|

시장보고서

상품코드

1851107

5G 커넥션 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)5G Connection - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

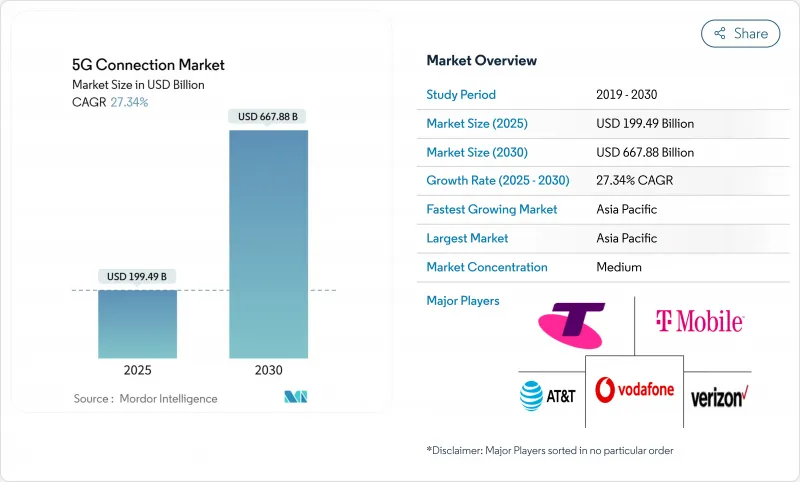

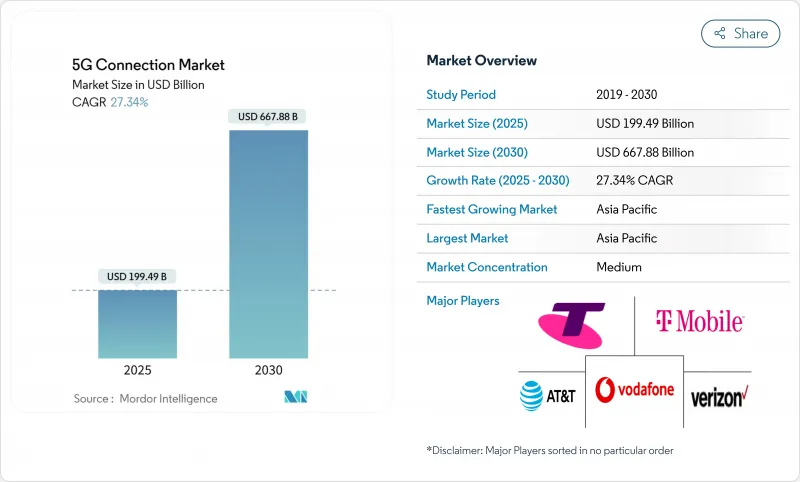

5G 커넥션 시장은 현재 1,994억 9,000만 달러의 수익을 올리고 있고, 2030년에는 6,678억 8,000만 달러에 이를 전망이며, CAGR 27.34%로 성장할 것으로 예측됩니다.

상용 전개는 커버리지 확장에서 네트워크의 고밀도화로 진행되고 있으며, 슬라이싱, 엣지 컴퓨팅, RedCap 디바이스 등 고급 기능의 급속한 도입이 가능해지고 있습니다. 아시아태평양은 중국의 440만 기지국과 인도의 전국적인 독립형 구축으로 세계 계약 수의 52%를 차지하는 반면, 북미는 고정 무선 액세스(FWA)의 보급으로 선도하고 있습니다. 통신 사업자는 비 독립형(NSA) 코어에서 독립형(SA) 코어로의 전환을 가속화하고 있습니다. SA 코어는 특히 엔터프라이즈 및 초신뢰 저지연(URLLC) 이용 사례에서 보다 높은 수익화 가능성을 이끌어내기 때문입니다. 제조, 헬스케어, 차량용 사설 5G 네트워크는 급속히 규모를 확대하고 있으며, 네트워크 API 마켓플레이스는 가까운 미래에 추가 수익원을 약속합니다. 그러나 미드밴드 주파수 대역의 가격 상승, 지방의 커버리지 경제성, 섬유의 가격 경쟁이 특정 지역에서의 성장을 계속 억제하고 있습니다.

세계의 5G 커넥션 시장 동향 및 인사이트

대용량 네트워크가 필요한 모바일 데이터 트래픽의 급증

5G 회선당 월간 데이터 사용량은 평균 70GB에 가깝고 4G의 4배에 달할 전망입니다. 중국의 5G 기지국은 440만 국으로, 이 부하에 대응하는 데 필요한 규모의 크기를 나타내고 있으며, 미드밴드 스펙트럼이 필수적인 것에 변함이 없지만, 중국 이외의 거점에서는 현재 4분의 1밖에 도입되고 있지 않습니다. 트래픽이 마이그레이션됨에 따라 통신 사업자는 커리어 어그리게이션 추가, Massive MIMO 업그레이드 및 동적 스펙트럼 공유를 선호합니다. 이러한 투자는 5G 커넥션 시장의 수익 성장을 지원하는 한편 네트워크의 에너지 효율을 최적화할 필요성을 높이고 있습니다.

고정 무선 액세스(FWA)가 광대역의 주류 대체 수단으로 상승

미국 사업자는 총 1,150만 회선의 FWA를 제공하고 있으며, 다운로드 속도의 중앙값이 200Mbps를 초과하게 되면 2028년까지 2,000만 회선에 이를 것으로 예측했습니다. 인도의 사업자는 한정적인 섬유 부설보다 비용면에서 유리한 점을 살려, 2027년까지 3,000만 명의 FWA 가입자를 목표로 하고 있습니다. Verizon은 2024년 1분기에 4억 5,200만 달러의 FWA 매출을 기록하여 단기 수익성을 보였습니다. 이러한 시장 개척을 종합하면 사용자 1인당 평균 매출액이 증가하고 5G 커넥션 시장의 대응 가능 베이스가 확대됩니다.

높은 CAPEX 및 미드밴드 주파수 대역 비용

2022-2025년 세계 인프라 투자액은 6,000억 달러 이상에 달할 것으로 예상되지만, 유럽 경매에서는 자금 조달 부담이 불균형하게 되어 SA코어를 가진 지역 통신 사업자는 중국의 80%에 비해 불과 2%에 그칩니다. 신흥 시장의 통신 사업자는 경매를 연기하고 레버리지의 상승을 완화하기 위해 타워 쉐어링을 모색합니다. 북유럽 경제의 네트워크 공유는 긍정적인 예를 보여주지만, 자본 압력은 여전히 5G 커넥션 시장으로의 완전한 진입을 억제하고 있습니다.

부문 분석

2024년 5G 커넥션 시장은 스마트폰 보급과 동영상 소비 성장에 힘입어 모바일 광대역이 62%를 차지했습니다. 동시에 M2M 및 IoT 링크는 스마트 공장, 병원 및 물류 허브에서 사설 5G 네트워크를 구축하는 데 힘입어 CAGR 28.63%로 확대될 전망입니다. 특히 미션 크리티컬 커뮤니케이션과 FWA 구독이 트래픽 증가에 기여하기 때문에 기업 경향은 네트워크 슬라이싱의 5G 커넥션 시장 규모를 크게 확대하고 있습니다. 하드웨어 벤더는 산업용 센서의 전력 소비를 줄이는 RedCap 칩셋을 발표하여 M2M 프로젝트의 실현 가능성을 가속화하고 있습니다. 엣지 네이티브 아키텍처는 실시간 분석이 경쟁력 있는 제조업에서 중요한 과제가 되기 때문에 M2M의 수익화를 더욱 촉진합니다.

셀룰러 IoT 엔드포인트의 지속적인 보급은 2028년까지 디바이스 수를 두 배로 늘릴 것으로 예상되며, 비용 최적화 모듈과 간소화된 온보딩 툴에 대한 지속적인 수요를 초래합니다. 미국의 FirstNet 확대에서 한국의 전국적인 공공 안전 네트워크에 이르기까지 미션 크리티컬 통신의 이용 사례는 서비스 차별화의 기회를 넓히고 있습니다. 그 결과 소비자 트래픽은 여전히 크고 기업 트래픽은 미래의 5G 커넥션 시장 성장에 압도적인 점유율을 얻는 새로운 균형이 확립되었습니다.

스트리밍과 게임이 모바일 광대역 트래픽을 지원하기 때문에 2024년 5G 커넥션 시장 규모에서 차지하는 소비자 이용 점유율은 76%를 유지했습니다. 그럼에도 불구하고 기업용 회선은 자동차, 헬스케어, 에너지에서 디지털 변혁의 지령에 의해 2030년까지의 CAGR이 30.47%에 이를 것으로 예측됩니다. 제조업이 두드러지는데, 1,000개가 넘는 활발한 프로젝트가 사설 5G로 전환한 후 회선 효율이 15-20% 향상되었다고 보고하고 있습니다. 싱가포르와 스웨덴 병원에서는 초저지연 비디오 링크가 통합되면 수술 시간이 단축되고 환자 결과가 향상되는 것으로 나타났습니다.

또한 스마트 시티 프로그램에서는 감시 카메라, 커넥티드 가로등, 환경 모니터가 도입되어 각각 기업 가입자 수를 늘리고 있습니다. 유틸리티 사업자는 실시간 그리드 밸런싱을 위해 5G로 눈을 돌리고, 석유 및 가스 사업자는 자동 검사 드론을 우선하고 있습니다. 이러한 추진 요인은 기업의 장기적인 수익 집중을 기울여 연결당 평균 수익을 늘리고 5G 커넥션 시장의 견고성을 높이고 있습니다.

5G 커넥션 시장 보고서는 연결 유형별(모바일 광대역, 고정 무선 액세스, 기타), 최종 사용자별(소비자, 엔터프라이즈), 스펙트럼 대역별(하위 1GHz, 1-6GHz 등), 네트워크 아키텍처별(논스탠다론, 독립형), 기기 카테고리별(스마트폰, 태블릿, FWA) CPE, 기타), 서비스 유형별(확장 모바일 광대역(eMBB), 대규모 머신 통신(mMTC) 등), 지역별로 분류됩니다.

지역 분석

아시아태평양은 2024년 세계 계약 수의 52%를 차지했으며, 2030년까지 연평균 복합 성장률(CAGR) 30.28%로 성장할 것으로 예측되고, 중국의 440만 기지국과 인도의 급속한 독립형 확대에 견인됩니다. 중국의 디지털 경제에 대한 공헌은 제조업, 소매업 및 서비스업에서 5G 플랫폼의 보급을 반영하여 2030년까지 2조 달러에 달할 것으로 보입니다. 인도의 릴라이언스 지오(Reliance Jio)는 100만 개 이상의 클라우드 네이티브 셀 사이트를 운영하고 있으며 예상 FWA 회선 수는 500만에서 2027년까지 3,000만으로 증가할 수 있습니다. 일본과 한국은 5G의 선진적인 상용 서비스를 조기에 시작함으로써 지역의 혁신 리더십을 유지하고 있으며 동남아시아에서는 2030년까지 1,300억 달러의 GDP 효과가 전망됩니다.

북미는 성숙하면서도 혁신 중심의 무대이며, 인구의 98%가 이미 5G를 이용하고 있습니다. T-모바일의 전국 SA 개발과 643만 FWA 회선은 소비자와 기업의 다양화를 보여줍니다. Verizon은 AST 스페이스 모바일과 위성 통신을 통해 제휴하여 지방에 남아 있는 격차를 메우려고 하며 캐나다와 멕시코의 통신 사업자는 RedCap 등 5G 첨단 기능을 통합하고 있습니다. 현재는 네트워크 API, 엣지 컴퓨팅, AI 지원 서비스 오케스트레이션의 수익화에 초점을 맞추고 있으며, 5G 커넥션 시장 전체에서 사이트 당 수익 밀도를 높이고 있습니다.

유럽은 엇갈린 진전을 보이고 있습니다. : 독일, 덴마크, 핀란드는 인구 커버율 95%를 넘고 있지만, SA 코어에서 가동하고 있는 계약은 불과 2%에 불과합니다. 영국의 Vodafone-Three 합병은 지방의 보급을 목표로 한 네트워크 업그레이드에 148억 6,000만 달러를 투입했으며, 북유럽의 주파수 공유 모델은 저비용으로 높은 가용성을 실현했습니다. 대륙의 통신 사업자는 현재 투자 주기를 유지하기 위해 경매의 합리화 및 라이선스료의 인하를 규제 당국에 요구하고 있어 SA 갭을 해소하고, 5G 접속 시장에서 보다 큰 가치를 끌어내려고 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 대용량 네트워크를 필요로 하는 모바일 데이터 트래픽 급증

- 광대역 대체의 주류로서 대두하는 고정 무선 액세스(FWA)

- 기업의 디지털화 및 IoT가 5G 도입 가속

- 생성형 AI 주도의 업링크 급증이 5G-SA 조기 전개 촉진

- 오픈 API 에코시스템에 의한 수익화

- 시장 성장 억제요인

- 높은 CAPEX 및 미드밴드 주파수 비용

- 농촌의 커버 경제성의 여전히 부족한 매력

- 섬유의 가격 경쟁이 도시의 FWA 보급 방해

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력 및 소비자

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 접속 유형별

- 모바일 광대역

- 고정 무선 액세스

- M2M과 IoT

- 미션 크리티컬 통신

- 사설망

- 최종 사용자별

- 소비자

- 기업

- 제조업

- 헬스케어

- 자동차 및 운송

- 스마트시티 및 공공안전

- 에너지 및 유틸리티

- 소매 및 물류

- 주파수 대역별

- 서브 1GHz(로우 밴드)

- 1-6GHz(미드 밴드)

- 24GHz 이상(밀리파/하이 밴드)

- 네트워크 아키텍처별

- 논스탠다론(NSA)

- 독립형(SA)

- 디바이스 카테고리별

- 스마트폰 및 태블릿

- FWA CPE

- IoT 모듈 및 게이트웨이

- 웨어러블 및 AR/VR 디바이스

- 산업용 라우터 및 견고 모듈

- 서비스 유형별

- 향상된 모바일 광대역(eMBB)

- 대규모 머신형 통신(mMTC)

- 초고신뢰 저지연 통신(URLLC)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 기타 남미

- 유럽

- 독일

- 프랑스

- 영국

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- AT&T Inc.

- Verizon Communications Inc.

- Vodafone Group Plc

- China Mobile Ltd.

- China Telecommunications Corp.

- T-Mobile US Inc.

- Telstra Corp. Ltd.

- Telefonica SA

- Deutsche Telekom AG

- Reliance Jio Infocomm Ltd.

- SK Telecom Co. Ltd.

- NTT Docomo Inc.

- KT Corp.

- Orange SA

- KDDI Corp.

- Bharti Airtel Ltd.

- Saudi Telecom Company(stc)

- Rakuten Mobile Inc.

- Etisalat by eand

- MTN Group Ltd.

제7장 시장 기회 및 향후 전망

AJY 25.11.12The 5G connections market currently generates USD 199.49 billion in revenue and is forecast to reach USD 667.88 billion by 2030, advancing at a 27.34% CAGR.

Commercial roll-outs have progressed from coverage expansion to network densification, enabling rapid adoption of advanced capabilities such as slicing, edge computing, and RedCap devices. Asia-Pacific accounts for 52% of global subscriptions thanks to China's 4.4 million base stations and India's nationwide standalone build-out, while North America leads in Fixed Wireless Access (FWA) penetration. Operators are accelerating the shift from non-standalone (NSA) to standalone (SA) cores as SA unlocks higher monetization potential, particularly for enterprise and ultra-reliable low-latency (URLLC) use cases. Private 5G networks in manufacturing, healthcare, and automotive are scaling quickly, and network-API marketplaces promise additional revenue streams in the near term. However, high mid-band spectrum prices, rural coverage economics, and fiber price wars continue to temper growth in selected regions.

Global 5G Connection Market Trends and Insights

Surge in mobile data traffic requiring higher-capacity networks

Monthly data usage per 5G line averages close to 70 GB-four times the 4G figure-fueled by cloud gaming and extended-reality services. China's 4.4 million 5G base stations illustrate the scale needed to carry this load, and mid-band spectrum remains vital, although only one quarter of non-Chinese sites currently deploy it. As traffic migrates, operators prioritize additional carrier aggregation, Massive MIMO upgrades, and dynamic spectrum sharing. These investments underpin revenue growth in the 5G connections market while raising the urgency to optimize network energy efficiency.

Fixed Wireless Access (FWA) emerging as mainstream broadband alternative

US operators collectively serve 11.5 million FWA lines, with projections of 20 million by 2028 as median download speeds exceed 200 Mbps. Operators in India aim for 30 million FWA subscribers by 2027 by exploiting cost advantages over limited fiber roll-outs. Verizon generated USD 452 million in Q1 2024 FWA revenue, demonstrating the format's near-term profitability. mmWave deployments increase urban capacity, and customer surveys show 44% preference for wireless home broadband. Collectively, these developments boost average revenue per user and broaden the 5G connections market addressable base.

High CAPEX and mid-band spectrum costs

Global infrastructure outlays will exceed USD 600 billion during 2022-2025, and European auctions drive disproportionate financing burdens that leave only 2% of regional operators with SA cores versus 80% in China. Emerging-market carriers postpone auctions and explore tower-sharing to mitigate rising leverage. Network sharing in Nordic economies shows positive examples, but capital pressures still curb full participation in the 5G connections market.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise digitization and IoT accelerating 5G adoption

- Generative-AI-driven uplink surge spurring early 5G-SA roll-outs

- Rural coverage economics remain unattractive

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mobile broadband accounted for 62% of the 5G connections market in 2024, underpinned by smartphone adoption and video consumption growth. At the same time, M2M and IoT links are expanding at a 28.63% CAGR, encouraged by private 5G network deployments across smart factories, hospitals, and logistics hubs. The enterprise tilt is materially increasing the 5G connections market size for network slicing, particularly as mission-critical communications and FWA subscriptions contribute incremental traffic. Hardware vendors have introduced RedCap chipsets that lower power draw for industrial sensors, accelerating M2M project viability. Edge-native architectures further catalyze M2M monetization as real-time analytics become table stakes in competitive manufacturing.

Continued proliferation of cellular IoT endpoints is projected to double device counts by 2028, creating relentless demand for cost-optimized modules and simplified onboarding tools. Mission-critical communication use cases, from FirstNet expansion in the US to nationwide public-safety networks in Korea, widen service differentiation opportunities. The resulting diversity cements a new equilibrium in which consumer traffic remains large, yet enterprise traffic captures the outsized share of future 5G connections market growth.

Consumer use retained 76% share of the 5G connections market size in 2024 as streaming and gaming sustained mobile broadband traffic. Nonetheless, enterprise lines will deliver a 30.47% CAGR through 2030, powered by digital-transformation mandates in automotive, healthcare, and energy. Manufacturing stands out: more than 1,000 active projects report 15-20% gains in line efficiency after switching to private 5G. Hospitals in Singapore and Sweden show reduced surgery times and enhanced patient outcomes once ultra-low-latency video links are integrated.

Smart-city programs are also deploying surveillance cameras, connected streetlights, and environmental monitors, each adding to the enterprise subscriber base. Utilities turn to 5G for real-time grid balancing, and oil-and-gas operators prioritize automated inspection drones. These converging drivers tilt long-term revenue concentration toward the enterprise, increasing average revenue per connection and deepening stickiness within the 5G connections market.

5G Connection Market Report is Segmented by Connection Type (Mobile Broadband, Fixed Wireless Access, and More), End-User (Consumer and Enterprise), Spectrum Band (Sub-1 GHz, 1-6 GHz, and More), Network Architecture (Non-Standalone and Standalone), Device Category (Smartphones and Tablets, FWA CPE, and More), Service Type (Enhanced Mobile Broadband (eMBB), Massive Machine-Type Communications (mMTC), and More), and Geography.

Geography Analysis

Asia-Pacific accounted for 52% of global subscriptions in 2024 and is forecast to grow at a 30.28% CAGR through 2030, led by China's 4.4 million base stations and India's rapid standalone expansion. China's digital-economy contribution is set to reach USD 2 trillion by 2030, reflecting widespread 5G platform adoption in manufacturing, retail, and services. India's Reliance Jio operates over 1 million cloud-native cell sites, while expected FWA lines could climb from 5 million to 30 million by 2027. Japan's and South Korea's early commercial 5G Advanced launches sustain regional innovation leadership, and Southeast Asia projects USD 130 billion in incremental GDP impact by 2030.

North America is a mature yet innovation-centric arena where 98% of the population already has 5G coverage. T-Mobile's nationwide SA deployment and 6.43 million FWA lines illustrate consumer and enterprise diversification. Verizon's satellite partnership with AST SpaceMobile seeks to close residual rural gaps, while Canadian and Mexican carriers integrate 5G Advanced features such as RedCap. Focus now turns to monetizing network APIs, edge compute, and AI-assisted service orchestration, driving higher revenue density per site across the 5G connections market.

Europe displays mixed progress: Germany, Denmark and Finland exceed 95% population coverage, yet only 2% of subscriptions run on SA cores. The United Kingdom's Vodafone-Three merger injects USD 14.86 billion into network upgrades aimed at rural inclusion, and Nordic spectrum-sharing models yield higher availability at lower cost. Continental operators now press regulators to streamline auctions and lower license fees to sustain investment cycles, seeking to close the SA gap and unlock greater value in the 5G connections market.

- AT&T Inc.

- Verizon Communications Inc.

- Vodafone Group Plc

- China Mobile Ltd.

- China Telecommunications Corp.

- T-Mobile US Inc.

- Telstra Corp. Ltd.

- Telefonica SA

- Deutsche Telekom AG

- Reliance Jio Infocomm Ltd.

- SK Telecom Co. Ltd.

- NTT Docomo Inc.

- KT Corp.

- Orange SA

- KDDI Corp.

- Bharti Airtel Ltd.

- Saudi Telecom Company (stc)

- Rakuten Mobile Inc.

- Etisalat by eand

- MTN Group Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in mobile data traffic requiring higher-capacity networks

- 4.2.2 Fixed Wireless Access (FWA) emerging as mainstream broadband alternative

- 4.2.3 Enterprise digitization and IoT accelerating 5G adoption

- 4.2.4 Generative-AI-driven uplink surge spurring early 5G-SA roll-outs

- 4.2.5 Monetization via Open-API ecosystems

- 4.3 Market Restraints

- 4.3.1 High CAPEX and mid-band spectrum costs

- 4.3.2 Rural coverage economics remain unattractive

- 4.3.3 Fiber price wars dampen urban FWA uptake

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Connection Type

- 5.1.1 Mobile Broadband

- 5.1.2 Fixed Wireless Access

- 5.1.3 M2M and IoT

- 5.1.4 Mission-critical Communications

- 5.1.5 Private Networks

- 5.2 By End-user

- 5.2.1 Consumer

- 5.2.2 Enterprise

- 5.2.2.1 Manufacturing

- 5.2.2.2 Healthcare

- 5.2.2.3 Automotive and Transportation

- 5.2.2.4 Smart Cities and Public Safety

- 5.2.2.5 Energy and Utilities

- 5.2.2.6 Retail and Logistics

- 5.3 By Spectrum Band

- 5.3.1 Sub-1 GHz (Low-Band)

- 5.3.2 1-6 GHz (Mid-Band)

- 5.3.3 above 24 GHz (mmWave / High-Band)

- 5.4 By Network Architecture

- 5.4.1 Non-Standalone (NSA)

- 5.4.2 Standalone (SA)

- 5.5 By Device Category

- 5.5.1 Smartphones and Tablets

- 5.5.2 FWA CPE

- 5.5.3 IoT Modules and Gateways

- 5.5.4 Wearables and AR/VR Devices

- 5.5.5 Industrial Routers and Rugged Modules

- 5.6 By Service Type

- 5.6.1 Enhanced Mobile Broadband (eMBB)

- 5.6.2 Massive Machine-Type Communications (mMTC)

- 5.6.3 Ultra-Reliable Low-Latency Communications (URLLC)

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 France

- 5.7.3.3 United Kingdom

- 5.7.3.4 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 ASEAN

- 5.7.4.6 Rest of Asia Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Saudi Arabia

- 5.7.5.1.2 UAE

- 5.7.5.1.3 Turkey

- 5.7.5.1.4 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Nigeria

- 5.7.5.2.3 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AT&T Inc.

- 6.4.2 Verizon Communications Inc.

- 6.4.3 Vodafone Group Plc

- 6.4.4 China Mobile Ltd.

- 6.4.5 China Telecommunications Corp.

- 6.4.6 T-Mobile US Inc.

- 6.4.7 Telstra Corp. Ltd.

- 6.4.8 Telefonica SA

- 6.4.9 Deutsche Telekom AG

- 6.4.10 Reliance Jio Infocomm Ltd.

- 6.4.11 SK Telecom Co. Ltd.

- 6.4.12 NTT Docomo Inc.

- 6.4.13 KT Corp.

- 6.4.14 Orange SA

- 6.4.15 KDDI Corp.

- 6.4.16 Bharti Airtel Ltd.

- 6.4.17 Saudi Telecom Company (stc)

- 6.4.18 Rakuten Mobile Inc.

- 6.4.19 Etisalat by eand

- 6.4.20 MTN Group Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment