|

시장보고서

상품코드

1851030

매니지드 프린트 서비스 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Managed Print Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

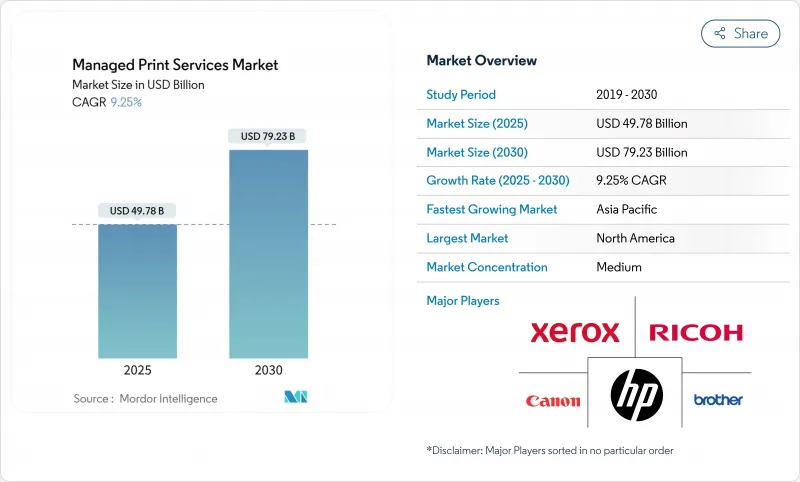

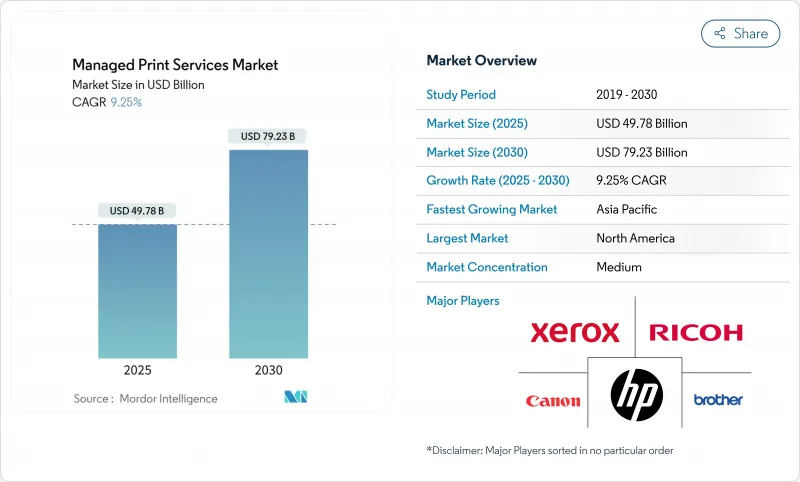

매니지드 프린트 서비스 시장 규모는 2025년에 497억 8,000만 달러, 2030년에는 792억 3,000만 달러에 이르고, CAGR 9.25%를 나타낼 것으로 추정되고 있습니다.

클라우드 연결, 하이브리드 워크 인프라 및 구독 가격은 대기업과 중소기업의 확장 기반에서 채택을 추진하고 있습니다. 보안이 높은 함대, 실시간 IoT 진단 및 자동화된 소모품 보충은 총 소유 비용을 낮추고 예기치 않은 다운타임을 줄이는 데 결정적인 효과를 발휘합니다. 수요는 또한 양면 인쇄 사용량, 이산화탄소 배출량 감소, 종이 폐기물 감소를 정량화할 수 있는 공급자가 보상하는 지속가능성 의무화를 반영합니다. 하드웨어 중심의 기존 기업은 분석, 워크플로우 자동화, 디바이스 아즈어 서비스를 융합시키고 AI 주도 최적화를 전문으로 하는 클라우드 네이티브 진출기업에 대항하여 점유율을 지키기 위해 경쟁 포지셔닝은 변화하고 있습니다. 지역적 기세는 아시아태평양에서 가장 두드러지며, 주요 제조업과 수출 지향 기업은 예지 보전을 업무 효율성의 테코로 간주하고 있습니다.

세계의 매니지드 프린트 서비스 시장 동향과 인사이트

원격 근무의 인쇄 인프라 최적화가 북미의 MPS 도입을 촉진

하이브리드 워크는 분산 인쇄가 비용과 보안의 위험이 되고 기업은 클라우드에 디바이스 관리를 집계할 필요가 있습니다. 기업은 보안 인쇄 릴리스, 사용자 인증, 암호화된 작업 라우팅을 채택하고 본사, 지사 및 집에서 인쇄하는 직원을 지원하면서 컴플라이언스를 유지합니다. Sharp의 Synappx Cloud Print는 이 요구사항을 대상으로 하며 작업 메타데이터만 보유하고 미국 기반의 금융기관 및 의료 시스템에서 선호하는 제로 트러스트 원칙을 강화하기 위해 설계되었습니다. 구독 가격은 사용량에 맞는 지출을 제공하며 서버 유지 관리가 필요 없으며 지속가능성 측정항목을 벤치마킹하는 대시보드를 제공합니다.

EU 기업의 MPS를 가속화하는 지속가능성과 탄소발자국의 의무화

EU의 기후 변화 정책에서 검증된 CO2 감축은 조달 기준이 되었습니다. 양면 인쇄 기본 설정, 자동 토너 재활용 및 용지 사용량 분석은 단면 인쇄 워크플로우와 비교하여 60% 배출량 감소를 입증했으며, 2030년까지 30-33%의 실적 감소를 요구하는 Corporate Climate Responsibility Monitor의 벤치마크를 충족합니다. 이를 통해 기업은 여러 년간 MPS 계약을 발급하여 감사 가능한 라이프사이클 분석과 저에너지 디바이스를 입증하는 공급자에게 Blue Angel 또는 EPEAT Gold 표준에 인증된 함대를 강조하고 있습니다.

북유럽의 디지털 변혁에 따른 사무실 인쇄량 감소

북유럽 기업은 전자 서명과 디지털 아카이브로 선도하여 직원 1인당 인쇄 매수를 2자리 줄이고 있습니다. 기존의 페이지당 비용 모델은 기준선의 볼륨이 줄어들면서 어려워지고 공급자는 워크플로의 디지털화 및 컨텐츠 관리로 범위를 넓힐 필요가 있습니다. 북유럽 교훈은 전자 송장 발행이 의무화되고 종이 폐지 목표가 확산됨에 따라 다른 성숙 경제국 수요를 예측합니다.

부문 분석

프린터/복사기 제조업체는 장치, 펌웨어 및 소모품을 통합 서비스 계약에 번들하여 2024년 매니지드 프린트 서비스 시장 점유율의 41%를 차지했습니다. HP는 인쇄 분야의 매출을 기록했습니다. HP는 2025년도 인쇄부문 매출액 42억 달러, 이익률 19.5%를 기록해 하드웨어를 중심으로 수익성을 입증했습니다. 시스템 통합사업자/리셀러는 CAGR 10.8%로 확대하여 멀티벤더의 중립성을 살려 규제 대상 고객을 위한 맞춤형 플릿 구축을 실시했습니다. 이 회사의 성장은 기기 브랜드보다 서비스의 충실성을 요구하는 고객의 의지를 보여줍니다. 독립 소프트웨어 공급업체는 워크플로우 병목 현상을 목표로 하여 다양한 하드웨어를 오버레이하는 분석 및 인쇄 보안 API를 통합하여 틈새 솔루션의 매니지드 프린트 서비스 시장을 확대하고 있습니다.

고객은 토너 단가를 판매하는 대신 가동 시간, 보안 규정 준수 및 환경 지표를 정량화할 수 있는 파트너에게 계약을 주문하는 경향이 커지고 있습니다. 제조업체는 통합자에게 장치의 원격 측정을 공개하고 분석을 공동 개발하며 채널 교육에 자금을 제공함으로써 이에 대응하고 있습니다. 반면, 리셀러는 HIPAA 규정 준수 템플릿과 같은 수직적인 전문성을 높여 OEM이 독점했던 전국 고객 명부에 들어갈 수 있습니다.

2024년의 매니지드 프린트 서비스 시장 규모의 65%는 On-Premise가 차지했으며, 그 중심은 거버넌스 정책에 의해 외부 데이터 전송이 제한되고 있는 금융 서비스, 방위, 유틸리티였습니다. 그러나 기업이 프린트 서버를 SaaS 플랫폼으로 마이그레이션하고 패치 적용, 대기열 관리 및 드라이버 인증 부하를 줄이기 때문에 매년 클라우드 배포가 11.2% 증가합니다. 선명한 Synappx 아키텍처는 원시 문서를 방화벽 뒤에 남겨 메타데이터만 보호합니다. 이는 클라우드의 확장성을 보장하면서 소블린 리스크를 줄이는 설계 패턴입니다. 공급업체는 현재 민감한 워크플로에 On-Premise 출력을 제공하고 표준 작업에 클라우드 스풀링을 오케스트레이션하는 하이브리드 제품을 패키징하고 있으며, 기업은 위험 관리를 유지하면서 퍼블릭 클라우드 배포를 용이하게 할 수 있습니다.

많은 기업들이 사내 인쇄 서버를 감사하는 것보다 빨리 SaaS 벤더가 SOC-2, ISO 27001, FedRAMP 인증을 획득한다고 생각하면 사이버 보험의 전제조건은 클라우드화를 더욱 가속화합니다. 초기 도입 기업은 지원 티켓을 30-40% 절감하여 IT 직원이 보다 가치 있는 이니셔티브에 전념할 수 있게 되었다고 보고되었습니다. 따라서 관리형 프린트 서비스 산업은 디바이스의 브레이크 픽스에서 지속적으로 업데이트되는 클라우드 분석에 의해 지원되는 지속적인 최적화로 축 발을 옮깁니다.

매니지드 프린트 서비스 시장은 채널 유형(프린터/복사기 제조업체, 시스템 인티그레이터/리셀러, 독립 소프트웨어 벤더(ISV)), 도입 형태(On-Premise, 클라우드 기반), 조직 규모(중소기업(SME), 대기업), 최종 사용자 가상(은행, 금융서비스 및 보험(BFSI), 헬스케어, IT 및 텔레콤, 기타), 지역별로 분류됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역 분석

북미는 성숙한 IT 에코시스템, 클라우드의 조기 도입, 엄격한 거버넌스 기준에 힘입어 매니지드 프린트 서비스 시장의 37%를 차지하고 선두를 차지하고 있습니다. 기업은 일상적으로 보안 인쇄 릴리스를 ID 및 액세스 관리 제품군과 통합하여 제로 트러스트 배포를 간소화합니다. 채널 에코시스템도 충실하고 OEM, 리셀러, ISV가 협력하여 문서 캡처부터 아카이브까지 엔드 투 엔드 자동화를 실현하고 있습니다. 미국의 포춘 500개 기업 중 상당수는 2030년까지 탄소 중립을 약속했으며 범위 3 감소를 위해 인쇄 플릿 최적화에 의존하고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있으며 2030년까지 연평균 복합 성장률(CAGR)은 12.1%를 나타낼 전망입니다. 중국 제조업체는 노동력 부족을 보완하고 24시간 365일 생산을 보장하기 위해 예지보전 분석을 조달하고 있습니다. 이는 2024년 인쇄그룹 매출이 2조 5,227억엔(168억 달러)에 달한 캐논이 잡은 기회입니다. 인도의 아웃소싱 기반은 서양 고객이 요구하는 ISO 27001 컴플라이언스 프레임워크에 안전한 풀 프린팅을 통합하는 경향을 강화하고 있습니다. 일본과 한국은 첨단 로봇 공학과 종이 워크플로우 유산의 균형을 유지하면서 클라우드 프린트 오케스트레이션을 디지털 혁신을 위한 브리지 기술로 만들고 있습니다. 동남아시아 중소기업은 자본 투자를 피하기 위해 구독 MPS를 채택하여 점진적이지만 급속한 볼륨 업에 기여하고 있습니다.

유럽은 디지털 성숙도가 높지만 지속가능성 정책에 역풍이 불고 있기 때문에 여전히 유리합니다. EU의 기업 지속가능성 보고 지침에 따라 기업은 라이프사이클에 미치는 영향을 문서화해야 하기 때문에 함대 감사 및 장비 통합이 확산되고 있습니다. 특히 북유럽 시장에서는 페이지 수가 줄어들고 있지만 워크플로우의 디지털화를 잔존 기기에 겹쳐 구매하고 있습니다. 독일, 영국, 프랑스는 BSI C5와 같은 고급 보안 인증을 필요로 하는 복잡한 멀티사이트 기업 및 공공 부문과의 계약을 통해 수요를 유지하고 있습니다. 공급자는 탄소 실적 대시보드와 인쇄 지표와 연동된 자동 탄소 오프셋 구매를 제공함으로써 차별화를 도모하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 북미의 MPS 도입을 견인하는 원격 워크·프린트 인프라의 최적화

- EU기업의 MPS를 가속시키는 지속가능성과 탄소 실적의 의무화

- 중소기업의 구독형 서비스 모델로의 이행이 시장을 견인

- 헬스케어 및 관공청에서의 프린트 기기 보안 및 컴플라이언스 요건 증가

- 아시아 대기업의 다운타임을 삭감하는 IoT 대응 플릿 분석이 시장을 견인

- 시장 성장 억제요인

- 북유럽의 디지털 변혁에 수반하는 오피스 인쇄 매수의 감소가 시장 억제

- 정부기관의 클라우드 기반 MPS를 막는 데이터 주권에 대한 우려

- 벤더의 락인 의식과 계약의 복잡성이 중소기업의 의욕 저하

- 남아시아의 신흥 시장에서 Capex-to-Opex 회계 이동의 저항

- 밸류체인 분석

- 규제 전망

- Porter's Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 시장에 주는 거시경제 동향의 평가

제5장 시장 규모와 성장 예측 수치

- 채널 유형별

- 프린터/복사기 제조업체

- 시스템 통합업체/재판매업체

- 독립 소프트웨어 벤더(ISVs)

- 배포 모드별

- On-Premise

- 클라우드 기반

- 조직 규모별

- 중소기업(SME)

- 대기업

- 최종 사용자 업계별

- BFSI

- 헬스케어

- IT 및 통신

- 정부

- 교육

- 기타 최종 사용자 업계별

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 북유럽 국가

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 중동

- GCC(사우디아라비아, UAE, 카타르)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Xerox Corporation

- Ricoh Company, Ltd.

- HP Inc.

- Canon Inc.

- Brother Industries, Ltd.

- Lexmark International, Inc.

- Konica Minolta, Inc.

- Samsung Electronics Co., Ltd.

- Kyocera Document Solutions Inc.

- Sharp Corporation

- Epson(세이코 Epson Corporation)

- Toshiba Tec Corporation

- FujiFilm Business Innovation Corp.

- Dell Technologies Inc.

- PrintFleet(ECI Software Solutions)

- PaperCut Software International

- Quadient SA

- Arc Document Solutions, Inc.

- EFI(Electronics For Imaging, Inc.)

- FlexPrint Managed Print Solutions

- OKI Electric Industry Co., Ltd.

- Pitney Bowes Inc.

- Wipro Ltd.

제7장 시장 기회와 향후 전망

KTH 25.11.11The managed print services market size is estimated at USD 49.78 billion in 2025 and is is forecast to reach USD 79.23 billion by 2030, expanding at a 9.25% CAGR.

Cloud connectivity, hybrid-work infrastructure, and subscription pricing are converging to lift adoption across large enterprises and an expanding base of small and medium businesses. Security-rich fleets, real-time IoT diagnostics, and automated consumables replenishment are proving decisive in lowering total cost of ownership and reducing unplanned downtime. Demand also reflects mounting sustainability mandates that reward providers able to quantify duplex usage, carbon savings, and paper-waste avoidance. Competitive positioning is shifting as hardware-centric incumbents blend analytics, workflow automation, and device-as-a-service bundles to defend share against cloud-native entrants specializing in AI-driven optimisation. Regional momentum is most pronounced in Asia-Pacific, where large manufacturers and export-oriented enterprises view predictive maintenance as an operational efficiency lever.

Global Managed Print Services Market Trends and Insights

Remote Work Print Infrastructure Optimisation Driving MPS Adoption in North America

Hybrid work has turned distributed print into a cost and security risk, prompting firms to consolidate device management in the cloud. Enterprises are adopting secure-print release, user authentication, and encrypted job routing to maintain compliance while supporting employees who print at headquarters, branch offices, or home. Sharp's Synappx Cloud Print targets this requirement, retaining job metadata only and reinforcing Zero Trust principles, a design favoured by US-based financial institutions and healthcare systems. Subscription pricing aligns spending to usage, eliminates server upkeep, and offers dashboards that benchmark sustainability metrics.

Sustainability and Carbon Footprint Mandates Accelerating EU Corporate MPS

EU climate policies now make verified CO2 reduction a procurement criterion. Duplex defaults, automated toner recycling, and paper-use analytics enable documented 60% emissions cuts relative to single-sided workflows, satisfying Corporate Climate Responsibility Monitor benchmarks that call for 30-33% footprint reductions by 2030. Corporates therefore award multi-year MPS contracts to providers demonstrating auditable lifecycle analytics and low-energy devices, putting a premium on fleets certified to Blue Angel or EPEAT Gold standards.

Declining Office Print Volumes Amid Digital Transformation in Nordics

Scandinavian corporations lead in e-signatures and digital archives, cutting per-employee print by double digits. Traditional cost-per-page models suffer as baseline volumes drop, prompting providers to broaden scopes to workflow digitisation and content management. Nordic lessons foreshadow demand in other mature economies as e-invoicing becomes compulsory and paper elimination targets spread.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Subscription-based Everything-as-a-Service Models Among SMEs

- Rising Print-Device Security and Compliance Requirements in Healthcare and Government

- Data Sovereignty Concerns Hindering Cloud-based MPS in Government Agencies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Printer/Copier Manufacturers owned a 41% stake of managed print services market share in 2024 by bundling devices, firmware, and consumables into integrated service agreements. Their captive install base, intellectual property, and direct field-service networks create switching costs that defend renewals. HP logged Printing segment revenue of USD 4.2 billion with a 19.5% margin in FY25, demonstrating hardware-anchored profitability. System Integrators/Resellers, expanding at 10.8% CAGR, capitalise on multi-vendor neutrality to architect bespoke fleets for regulated clients. Their growth signals customer appetite for service depth over device brand. Independent Software Vendors target workflow bottlenecks, embedding analytics and print-security APIs that overlay diverse hardware, thereby widening the managed print services market for niche solutions.

Customers increasingly award contracts to partners able to quantify uptime, security compliance, and environmental metrics rather than sell per-unit toner. Manufacturers answer by opening device telemetry to integrators, co-developing analytics, and funding channel training. Resellers, meanwhile, cultivate vertical specialisation-such as HIPAA compliance templates-that lets them penetrate national account rosters previously dominated by OEMs.

On-premise fleets still represent 65% of managed print services market size in 2024, anchored by financial services, defence, and utilities whose governance policies restrict external data transit. Yet cloud deployments will grow 11.2% annually as enterprises migrate print servers to SaaS platforms, offloading patching, queue management, and driver certification. Sharp's Synappx architecture secures metadata only, leaving raw documents behind the firewall, a design pattern that mitigates sovereignty risks while capturing cloud scalability. Providers now package hybrid offerings that orchestrate on-premise output for sensitive workflows and cloud spooling for standard jobs, enabling firms to ease into public-cloud adoption while maintaining risk controls.

Cyber insurance prerequisites further accelerate cloud, given that SaaS vendors certify against SOC-2, ISO 27001, and FedRAMP faster than many enterprises can audit internal print servers. Early movers report 30-40% support ticket reductions, freeing IT staff for higher-value initiatives. The managed print services industry therefore pivots from device break-fix toward continuous optimisation supported by always-updated cloud analytics.

Managed Print Services Market is Segmented by Channel Type (Printer/Copier Manufacturers, System Integrators/Resellers, Independent Software Vendors (ISVs)), Deployment Mode (On-Premise, Cloud-Based), Organization Size (Small and Medium Enterprises (SMEs), Large Enterprises), End-User Vertical (BFSI, Healthcare, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America heads the managed print services market with a 37% slice, underpinned by mature IT ecosystems, early cloud adoption, and stringent governance standards. Enterprises routinely integrate secure-print release with identity-and-access-management suites, streamlining Zero Trust rollouts. Channel ecosystems are deep, with OEMs, resellers, and ISVs collaborating to deliver end-to-end automation from document capture to archiving. The market also benefits from aggressive sustainability commitments by US Fortune 500 firms, many of which have pledged carbon neutrality by 2030 and rely on print fleet optimisation for scope-3 reductions.

Asia-Pacific is the fastest climber, logging a 12.1% CAGR to 2030. Chinese manufacturers procure predictive-maintenance analytics to offset labour shortages and ensure 24 X 7 production, an opportunity seized by Canon, whose Printing Group sales hit Yen 2,522.7 billion (USD 16.8 billion) in 2024. India's outsourcing hubs increasingly embed secure pull printing in ISO 27001 compliance frameworks demanded by Western clients. Japan and South Korea balance advanced robotics with paper-workflow legacies, making cloud print orchestration a bridge technology for digital transformation. Southeast Asian SMEs adopt subscription MPS to avoid capex, contributing incremental but rapid volumes.

Europe exhibits high digital maturity yet remains lucrative owing to sustainability policy headwinds. Companies must document lifecycle impacts under the EU Corporate Sustainability Reporting Directive, prompting widespread fleet audits and device consolidation. Nordic markets, in particular, show declining page volumes but buy workflow digitisation layered onto remaining devices. Germany, the United Kingdom, and France sustain demand through complex multi-site enterprises and public-sector contracts that require advanced security certifications such as BSI C5. Providers differentiate by offering carbon-footprint dashboards and automated carbon offset purchasing tied to print metrics.

- Xerox Corporation

- Ricoh Company, Ltd.

- HP Inc.

- Canon Inc.

- Brother Industries, Ltd.

- Lexmark International, Inc.

- Konica Minolta, Inc.

- Samsung Electronics Co., Ltd.

- Kyocera Document Solutions Inc.

- Sharp Corporation

- Epson (Seiko Epson Corporation)

- Toshiba Tec Corporation

- FujiFilm Business Innovation Corp.

- Dell Technologies Inc.

- PrintFleet (ECI Software Solutions)

- PaperCut Software International

- Quadient SA

- Arc Document Solutions, Inc.

- EFI (Electronics For Imaging, Inc.)

- FlexPrint Managed Print Solutions

- OKI Electric Industry Co., Ltd.

- Pitney Bowes Inc.

- Wipro Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Remote Work Print Infrastructure Optimization Driving MPS Adoption in North America

- 4.2.2 Sustainability and Carbon Footprint Mandates Accelerating EU Corporate MPS

- 4.2.3 Shift Toward Subscription-based Everything-as-a-Service Models Among SMEs Drives the Market

- 4.2.4 Rising Print-Device Security and Compliance Requirements in Healthcare and Government

- 4.2.5 IoT-Enabled Fleet Analytics Reducing Downtime in Large Asian Enterprises Drives the Market

- 4.3 Market Restraints

- 4.3.1 Declining Office Print Volumes Amid Digital Transformation in Nordics Hinders the Market

- 4.3.2 Data Sovereignty Concerns Hindering Cloud-based MPS in Government Agencies

- 4.3.3 Vendor Lock-in Perception and Contract Complexity Discouraging SMEs

- 4.3.4 Capex-to-Opex Accounting Shift Resistance in Emerging South Asian Markets Restraints the Market

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Channel Type

- 5.1.1 Printer/Copier Manufacturers

- 5.1.2 System Integrators/Resellers

- 5.1.3 Independent Software Vendors (ISVs)

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud-based

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-user Vertical

- 5.4.1 BFSI

- 5.4.2 Healthcare

- 5.4.3 IT and Telecom

- 5.4.4 Government

- 5.4.5 Education

- 5.4.6 Other End-user Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Nordics

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC (Saudi Arabia, UAE, Qatar)

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Xerox Corporation

- 6.4.2 Ricoh Company, Ltd.

- 6.4.3 HP Inc.

- 6.4.4 Canon Inc.

- 6.4.5 Brother Industries, Ltd.

- 6.4.6 Lexmark International, Inc.

- 6.4.7 Konica Minolta, Inc.

- 6.4.8 Samsung Electronics Co., Ltd.

- 6.4.9 Kyocera Document Solutions Inc.

- 6.4.10 Sharp Corporation

- 6.4.11 Epson (Seiko Epson Corporation)

- 6.4.12 Toshiba Tec Corporation

- 6.4.13 FujiFilm Business Innovation Corp.

- 6.4.14 Dell Technologies Inc.

- 6.4.15 PrintFleet (ECI Software Solutions)

- 6.4.16 PaperCut Software International

- 6.4.17 Quadient SA

- 6.4.18 Arc Document Solutions, Inc.

- 6.4.19 EFI (Electronics For Imaging, Inc.)

- 6.4.20 FlexPrint Managed Print Solutions

- 6.4.21 OKI Electric Industry Co., Ltd.

- 6.4.22 Pitney Bowes Inc.

- 6.4.23 Wipro Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment