|

시장보고서

상품코드

1851028

소프트웨어 정의 광역 네트워크(SD-WAN) 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Software-Defined Wide Area Network - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

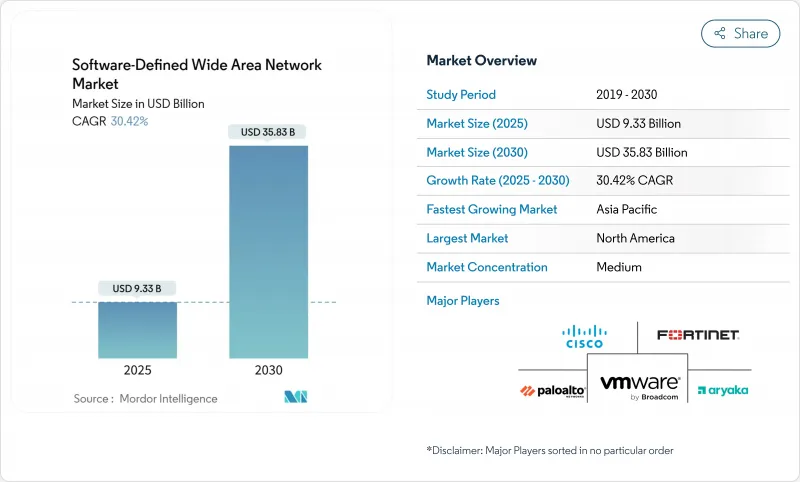

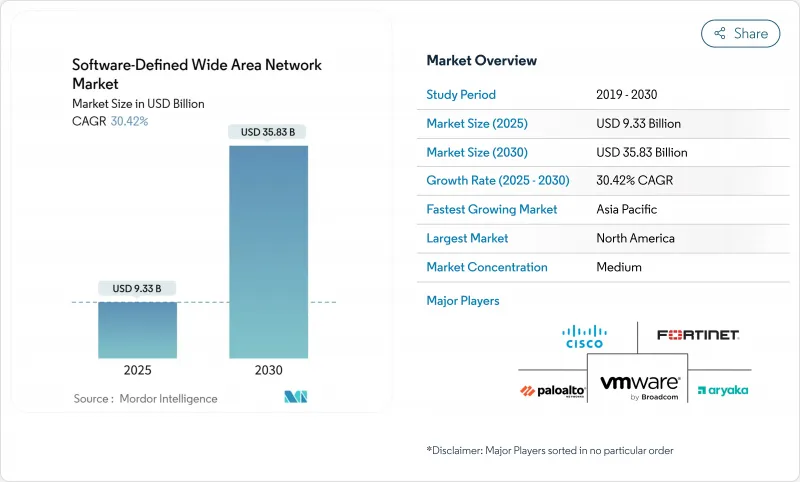

소프트웨어 정의 광역 네트워크(SD-WAN) 시장 규모는 2025년에 93억 3,000만 달러, 예측 기간(2025-2030년)의 CAGR은 30.42%를 나타내고, 2030년에는 358억 3,000만 달러에 이를 것으로 예측됩니다.

이 전망은 레거시 MPLS에서 분산 워크포스, AI 주도 워크로드, 5G 트래픽을 유지하는 클라우드 네이티브 아키텍처로의 결정적인 마이그레이션을 반영합니다. 엔터프라이즈 의사 결정자는 클라우드에 직접 연결, 통합된 보안 및 용도를 의식한 라우팅을 선호하며 공급업체가 자동화 및 머신러닝을 제품 전체에 통합하도록 촉구합니다. 클라우드 하이퍼스케일러와 통신 사업자의 파트너십은 대용량 액세스, 네트워크 슬라이싱, 관리 보안을 성과 기반 서비스 모델로 번들로 채택을 가속화하고 있습니다. 반면 인력 부족과 데이터 플레인 보안 우려가 단기적인 보급을 억제하고 있지만 기업이 대역폭 효율성과 운영 민첩성을 추구하고 있기 때문에 장기적인 궤도는 여전히 강세를 보이고 있습니다.

세계의 소프트웨어 정의 광역 네트워크(SD-WAN) 시장 동향과 통찰

클라우드 중심 용도 폭발

SaaS 및 클라우드 네이티브 워크로드로의 급속한 전환으로 기업은 분산 용도에 대한 지연 없는 액세스를 목표로 WAN 설계를 재구성합니다. Salesforce는 Prisma SD-WAN을 채택한 후 통신 비용을 올리지 않고도 사용 가능한 대역폭을 5배로 늘렸습니다. 기업은 현재 수천 개의 클라우드 서비스를 실시간으로 식별, 분류 및 우선 순위를 매기는 정책 엔진을 찾고 있으며, 상업 모델을 용량 기반에서 경험 수준 계약으로 전환하고 있습니다. 하이퍼스케일러도 이에 대응하고 있습니다. Google Cloud는 Lumen과 제휴하여 50,000개의 위치에 400Gbps의 광섬유를 제공하고 AI 워크로드를 위한 클라우드 WAN과 SD-WAN 오케스트레이션을 통합했습니다. 멀티클라우드에 걸친 컴퓨팅, 스토리지 및 광역 연결을 브리지하는 단일 공급업체의 스택이 구매자에게 지원되고 통합이 가속화되고 있습니다. 소프트웨어 정의 광역 네트워크(SD-WAN) 시장은 이러한 클라우드 전략과 네트워크 전략의 연계로부터 계속 혜택을 받습니다.

하이브리드/원격 근무 중심의 WAN 민첩성

영구적인 하이브리드 워크 모델은 기업 패브릭을 모든 엔드 포인트로 확장하는 탄력적 인 링크, 제로 터치 프로비저닝 및 통합 보안이 필요합니다. MPLS 프로비저닝은 많은 시장에서 여전히 40주 이상 걸리는 반면, SD-WAN은 광대역, 4G, 위성을 사용하여 액티브 액티브 경로 선택을 수행하므로 며칠 만에 브랜치를 시작할 수 있습니다. T-Mobile은 Palo Alto Networks와 협력하여 5G 고급 액세스와 클라우드 보안을 결합한 관리 SASE를 시작하여 기업에 탄력적인 대역폭과 본사에서 홈 오피스까지 일관된 정책을 제공합니다. 이러한 민첩성을 요구하는 수요로 인해 소프트웨어 정의 광역 네트워크(SD-WAN) 시장은 특히 거점 수가 불안정한 다국적 기업들 사이에서 가파른 채택 곡선을 유지하고 있습니다.

데이터 플레인 보안 및 제어 플레인 공격 표면

지점 사이트에서 인터넷에 직접 침입하면 위협 대상이 확대됩니다. IFIC 은행은 차세대 방화벽과 SD-WAN 에지를 결합하여 모니터링 비용을 40% 절감하고 엄격한 규제 당국의 감사에도 대응할 수 있게 되었습니다. 단일 구성 오류가 네트워크 전체에 전파될 수 있기 때문에 제어 플레인 침해는 여전히 심각한 위험입니다. 따라서 벤더는 오케스트레이션 채널 전체에서 제로 트러스트 자세 검사, 보안 하드웨어 모듈 및 상호 TLS를 통합합니다. 보안 딜리전스는 일부 롤아웃을 지연시키지만 소프트웨어 정의 광역 네트워크(SD-WAN) 시장에 대한 신뢰를 높이면 궁극적으로 채택을 촉진합니다.

부문 분석

클라우드 호스팅 오버레이는 2024년 소프트웨어 정의 광역 네트워크(SD-WAN) 시장 점유율의 48%를 차지했고 소프트웨어 정의 광역 네트워크(SD-WAN) 시장 규모의 45억 달러에 해당하며 2030년까지 33.2%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다. 기업은 자본 투자를 줄이고 IaaS 및 SaaS 환경에 마찰없는 링크를 제공하는 소비 기반 모델을 선호합니다. 프레미스 기반 플랫폼은 엄격한 규제 분야에서는 뿌리가 있지만 하드웨어 업데이트 사이클과 에코시스템의 규모가 작아 보급이 늦어지고 있습니다. 하이브리드 설계는 On-Premise 컨트롤러 인스턴스와 퍼블릭 클라우드를 융합시켜 데이터 레지던시를 충족하는 동시에 세계 POP를 활용하여 규모를 확장합니다.

벤더 경쟁은 클라우드 실적 밀도와 API 통합의 깊이로 점점 더 치열해지고 있습니다. 브로드콤이 VMware VeloCloud와 시만텍의 에지 노드를 통합하면 라인 속도로 보안 및 서비스 품질을 구현할 수 있는 분산형 클라우드 퍼스트 패브릭으로의 전환을 보여줍니다. 구매자는 클라우드 애플리케이션를 자동으로 감지하고 Terraform을 통해 정책을 조정하며 서비스 메시와 통합하는 솔루션을 찾고 있습니다. 이러한 기능을 통해 클라우드 배포는 소프트웨어 정의 광역 네트워크(SD-WAN) 시장의 주요 성장 엔진이 되었습니다.

2024년 소프트웨어 정의 광역 네트워크(SD-WAN) 시장 규모는 솔루션이 매출액의 65%를 차지하며 61억 달러에 해당합니다. 조기 어댑터는 개념 증명의 하드웨어 번들에서 풀 스케일 관리형 SD-WAN 시설로 전환하고 있습니다. 통합, 정책 설계 및 24 X 7 모니터링에는 많은 기업이 부족한 전문 기술이 필요합니다. 따라서 컨설팅과 수명주기 관리가 계약 총액에서 차지하는 비율이 증가하고 있습니다.

Zayo와 같은 공급자는 SSE의 리더인 Netskope와 제휴하여 보안 에지와 연결성을 단일 SLA로 제공합니다. 이러한 성장의 궤적은 장기적인 차별화가 독자적인 하드웨어보다 플랫폼 개방성과 서비스 혁신에 의존한다는 것을 시사하며, 소프트웨어 정의 광역 네트워크(SD-WAN) 시장에서의 하이브리드 가치 획득을 강화하고 있습니다.

소프트웨어 정의 광역 네트워크(SD-WAN) 시장 보고서는 배포 형태(구내, 클라우드, 하이브리드), 구성요소(솔루션 및 서비스), 조직 규모(대기업 및 중소기업), 최종 사용자 산업(건강, 은행, 금융서비스 및 보험(BFSI), 소매·소비자 서비스, 제조, 운송 및 물류, IT 및 통신 등), 지역별로 분류됩니다.

지역 분석

북미는 2024년 소프트웨어 정의 광역 네트워크(SD-WAN) 시장 규모의 55%를 차지했고 클라우드 도입의 진전, 벤처 기업의 활발한 자금 조달, 적극적인 사이버 규제를 반영하고 있습니다. Verizon에 의한 59억 달러의 MPLS 손상은 소프트웨어 중심의 오버레이가 레거시 전송의 경제성을 악화시키는 방법을 보여줍니다. 보안 인터넷 게이트웨이에 보조금을 내는 미국 연방 정부 프로그램은 수요를 더욱 자극하고 캐나다와 멕시코는 자동차와 소매의 다국적 기업에 의한 국경을 넘어 통합의 혜택을 받습니다. 이 지역은 현재 SASE 융합으로 전환되어 공급업체들이 모든 소프트웨어 정의 광역 네트워크 시장에 서비스형 방화벽 및 제로 트러스트 인증을 번들로 제공하도록 유도하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 32.6%로 가장 빠르게 확대되는 지역입니다. 적극적인 5G 배포를 통해 기업은 셀룰러와 광대역을 프로그래밍 가능한 오버레이로 결합하는 클린 시트 옵션을 얻을 수 있습니다. Singtel은 2024년 기업용 SD-WAN 에지 위에 소비자 등급의 5G 네트워크 슬라이싱을 확장하여 통신 사업자의 의욕이 이 지역의 보급을 촉진하고 있음을 강조하고 있습니다. 중국의 스마트 제조 클러스터, 인도의 IT 아웃소싱 허브 및 ASEAN의 초성장 디지털 경제가 융합되어 수십억 달러 규모 수요가 창출됩니다. 현지 시스템 통합사업자는 세계 OEM과 협력하여 규정 준수 및 언어 현지화를 통해 소프트웨어 정의 광역 네트워크(SD-WAN) 시장의 밑단을 확장합니다.

유럽은 단편적인 규정에도 불구하고 상당한 양을 공급하고 있습니다. 유럽위원회의 '디지털의 10년'은 2030년까지 2,000억 유로를 차세대 연결에 투입하는 것을 목표로 하고 있으며, SD-WAN은 국경을 넘은 데이터 흐름의 핵심 요소가 되고 있습니다. 기술 부족은 여전히 심각하며, 독일만으로도 2026년까지 78만 명의 ICT 전문가가 부족할 것으로 예측됩니다. Vodafone UK와 같은 운영자는 탄소 보고서와 안전한 에지 디자인을 융합시킨 권고 사례로 대응합니다. 그 결과, 유럽의 규제와 지속가능성에 대한 요구는 성숙한 공급업체의 강점을 발휘하고 소프트웨어 정의 광역 네트워크(SD-WAN) 시장의 꾸준한 성장을 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 클라우드 중심의 용도 폭발

- 하이브리드/리모트 워크 주도의 WAN 민첩성

- MPLS 코스트아웃과 대역폭 최적화

- AI에 의한 자기 복구 루트의 최적화

- 5G 네트워크 슬라이싱과 SD-WAN 컨버전스

- ESG 연계 탄소 인식 라우팅 수요

- 시장 성장 억제요인

- 데이터 플레인의 보안 및 제어 플레인 공격 표면

- SD-WAN 아키텍처의 인력 부족

- 독자 오버레이의 락 인 리스크

- CPE 공급망의 병목

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 전개 모드별

- 전제

- 클라우드

- 하이브리드

- 컴포넌트별

- 솔루션

- 서비스

- 조직 규모별

- 대기업

- 중소기업

- 최종 사용자 업계별

- 헬스케어

- BFSI

- 소매 및 소비자 서비스

- 제조업

- 운송 및 물류

- IT 및 텔레콤

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Cisco Systems

- Fortinet

- VMware(Broadcom)

- Aryaka Networks

- Versa Networks

- HPE Aruba

- Nokia(Nuage Networks)

- Huawei

- Tata Communications

- Ericsson

- Cato Networks

- Palo Alto Networks

- Silver Peak(HPE)

- Masergy(Comcast)

- Juniper Networks

- Citrix Systems

- Zscaler

- Riverbed Technology

- Check Point Software

- Barracuda Networks

- ATandT Business

- Telstra

제7장 시장 기회와 장래의 전망

SHW 25.11.11The Software-Defined Wide Area Network Market size is estimated at USD 9.33 billion in 2025, and is expected to reach USD 35.83 billion by 2030, at a CAGR of 30.42% during the forecast period (2025-2030).

This outlook reflects the decisive shift from legacy MPLS to cloud-native architectures that sustain distributed workforces, AI-driven workloads, and 5G traffic. Enterprise decision makers are prioritizing direct-to-cloud connectivity, integrated security, and application-aware routing, pushing vendors to embed automation and machine learning across offerings. Partnerships between cloud hyperscalers and telecom carriers accelerate adoption by bundling high-capacity access, network slicing, and managed security under outcome-based service models. Meanwhile, talent shortages and data-plane security concerns temper near-term rollouts, yet the long-run trajectory remains strong as enterprises pursue bandwidth efficiency and operational agility.

Global Software-Defined Wide Area Network Market Trends and Insights

Cloud-centric Application Explosion

Rapid migration to SaaS and cloud-native workloads reshapes WAN design as enterprises target latency-free access to distributed applications. Salesforce increased available bandwidth fivefold after adopting Prisma SD-WAN without raising telecom costs. Enterprises now demand policy engines that identify, classify, and prioritise thousands of cloud services in real time, shifting commercial models from capacity-based to experience-level agreements. Hyperscalers are responding: Google Cloud teamed with Lumen to deliver 400 Gbps fibre to 50,000 locations, embedding Cloud WAN and SD-WAN orchestration for AI workloads. Consolidation accelerates as buyers favour single-vendor stacks that bridge compute, storage, and wide-area connectivity across multi-cloud estates. The Software-Defined Wide Area Network market continues to benefit from this alignment of cloud and network strategies.

Hybrid/Remote-work-driven WAN Agility

Permanent hybrid work models require resilient links, zero-touch provisioning, and integrated security that extend corporate fabrics to any endpoint. MPLS provisioning still runs 40-plus weeks in many markets, whereas SD-WAN enables branch turn-ups in days using broadband, 4G, and satellite for active-active path selection. T-Mobile collaborated with Palo Alto Networks to launch a managed SASE offer that marries 5G Advanced access with cloud security, giving enterprises elastic bandwidth and consistent policy from headquarters to home offices. Demand for such agility keeps the Software-Defined Wide Area Network market on a steep adoption curve, especially among multinational corporations with volatile site counts.

Data-plane Security and Control-plane Attack Surface

Direct internet breakouts at branch sites enlarge the threat canvas. IFIC Bank mitigated exposure by combining next-generation firewalls with its SD-WAN edge, lowering monitoring costs by 40% while satisfying strict regulatory audits. Control-plane compromise remains a material risk because a single misconfiguration can propagate network-wide. Vendors are therefore integrating zero-trust posture checks, secure hardware modules, and mutual TLS across orchestration channels. Security diligence slows some rollouts, yet ultimately lifts adoption by increasing confidence in the Software-Defined Wide Area Network market.

Other drivers and restraints analyzed in the detailed report include:

- MPLS Cost-out and Bandwidth Optimisation

- AI-driven Self-healing Route Optimisation

- Shortage of SD-WAN Architecture Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-hosted overlays captured 48% of the Software-Defined Wide Area Network market share in 2024, equal to USD 4.5 billion of the Software-Defined Wide Area Network market size, and are set to expand at 33.2% CAGR to 2030. Enterprises favour consumption-based models that remove capex and provide frictionless links into IaaS and SaaS environments. Premise-based platforms persist in highly regulated sectors but face slower uptake due to hardware refresh cycles and smaller ecosystems. Hybrid designs blend controller instances on-premises with public cloud to satisfy data residency while leveraging global POPs for scale.

Vendor competition increasingly revolves around cloud footprint density and API integration depth. Broadcom's unification of VMware VeloCloud with Symantec edge nodes exemplifies the pivot to distributed, cloud-first fabrics capable of enforcing security and quality of service at line-rate. Buyers seek solutions that auto-discover cloud apps, adjust policies via Terraform, and integrate with service meshes. These capabilities keep cloud deployment the primary growth engine in the Software-Defined Wide Area Network market.

Solutions generated 65% of revenue in 2024, equating to USD 6.1 billion of Software-Defined Wide Area Network market size, while services posted the steeper 32.45% CAGR outlook. Early adopters have transitioned from proof-of-concept hardware bundles to full-scale managed SD-WAN estates. Integration, policy design, and 24 X 7 monitoring demand specialist skills that many enterprises lack. Consulting and lifecycle management, therefore, account for a rising share of total contract value.

Providers like Zayo partner with SSE leader Netskope to deliver secure edge plus connectivity as a single SLA, illustrating how services envelop technology to deliver outcomes. The growth trajectory signals that long-term differentiation will hinge on platform openness and service innovation more than on proprietary hardware, reinforcing hybrid value capture in the Software-Defined Wide Area Network market.

The Software-Defined Wide Area Network Market Report is Segmented by Deployment Mode (Premise, Cloud, Hybrid), Component (Solutions and Services), Organisation Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (Healthcare, BFSI, Retail and Consumer Services, Manufacturing, Transport and Logistics, IT and Telecom, and Others), and Geography.

Geography Analysis

North America accounted for 55% of the Software-Defined Wide Area Network market size in 2024, reflecting advanced cloud adoption, robust venture funding, and proactive cyber regulations. Verizon's USD 5.9 billion MPLS impairment illustrates how software-driven overlays cannibalise legacy transport economics. US federal programs that subsidise secure internet gateways further stimulate demand, while Canada and Mexico benefit from cross-border integrations by auto and retail multinationals. The region now pivots to SASE convergence, pushing vendors to bundle firewall-as-a-service and zero-trust authentication into every Software-Defined Wide Area Network market offer.

Asia Pacific represents the fastest expanding theatre, pacing at 32.6% CAGR to 2030. Aggressive 5G rollouts give enterprises clean-sheet options to bond cellular with broadband under programmable overlays. Singtel extended consumer-grade 5G network slicing on top of its enterprise SD-WAN edge in 2024, underscoring how carrier ambition propels regional uptake. China's smart-manufacturing clusters, India's IT outsourcing hubs, and ASEAN's hyper-growth digital economy converge to create multi-billion-dollar incremental demand. Local system integrators partner with global OEMs to tailor compliance and language localisation, broadening the Software-Defined Wide Area Network market footprint.

Europe delivers a sizeable volume despite fragmented regulations. The European Commission's Digital Decade aims to channel EUR 200 billion into next-gen connectivity by 2030, making SD-WAN a core element for cross-border data flow. Skills shortages remain acute; Germany alone expects a gap of 780,000 ICT professionals by 2026. Operators like Vodafone UK respond with advisory practices that fuse carbon reporting and secure edge design. Consequently, Europe's layered regulatory and sustainability demands play to the strengths of mature vendors, reinforcing steady growth in the Software-Defined Wide Area Network market.

- Cisco Systems

- Fortinet

- VMware (Broadcom)

- Aryaka Networks

- Versa Networks

- HPE Aruba

- Nokia (Nuage Networks)

- Huawei

- Tata Communications

- Ericsson

- Cato Networks

- Palo Alto Networks

- Silver Peak (HPE)

- Masergy (Comcast)

- Juniper Networks

- Citrix Systems

- Zscaler

- Riverbed Technology

- Check Point Software

- Barracuda Networks

- ATandT Business

- Telstra

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-centric application explosion

- 4.2.2 Hybrid/remote-work-driven WAN agility

- 4.2.3 MPLS cost-out and bandwidth optimization

- 4.2.4 AI-driven self-healing route optimisation

- 4.2.5 5G network slicing and SD-WAN convergence

- 4.2.6 ESG-linked carbon-aware routing demand

- 4.3 Market Restraints

- 4.3.1 Data-plane security and control-plane attack surface

- 4.3.2 Shortage of SD-WAN architecture talent

- 4.3.3 Proprietary overlay lock-in risks

- 4.3.4 CPE supply-chain bottlenecks

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Solutions

- 5.2.2 Services

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-user Industry

- 5.4.1 Healthcare

- 5.4.2 BFSI

- 5.4.3 Retail and Consumer Services

- 5.4.4 Manufacturing

- 5.4.5 Transport and Logistics

- 5.4.6 IT and Telecom

- 5.4.7 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems

- 6.4.2 Fortinet

- 6.4.3 VMware (Broadcom)

- 6.4.4 Aryaka Networks

- 6.4.5 Versa Networks

- 6.4.6 HPE Aruba

- 6.4.7 Nokia (Nuage Networks)

- 6.4.8 Huawei

- 6.4.9 Tata Communications

- 6.4.10 Ericsson

- 6.4.11 Cato Networks

- 6.4.12 Palo Alto Networks

- 6.4.13 Silver Peak (HPE)

- 6.4.14 Masergy (Comcast)

- 6.4.15 Juniper Networks

- 6.4.16 Citrix Systems

- 6.4.17 Zscaler

- 6.4.18 Riverbed Technology

- 6.4.19 Check Point Software

- 6.4.20 Barracuda Networks

- 6.4.21 ATandT Business

- 6.4.22 Telstra

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment