission and Japan's Society 5.0 vision reinforce the regional pipeline for controls, sensors, and platform integration.

North America is a mature but innovation-led arena. Signify's 2024 data show that the United States contributed USD 2.20 billion, roughly one-third of its global sales. Residential remodels remain strong, yet office downsizing after COVID slows some retrofit schedules. WELL and LEED adoption maintains momentum for human-centric upgrades that justify premium fixtures and advanced controls.

Europe occupies a design-centric and regulation-heavy position. The Ecodesign Directive obliges LED transitions across commercial estates, and the region champions high color-rendering products that align with its emphasis on visual comfort. Automakers in Germany and France extend ambient packages downrange, spurring component suppliers to deliver cost-optimized RGB modules.

South America and the Middle East & Africa together contribute a smaller share but post healthy growth. GCC hospitality refurbishments prioritize dramatic ambience, while African infrastructure programs channel public funds into efficient street lighting that doubles as a smart-city gateway. The ambient lighting market gains long-term upside as governments apply green-building codes and attract foreign direct investment.

- Signify N.V. (Philips Lighting)

- Acuity Brands, Inc.

- ams OSRAM AG

- Hubbell Incorporated

- Eaton Corporation plc (Cooper Lighting)

- Cree Lighting (Savant Systems)

- Zumtobel Group

- GE Lighting, a Savant company

- Panasonic Life Solutions

- Wipro Lighting

- Samsung Electronics (LED Division)

- LG Innotek

- Bridgelux, Inc.

- Helvar Oy

- Dialight plc

- Fagerhult Group

- Legrand S.A.

- Lutron Electronics

- SPI Lighting

- Amerlux, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 LED Retrofit Mandates Accelerating Commercial Up-grades in EU and Australia

- 4.2.2 Smart-city Investments Driving Connected Street-light Retrofits in Asia

- 4.2.3 OEM-Triggered Ambient Packages in Mid-segment Autos (Asia and Europe)

- 4.2.4 WELL and LEED v4 Standards Pushing Human-Centric Lighting in United States Offices

- 4.2.5 Hospitality Re-brand Cycles Increasing Aesthetic Ambient Budgets (Gulf Cooperation Council Countries)

- 4.2.6 Rapid e-commerce Warehouse Build-outs Needing Low-glare Luminaires

- 4.3 Market Restraints

- 4.3.1 High Inrush-Current Failures in Large-scale LED Strip Deployments

- 4.3.2 Fragmented Wireless Protocols Elevating Control-System Integration Cost

- 4.3.3 Post-COVID Office Downsizing Reducing Retrofit Pipelines (NA and EU)

- 4.3.4 Tight Rare-earth Supply Chain Inflating Phosphor and Driver Prices

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Offering

- 5.1.1 Lamps and Luminaires

- 5.1.1.1 Incandescent Lamps

- 5.1.1.2 Halogen Lamps

- 5.1.1.3 Fluorescent Lamps

- 5.1.1.4 Light-Emitting Diode (LED)

- 5.1.2 Lighting Controls

- 5.1.1 Lamps and Luminaires

- 5.2 By Installation Phase

- 5.2.1 New Construction

- 5.2.2 Retrofit and Renovation

- 5.3 By Type

- 5.3.1 Surface-mounted Light

- 5.3.2 Track Light

- 5.3.3 Strip Light

- 5.3.4 Suspended Light

- 5.3.5 Recessed Light

- 5.4 By Lumen Output

- 5.4.1 Sub 3 000 lm (Residential)

- 5.4.2 3 001 - 10 000 lm (Commercial)

- 5.4.3 Above10 000 lm (Industrial and Outdoor)

- 5.5 By Connectivity

- 5.5.1 Wired (DALI, KNX)

- 5.5.2 Wireless (Zigbee, BLE Mesh, Thread)

- 5.6 By End User

- 5.6.1 Residential

- 5.6.2 Automotive

- 5.6.3 Hospitality and Retail

- 5.6.4 Healthcare

- 5.6.5 Industrial and Logistics

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Nordics

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 South Korea

- 5.7.3.4 India

- 5.7.3.5 South East Asia

- 5.7.3.6 Australia

- 5.7.3.7 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 United Arab Emirates

- 5.7.5.1.2 Saudi Arabia

- 5.7.5.1.3 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Signify N.V. (Philips Lighting)

- 6.4.2 Acuity Brands, Inc.

- 6.4.3 ams OSRAM AG

- 6.4.4 Hubbell Incorporated

- 6.4.5 Eaton Corporation plc (Cooper Lighting)

- 6.4.6 Cree Lighting (Savant Systems)

- 6.4.7 Zumtobel Group

- 6.4.8 GE Lighting, a Savant company

- 6.4.9 Panasonic Life Solutions

- 6.4.10 Wipro Lighting

- 6.4.11 Samsung Electronics (LED Division)

- 6.4.12 LG Innotek

- 6.4.13 Bridgelux, Inc.

- 6.4.14 Helvar Oy

- 6.4.15 Dialight plc

- 6.4.16 Fagerhult Group

- 6.4.17 Legrand S.A.

- 6.4.18 Lutron Electronics

- 6.4.19 SPI Lighting

- 6.4.20 Amerlux, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment