|

시장보고서

상품코드

1851093

음성 바이오메트릭스 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Voice Biometrics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

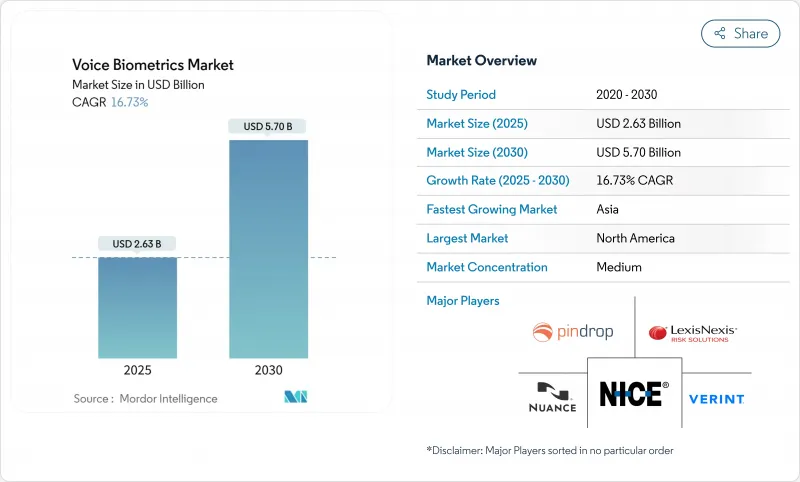

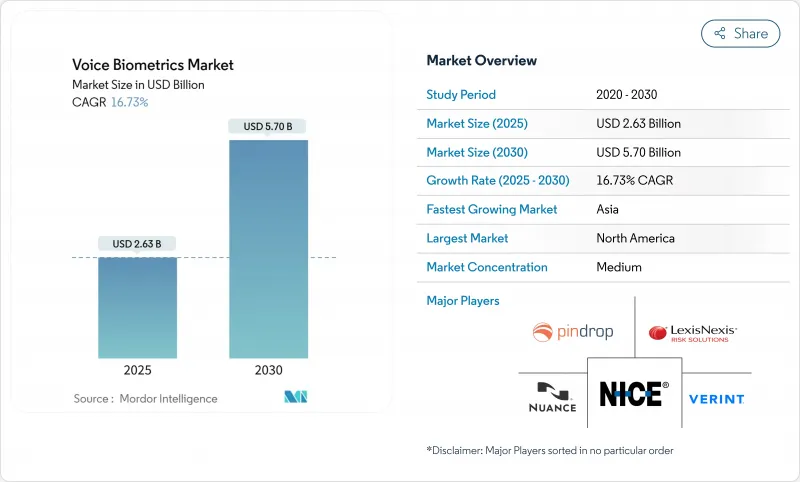

음성 바이오메트릭스 시장은 2025년에는 26억 3,000만 달러로 추정되고, 2030년에는 57억 달러에 이를 것으로 예측되며, CAGR 16.73%로 성장할 전망입니다.

사이버 범죄자들이 인공지능, 소셜 엔지니어링, 합성 음성을 무기로 하고 암호의 신뢰성을 저하시키고 있기 때문에 수요가 높아지고 있습니다. 금융기관, 통신 사업자, 정부 기관은 지식 기반 질문을 실시간 음성 인증으로 대체함으로써 대응하고 있습니다. 5G의 커버리지 확대, 스마트폰의 엣지 AI 칩, 클라우드 추론 비용의 저하도 채용을 뒷받침하고 있습니다. 규제 당국은 성문을 기밀성이 높은 개인 데이터로 분류하고 있기 때문에 기업은 프라이버시 바이 디자인의 실천이 되는 스푸핑 방지 분석을 조합해야 합니다. 플랫폼 기업이 생체 인식을 제로 트러스트 툴킷에 통합하는 반면, 전문 기업은 딥 페이크 검출 모듈과 저자원 방언을 위해 조정된 다국어 모델을 제공하기 때문에 공급업체의 통합이 진행되고 있습니다.

세계의 음성 바이오메트릭스 시장 동향 및 인사이트

모바일 뱅킹에서 패스워드리스 인증으로 마이그레이션

은행과 전자 지갑 제공업체는 로그인 시 포기를 줄이고 계정 탈취 사기를 막기 위해 정적 암호를 음성 인쇄로 대체합니다. 컨택 센터 리더의 81%는 이미 음성 인증을 도입하거나 계획했으며, 아일랜드 은행과 같은 주요 기관은 3,600만 달러를 투자하여 대화형 음성 응답 메뉴에 음성 검사를 통합했습니다. 이 방식은 타이핑에 시간이 걸리고, 실수를 하기 쉬운 작은 화면에 적합하며, 통화 중에 지속적으로 인증을 함으로써, 핸들링 시간을 단축하고, 원 타임 코드를 삭제할 수 있습니다.

강력한 고객 인증에 대한 규제 압력

PSD2, 인도 준비 은행 지침, 미국 인스턴트 지불 레일 등의 규칙에 따라 금융 회사는 최소한 두 개의 독립적인 요소로 사용자의 신원을 증명할 의무가 있습니다. 음성 바이오메트릭스는 고객에게 추가 하드웨어를 제공하지 않고 규정 준수를 충족하는 고유한 레이어를 추가합니다. EU의 인공지능법은 음성 검증을 고위험 카테고리로 자리매김하고 공급자에게 모델 거버넌스, 바이어스 테스트, 사고 대응을 문서화할 것을 의무화하고, 인증 플랫폼의 조달을 가속화하고 있습니다.

다국어 및 방언이 풍부한 모델의 편향

학술적 벤치마크는 비표준 악센트, 성별 및 연령 그룹의 단어 오류율이 높은 것으로 나타났으며 공정성에 대한 논의가 일어나고 있습니다. 격차는 신뢰를 훼손하고, 일반에 대한 보급을 늦추며, 평등 지침을 위반할 수 있습니다. 공급업체는 현재 교육 코퍼스를 확장하고 정기적인 바이어스 감사를 실시하며 규제 당국과 시민 사회의 옵저버를 안심시키기 위해 투명한 모델 카드를 발행하고 있습니다.

부문 분석

패시브 검증은 2024년 음성 바이오메트릭스 시장의 20% 미만이었지만, CAGR 18.8%로 주요 시장보다 빠르게 성장할 것으로 예측됩니다. 그 매력은 자연스럽게 대화하는 동안 발신자를 인증하고 스크립팅 된 문구를 제거하며 평균 처리 시간을 최대 45초 단축하는 것입니다. 콜로라도의 신용 조합에서는 키패드 질문으로 대체한 후 시간 절약을 확인했습니다. 활성 방법은 62%의 리더십을 유지합니다. 왜냐하면 의무화된 문구는 고가치 전송과 정부 클리어런스에 필수적인 견고한 감사 추적을 제공하기 때문입니다. 위험 점수가 허용 범위를 초과하는 경우에만 활성 폴백을 발생시키는 하이브리드 스택이 나타납니다.

패시브 솔루션은 엣지 디바이스에서 실행되는 실시간 신호 처리 및 스피커 다이얼라이제이션의 발전으로 혜택을 누리고 있습니다. 세션 중 지속적인 모니터링은 계정 공유 및 강제 감지에도 도움이 됩니다. 한편, 액티브 엔진은 보다 짧은 패스프레이즈와 지원되는 휴대 단말기에서의 프롬프트리스 인증에 의해 혁신합니다. 이 두 부서는 기업이 보증 및 사용성을 결합하여 음성 바이오메트릭스 시장을 강화합니다.

코어가 되는 음성 특징 추출 라이브러리와 모델 관리 콘솔에 의해 2024년에도 소프트웨어가 지출의 70%를 차지했습니다. 그러나 전문 서비스 및 관리 서비스는 CAGR 18.5%로 추이할 것으로 예측됩니다. 이는 수십 개의 언어를 지원하는 엔진의 미세 조정, 레거시 IVR 플랫폼에 대한 연결, 딥페이크 공격에 대한 레드 팀 테스트 수행 등의 필요성을 반영합니다. 텔레콤 비즈니스 프로세스 아웃소서는 틈새 알고리즘 공급업체와 제휴하여 호스팅, 튜닝 및 지속적인 악성 모니터링을 번들로 제공하는 턴키 패키지를 제공합니다.

컨설턴트는 또한 진화하는 개인정보 보호법을 통해 고객의 조타를 수행하고 데이터 보호 영향 평가를 초안하며 동의 흐름을 설계합니다. 관리 서비스 계약에는 침해 사건에 대한 신속한 대응 팀과 분기별 편견 보고서도 포함됩니다. 이러한 계약이 성숙함에 따라 부정 손실 감소와 연계된 성과 기반 가격 설정이 보급되어 서비스 수입이 음성 바이오메트릭스 시장에 깊숙히 통합될 수 있습니다.

음성 바이오메트릭스 시장은 유형별(활성 바이오메트릭스 및 패시브 바이오메트릭스), 전개 모드별(온프레미스 및 클라우드), 기업 규모별(중소기업 및 대기업), 최종 이용 산업별(은행, 금융 서비스 및 보험, 기타), 용도별(부정 검출 및 예방, 기타), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역 분석

북미는 은행, 카드 네트워크, 헬스케어 제공업체의 조기 채용으로 음성 바이오메트릭스 시장의 가장 큰 부분을 차지합니다. 연방 규정에서 성문은 기밀성이 높은 식별자로 분류되므로 공급업체는 FedRAMP 인증 클라우드 및 암호화를 도입하고 정부 기관의 감사를 지원합니다. 기업의 사이버 대책 예산을 통한 컨택 센터의 현대화는 수요를 더욱 높여줍니다. 벤처캐피탈도 음성 보안의 신흥기업을 지원하고 혁신을 현지에 두고 있습니다.

아시아태평양이 가장 빠르게 성장하고 있습니다. 인도의 통일 결제 인터페이스와 스마트폰의 급속한 보급이 언어에 얽매이지 않는 종합적인 인증의 토양을 형성하고 있습니다. 중국은 슈퍼 앱 생태계 전반에 걸쳐 화자 인증 규모를 확대하고 ASEAN의 통신 사업자는 SIM 스왑 사기를 억제하기 위해 음성 라이브 렌스를 통합하고 있습니다. 지역 데이터 현지화 방법은 국경 내에서 모델을 호스팅하는 합작 투자를 장려하고 국내 용량을 자극합니다.

유럽에서는 첨단 인프라와 세계에서 가장 엄격한 프라이버시 프레임 워크가 결합되어 있습니다. 인공지능법은 화자 인식을 고위험으로 지정하고 있으므로 기업은 설명 가능한 추론과 상세한 감사 로그를 갖춘 인증 툴킷을 조달합니다. 뱅크 오브 아일랜드의 3,400만 유로(3,600만 달러) 프로그램과 같은 투자 발표는 컴플라이언스와 고객의 편의성이 교차하는 곳에 예산이 흐르고 있음을 보여줍니다.

라틴아메리카와 아프리카는 절대적인 지출액으로 뒤처져 있지만 상당한 상승 여지가 있습니다. 브라질과 남아프리카의 통신 사업자는 음성 대응 IVR을 도입하고, 에이전트의 작업 부담을 경감하며, 선불 가입자의 확인을 실시했습니다. 독립 타워 전개로 4G 커버리지가 향상되어 클라우드 추론이 가능해졌습니다. 현지 악센트의 다양성과 자원이 적은 언어는 트랜스퍼 학습이나 지역 데이터세트를 통해 벤더가 대처할 수 있는 과제로 음성 바이오메트릭스 시장의 리치를 넓히고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 모바일 뱅킹에서 패스워드리스 인증으로의 전환

- 강력한 고객 인증에 대한 규제 압력(PSD2, RBI, FedNow)

- 딥페이크 사기의 급증이 콘택트 센터의 업그레이드 촉진

- 신흥 아시아에서 핀텍 주도의 급속한 결제 성장

- 기업에서 제로 트러스트 아키텍처 채용 확대

- 전화 회사에서 음성 대응 IVR의 비용 절감 의무

- 시장 성장 억제요인

- 다언어 및 방언 리치 모델의 바이어스

- 클라우드 도입을 제한하는 데이터 거주 규제

- 리모트 ID&V에서의 음향 변동(비디오 통화)

- 스마트 홈에서 배경 음성으로부터의 높은 오인식률

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 경쟁 기업 간 경쟁 관계

- 대체품의 위협

- 투자 분석

제5장 시장 규모 및 성장 예측

- 인증 유형별

- 액티브 바이오메트릭스

- 패시브 바이오메트릭스

- 컴포넌트별

- 소프트웨어/SDK

- 서비스(통합, 컨설팅, 관리)

- 전개 모드별

- 클라우드

- 온프레미스

- 기업 규모별

- 중소기업

- 대기업

- 채널 및 액세스 포인트별

- IVR 및 콘택트 센터

- 모바일 앱

- 웹과 키오스크

- 스마트 디바이스 및 IoT

- 용도별

- 부정 행위의 검출 및 방지

- 고객인증과 IDandV

- 결제 및 거래 보안

- 워크포스 관리 및 논리 액세스

- 최종 이용 산업별

- 은행, 금융서비스 및 보험

- 정부 및 법 집행 기관

- 통신 및 IT

- 헬스케어

- 소매, 전자상거래, CPG

- 운송 및 물류

- 기타(교육, 접객)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN-5

- 호주

- 뉴질랜드

- 기타 아시아태평양

- 중동

- GCC

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Nuance Communications Inc.

- NICE Ltd

- Verint Systems Inc.

- Pindrop Security Inc.

- LexisNexis Risk Solutions Inc.

- LumenVox LLC

- Phonexia sro

- Auraya Inc.

- Aculab Plc

- Uniphore Software Systems

- SESTEK

- VoicePIN.com Sp. z oo

- Illuma

- BioCatch Ltd.

- Reality Defender

- Sensory Inc.

- Neustar Inc.

- Veridas

- ID R&D Inc.

- Synaptics Inc.

제7장 시장 기회 및 향후 전망

AJY 25.11.12The voice biometrics market is valued at USD 2.63 billion in 2025 and is forecast to reach USD 5.70 billion by 2030, advancing at a 16.73% CAGR.

Demand is rising because cyber-criminals now weaponize artificial intelligence, social engineering, and synthetic speech, rendering passwords unreliable. Financial institutions, telecom operators, and government agencies respond by replacing knowledge-based questions with real-time voice verification. Wider 5G coverage, edge AI chips in smartphones, and lower cloud inference costs also sustain adoption. Regulatory authorities classify voiceprints as sensitive personal data, so organizations must combine privacy-by-design practices with anti-spoofing analytics. Vendor consolidation is underway as platform players integrate biometrics into zero-trust toolkits, while specialist firms supply deepfake detection modules and multilingual models tuned for low-resource dialects.

Global Voice Biometrics Market Trends and Insights

Transition to password-less authentication in mobile banking

Banks and e-wallet providers substitute static passwords with voiceprints to decrease abandonment during log-in and to stop account-takeover fraud. 81% of contact-center leaders already deploy or plan voice verification, and flagship institutions such as Bank of Ireland invested USD 36 million to embed voice checks into interactive voice response menus. The method suits small screens where typing is slow and error-prone, while continuous authentication during a call trims handle time and removes one-time codes.

Regulatory pressure for strong customer authentication

Rules such as PSD2, the Reserve Bank of India's guidelines, and US instant-payment rails oblige financial firms to prove user identity with at least two independent factors. Voice biometrics adds an inherent layer that satisfies compliance without extra hardware for customers. The EU Artificial Intelligence Act labels voice verification a high-risk category, obliging providers to document model governance, bias testing, and incident response, accelerating procurement of certified platforms.

Bias in multilingual and dialect-rich models

Academic benchmarks show higher word-error rates for under-represented accents, genders, and age groups, triggering fairness debates. Disparities erode trust, slow public roll-outs, and may breach equality directives. Vendors now widen training corpora, run periodic bias audits, and issue transparent model cards to reassure regulators and civil-society observers.

Other drivers and restraints analyzed in the detailed report include:

- Deepfake-driven contact-center upgrades

- Fintech-led payment growth in emerging Asia

- Data-residency rules limiting cloud deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passive verification analyzed less than 20% of the voice biometrics market in 2024, yet is forecast to grow faster than the headline rate, moving at 18.8% CAGR. Its appeal lies in authenticating callers during natural conversation, eliminating scripted phrases, and shaving up to 45 seconds from average handle-time. The Credit Union of Colorado confirmed time savings after replacing keypad questions. Active methods retain 62% leadership because mandated phrases deliver robust audit trails critical for high-value transfers and government clearances. Hybrid stacks are emerging that trigger active fallback only when risk scores exceed tolerance.

Passive solutions benefit from advances in real-time signal processing and speaker diarization running on edge devices. Continuous monitoring throughout a session also helps detect account sharing and coercion. Meanwhile, active engines innovate with shorter passphrases and promptless verification on supported handsets. The two branches together reinforce the voice biometrics market as enterprises mix assurance and usability.

Software still provided 70% of spending in 2024 thanks to core speech-feature extraction libraries and model-management consoles. Yet professional and managed services are projected to advance 18.5% CAGR, reflecting the need to fine-tune engines for dozens of languages, connect to legacy IVR platforms, and run red-team tests against deepfake attacks. Telecom-business-process outsourcers partner with niche algorithm suppliers to offer turnkey packages that bundle hosting, tuning, and continuous fraud monitoring.

Consultants also steer clients through evolving privacy law, draft data-protection-impact assessments, and design consent flows. Managed-service contracts include rapid-response teams for breach events and quarterly bias reporting. As these engagements mature, outcome-based pricing linked to fraud-loss reduction gains traction, embedding service revenue deeper into the voice biometrics market.

Voice Recognition Biometrics Market It Segmented by Type (Active Biometrics and Passive Biometrics), Deployment Model (On-Premises and Cloud), Enterprise Size (Small and Medium Enterprises and Large Enterprises), End-Use Industry (Banking, Financial Services and Insurance, and More), Application (Fraud Detection and Prevention and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America holds the largest portion of the voice biometrics market owing to early adoption by banks, card networks, and healthcare providers. Federal rules classify voiceprints as sensitive identifiers, so vendors deploy FedRAMP-authorized clouds and encryption to satisfy agency audits. Contact-center modernization funded under corporate cyber-resilience budgets further boosts demand. Venture capital also backs speech-security startups, keeping innovation local.

Asia Pacific is the swiftest-growing region. India's unified-payments interface and rapid smartphone uptake create fertile ground for inclusive, language-agnostic authentication. China scales speaker recognition across super-app ecosystems, while ASEAN telcos embed voice liveness to curb SIM-swap fraud. Regional data-localization laws encourage joint ventures that host models inside national borders, stimulating domestic capacity.

Europe combines advanced infrastructure with the world's strictest privacy framework. The Artificial Intelligence Act designates speaker recognition as high-risk, so enterprises procure certified toolkits with explainable inference and detailed audit logs. Investment announcements such as Bank of Ireland's EUR 34 million (USD 36 million) program show that budget still flows where compliance and customer convenience intersect.

Latin America and Africa trail in absolute spend but present sizable upside. Telecom operators in Brazil and South Africa deploy voice-enabled IVR to cut agent workload and verify prepaid subscribers. Independent tower roll-outs have improved 4G coverage, enabling cloud inference. Local accent diversity and low-resource languages are challenges that vendors address through transfer learning and regional datasets, thereby extending reach of the voice biometrics market.

- Nuance Communications Inc.

- NICE Ltd

- Verint Systems Inc.

- Pindrop Security Inc.

- LexisNexis Risk Solutions Inc.

- LumenVox LLC

- Phonexia s.r.o.

- Auraya Inc.

- Aculab Plc

- Uniphore Software Systems

- SESTEK

- VoicePIN.com Sp. z o.o.

- Illuma

- BioCatch Ltd.

- Reality Defender

- Sensory Inc.

- Neustar Inc.

- Veridas

- ID R&D Inc.

- Synaptics Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Transition to Password-less Authentication in Mobile Banking

- 4.2.2 Regulatory Pressure for Strong Customer Authentication (PSD2, RBI, FedNow)

- 4.2.3 Surge in Deep-Fake Fraud Driving Contact-Center Upgrades

- 4.2.4 Rapid FinTech-Led Payment Growth in Emerging Asia

- 4.2.5 Growing Adoption of Zero-Trust Architecture in Enterprises

- 4.2.6 Voice-Enabled IVR Cost-Saving Mandates in Telcos

- 4.3 Market Restraints

- 4.3.1 Bias in Multilingual & Dialect-Rich Models

- 4.3.2 Data-Residency Regulations Limiting Cloud Deployment

- 4.3.3 Acoustic Variability in Remote ID&V (Video Calls)

- 4.3.4 High False-Accept Rate from Background Speech in Smart Homes

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Authentication Type

- 5.1.1 Active Biometrics

- 5.1.2 Passive Biometrics

- 5.2 By Component

- 5.2.1 Software/SDK

- 5.2.2 Services (Integration, Consulting, Managed)

- 5.3 By Deployment Model

- 5.3.1 Cloud

- 5.3.2 On-premise

- 5.4 By Enterprise Size

- 5.4.1 Small and Medium Enterprises

- 5.4.2 Large Enterprises

- 5.5 By Channel/Access Point

- 5.5.1 IVR/Contact Center

- 5.5.2 Mobile Apps

- 5.5.3 Web and Kiosk

- 5.5.4 Smart Devices/IoT

- 5.6 By Application

- 5.6.1 Fraud Detection and Prevention

- 5.6.2 Customer Authentication and IDandV

- 5.6.3 Payments and Transaction Security

- 5.6.4 Workforce Management/Logical Access

- 5.7 By End-use Industry

- 5.7.1 Banking, Financial Services and Insurance

- 5.7.2 Government and Law Enforcement

- 5.7.3 Telecom and IT

- 5.7.4 Healthcare

- 5.7.5 Retail, E-commerce and CPG

- 5.7.6 Transport and Logistics

- 5.7.7 Others (Education, Hospitality)

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Argentina

- 5.8.2.3 Rest of South America

- 5.8.3 Europe

- 5.8.3.1 United Kingdom

- 5.8.3.2 Germany

- 5.8.3.3 France

- 5.8.3.4 Italy

- 5.8.3.5 Spain

- 5.8.3.6 Nordics

- 5.8.3.7 Rest of Europe

- 5.8.4 APAC

- 5.8.4.1 China

- 5.8.4.2 India

- 5.8.4.3 Japan

- 5.8.4.4 South Korea

- 5.8.4.5 ASEAN-5

- 5.8.4.6 Australia

- 5.8.4.7 New Zealand

- 5.8.4.8 Rest of APAC

- 5.8.5 Middle East

- 5.8.5.1 GCC

- 5.8.5.2 Turkey

- 5.8.5.3 Rest of Middle East

- 5.8.6 Africa

- 5.8.6.1 South Africa

- 5.8.6.2 Nigeria

- 5.8.6.3 Rest of Africa

- 5.8.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Nuance Communications Inc.

- 6.4.2 NICE Ltd

- 6.4.3 Verint Systems Inc.

- 6.4.4 Pindrop Security Inc.

- 6.4.5 LexisNexis Risk Solutions Inc.

- 6.4.6 LumenVox LLC

- 6.4.7 Phonexia s.r.o.

- 6.4.8 Auraya Inc.

- 6.4.9 Aculab Plc

- 6.4.10 Uniphore Software Systems

- 6.4.11 SESTEK

- 6.4.12 VoicePIN.com Sp. z o.o.

- 6.4.13 Illuma

- 6.4.14 BioCatch Ltd.

- 6.4.15 Reality Defender

- 6.4.16 Sensory Inc.

- 6.4.17 Neustar Inc.

- 6.4.18 Veridas

- 6.4.19 ID R&D Inc.

- 6.4.20 Synaptics Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment