|

시장보고서

상품코드

1851089

방공 시스템 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Air Defense Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

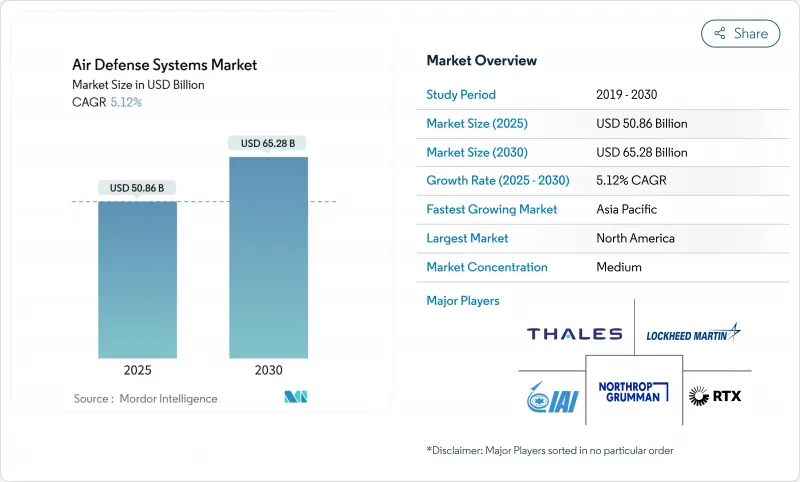

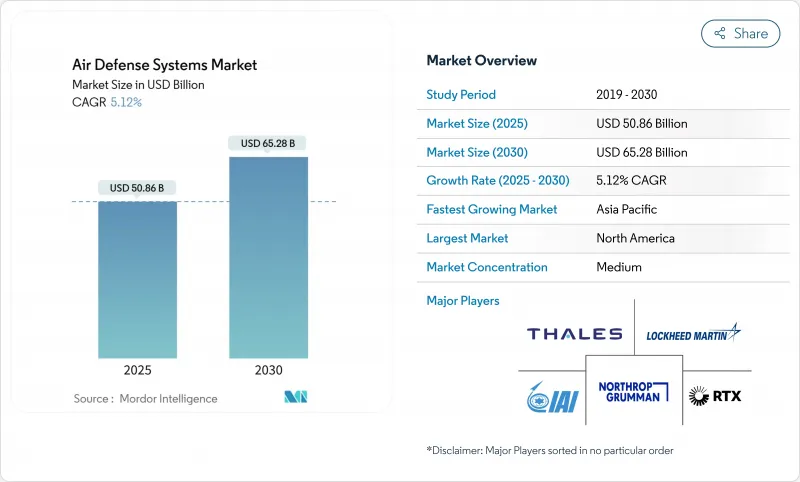

방공 시스템 시장은 2025년에 508억 6,000만 달러로 추정되며, 2030년에는 652억 8,000만 달러로 상승하여 CAGR 5.12%로 성장할 것으로 예측됩니다.

수요는 항공기 중심의 무기에서 극초음속 활공기, 기동탄도 미사일, 저비용 드론군에 대항하는 다층 솔루션으로 이동하고 있습니다. 국방부는 예산을 통합 아키텍처, 고출력 마이크로파 이펙터, 교전 사이클을 단축하는 AI 대응 명령 네트워크로 전환합니다. 북미가 가장 큰 구매자임에 변함이 없지만, 아시아태평양은 영토 문제에 따라 조달과 국산화가 가속되면서 가장 빠른 성장을 기록하고 있습니다. 프라임 계약자는 기록적인 백로그로 인해 다년간의 전망을 유지하고 있지만, 반도체공급망과 수출관리 체제의 갭이 단기 납품을 억제하고 있습니다.

세계의 방공 시스템 시장의 동향과 인사이트

통합 방공 및 미사일 방위 조달의 가속화

세계 군 조직은 현재 센서-투-슈터의 통합을 중요시하고 있으며, 레이더, 전기 광학 센서 및 이펙터를 단일 화기관제 생태계에 융합하는 개방형 아키텍처 커맨드 네트워크에 자금을 제공합니다. 미국 육군의 통합 전투 지휘 시스템은 폴란드에서 초기 운영 능력을 달성하면서 패트리어트, 센티넬, THAAD 포대 간의 실시간 데이터 교환을 입증했습니다. 유럽에서는 탈레스가 주도하는 23개 파트너로 구성된 EISNET 프로그램이 명령 대기 시간을 단축하고 공급업체 참여를 확대하기 위해 인터페이스를 표준화합니다. 각국 정부는 긴급 상황에서 항공 교통 규제 당국이 방어 노드와 협력할 수 있도록 민간과 군 간의 링크에 자금을 제공합니다. 하드웨어 주문과 관련된 폴란드의 25억 달러의 소프트웨어 패키지에서 볼 수 있듯이 통합 계약은 종종 개별 발사기의 비용을 초과합니다. 그 결과 소프트웨어 엔지니어링과 사이버 보안 네트워킹 능력이 입찰 결과를 좌우하는 경우가 많습니다.

증가하는 공중 위협의 스펙트럼

극초음속 활공기는 교전 창을 수초로 압축하므로 우주 기반의 적외선 위성과 노스롭 그라만이 개발 중인 신형 활공 위상 요격 미사일에 투자할 수 밖에 없습니다. 동시에 1대당 1,000달러 이하의 무인 항공기가 지휘부와 탄약고를 위협합니다. 군은 현재 비용과 위협의 규모를 일치시키기 위해 키네틱 미사일과 고전력 마이크로 웨이브 트럭과 무선 주파수 재머를 결합한 레이어드 아키텍처를 조달하고 있습니다. 미국 육군은 2025년의 방공 및 미사일 방위 예산을 56억 달러로 거의 배 가까이 증액해, 이러한 혼합 능력 부대의 배치를 가속시키고 있습니다. 재정적 긴급성은 요격 미사일, 레이더 업그레이드 및 UAS 키트를 선호하는 NATO의 보정 예산에도 반영됩니다.

GaN 기반 레이더 T/R 모듈 공급망의 병목 현상

질화 갈륨은 능동 전자 주사식 위상배열 레이더에 필수적이지만, 갈륨 화합물에 대한 중국의 수출 규제로 2024년에 공급이 줄어들었습니다. 미국 정부 책임국은 서부 공장에 새로운 설비투자를 하지 않으면 군사 수요를 충족할 수 없으며 리드타임은 12-18개월 연장된다고 경고하고 있습니다. 국방 당국은 현재 웨이퍼의 이중 공급을 수행하고 전략적 비축을 수행하고 있지만, 새로운 팹의 재정비에는 시간과 비용이 필요합니다. 같은 기판을 둘러싼 5G 통신 사업자와의 경쟁은 가격 경쟁을 더욱 격화시키고, 군으로부터의 주문은 파운드리의 후순위로 밀려납니다.

부문 분석

미사일 방어 시스템은 2024년 수익의 51.85%를 차지하였으며 264억 달러의 방공 시스템 시장 규모를 지원합니다. 수요는 패트리어트, THAAD, S-400 등 인구 집중 지구와 억지력을 지키는 국가 전략 프로그램에 기인합니다. 그러나 대 UAS 솔루션의 2030년까지의 CAGR은 11.21%로 도시와 전장의 공역에서의 소형 드론의 확산을 반영하고 있습니다. 군은 500달러의 쿼드콥터가 300만 달러의 요격 미사일을 발사하는 지속 불가능한 비용을 고려하여 무선 주파수 재머, 고출력 마이크로 웨이브 트레일러, 키네틱 코요테 요격 미사일 조달을 가속화하고 있습니다. 레이어 믹스는 교전 당 지출을 줄이고 더 높은 가치의 목표를 위해 장거리 요격 미사일을 보존합니다.

대 로켓포, 대포, 박격포 시스템은 간접포의 위협에도 같은 논리를 전개하고, 대공포와 지대공 미사일은 중고급 항공기에 필수적으로 유지되고 있습니다. 카타르와 같은 구매자들은 최근 코요테 블록 2 이펙터에 음향, 레이더, EO 센서를 연결하는 완전 통합된 대 드론 노드를 10억 달러에 주문했습니다. 이와 같은 전문화를 통해 공급업체는 다양해지고, 예전에는 레거시 미사일 제조업체에 한정되어 있던 분야에서 신규 참가 기업이 힘을 발휘할 수 있게 됩니다. 수요 포트폴리오의 균형을 통해 대 UAS는 보다 광범위한 방공 시스템 시장에서 중요한 성장 엔진으로 자리매김하고 있습니다.

육상발사기는 2024년 지출액의 42.90%를 차지하였으며, 수도, 항공기지, 산업중추를 지키는 고정설비로서 방공 시스템 시장 점유율을 지원하고 있습니다. 각국은 패트리어트와 S-400을 계속 확장하고 있지만, 대함탄도 미사일의 위협이 높아지고 있기 때문에 해상 기반 플랫폼은 CAGR 5.89%로 성장을 지속하고, 있습니다. 최신 이지스 구축함은 탄도 미사일 방어를 통합한 소프트웨어 업데이트를 탑재하고, 일부 해군은 드론 제압을 위해 갑판 탑재 레이저를 추가하고 있습니다. 해안 국가들은 항만과 해상 플랫폼 주변의 지역 침범을 거부하고 협동 교전 기능을 갖춘 함선 통합 레이더 수요를 높이고 있습니다.

항공기 장착 시스템은 원정 항공 원호를 제공하며 육상 배터리가 도착하기 전에 필요를 채우는 경우가 많습니다. 우주 기반 센서는 조기 경보 데이터를 각 플랫폼에 전달하여 세계 미사일 추적의 백본 역할을 합니다. 현재 지역 횡단적인 큐잉이 생존성을 정의하고 있기 때문에 해군은 실시간 위성 피드와 지상 레이더 트럭을 수용하는 오픈 인터페이스를 지정하고 있습니다. 이 수렴은 해상 및 지상 조달주기의 역사적 경계를 모호하게 만들고 방공 시스템 시장의 기회를 더욱 확대합니다.

지역 분석

북미는 2024년 세계 매출의 37.90%를 차지하였으며 미국의 다층적인 국토 방어력과 견고한 대외 군사 판매 파이프라인에 의해 지원되고 있습니다. RTX와 록히드 마틴의 2025년 1분기 매출은 총 380억 달러를 넘었으며 국내의 대규모 기술 기반을 제공합니다. 캐나다의 NORAD 현대화는 오버 더 호라이즌 레이더 사이트와 북극 위성 통신에 자금을 투입하고 멕시코는 중요한 에너지 인프라를 위해 모바일 SHORAD 구매를 고려하고 있습니다. 미국 우주군의 우주 기반 미사일 경보 프로그램은 다수 동맹국의 요격 체인에 데이터를 공급하면서 지역적 영향력을 증폭시킵니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 가장 높은 7.90%를 기록할 전망입니다. 일본은 이지스 어쇼어의 파생형 개발에 착수하고 한국의 계약자는 KM-SAM II를 걸프 국가 고객에게 수출하여 이 지역이 수입국에서 순수출국으로 이동하고 있음을 나타냅니다. 인도는 통합 방공 무기 시스템의 개발을 가속화하여 센서 패키지의 공동 생산 오프셋을 협상하고 있습니다. 호주는 공동 프로젝트 9102에 자금을 제공하고 이지스 함에 연결하는 소버린 위성 통신을 추가합니다. 필리핀과 같은 소규모 국가는 군도 지형에 대한 신속한 대응에 대한 욕구를 반영하여 Spyder와 FA-50 함대를 확장합니다.

유럽은 유럽 스카이실드 이니셔티브 하에서 투자를 확대하고 21개국을 공통 조달, 조직, 훈련 모델에 참여시켜 수요를 집약합니다. 독일은 IRIS-T SLM 배터리를, 폴란드는 IBCS 기반 Wisla 대대를, 최근 NATO에 가입한 스웨덴은 록히드 마틴에 TPI-4 감시 레이더를 주문했습니다. EU 기금은 국경을 넘어서는 대기열을 확보하기 위한 개방형 아키텍처 명령 시스템에 중점을 둡니다.

중동에서는 걸프 국가가 순항 미사일과 무인 정찰기에 대한 정유소와 공항을 강화하기 때문에 미국, 유럽 및 자국의 솔루션이 혼합되어 있습니다. 사우디아라비아는 2025년 THAAD 부품 조립을 국내에서 시작하여 '비전 2030' 하에서 국산화를 강화하고 있습니다. 이스라엘은 아이언 돔과 David's Sling 등의 다층 애드온을 개발하고 전투에서 입증된 벤치마크를 제공함으로써 세계 입찰 사양을 형성하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 통합 방공 및 미사일 방위 조달의 가속

- 공중으로부터의 위협 격화

- 스텔스 검출을 위한 AI 대응 센서 퓨전

- 모바일 지향 에너지 SHORAD의 채용

- GaN 기반 AESA 레이더 비용 저하

- 대 UAS 및 포인트 디펜스에 대한 예산 증가

- 시장 성장 억제요인

- GaN 레이더 모듈 공급 체인의 병목

- 엄격한 ITAR과 MTCR의 수출 규제가 신흥국에의 시스템 판매를 제한

- 기동하는 극초음속 목표를 확실히 요격하기 위한 기술적 및 재료적 과제, 연구개발 리스크의 증가

- 전자파의 혼잡이 상호 운용성의 과제를 높임

- 밸류체인 분석

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 시스템별

- 미사일 방어 시스템

- 대공포 및 SAM 시스템

- 대 무인 항공기 시스템(C-UAS)

- 대 로켓포, 대포, 박격포(C-RAM)

- 플랫폼별

- 육상 기반

- 해상 기반

- 항공 기반

- 우주 기반

- 범위별

- 단거리

- 중거리

- 장거리

- 서브시스템별

- 무기 시스템

- 화기관제 시스템

- 커맨드 & 컨트롤 시스템

- 기타

- 기술별

- 키네틱 킬 이펙터

- 고에너지 레이저 시스템

- 고전력 마이크로파 시스템

- 전자전(EW) 소프트킬 솔루션

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 이스라엘

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- RTX Corporation

- Lockheed Martin Corporation

- Israel Aerospace Industries Ltd.

- Northrop Grumman Corporation

- Thales Group

- Saab AB

- Rheinmetall AG

- Leonardo SpA

- Kongsberg Gruppen ASA

- The Boeing Company

- ASELSAN Elektronik Sanayi ve Ticaret AS

- Hanwha Systems Co., Ltd.

- Rafael Advanced Defense Systems Ltd.

- L3Harris Technologies, Inc.

- BAE Systems plc

- MBDA

- Diehl Group

- Elbit Systems Ltd.

- Bharat Dynamics Limited(BDL)

- China Aerospace Science and Technology Corporation

- MDA Ltd.

- China North Industries Group Corporation(Norinco)

제7장 시장 기회와 미래 전망

CSM 25.11.20The air defense systems market is valued at USD 50.86 billion in 2025 and is projected to climb to USD 65.28 billion by 2030, advancing at a 5.12% CAGR.

Demand pivots from aircraft-centric weapons to multilayer solutions that counter hypersonic glide vehicles, maneuvering ballistic missiles, and low-cost drone swarms. Defense ministries re-prioritize budgets toward integrated architectures, high-power microwave effectors, and AI-enabled command networks that shorten engagement cycles. North America remains the largest buyer, while Asia-Pacific records the fastest regional growth as territorial disputes accelerate procurement and indigenous production. Prime contractors sustain multi-year visibility through record backlogs, yet gaps in semiconductor supply chains and export-control regimes temper short-term deliveries.

Global Air Defense Systems Market Trends and Insights

Acceleration of Integrated Air and Missile Defense Procurement

Global militaries now treat sensor-to-shooter integration as critical, funding open-architecture command networks that fuse radars, electro-optical sensors, and effectors into a single fire-control ecosystem. The US Army's Integrated Battle Command System achieved initial operational capability in Poland, demonstrating real-time data exchange among Patriot, Sentinel, and THAAD batteries. In Europe, the 23-partner EISNET program led by Thales standardizes interfaces to cut command latency and widen supplier participation. Governments fund civilian-military links so air traffic regulators can coordinate with defense nodes during emergencies. Integration contracts often exceed the cost of individual launchers, as evidenced by Poland's USD 2.5 billion software package, which accompanies hardware orders. As a result, software engineering and cyber-secure networking capabilities increasingly decide tender outcomes.

Escalating Spectrum of Airborne Threats

Hypersonic glide vehicles compress engagement windows to seconds, forcing investment in space-based infrared satellites and nascent glide-phase interceptors under development by Northrop Grumman. Simultaneously, drone swarms costing under USD 1,000 per airframe threaten command posts and ammunition depots. Militaries now procure layered architectures that mate kinetic missiles with high-power microwave trucks and radio-frequency jammers to match cost with threat scale. The US Army nearly doubled its 2025 air and missile defense budget to USD 5.6 billion to speed deployment of such mixed-capability formations. Fiscal urgency is echoed in NATO supplemental budgets prioritizing interceptors, radar upgrades, and counter-UAS kits.

Supply-Chain Bottlenecks in GaN-Based Radar T/R Modules

Gallium nitride is indispensable for active electronically scanned array radars, yet Chinese export curbs on gallium compounds tightened supplies in 2024. The US Government Accountability Office warns that Western fabs cannot meet military demand without fresh capital investment, stretching lead times by 12-18 months. Defense primes now dual-source wafers and lobby for strategic stockpiles, but requalification of new fabs takes time and adds cost. Competition from 5G telecoms for the same substrates further inflates pricing and crowds military orders to the back of foundry queues.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Sensor Fusion Improving Track-Before-Detect Probability for Stealth Targets

- Emergence of Mobile Directed-Energy SHORAD for Base and Asset Protection

- Stringent ITAR and MTCR Export Controls Limiting System Sales to Emerging Nations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Missile defense systems accounted for 51.85% of 2024 revenues, anchoring the air defense systems market size at USD 26.4 billion. Demand stems from national strategic programs such as Patriot, THAAD, and S-400 that safeguard population centers and deterrent forces. Yet counter-UAS solutions register an 11.21% CAGR to 2030, mirroring the proliferation of small drones over urban and battlefield airspace. Militaries weigh the unsustainable cost of firing USD 3 million interceptors at USD 500 quadcopters, accelerating procurement of radio-frequency jammers, high-power microwave trailers, and kinetic Coyote interceptors. A layered mix reduces expenditure per engagement and preserves long-range interceptors for higher-value targets.

Counter-rocket, artillery, and mortar systems extend the same logic to indirect-fire threats, while anti-aircraft guns and surface-to-air missiles remain essential for medium-altitude aircraft. Buyers such as Qatar recently placed USD 1 billion orders for fully integrated counter-drone nodes that link acoustic, radar, and EO sensors to Coyote Block 2 effectors. This specialization diversifies supplier rosters, giving newer entrants leverage in a field once reserved for legacy missile houses. The rebalanced demand portfolio positions Counter-UAS as a critical growth engine within the broader air defense systems market.

Land-based launchers generated 42.90% of 2024 spending and anchor the air defense systems market share because fixed installations guard capitals, air bases, and industrial hubs. Nations continue to expand Patriot and S-400 sites, yet sea-based platforms are posting a 5.89% CAGR thanks to rising anti-ship ballistic missile threats. Modern Aegis destroyers carry revised software builds incorporating ballistic missile defense, and several navies add deck-mounted lasers for drone suppression. Littoral nations seek area denial around ports and offshore platforms, boosting demand for ship-integrated radars with cooperative engagement functions.

Aircraft-mounted systems supply expeditionary air coverage, often plugging gaps before land batteries arrive. Space-based sensors distribute early-warning data to every platform, acting as the backbone of global missile tracking. Because cross-domain cueing now defines survivability, navies specify open interfaces that accept real-time satellite feeds and ground radar tracks. This convergence blurs the historical boundary between maritime and terrestrial procurement cycles and further enlarges the opportunity within the air defense systems market.

The Air Defense Systems Market Report is Segmented by System (Missile Defense Systems, Anti-Aircraft Gun and SAM Systems, and More), Platform (Land-Based, Sea-Based, and More), Range (Short, Medium, and Long), Sub-System (Weapon System, Fire Control System, and More), Technology (Kinetic-Kill Effectors, and More ), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America controlled 37.90% of global revenue in 2024, buoyed by the United States' multi-layered homeland shield and robust foreign military sales pipeline. Combined Q1 2025 sales of RTX and Lockheed Martin surpassed USD 38 billion, providing a large domestic engineering base. Canada's NORAD modernization injects funds into over-the-horizon radar sites and Arctic satellite communications, while Mexico explores mobile SHORAD purchases for critical energy infrastructure. Space-based missile warning programs under the US Space Force amplify regional influence because their data feeds many allied intercept chains.

Asia-Pacific posts the fastest 7.90% CAGR to 2030. Japan fields Aegis Ashore derivatives, and contractors in South Korea exported the KM-SAM II to Gulf customers, demonstrating the region's shift from importer to net exporter. India accelerates its Integrated Air Defence Weapon System and negotiates co-production offsets for sensor packages. Australia funds Joint Project 9102 to add sovereign satellite communications that plug into Aegis afloat. Smaller players like the Philippines expand Spyder and FA-50 fleets, reflecting a desire for quick-reaction coverage of archipelagic terrain.

Europe increases investment under the European Sky Shield Initiative, bringing 21 nations into a common procure-organize-train model that aggregates demand. Germany champions IRIS-T SLM batteries, Poland fields IBCS-based Wisla battalions, and recent NATO entrant Sweden ordered TPY-4 surveillance radars from Lockheed Martin. EU funds focus on open-architecture command systems to ensure cross-border cueing.

The Middle East attracts a mix of US, European, and indigenous solutions as Gulf states harden refineries and airports against cruise missiles and drones. Saudi Arabia initiated domestic THAAD component assembly in 2025, reinforcing localization under Vision 2030. Israel continues to iterate on Iron Dome and multi-layer add-ons such as David's Sling, offering combat-proven benchmarks that shape tender specifications worldwide.

- RTX Corporation

- Lockheed Martin Corporation

- Israel Aerospace Industries Ltd.

- Northrop Grumman Corporation

- Thales Group

- Saab AB

- Rheinmetall AG

- Leonardo S.p.A.

- Kongsberg Gruppen ASA

- The Boeing Company

- ASELSAN Elektronik Sanayi ve Ticaret Anonim ?irketi

- Hanwha Systems Co., Ltd.

- Rafael Advanced Defense Systems Ltd.

- L3Harris Technologies, Inc.

- BAE Systems plc

- MBDA

- Diehl Group

- Elbit Systems Ltd.

- Bharat Dynamics Limited (BDL)

- China Aerospace Science and Technology Corporation

- MDA Ltd.

- China North Industries Group Corporation (Norinco)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Acceleration of integrated air and missile defense procurement

- 4.2.2 Escalating spectrum of airborne threats

- 4.2.3 AI-enabled sensor fusion for stealth detection

- 4.2.4 Mobile directed-energy SHORAD adoption

- 4.2.5 GaN-based AESA radar cost decline

- 4.2.6 Higher budgets for counter-UAS and point defense

- 4.3 Market Restraints

- 4.3.1 Supply-chain bottlenecks in GaN radar modules

- 4.3.2 Stringent ITAR and MTCR export controls limiting system sales to emerging nations

- 4.3.3 Technical and materials challenges in reliably intercepting maneuvering hypersonic targets, inflating R&D risk

- 4.3.4 Electromagnetic spectrum congestion raising inter-operability challenges

- 4.4 Value Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers/Consumers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By System

- 5.1.1 Missile Defense Systems

- 5.1.2 Anti-Aircraft Gun and SAM Systems

- 5.1.3 Counter-Unmanned Aerial Systems (C-UAS)

- 5.1.4 Counter-Rocket, Artillery and Mortar (C-RAM)

- 5.2 By Platform

- 5.2.1 Land-Based

- 5.2.2 Sea-Based

- 5.2.3 Air-Based

- 5.2.4 Space-Based Early-Warning Assets

- 5.3 By Range

- 5.3.1 Short Range

- 5.3.2 Medium Range

- 5.3.3 Long Range

- 5.4 By Sub-system

- 5.4.1 Weapon System

- 5.4.2 Fire Control System

- 5.4.3 Command and Control System

- 5.4.4 Others

- 5.5 By Technology

- 5.5.1 Kinetic-Kill Effectors

- 5.5.2 High-Energy Laser Systems

- 5.5.3 High-Power Microwave Systems

- 5.5.4 Electronic Warfare (EW) Soft-Kill Solutions

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Israel

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 RTX Corporation

- 6.4.2 Lockheed Martin Corporation

- 6.4.3 Israel Aerospace Industries Ltd.

- 6.4.4 Northrop Grumman Corporation

- 6.4.5 Thales Group

- 6.4.6 Saab AB

- 6.4.7 Rheinmetall AG

- 6.4.8 Leonardo S.p.A.

- 6.4.9 Kongsberg Gruppen ASA

- 6.4.10 The Boeing Company

- 6.4.11 ASELSAN Elektronik Sanayi ve Ticaret Anonim ?irketi

- 6.4.12 Hanwha Systems Co., Ltd.

- 6.4.13 Rafael Advanced Defense Systems Ltd.

- 6.4.14 L3Harris Technologies, Inc.

- 6.4.15 BAE Systems plc

- 6.4.16 MBDA

- 6.4.17 Diehl Group

- 6.4.18 Elbit Systems Ltd.

- 6.4.19 Bharat Dynamics Limited (BDL)

- 6.4.20 China Aerospace Science and Technology Corporation

- 6.4.21 MDA Ltd.

- 6.4.22 China North Industries Group Corporation (Norinco)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment