|

시장보고서

상품코드

1851050

SOCaaS(Security Operation Center As A Service) 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Security Operation Center As A Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

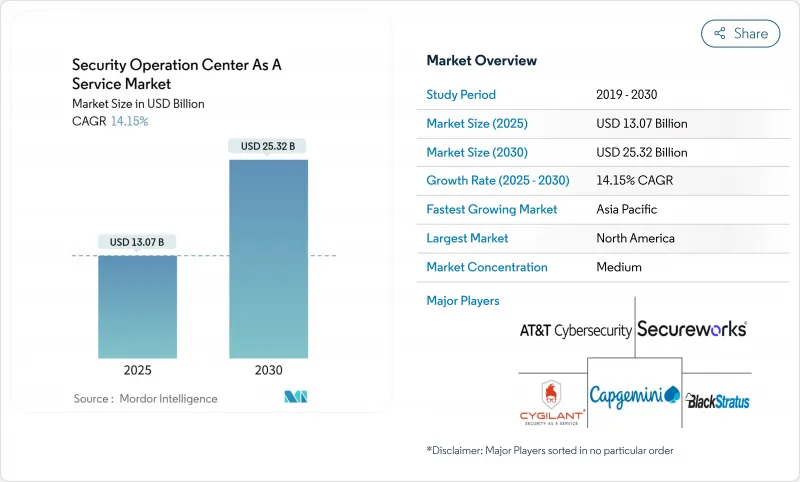

SOCaaS(SOC As A Service) 시장은 2025년에 130억 7,000만 달러에 이를 전망이며, 2030년에는 253억 2,000만 달러에 이르고, CAGR 14.15%로 확대될 것으로 예측됩니다.

급성장의 배경에는 리액티브한 방어로부터 AI 주도형 상시 탐지 및 대응으로의 시프트가 있습니다. 아웃소싱 모델은 격화하는 다중 벡터 공격과 심각한 인력 부족이라는 두 가지 중압을 해결하는 동시에 24시간 체제의 커버리지를 요구하는 엄격한 정보 공개 규칙에도 대응합니다. 대기업이 주요 구매자임에 틀림없지만 비용 효율적인 구독 기반 서비스를 통해 중소기업도 엔터프라이즈급 보호를 보장할 수 있습니다. 퍼블릭 클라우드 제공은 도입 속도가 빠르기 때문에 우위를 차지하고 있지만, 고객이 주권 요구사항과 유연성의 균형을 맞추기 원하므로 하이브리드 아키텍처가 인기를 끌고 있습니다. Sophos가 Secure Works를 인수함에 따라 주목된 통합은 로깅 관리, 고급 분석, 자율적 대응을 융합한 통합 플랫폼으로 업계가 전환하고 있음을 시사하고 있습니다.

세계의 SOCaaS(SOC As A Service) 시장의 동향과 인사이트

다중 벡터 사이버 공격의 급격한 증가

현재 공격은 클라우드 워크로드, 산업 제어, 직원 엔드포인트에 이르고 있으며, 기업은 매일 수십억 개의 이벤트를 상관시켜야 합니다. 운영 기술의 보안 침해는 전년 대비 73% 증가했으며, 다운타임이 발생하면 제조업체는 하루에 100만 달러의 손실을 입을 수 있습니다. Ransomware-as-a-Service 플랫폼은 적대자의 장벽을 더욱 낮추기 때문에 구매자는 알 수 없는 패턴을 실시간으로 포착하는 AI를 탑재한 SOCaaS를 선택하게 되었습니다. 자율적인 조사는 인적 노력을 줄이고 통합된 위협의 원격 측정은 체류 시간을 단축합니다.

심각화하는 사이버 보안 인력 부족

유럽 기업의 32%가 중요한 보안 업무 중에서도 특히 아키텍처 및 엔지니어링 업무를 수행할 수 없습니다. 급여 상승으로 24시간 365일 체제의 인력 배치를 할 수 없는 기업도 적지 않습니다. 아웃소싱된 SOC가 공인 분석가를 제공하는 한편, Microsoft 보안 파일럿의 11개 AI 에이전트와 같은 자동화 도구를 통해 누락된 인력을 전략적 업무로 돌리고 있습니다.

데이터 주권과 로그 상주에 대한 우려

현재 100개가 넘는 사법 관할구가 국경을 넘어서는 로그 보존을 제한하고 있기 때문에 공급자는 지역 데이터 노드와 주권 클라우드 인스턴스를 개시해야 합니다. 이러한 추가 장비는 비용을 증가시키고 특히 독일 행정과 호주 건강 관리와 같은 세밀한 감사 규칙이 있는 분야에서는 온보딩을 지연시킬 수 있습니다.

부문 분석

대기업은 2024년 SOC 시장 규모의 62.3%를 차지하였습니다. 대기업은 사내 전문가를 아키텍처 업무로 전환하기 위해 아웃소싱된 SOC에 전적으로 의존하고 있습니다. 같은 시기에 중소기업이 CAGR 15.7%로 서비스를 채택한 것은 사용자 1인당 매월 64-250달러의 구독 가격이 드디어 중견기업의 예산에 적합해졌음을 나타냅니다. 중소기업에서는 사내에 사고 대응 전문가가 없기 때문에 맞춤형 플레이북을 채용하고 있습니다.

지속적인 분석가 부족으로 인해 외부 SOC 커버가 업무상 필요합니다. 중소기업은 또한 대규모 자본 투자 없이 ISO 27001 및 HIPAA 규정 준수를 용이하게 하는 번들 규제 도구가 필요합니다. 한편, 다국적 기업은 SOCaaS의 출력을 기존 SIEM 워크플로에 통합하여 근본 원인 분석을 가속화하고 있습니다. 두 기업 모두 비즈니스에 미치는 영향에 따라 위협 우선순위를 결정하는 클라우드 네이티브 대시보드로 혜택을 누리고 있지만, 사용자 정의의 수준에 따라 시장의 최상급 프리미엄 제품은 여전히 차별화되고 있습니다.

보안 모니터링 및 로그 관리는 2024년 매출의 34.5%를 차지했습니다. 관리형 탐지 및 대응은 현재 14.3%로 성장하고 있으며, 컴플라이언스 기록뿐만 아니라 프로액티브 헌팅을 제공하기 때문에 레거시 모니터링을 추월하는 위치에 있습니다. BlueVoyant 고객은 MDR에 도구를 통합하고 오탐지 및 침해 빈도를 줄여 210%의 ROI를 기록했습니다.

MDR 플랫폼은 사용자, 네트워크 및 클라우드의 원격 측정을 연관시키기 위해 머신러닝을 사용합니다. 통합된 사고 대응 튜닝은 해결까지의 평균 시간을 한 자리 분으로 단축하여 규제 부문에 중요한 판매 포인트가 됩니다. 또한 자동 탐지가 어려운 고급 영구적 위협에도 대응하는 위협 헌팅 구독을 제공합니다. 모의 연습과 퍼플 팀 테스트 등의 컨설팅 애드온은 성숙한 구매자를 위한 풀 스펙트럼 포트폴리오를 완성시킵니다.

SOCaaS(Security Operations Center As A Service) 시장은 기업 규모별(중소기업, 대기업), 서비스 유형별(MDR(관리형 탐지 및 대응), 인시던트 응답, 위협 헌팅 등), 배포 모델별(퍼블릭 클라우드, 프라이빗 클라우드 등), 최종 사용자 산업별(은행, 금융서비스 및 보험(BFSI), 제조업 등), 지역별 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 2024년 지출액의 26.5%를 차지하였습니다. 클라우드의 조기 도입, 감시 제어를 의무화하는 성숙한 사이버 보험 시장, 강력한 벤처 자금 조달을 통해 SOCaaS에 유리한 생태계를 구축하고 있습니다. 미국에서는 SEC 인시던트 공개 규칙과 같은 규정에 따라 중견기업조차도 24시간 365일 커버리지를 계약하게 되었습니다. 캐나다도 비슷한 경향이 있지만 공급자를 선택할 때 데이터 잔여 조항을 특히 강조합니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 15.2%로 성장을 이끌 것으로 예측됩니다. 이 지역의 퍼블릭 클라우드 매출은 2022년부터 2024년에 걸쳐 거의 두배로 증가하였으며 고객층이 넓어지고 있습니다. 일본과 인도의 각국 정부는 정보 유출 통지 일정을 조화시켜 플랫폼에 얽매이지 않는 SOC의 도입을 촉진하고 있습니다. 지역 SOCaaS 프레임워크를 채택한 아폴로 병원은 신흥 시장의 의료 제공업체가 현지 개인 정보 보호법을 준수하면서 업무를 안전하게 수행하는 방법을 보여줍니다.

유럽은 NIS2 지침 덕분에 여전히 전략적 시장이 되었습니다. 기간 서비스 사업자는 지속적인 모니터링, 위험 관리 및 신속한 통지를 증명해야 합니다. 2024년 평균 보안 예산은 1,500만 유로에 달했으며, 지역 SOC 사업자의 비즈니스 기회가 확대되고 있습니다. 엄격한 데이터 주권은 국내 시설 설치에 의욕적인 공급자에 대한 수요를 뒷받침하고 있습니다. 남미, 중동, 아프리카는 현재 소규모 거점을 유지하고 있지만, 디지털 결제, 전자 정부, 중요 인프라 프로젝트에 의해 사이버 리스크에 대한 노출이 높아지기 때문에 수요가 높아지고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 멀티 벡터 사이버 공격의 급격한 증가

- 심각화하는 사이버 보안 인력 부족

- 클라우드와 하이브리드 IT의 공격 대상 확대

- 인시던트의 실시간 공개를 요구하는 규제의 움직임

- 24시간 365일 MDR을 의무화하는 사이버보험

- 통합된 가시성이 요구되는 OT/IoT 컨버전스

- 시장 성장 억제요인

- 데이터 주권과 로그 거주에 관한 우려

- 레거시 툴과의 통합 복잡성

- 아웃소싱 SOC의 제한된 조직 고유 상황

- 높은 위양성률에 의한 주의 환기 피로

- 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 시장의 거시경제 요인 평가

제5장 시장 규모와 성장 예측

- 기업 규모별

- 중소기업

- 대기업

- 서비스 유형별

- 관리형 탐지 및 대응(MDR)

- 인시던트 응답과 위협 헌팅

- 보안 모니터링 및 로그 관리

- 기타

- 전개 모델별

- 퍼블릭 클라우드

- 프라이빗 클라우드

- 하이브리드 클라우드

- 최종 사용자 업계별

- BFSI

- IT 및 텔레콤

- 헬스케어 및 생명과학

- 제조업

- 정부 및 공공 부문

- 소매 및 전자상거래

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- SecureWorks

- IBM Security

- ATandT Cybersecurity

- Arctic Wolf Networks

- Trustwave(Singtel)

- Atos

- BAE Systems

- Capgemini

- Symantec(Broadcom)

- Thales

- Fujitsu

- NTT Security

- CenturyLink(Lumen)

- Alert Logic

- Cygilant

- BlackStratus

- Digital Guardian

- Rapid7

- Securonix

- FireEye(Trellix)

제7장 시장 기회와 미래 전망

CSM 25.11.20The Security Operations Center as a Service market is valued at USD 13.07 billion in 2025 and is forecast to reach USD 25.32 billion by 2030, expanding at a 14.15% CAGR.

Rapid growth springs from the shift away from reactive defenses toward always-on, AI-driven detection and response. Outsourced models solve the dual pressure of intensifying multi-vector attacks and an acute talent shortage while aligning with tougher disclosure rules that demand round-the-clock coverage. Large enterprises remain the principal buyers, yet cost-efficient, subscription-based services now open the door for smaller firms to secure enterprise-grade protection. Public cloud delivery dominates because it speeds deployment, although hybrid architectures are gaining traction as customers balance sovereignty requirements with flexibility. Consolidation, highlighted by Sophos acquiring Secureworks, points to an industry moving toward unified platforms that fuse log management, advanced analytics, and autonomous response.

Global Security Operation Center As A Service Market Trends and Insights

Exponential Rise in Multi-Vector Cyber-Attacks

Attacks now span cloud workloads, industrial controls, and employee endpoints, forcing enterprises to correlate billions of events daily. Operational technology breaches rose 73% year over year, and downtime can cost manufacturers USD 1 million per day.Ransomware-as-a-Service platforms further lower the barrier for adversaries, which pushes buyers toward AI-powered SOCaaS to catch unknown patterns in real time. Autonomous investigation cuts human effort, and unified threat telemetry reduces dwell time.

Escalating Cybersecurity-Talent Shortage

Thirty-two percent of European firms still cannot fill critical security roles, especially architecture and engineering positions. Salary inflation leaves many organizations unable to staff 24/7 coverage. Outsourced SOCs supply certified analysts, while automation tools such as Microsoft Security Copilot's 11 AI agents redirect scarce personnel toward strategy tasks.

Data-Sovereignty and Log-Residency Concerns

More than 100 jurisdictions now restrict cross-border log storage, forcing providers to stand up regional data nodes and sovereign cloud instances. These extra facilities raise costs and can delay onboarding, particularly in sectors with granular audit rules such as public administration in Germany or healthcare in Australia.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Cloud and Hybrid IT Attack Surface

- Regulatory Push for Real-Time Incident Disclosure

- Integration Complexity with Legacy Tooling

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Large enterprises represented 62.3% of the Security Operations Center as a Service market size in 2024. They rely on outsourced SOCs as force multipliers that free internal specialists for architecture work. The same period saw small and medium enterprises adopt services at a 15.7% CAGR, signalling that subscription pricing between USD 64 and USD 250 per user each month finally fits mid-market budgets. SMEs embrace curated playbooks because they lack in-house incident response expertise.

Continuous analyst shortages make external SOC coverage an operational necessity. Smaller businesses also value bundled regulatory tooling that eases ISO 27001 or HIPAA compliance without major capex. Meanwhile, multinational conglomerates integrate SOCaaS outputs into existing SIEM workflows to accelerate root-cause analysis. Both cohorts gain from cloud-native dashboards that prioritize threats by business impact, yet customization depth still differentiates premium offerings for the top end of the market.

Security Monitoring and Log Management commanded 34.5% of 2024 revenue. Managed Detection and Response is now growing at 14.3% and is positioned to overtake legacy monitoring because it supplies proactive hunting, not just compliance records. BlueVoyant clients recorded a 210% ROI after consolidating tools under MDR, which cut false positives and breach frequency.

MDR platforms use machine learning to correlate user, network, and cloud telemetry. Integrated incident response tuning trims mean time to resolution to single-digit minutes, a key selling point for regulated sectors. Complementary threat-hunting subscriptions address advanced persistent threats that elude automatic detection. Consulting add-ons such as tabletop exercises and purple-team testing round out full-spectrum portfolios for mature buyers.

Security Operations Center As A Service (SOCaaS) Market is Segmented by Enterprise Size (SMEs and Large Enterprises), Service Type (Managed Detection and Response (MDR), Incident Response and Threat Hunting, and More), Deployment Model (Public Cloud, Private Cloud, and More), End-User Industry (BFSI, Manufacturing, and More), by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 26.5% of 2024 spending. Early cloud adoption, mature cyber-insurance markets that mandate monitored controls, and strong venture funding create an ecosystem favorable to SOCaaS. United States regulations, including the SEC's incident disclosure rule, push even mid-cap firms to contract 24/7 coverage. Canada follows a similar path but places extra weight on data-residency clauses when selecting providers.

Asia-Pacific is projected to lead growth with a 15.2% CAGR through 2030. Public-cloud revenue in the region nearly doubled between 2022 and 2024, broadening the customer pool. Governments from Japan to India are harmonising breach-notification timelines, encouraging platform-agnostic SOC uptake. Apollo Hospital's adoption of a regional SOCaaS framework shows how emerging-market health providers secure operations while meeting local privacy laws.

Europe remains a strategic market thanks to the NIS2 Directive. Essential service operators must prove continuous monitoring, risk management, and rapid notification. Average security budgets reached EUR 15 million in 2024, reinforcing the opportunity for regional SOC players. Strict data sovereignty drives demand for providers willing to set up facilities in the country. South America, the Middle East, and Africa maintain smaller bases today, yet present rising demand as digital payments, e-government, and critical-infrastructure projects increase cyber-risk exposure.

List of Companies Covered in this Report:

- SecureWorks

- IBM Security

- ATandT Cybersecurity

- Arctic Wolf Networks

- Trustwave (Singtel)

- Atos

- BAE Systems

- Capgemini

- Symantec (Broadcom)

- Thales

- Fujitsu

- NTT Security

- CenturyLink (Lumen)

- Alert Logic

- Cygilant

- BlackStratus

- Digital Guardian

- Rapid7

- Securonix

- FireEye (Trellix)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Exponential rise in multi-vector cyber-attacks

- 4.2.2 Escalating cybersecurity-talent shortage

- 4.2.3 Expanding cloud and hybrid IT attack surface

- 4.2.4 Regulatory push for real-time incident disclosure

- 4.2.5 Cyber-insurance mandates for 24/7 MDR

- 4.2.6 OT/IoT convergence demanding unified visibility

- 4.3 Market Restraints

- 4.3.1 Data-sovereignty and log-residency concerns

- 4.3.2 Integration complexity with legacy tooling

- 4.3.3 Limited organization-specific context in outsourced SOC

- 4.3.4 Alert-fatigue from high false-positive rates

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Force Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Enterprise Size

- 5.1.1 Small and Medium Enterprises (SMEs)

- 5.1.2 Large Enterprises

- 5.2 By Service Type

- 5.2.1 Managed Detection and Response (MDR)

- 5.2.2 Incident Response and Threat Hunting

- 5.2.3 Security Monitoring and Log Management

- 5.2.4 Others

- 5.3 By Deployment Model

- 5.3.1 Public Cloud

- 5.3.2 Private Cloud

- 5.3.3 Hybrid Cloud

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 IT and Telecom

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Manufacturing

- 5.4.5 Government and Public Sector

- 5.4.6 Retail and E-commerce

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SecureWorks

- 6.4.2 IBM Security

- 6.4.3 ATandT Cybersecurity

- 6.4.4 Arctic Wolf Networks

- 6.4.5 Trustwave (Singtel)

- 6.4.6 Atos

- 6.4.7 BAE Systems

- 6.4.8 Capgemini

- 6.4.9 Symantec (Broadcom)

- 6.4.10 Thales

- 6.4.11 Fujitsu

- 6.4.12 NTT Security

- 6.4.13 CenturyLink (Lumen)

- 6.4.14 Alert Logic

- 6.4.15 Cygilant

- 6.4.16 BlackStratus

- 6.4.17 Digital Guardian

- 6.4.18 Rapid7

- 6.4.19 Securonix

- 6.4.20 FireEye (Trellix)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment