|

시장보고서

상품코드

1851076

클라우드 무선 액세스 네트워크 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Cloud Radio Access Network - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

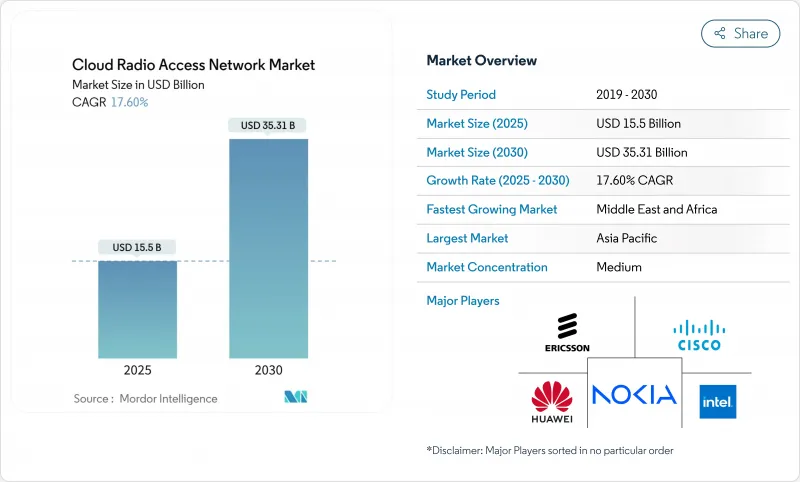

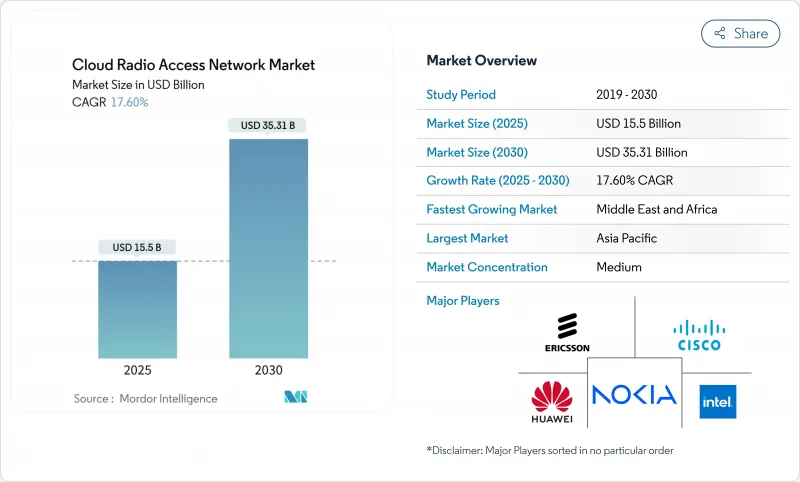

클라우드 무선 액세스 네트워크 시장 규모는 2025년에 155억 달러로 추정되고, 2030년에는 353억 1,000만 달러에 이를 것으로 추정 및 예측되며, 예측 기간(2025-2030년) CAGR 17.60%로 성장할 전망입니다.

5G의 급속한 전개, 베이스밴드 처리의 집중화 추진, 네트워크 운영 비용 절감에 대한 압력 증가로 수요가 높아지고 있습니다. 통신 사업자는 클라우드에 리소스를 풀링하여 셀 사이트의 처리량 및 주파수 활용을 향상시키는 밀집된 도시 클러스터에서 다중 계층 커버리지 전략을 수립하고 있습니다. 미국, 일본 및 유럽의 주요 도시에서의 상업적 실증은 AI 지원 스케줄링이 전체 액티브 무선 전력 소비를 줄이고 네트워크의 현대화와 동시에 지속가능성 목표를 지원할 수 있음을 보여줍니다. 기존 벤더가 소프트웨어 중심의 진출기업으로부터 점유율을 지키기 위해 경쟁이 격화되고 있으며, 무선, 컴퓨트, 실리콘의 전문 지식을 조합해 제품 로드맵을 가속시키는 제휴가 잇따르고 있습니다. 클라우드 라디오 액세스 네트워크 시장은 정책 지원을 통해 혜택을 받고 있으며 국가별로 크게 다른 주파수 대역의 릴리스 일정과 프론트 홀 병목 현상과 관련된 역풍에 직면하고 있습니다.

세계의 클라우드 무선 액세스 네트워크 시장 동향 및 인사이트

5G의 급속한 보급 및 고밀도화가 아키텍처 변화 촉진

세계의 통신 사업자는 미드밴드 5G 레이어를 라이트업하고 커버리지 갭을 채우기 위해 스몰셀을 추가합니다. 이러한 환경에서 클라우드 무선 액세스 네트워크 시장은 하드웨어를 중복하지 않고 수천 개의 무선을 관리하는 데 필요한 중앙 집중식 컴퓨팅 풀을 제공합니다. 도쿄, 서울, 뉴욕에서의 현장시험으로는 베이스밴드 워크로드를 동적으로 시프트시킴으로써 이용률을 30% 향상시키고, 셀의 피크 처리량을 25% 향상시킬 수 있었습니다. 상용 5G 독립형 코어는 현재 가상 베이스밴드 기능과 시간적 제약이 있는 스케줄링을 조정하고 있으며 클라우드 네이티브 원칙이 기능 릴리스 사이클을 단축하는 방법을 명확하게 보여줍니다. 중국과 미국의 대규모 전개는 동일한 클라우드 사이트에서 여러 무선 세대를 호스팅할 수 있음을 보여주고 주파수 대역 재조달 결정을 용이하게 하고 점진적인 전환 경로를 지원했습니다. 이러한 장점은 특히 실내 커버리지의 의무에서 고밀도 무선 그리드가 필요한 경우 지속적인 투자에 박차를 가합니다.

CAPEX 및 OPEX의 감소가 비즈니스 사례 지원

가상화 기저대역 풀의 경제적 매력은 즉시 발휘됩니다. 풀링은 하드웨어 중복을 줄이고 부동산 비용을 줄이며 업그레이드를 간소화합니다. 북미 벤더의 사례 연구에 따르면 3가지 레거시 베이스밴드를 단일 클라우드 클러스터에 통합한 사업자는 1년 롤아웃으로 CAPEX를 3분의 1 가까이 줄일 수 있었다고 합니다. 자동화 도구를 통해 예방 유지보수 및 원격 소프트웨어 업데이트의 규모가 확대되면 OPEX도 줄어듭니다. AI 스케줄러가 오프 피크 시에 가벼운 라디오를 딥 슬립 모드로 설정하면 네트워크의 전력 효율 프로파일이 개선되고 에너지 비용이 줄어듭니다. 이러한 절약은 적극적인 5G 확장 계획을 지원하는 것이며, 특히 통신 사업자에게는 배당 약정과 서비스 품질 향상의 필요성의 균형을 맞추는 데 중요합니다. 퍼블릭 클라우드의 소비 기반 가격 모델이 보급됨에 따라 통신 사업자는 트래픽의 피크에 맞추어 지출을 조정할 수 있는 유연성이 증가하고 클라우드 아키텍처의 매력이 높아지고 있습니다.

스펙트럼의 희소성 및 규제 제한으로 인한 기세 감소

미드밴드 주파수 대역의 적시 클리어런스 및 경매는 여전히 전국적인 5G 구축의 억제요인이 되고 있습니다. 미국 연방통신위원회의 경매 권한이 2024년에 만료됨에 따라 향후 출시에 대한 불확실성이 발생하여 일부 통신사업자의 투자 주기가 둔화되었습니다. 또한 많은 신흥 시장은 클라우드 RAN에 최적화된 5G 레이어의 턴키 전개를 지연시키는 불투명한 할당 프로세스와 정치 주도 할당 프로세스를 추진하고 있습니다. 라이선스가 정비되어 있어도, 가드 밴드 조건이나 전력 레벨의 상한에 의해 네트워크 레이아웃이 제한되는 일이 있어, 사업자는 무선 계획을 복잡하게 하는 단편적인 보유물에 의지할 수밖에 없습니다. 이러한 현실은 전개 속도를 완만하게 하고, 풀링의 경제성이 설득력을 갖게 되는 시점을 미끄러질 수 있습니다.

부문 분석

솔루션 시장 세분화 시장 규모는 2024년에는 113억 달러에 이르렀고, 부문 수익의 73%에 해당했습니다. 그러나 멀티벤더 환경이 주류가 됨에 따라 서비스 시장의 CAGR은 18.4%로 급속히 확대될 전망입니다. 초기 그린필드 전개에는 주로 하드웨어 및 가상화 베이스밴드 라이선스가 필요했지만, 현재의 브라운필드 업그레이드는 통합, 네트워크 최적화, 라이프사이클 지원을 요구하고 있습니다. 유럽의 통신 사업자는 AI 주도의 성능 분석과 DevOps의 실현을 번들로 한 다년간의 매니지드 서비스 계약을 체결해, 사내 팀이 새로운 서비스의 설계를 우선할 수 있도록 하고 있습니다. 컨설팅 팀은 현재 레거시 4G 트래픽과 새로운 사설 5G 이용 사례 간의 균형을 이루는 기존 캐리어에 중요한 역할을 하는 주파수 대역 리퍼밍, 기능 분할 선택 및 마이그레이션 순서 결정을 지도하고 있습니다. 하드웨어 제공업체는 개방형 인터페이스와 레퍼런스 자동화 워크플로우를 통합하여 제품과 전문 서비스 간의 경계를 모호하게 만듭니다. 2030년이 가까워짐에 따라 이러한 조합은 클라우드 무선 액세스 네트워크 시장의 수익 풀에서 차지하는 서비스의 비율을 높일 것입니다.

꾸준한 혁신의 흐름이 솔루션 사업의 활력을 유지하고 있습니다. 실리콘 메이저의 각 회사는 빔포밍 및 포워드 에러 보정을 위한 통합 가속을 도입하여 랙 유닛당 기저대역 용량을 2023년 블레이드에 비해 2배 이상으로 늘렸습니다. 무선 공급업체는 옥상 및 실내용으로 조정된 경량의 Massive MIMO 어레이를 통해 이러한 이점을 보완합니다. 이러한 진보는 총소유비용을 줄이는 동시에 대응가능한 고객 기반을 확대하고 솔루션측의 수익성장을 완만하면서도 일관되게 지원하고 있습니다. 결과적으로 소프트웨어, 실리콘 및 서비스는 중앙 집중식 오케스트레이션 무선 레이어로의 전환을 강화하고 시장 세분화의 기존 부문와 기업 부문의 채택을 확대하는 균형 잡힌 상황이 되었습니다.

2024년에는 통신 사업자가 미드밴드 주파수대 활용에 자본을 투하하기 때문에 5G층이 클라우드 무선 액세스 네트워크 시장 전체의 수익의 61%를 차지했습니다. 통신 사업자는 Industry 4.0 워크로드에 필수적인 슬라이싱과 초저지연 파이프라인을 가능하게 하는 독립형 아키텍처로 빠르게 전환했습니다. 가상화된 기저대역 풀은 일반 서버에서 비독립형 5G, LTE, NR을 실행할 수 있게 하며, 캐리어는 용량 업그레이드를 우선하여 3G를 단계적으로 폐지할 수 있습니다. 4G LTE는 여전히 의미있는 수익을 창출하고 있지만, 데이터 양이 많은 소비자의 사용이 보조금이 있는 장치를 사용하는 5G 번들에 끌려가면서 점유율은 해마다 감소하고 있습니다.

오픈 RAN은 공급망의 다양화에 열성적인 북미와 아시아의 티어온의 주목도 높은 헌신에 의해 뒷받침되며, 2030년까지 27%의 연평균 복합 성장률(CAGR)로 가장 빠른 궤도를 나타냅니다. 이 모델의 개방형 인터페이스는 블리드 최상의 조합을 촉진하지만 통합 오버 헤드는 여전히 큽니다. 그럼에도 불구하고 달라스와 서울에서 실행되는 네트워크의 테스트 결과는 통합 클라우드 플랫폼에서 오케스트레이션하면 멀티 벤더 Massive MIMO 스택이 모놀리식 시스템과 동등한 스펙트럼 효율을 달성할 수 있음을 보여줍니다. 미국 정부로부터의 보조금 프로그램 등의 규제 지원도 더욱 기세를 늘리고 있습니다. 이러한 힘을 종합하면 Open RAN은 주요 디스랩터로 자리매김하고 공급업체의 다양성을 넓히는 동시에 시장 전체의 경쟁력학을 격화시키고 있습니다.

지역 분석

아시아태평양은 2024년 매출 점유율 39%로 클라우드 무선 액세스 네트워크 시장을 독점하였고, CAGR 23.1%로 성장을 선도하고 있습니다. 중국, 일본, 한국의 적극적인 5G 전개는 대규모 지역 데이터센터에 연결된 고밀도 스몰셀 그리드에 의존합니다. 심천과 서울의 통신 사업자들은 이미 핵심 사업가에서 상용 개방형 인터페이스 클러스터를 운영하고 있으며, 축제 피크 시 비디오 스트리밍을 위한 실시간 주파수 풀링을 선보이고 있습니다. 정부는 가상화 투자에 대한 주파수 대역 요금 리베이트와 같은 지원 정책 프레임워크를 제공합니다. 벤더 에코시스템은 오픈 테스트 베드를 중심으로 발전하고 있으며, OREX 이니셔티브와 같은 합작투자는 수출 기회를 노리고 이 지역의 리더십을 확고히 하고 있습니다.

북미는 매출에서 2위를 차지했습니다. 미국의 통신 사업자는 2026년까지 레거시 하드웨어를 오픈 대응 무선으로 전환하기 위해 수십억 달러의 예산을 계상했습니다. CHIPS 및 과학법에 근거한 연방 보조금은 AI 기반 스케줄링 엔진을 강화하는 실리콘 연구에 공동 출자하여 국내 공급망에 높은 탄력성을 제공합니다. 라스베가스와 시애틀의 초기 도입은 GPU 가속을 사용하는 클라우드 노드가 XR 게임 및 산업 자동화를 위한 밀리초 수준의 엄격한 대기 시간 목표를 달성할 수 있음을 입증합니다. 캐나다 사업자가 핀란드나 한국의 벤더와 협력함으로써 지역의 혁신 영역이 확대되고, 보다 넓은 클라우드 무선 액세스 네트워크 시장을 지원하는 국경을 넘은 기술 교류가 강조되고 있습니다.

유럽에서는 규제 강화 및 경쟁의 필요성으로 인해 도입이 가속화되고 있습니다. 영국, 독일, 스페인의 통신 사업자는 무선, 베이스밴드, 관리 시스템 간의 상호 운용성을 입증하는 공공 테스트 실험실에 힘입어 최초의 상용 5G Open RAN 매크로 사이트를 전개했습니다. 유럽 연합(EU)은 5G 및 6G 네트워크의 연구 개발에 자금을 제공하고 있으며 RAN 소프트웨어의 인재 확보를 위한 산학 파이프라인을 강화하고 있습니다. 단독으로 5G 커버율이 늦었음에도 불구하고 기존 사업자는 총소유비용 절감 및 서비스 혁신의 가속화를 주된 동기로 무선 레이어의 클라우드화 계획을 급속도로 진행하고 있습니다. 현재 진행중인 인프라 프로그램은 지역 회랑을 통한 광섬유 백본을 업그레이드하여 역사적인 병목 현상을 제거하고 클라우드 무선 액세스 네트워크 시장 개발을 지역 전반에 걸쳐 더욱 확대합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 급속한 5G 전개 및 고밀도화

- 집중 베이스 밴드에 의한 CAPEX-OPEX의 절약

- 모바일 데이터의 지수 함수 성장

- 네트워크 가상화 및 SDN 수요

- AI에 의한 RAN 최적화의 채용

- 에너지 효율 규제가 클라우드 RAN 뒷받침

- 시장 성장 억제요인

- 주파수대의 희소성 및 규제의 한계

- 한정된 프론트 홀 파이버 및 지연의 과제

- 중앙 집중식 아키텍처의 보안 및 개인 정보 보호 위험

- 신흥 시장에서 불확실한 ROI

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 투자 분석

제5장 시장 규모 및 성장 예측

- 컴포넌트별

- 솔루션

- 서비스

- 전문

- 매니지드

- 네트워크 유형별

- 5G

- 4G

- LTE

- 3G(EDGE)

- 전개 모델별

- 집중형 RAN(C-RAN)

- 가상화 RAN(vRAN)

- 오픈 RAN(O-RAN)

- 하이브리드 클라우드 RAN

- 최종 사용자별

- 모바일 네트워크 사업자

- 기업

- 정부 및 공공안전

- 중립 호스트 및 타워 코스

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 튀르키예

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Huawei Technologies Co. Ltd.

- Nokia Corporation

- Telefonaktiebolaget LM Ericsson

- Cisco Systems Inc.

- Samsung Electronics Co. Ltd.

- ZTE Corporation

- Intel Corporation

- Fujitsu Limited

- NEC Corporation

- Mavenir Systems Inc.

- Parallel Wireless Inc.

- Rakuten Symphony

- Altiostar(Rakuten)

- CommScope Holding Co. Inc.

- Casa Systems Inc.

- Airspan Networks Inc.

- Hewlett Packard Enterprise(HPE)

제7장 시장 기회 및 향후 전망

AJY 25.11.12The Cloud Radio Access Network Market size is estimated at USD 15.5 billion in 2025, and is expected to reach USD 35.31 billion by 2030, at a CAGR of 17.60% during the forecast period (2025-2030).

Rapid 5G rollouts, the push for centralized baseband processing, and mounting pressure to trim network operating costs keep demand high. Operators are mapping out multi-layer coverage strategies in dense urban clusters, where pooling resources in the cloud has begun lifting cell-site throughput and spectrum utilization. Commercial proofs in the United States, Japan, and leading European capitals also indicate that AI-assisted scheduling can cut power draw across active radios, supporting sustainability targets alongside network modernization. Competition is intensifying as incumbent vendors defend their share against software-centric entrants, prompting a wave of partnerships that combine radio, compute, and silicon expertise to accelerate product road maps. While the cloud radio access network market benefits from supportive policy incentives, it still faces headwinds linked to spectrum release timetables and fronthaul bottlenecks that vary sharply by country.

Global Cloud Radio Access Network Market Trends and Insights

Rapid 5G Rollouts and Densification Drive Architectural Change

Global operators are lighting up mid-band 5G layers and adding small cells to fill coverage gaps. In this environment, the cloud radio access network market delivers the centralized compute pools needed to manage thousands of radios without duplicating hardware. Field trials in Tokyo, Seoul, and New York show that dynamically shifting baseband workloads can raise utilisation by 30% and boost peak cell throughput by 25%. Commercial 5G standalone cores are now coordinating time-sensitive scheduling with virtual baseband functions, underscoring how cloud-native principles shorten feature release cycles. Large-scale deployments in China and the United States reveal that the same cloud site can host multiple radio generations, easing spectrum-refarming decisions and supporting progressive migration paths. These advantages spur continued investment, particularly where indoor coverage obligations require dense radio grids.

CAPEX and OPEX Savings Sustain the Business Case

The economic attraction of virtualized baseband pools is immediate: pooling reduces hardware duplication, trims real-estate expense, and simplifies upgrades. Vendor case studies from North America indicate that operators consolidating three legacy baseband types into a single cloud cluster recorded CAPEX cuts nearing one-third during year-one rollouts. OPEX declines follow as automation tools scale preventive maintenance and remote software updates. Energy bills fall when AI schedulers place lightly loaded radios in deep-sleep modes during off-peak periods, improving the network's power-efficiency profile. These savings underpin aggressive 5G expansion plans, especially for carriers balancing dividend commitments with the need to enhance the quality of service. As consumption-based pricing models for public cloud gain traction, operators gain added flexibility to align spending with traffic peaks, reinforcing the appeal of cloud architecture.

Spectrum Scarcity and Regulatory Limits Dent Momentum

Timely clearance and auction of mid-band spectrum remains a gating factor for nationwide 5G builds. The expiry of auction authority at the United States Federal Communications Commission in 2024 introduced uncertainty around future releases, slowing some carrier investment cycles. Many emerging markets also grapple with opaque or politically driven allocation processes that delay turnkey deployment of 5G layers optimized for cloud RAN. Even where licenses are in place, guard-band conditions and power-level caps can restrict network layouts, forcing operators to rely on fragmented holdings that complicate radio planning. These realities moderate roll-out velocity and can postpone the point when pooling economics become compelling.

Other drivers and restraints analyzed in the detailed report include:

- Exponential Mobile-Data Growth Necessitates Architectural Innovation

- Network Virtualization and SDN Adoption Reshape Strategies

- Limited Fronthaul Fibre and Latency Challenges Constrain Deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The cloud radio access network market size derived from Solutions hit USD 11.3 billion in 2024, equal to 73% of segment revenue. Yet the Services market is expanding faster at an 18.4% CAGR as multi-vendor environments become the norm. Early greenfield installations chiefly required hardware and virtualized baseband licenses, but current brownfield upgrades demand integration, network optimization, and lifecycle support. Operators in Europe are signing multi-year managed-service contracts that bundle AI-driven performance analytics with DevOps enablement, letting internal teams prioritise new-service design. Consulting teams now guide spectrum-refarming, functional-split selection, and migration sequencing, roles critical for incumbent carriers balancing legacy 4G traffic and emerging private 5G use cases. Hardware providers respond by embedding open interfaces and reference automation workflows, blurring the line between product and professional service. In turn, this mix pushes the Services slice to account for a deeper share of the cloud radio access network market revenue pool as 2030 approaches.

A steady flow of innovation keeps the Solutions business vibrant. Silicon majors introduced integrated acceleration for beamforming and forward-error correction, lifting baseband capacity per rack unit by over 2X compared with 2023 blades. Radio suppliers complement these gains with lightweight Massive MIMO arrays tailored for rooftop and indoor settings. Such advancements compress the total cost of ownership while widening the addressable customer base, supporting consistent though moderate revenue growth on the Solutions side. The net result is a balanced landscape where software, silicon, and services each reinforce the transition to centrally orchestrated radio layers, widening adoption across incumbent and enterprise segments of the cloud radio access network market.

In 2024, the 5G tier commanded 61% of the overall cloud radio access network market revenue as carriers devoted capital to harness mid-band spectrum. Operators pivoted quickly to standalone architectures, which permit slicing and ultra-low-latency pipelines critical for Industry 4.0 workloads. Virtualized baseband pools make it feasible to run non-standalone 5G, LTE, and NR on common servers, letting carriers phase out 3G in favor of capacity upgrades. While 4G LTE still generates meaningful returns, its share declines each year as data-heavy consumer usage gravitates toward 5G bundles with subsidized devices.

Open RAN exhibits the fastest trajectory at a 27% CAGR through 2030, buoyed by high-profile commitments from North American and Asian tier-ones keen to diversify supply chains. The model's open interfaces encourage best-of-breed combinations, but integration overhead remains considerable. Nevertheless, pilot results from live networks in Dallas and Seoul show that multi-vendor Massive MIMO stacks can reach spectral-efficiency parity with monolithic systems when orchestrated from a unified cloud platform. Regulatory support, such as grant programs from the United States government, offers added momentum. Collectively, these forces position Open RAN as a key disruptor, widening supplier diversity while intensifying competitive dynamics across the cloud radio access network market.

The Cloud Radio Access Network (C-RAN) Market Report is Segmented by Component (Solution and Services), Network Type (5G, 4G, LTE, 3G ), Deployment Model (Centralised RAN [C-RAN], Virtualised RAN [vRAN], Open RAN [O-RAN], and Hybrid Cloud RAN), End User (Mobile Network Operators, Enterprises, Government and Public-Safety, and Neutral Host/TowerCos) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific dominates the cloud radio access network market with 39% revenue share in 2024 and leads in growth with a 23.1% CAGR. Aggressive 5G rollouts in China, Japan, and South Korea rely on high-density small-cell grids linked to large regional data centres. Operators in Shenzhen and Seoul already operate commercial open-interface clusters in core business districts, showcasing real-time spectrum pooling for video streaming during peak festivals. Governments provide supportive policy frameworks, such as spectrum fee rebates for virtualisation investments. Vendor ecosystems flourish around open testbeds, and joint ventures like the OREX initiative target export opportunities, cementing the region's leadership.

North America ranks second in terms of revenue. United States carriers earmarked multibillion-dollar budgets to swap legacy hardware for open-capable radios by 2026. Federal grants under the CHIPS and Science Act co-fund silicon research that empowers AI-based scheduling engines, giving domestic supply chains greater resilience. Early deployments in Las Vegas and Seattle prove that GPU-accelerated cloud nodes can meet stringent millisecond-level latency targets for XR gaming and industrial automation. Canadian operator collaborations with Finnish and Korean vendors extend the regional innovation sphere, highlighting cross-border technology exchange that supports the wider cloud radio access network market.

Europe accelerates adoption through a blend of regulatory mandates and competitive necessity. Operators in the United Kingdom, Germany, and Spain rolled out the first commercial 5G Open RAN macro sites, supported by public test labs that certify interoperability among radios, basebands, and management systems. The European Union dedicates funding tranches to 5G and 6G network R&D, which bolsters an academic-industry pipeline for RAN software talent. Despite lagging standalone 5G coverage, incumbents pursue fast-track plans to cloudify their radio layers, citing lower total cost of ownership and faster service innovation as key motivators. Ongoing infrastructure programs upgrade fibre backbones through rural corridors, which will remove a historic bottleneck and further expand the cloud radio access network market footprint across the region.

- Huawei Technologies Co. Ltd.

- Nokia Corporation

- Telefonaktiebolaget LM Ericsson

- Cisco Systems Inc.

- Samsung Electronics Co. Ltd.

- ZTE Corporation

- Intel Corporation

- Fujitsu Limited

- NEC Corporation

- Mavenir Systems Inc.

- Parallel Wireless Inc.

- Rakuten Symphony

- Altiostar (Rakuten)

- CommScope Holding Co. Inc.

- Casa Systems Inc.

- Airspan Networks Inc.

- Hewlett Packard Enterprise (HPE)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid 5G rollout and densification

- 4.2.2 CAPEX-OPEX savings via centralized baseband

- 4.2.3 Exponential mobile-data growth

- 4.2.4 Network virtualization and SDN demand

- 4.2.5 AI-driven RAN optimisation adoption

- 4.2.6 Energy-efficiency regulations push cloud RAN

- 4.3 Market Restraints

- 4.3.1 Spectrum scarcity and regulatory limits

- 4.3.2 Limited fronthaul fibre and latency challenges

- 4.3.3 Security and privacy risks in centralised architecture

- 4.3.4 Uncertain ROI in emerging markets

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solution

- 5.1.2 Services

- 5.1.2.1 Professional

- 5.1.2.2 Managed

- 5.2 By Network Type

- 5.2.1 5G

- 5.2.2 4G

- 5.2.3 LTE

- 5.2.4 3G (EDGE)

- 5.3 By Deployment Model

- 5.3.1 Centralised RAN (C-RAN)

- 5.3.2 Virtualised RAN (vRAN)

- 5.3.3 Open RAN (O-RAN)

- 5.3.4 Hybrid Cloud RAN

- 5.4 By End User

- 5.4.1 Mobile Network Operators

- 5.4.2 Enterprises

- 5.4.3 Government and Public-Safety

- 5.4.4 Neutral Host/TowerCos

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Huawei Technologies Co. Ltd.

- 6.4.2 Nokia Corporation

- 6.4.3 Telefonaktiebolaget LM Ericsson

- 6.4.4 Cisco Systems Inc.

- 6.4.5 Samsung Electronics Co. Ltd.

- 6.4.6 ZTE Corporation

- 6.4.7 Intel Corporation

- 6.4.8 Fujitsu Limited

- 6.4.9 NEC Corporation

- 6.4.10 Mavenir Systems Inc.

- 6.4.11 Parallel Wireless Inc.

- 6.4.12 Rakuten Symphony

- 6.4.13 Altiostar (Rakuten)

- 6.4.14 CommScope Holding Co. Inc.

- 6.4.15 Casa Systems Inc.

- 6.4.16 Airspan Networks Inc.

- 6.4.17 Hewlett Packard Enterprise (HPE)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment