|

시장보고서

상품코드

1851058

공공안전 애널리틱스 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Public Safety Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

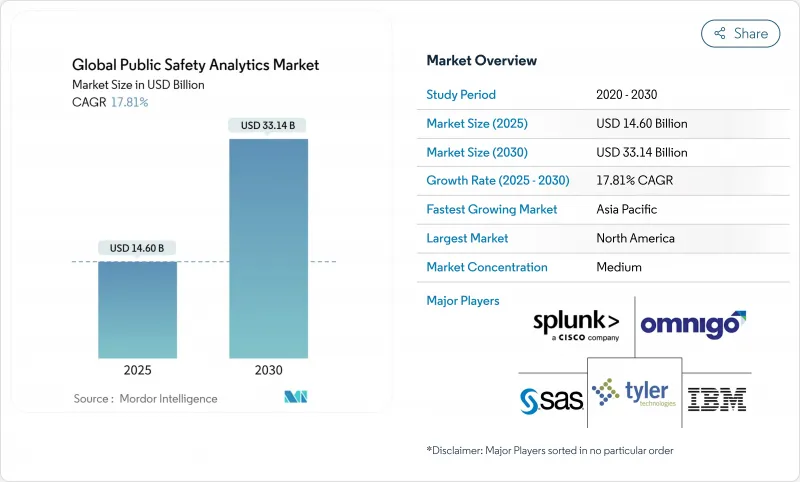

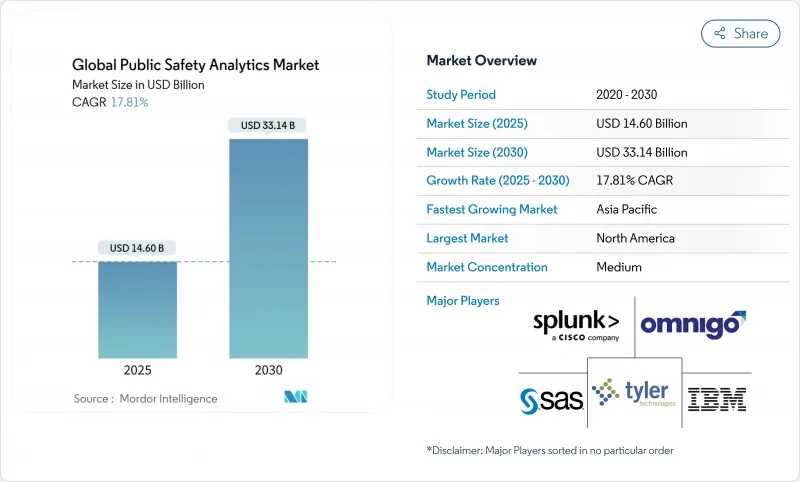

공공안전 애널리틱스 시장의 규모는 2025년에 146억 달러, 2030년에는 331억 4,000만 달러에 이르고, CAGR 17.81%를 나타낼 것으로 예측됩니다.

규제 당국의 모니터링 강화, 사이버 물리적 위협의 급증, 실시간 데이터 구동 의사 결정의 필요성으로 기술 도입이 가속화되고 있습니다. 북미 관계기관은 NG911의 전개를 위해 자본을 앞당기고 있으며 유럽의 이해관계자는 EU의 AI법 설명 가능성 조항을 충족하기 위해 플랫폼을 재설계하고 있습니다. 아시아의 5G 엣지 구축은 초저지연 비디오 분석을 실현하고 클라우드 마이그레이션은 자원에 제약이 있는 관할 구역의 액세스를 민주화하고 있습니다. 공급업체는 투명성 도구를 통합하고 구독 모델로 이동하고 개방형 API를 중심으로 생태계를 구축하여 컴플라이언스 압박을 벗어나 수익을 창출하고 있습니다.

세계의 공공안전 애널리틱스 시장의 동향과 인사이트

NG911 데이터 통합의 의무화(북미)

FCC의 점진적인 의무화로 인해 발신자 서비스 제공업체는 IP 기반 SIP를 통해 911 트래픽을 전달하고 공통 표준을 준수해야 하며, 통화 처리 및 애널리틱스 백엔드를 현대화하기 위해 각 기관을 지원하고 있습니다. 128억-169억 달러의 예산 견적으로 제안된 연방 정부의 자금 조달 메커니즘이 조달 파이프라인을 촉진하고 있습니다. NG911과 FirstNet을 결합하면 텍스트, 비디오 및 위치 정보 스트림이 상황 인텔리전스를 위해 융합되는 음성과 데이터의 융합 환경이 생겨 대응 가능한 공공안전 애널리틱스 시장이 확대됩니다.

알고리즘 투명성에 대한 EU AI법의 요구 사항

2024년 6월부터 이 법은 법 집행 인공지능을 고위험으로 분류하고 위험 로그, 바이어스 테스트 및 인적 모니터링을 의무화하고 있습니다. 공급업체는 설계 단계에서 설명 가능성 모듈과 바이어스 대시보드를 하드 코딩하고 컴플라이언스를 기능 차별화 플레이로 바꿉니다. 바이오메트릭 공급업체는 이미 공정성 임계값을 충족하기 위해 알고리즘을 재설계하고 있으며 공공안전 애널리틱스 시장의 유럽 부문 전체에서 업데이트 사이클을 가속화하고 있습니다.

알고리즘 바이어스 사건으로 인한 소송 위험(미국 및 EU)

시민 권익 단체는 인종 프로파일링을 강화할 것으로 예상되는 단속 도구에 대한 집단 소송을 요구하고 있으며, 지자체에 배치의 일시 정지나 축소를 촉구하고 있습니다. EU의 인공지능 법률은 감시와 함께 위험한 바이오메트릭 시스템을 허용하기 때문에 공급업체는 편견이 계속되면 법적 책임을 질 수 있습니다. 이러한 환경은 공공안전 애널리틱스 시장의 입찰량을 억제하고 판매 사이클을 장기화하고 있습니다.

부문 분석

소프트웨어는 2024년 매출의 60%를 차지하였으며 데이터 수집, 융합 및 시각화를 지원합니다. 녹화 관리 및 조사 도구와 같은 핵심 용도는 통화 로그, 비디오 스트림 및 센서 경고를 캡처하여 인텔리전스를 지원하는 데이터 세트를 생성합니다. AI 플러그인, 지리공간 대시보드 및 실시간 경고는 워크플로의 범위를 넓혀 상황 인식을 향상시킵니다. 기관이 911, CAD, RMS 피드를 통합함에 따라 API 중심 플랫폼에 대한 수요가 증가하고 있으며, 공공안전 애널리틱스 시장을 확대하고 있습니다.

전문 서비스는 19.0%의 연평균 복합 성장률(CAGR)로 상승하고 있습니다. 이는 공공기관이 데이터 사이언티스트 인력이 부족하여 통합, 교육, 알고리즘 튜닝을 외주해야 하기 때문입니다. 매니지드 서비스 번들은 특히 지방 및 자금이 부족한 부문의 경우 설비 투자 임계값을 낮추고 가치 실현까지의 시간을 단축합니다. CJIS 및 FedRAMP와 같은 클라우드 인증 프레임워크는 공급업체 선택의 위험을 줄이고 공공안전 애널리틱스 업계의 서비스 대응 기반을 확대합니다.

예측 엔진은 2024년 지출의 48%를 차지하였으며 핫스팟 예측, 경찰관 라우팅, 강도 패턴 분석을 가능하게 합니다. 범죄 예측 대시보드를 도입함으로써 시간 외 노동이 크게 줄어들고 사건 해결도 빨라졌다고 각 경찰서는 보고하고 있습니다. 그럼에도 불구하고, 격차의 영향에 관한 조사 결과를 둘러싸고 논쟁이 일어나고 있으며, 일부 의회는 시험적인 도입으로 돌아가고 있어, 공공안전 애널리틱스 시장에서의 효율성의 향상과 시민 권익 보호와의 미묘한 밸런스가 부각되고 있습니다.

CAGR 21.0%로 예측되는 처방 분석은 순찰 재배치부터 의료 파견 처치에 이르기까지 최적의 개입을 권장함으로써 예측을 구축합니다. 이 다음 전망은 성과 기반 단속 의무화와 과다 복용의 가치 기반 관리를 따릅니다. 독립적인 모델의 검증을 의무화하는 연방 정부 가이드라인은 전개가 둔화되지만, 궁극적으로 이 분야를 전문화하고 공공안전 애널리틱스 시장 전반공급업체의 신뢰성을 강화합니다.

지역 분석

북미는 2024년 매출의 39%를 차지했으며 FCC의 NG911 명령과 연방 정부의 클라우드 근대화 예산에 의해 뒷받침되었습니다. 일리노이와 같은 주는 이미 114개의 응답 지점을 지리공간 라우팅으로 전환하고, 성능 개선을 검증하고, 인접한 애널리틱스 조달을 자극하고 있습니다. 연방 정부의 오피오이드 위기 대책 보조금은 과다 복용 핫스팟 매핑에 애널리틱스를 할당하고 지역의 공공안전 애널리틱스 시장 점유율을 더욱 확대하고 있습니다.

아시아는 2025년부터 2030년의 CAGR이 19.2%로 전 지역을 웃돌 것으로 예상됩니다. 고밀도 도시와 국가 스마트 도시 프로그램은 통합 안전 플랫폼에 대한 수요를 지원합니다. 5G의 대규모 배포로 모바일 커맨드 포스트를 위한 엣지 애널리틱스가 실현되는 한편, 중국, 한국, 싱가포르에서는 소버린 AI에 대한 투자가 400억 달러를 넘어서고 있습니다. 이 기세는 UX를 지역화하고 다양한 프라이버시 규범을 준수할 수 있는 지역 공급업체에게 공공안전 애널리틱스 시장 규모를 밀어 올립니다.

유럽의 성장은 규정 준수에 따라 달라집니다. EU AI법의 투명성 조항은 제품 로드맵을 교체하고 바이어스 테스트 툴킷과 감사 대응 로그가 있는 공급업체를 지원합니다. 한편 영국 경찰은 연간 20억 파운드(25억 달러)를 지출하고 있으며 주로 레거시 IT를 새로 업데이트하고 있습니다. 디지털 유럽 프로그램에 근거한 범유럽 조성금은 국경을 넘은 상호 운용성의 파일럿 사업에 자금을 제공하고 있어 공공안전 애널리틱스 시장에 대한 장기적인 수요를 확고히 하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- NG9-1-1 데이터 통합 전개의 의무화

- EU의 AI법이 요구하는 알고리즘의 투명성

- 응급 구조대 비디오 스트림을 위한 5G 엣지 전개의 가속화

- 급속한 도시화가 스마트 시티 안전 플랫폼에 박차를 가함

- 분석 주도의 예방을 요구하는 연방 오피오이드 위기 대책 기금

- 위성 EO+GNSS 데이터가 재해 대책의 예산 항목으로 포함됨

- 시장 성장 억제요인

- 알고리즘 바이어스 사건에 의한 소송 리스크

- 현 레벨 이하의 단편화한 레거시 RMS/CAD 데이터의 사일로화

- 입찰 규칙에 관련되는 조달 사이클의 지연

- 데이터 사이언스에 정통한 인재의 에이전시 내에서의 희소성

- 가치/공급망 분석

- 규제 전망

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 컴포넌트별

- 소프트웨어

- 레코드 매니지먼트

- 조사관리

- 위치/지리공간 인텔리전스

- 범죄 인텔리전스

- 예측 및 처방 모듈

- 서비스

- 전문 서비스

- 매니지드/PSaaS

- 소프트웨어

- 분석 유형별

- 기술적 분석

- 진단 분석

- 예측 분석

- 처방적 분석

- 전개 모델별

- On-Premise

- 클라우드/SaaS

- 용도별

- 참고인 스크리닝

- 감시 및 비디오 분석

- 인시던트 검출 및 관리

- 패턴 인식과 핫스팟 매핑

- 자원 할당 최적화

- 최종 사용자별

- 법 집행

- 응급 의료와 EMS

- 소방 및 구조

- 수송과 중요 인프라

- 기타 정부 기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 호주

- 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 나이지리아

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- IBM Corporation

- Motorola Solutions Inc.

- Tyler Technologies Inc.

- Splunk Inc.

- Omnigo Software

- SAS Institute Inc.

- Hexagon AB

- NICE Ltd

- NEC Corporation

- Atos SE

- CentralSquare Technologies

- Verint Systems Inc.

- ESRI Inc.

- Genetec Inc.

- Microsoft Corp.

- Axon Enterprise

- IDEMIA

- Mark43 Inc.

- Genetec Inc.

- Palantir Technologies

- Hitachi Vantara

- Ericsson

제7장 시장 기회와 미래 전망

CSM 25.11.20The public safety analytics market size is valued at USD 14.60 billion in 2025 and is projected to reach USD 33.14 billion in 2030, advancing at a 17.81% CAGR.

Heightened regulatory scrutiny, soaring cyber-physical threats, and the imperative for real-time, data-driven decision-making are accelerating technology adoption. North American agencies are front-loading capital toward NG911 rollouts, while European stakeholders are redesigning platforms to satisfy the EU AI Act's explainability clauses. Asia's 5G edge build-out is unlocking ultra-low-latency video analytics, and cloud migration is democratising access for resource-constrained jurisdictions. Vendors are embedding transparency tooling, pivoting to subscription models, and orchestrating ecosystems around open APIs to convert compliance pressure into revenue upside.

Global Public Safety Analytics Market Trends and Insights

Mandated NG911 Data-Integration Rollouts (North America)

The FCC's phased mandate obliges originating service providers to deliver 911 traffic via IP-based SIP and comply with common standards, pushing agencies to modernise call-handling and analytics back-ends. Budget estimates of USD 12.8-16.9 billion and proposed federal funding mechanisms are catalysing procurement pipelines. Coupling NG911 with FirstNet is spawning a converged voice-data environment where text, video, and location streams are fused for situational intelligence, thereby expanding the addressable public safety analytics market.

EU AI Act Requirements for Algorithmic Transparency

Effective June 2024, the Act classifies law-enforcement AI as high-risk, mandating risk logs, bias testing, and human oversight. Suppliers are hard-coding explainability modules and bias dashboards at the design stage, transforming compliance into a feature-differentiation play. Biometrics vendors are already re-engineering algorithms to meet fairness thresholds, accelerating refresh cycles across the European segment of the public safety analytics market.

Litigation Risk from Algorithmic Bias Cases (US & EU)

Civil-rights groups are pressing class actions against predictive-policing tools that allegedly reinforce racial profiling, impelling municipalities to pause or scale back deployments. The EU AI Act's allowance for high-risk biometric systems, albeit with oversight, leaves vendors vulnerable to legal challenge if bias persists. This environment suppresses tender volumes and elongates sales cycles for the public safety analytics market.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating 5G Edge Deployments for First-Responder Video Streams

- Rapid Urbanisation Spurring Smart-City Safety Platforms

- Fragmented Legacy RMS/CAD Data Silos Below County Level

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software contributed 60% of 2024 revenue, underpinning data ingestion, fusion, and visualisation. Core applications such as record management and investigation tools ingest call logs, video streams, and sensor alerts to generate intelligence-ready datasets. AI plugins, geospatial dashboards, and real-time alerting broaden workflow coverage and elevate situational awareness. As agencies converge 911, CAD, and RMS feeds, demand for API-centric platforms is escalating, expanding the public safety analytics market.

Professional services are rising at 19.0% CAGR because agencies lack cleared data-science talent and must outsource integration, training, and algorithm tuning. Managed-service bundles lower CapEx thresholds and accelerate time-to-value, particularly for rural or cash-strapped departments. Cloud certification frameworks such as CJIS and FedRAMP de-risk vendor selection, thereby broadening the public safety analytics industry's services addressable base.

Predictive engines controlled 48% of 2024 spend, enabling hotspot forecasting, officer routing, and burglary pattern analysis. Departments report material overtime savings and faster case closures after deploying crime-forecast dashboards. Yet controversy over disparate-impact findings is sending some councils back to pilot mode, underscoring the delicate balance between efficiency gains and civil-liberties safeguards in the public safety analytics market.

Prescriptive analytics, projected at 21.0% CAGR, builds on prediction by recommending the best-fit intervention-ranging from patrol redeployment to medical dispatch triage. This next horizon aligns with outcome-based policing mandates and value-based care in overdoses. Federal guidelines requiring independent model validation will slow rollouts but ultimately professionalise the segment, reinforcing vendor credibility across the public safety analytics market.

The Public Safety Analytics Market is Segmented by Component (Software, Services), Analytics Type (Descriptive Analytics, Diagnostic Analytics, and More), Deployment Model (On-Premise, Cloud), Application (Person-Of-Interest Screening, Surveillance and Video Analytics, and More), End User (Law Enforcement, Emergency Medical and EMS, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America controlled 39% of 2024 revenue, propelled by the FCC's NG911 order and federal cloud modernisation budgets. States such as Illinois have already shifted 114 answering points to geospatial routing, validating performance improvements and stimulating adjacent analytics procurements. Federal opioid-crisis grants earmark analytics for overdose hotspot mapping, further enlarging the regional public safety analytics market share.

Asia is outpacing all regions with a 19.2% CAGR trajectory between 2025 and 2030. High-density urban corridors and national smart-city programmes anchor demand for integrated safety platforms. Massive 5G rollouts unlock edge analytics for mobile command posts, while sovereign AI investments exceed USD 40 billion across China, South Korea, and Singapore. This momentum elevates the public safety analytics market size for regional suppliers that can localise UX and comply with divergent privacy codes.

Europe's growth is dictated by regulatory compliance. The EU AI Act's transparency clauses are reshuffling product roadmaps, favouring vendors with bias-testing toolkits and audit-ready logs. Meanwhile, UK police forces spend GBP 2 billion (USD 2.5 billion) annually, predominantly refreshing legacy IT, signalling latent upside once transformation accelerates. Pan-European grants under the Digital Europe Programme fund cross-border interoperability pilots, cementing long-term demand for the public safety analytics market.

- IBM Corporation

- Motorola Solutions Inc.

- Tyler Technologies Inc.

- Splunk Inc.

- Omnigo Software

- SAS Institute Inc.

- Hexagon AB

- NICE Ltd

- NEC Corporation

- Atos SE

- CentralSquare Technologies

- Verint Systems Inc.

- ESRI Inc.

- Genetec Inc.

- Microsoft Corp.

- Axon Enterprise

- IDEMIA

- Mark43 Inc.

- Genetec Inc.

- Palantir Technologies

- Hitachi Vantara

- Ericsson

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandated NG 9-1-1 Data-Integration Rollouts

- 4.2.2 EU AI Act Requirements for Algorithmic Transparency

- 4.2.3 Accelerating 5G Edge Deployments for First-Responder Video Streams

- 4.2.4 Rapid Urbanisation Spurring Smart-City Safety Platforms

- 4.2.5 Federal Opioid-Crisis Funds Requiring Analytics-Led Prevention

- 4.2.6 Satellite EO + GNSS Data Becoming Budget-Line Items for Disaster Readiness

- 4.3 Market Restraints

- 4.3.1 Litigation Risk from Algorithmic Bias Cases

- 4.3.2 Fragmented Legacy RMS/CAD Data Silos Below County Level

- 4.3.3 Procurement-Cycle Delays Tied to Public-Tender Rules

- 4.3.4 Scarcity of Cleared Data-Science Talent Inside Agencies

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Record Management

- 5.1.1.2 Investigation Management

- 5.1.1.3 Location/Geo-Spatial Intelligence

- 5.1.1.4 Criminal and Crime Intelligence

- 5.1.1.5 Predictive and Prescriptive Modules

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed / PSaaS

- 5.1.1 Software

- 5.2 By Analytics Type

- 5.2.1 Descriptive Analytics

- 5.2.2 Diagnostic Analytics

- 5.2.3 Predictive Analytics

- 5.2.4 Prescriptive Analytics

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Cloud / SaaS

- 5.4 By Application

- 5.4.1 Person-of-Interest Screening

- 5.4.2 Surveillance and Video Analytics

- 5.4.3 Incident Detection and Management

- 5.4.4 Pattern Recognition and Hot-Spot Mapping

- 5.4.5 Resource-Allocation Optimisation

- 5.5 By End-User

- 5.5.1 Law Enforcement

- 5.5.2 Emergency Medical and EMS

- 5.5.3 Firefighting and Rescue

- 5.5.4 Transportation and Critical Infrastructure

- 5.5.5 Other Government Agencies

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Nordics

- 5.6.3.7 Rest of Europe

- 5.6.4 APAC

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Australia

- 5.6.4.7 New Zealand

- 5.6.4.8 Rest of APAC

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Motorola Solutions Inc.

- 6.4.3 Tyler Technologies Inc.

- 6.4.4 Splunk Inc.

- 6.4.5 Omnigo Software

- 6.4.6 SAS Institute Inc.

- 6.4.7 Hexagon AB

- 6.4.8 NICE Ltd

- 6.4.9 NEC Corporation

- 6.4.10 Atos SE

- 6.4.11 CentralSquare Technologies

- 6.4.12 Verint Systems Inc.

- 6.4.13 ESRI Inc.

- 6.4.14 Genetec Inc.

- 6.4.15 Microsoft Corp.

- 6.4.16 Axon Enterprise

- 6.4.17 IDEMIA

- 6.4.18 Mark43 Inc.

- 6.4.19 Genetec Inc.

- 6.4.20 Palantir Technologies

- 6.4.21 Hitachi Vantara

- 6.4.22 Ericsson

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment