|

시장보고서

상품코드

1851122

항공기 페어링 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Aircraft Fairings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

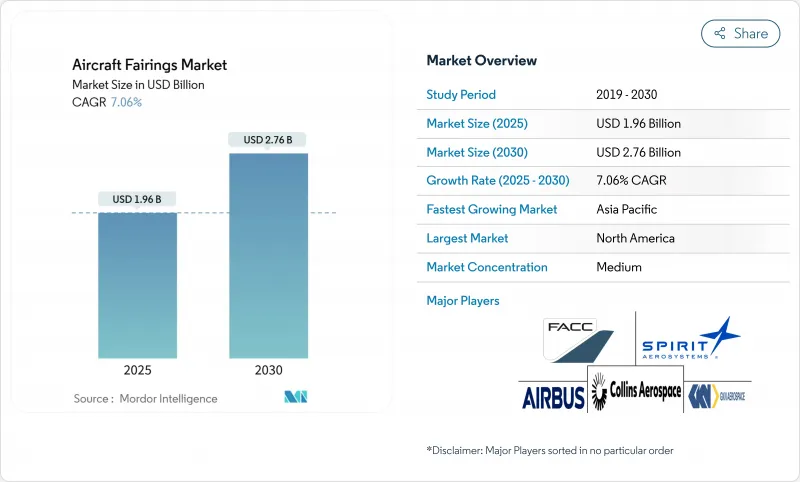

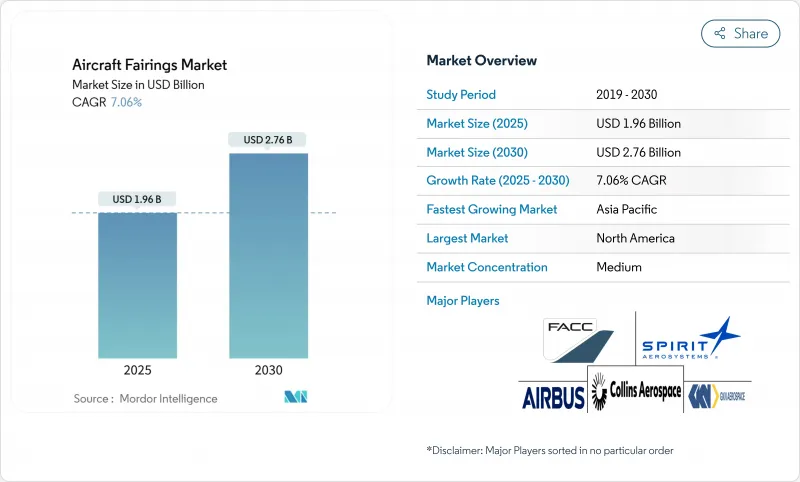

항공기 페어링 시장은 2025년에 19억 6,000만 달러, 2030년에는 27억 6,000만 달러 규모에 이를 전망이며, 예측 기간 중 CAGR은 7.06%를 나타낼 전망입니다.

1만 5,000대가 넘는 민간 제트기의 견조한 생산 준비, 연비 효율의 의무화, 노후화된 항공기의 대체 촉진의 가속이 장기적인 수요 전망을 가져오고 있습니다. 복합재료의 혁신은 이 성장 패턴의 핵심입니다. 탄소섬유 강화 중합체(CFRP)는 이미 사용중인 페어링 재료의 70%를 차지하고 있으며,이 변화는 구조 중량을 줄이고 내 부식성을 향상시킵니다. 2024년 판매량의 48%를 차지한 내로우 바디 프로그램에 대한 의존도가 높아지고 있으며, 비용을 억제하면서 생산 규모를 확대할 수 있는 공급자가 유리합니다. 한편, UAV와 eVTOL의 컨셉이 급증하고 있으며, 각각이 래피드 프로토타이핑과 소량 생산을 우선하고 있기 때문에 1대당 마진이 높은 프리미엄 틈새가 형성되고 있습니다. 그 결과 항공기 페어링 시장은 대량 생산되는 상용 프로그램과 급속히 변화하는 첨단 항공 모빌리티 수요 풀로 이분되고 있으며 공급업체는 두 분야의 용량을 헤지 할 필요가 있습니다.

세계의 항공기 페어링 시장 동향 및 인사이트

연비 목표 달성을 위한 복합재의 채용 급증

연료비 절감 압력에 노출된 항공사는 알루미늄에서 CFRP제 페어링으로 전환하고 있으며 차세대 항공기의 복합재 비율은 기존 A330의 13%에서 현재는 50% 이상으로 상승하고 있습니다. 에어버스의 다기능 동체실증기에서는 열가소성 수지의 스킨을 사용함으로써 10%의 경량화가 가능함을 보여줍니다. 복합재 페어링을 설치한 경우 평생 연료를 절약하여 항공기 구입 가격의 15-20%를 상쇄할 수 있습니다. 그러나 이러한 전환은 오토클레이브, 로봇 레이업 셀, 전문 노동력을 위해 많은 자본 지출을 필요로 하므로 진입 장벽이 높아지고 OEM은 성숙한 복합재 생태계를 소유하는 파트너를 선호하게 되었습니다.

노후된 항공기의 신속한 함대 교환

연간 700대 이상의 제트기가 퇴역해, 후부 시장을 확대하는 부품의 수확과 개수 수요를 유발합니다. 와이드 바디의 페어링은 장거리 운송의 사이클에 의해 마모가 심해져, 납품이 지연되는 가운데, 운항회사는 신조기보다 공력 업그레이드 키트를 요구하게 됩니다. 스미토모 상사와 Werner Aero사와의 제휴로 대표되는 바와 같이, 복합재 페어링을 2차 시장용으로 재생하는 서큘러 이코노미 프로그램은 지지를 모으고 있지만, CFRP의 리사이클에는 한계가 있고 비용이 많이 든다는 엄격한 현실에 직면하고 있습니다.

탄소섬유, 에폭시 수지, 고온 수지의 가격 상승과 변동이 공급자 마진을 압박

항공우주분야의 탄소섬유 수요는 매년 17% 증가할 것으로 예측되고 있지만 생산능력 증강에는 고가이고 장기적인 투자가 필요합니다. 지정학적 긴장과 관세에 대한 익스포저는 가격 예측을 복잡하게 하고, 공급업체에게 코스트 플러스 계약의 채용을 촉구하지만, 중소기업은 운전 자본을 유지할 수 없는 상황에 몰립니다.

부문 분석

동체 페어링은 2024년 항공기 페어링 시장 규모의 33.24%를 차지한 복잡한 날개와 동체의 접합 형상과 OEM 통합의 허들 높이로 인해 늘어났습니다. 설계를 변경하면 공기역학적 특성을 재시험해야 하기 때문에 기존 공급업체는 그 자리를 새기기가 어렵고 수요는 계속 침체를 겪고 있습니다. 랜딩 기어 페어링은 공항 소음 규제 강화 및 eVTOL 프로그램을 통한 격납식 스트럿 요구 사항을 뒷받침하며 CAGR 7.15%로 가속화되었습니다. 날개 몸통 페어링과 제어 표면 페어링은 주류 제조율을 따라 유지되지만, 엔진 페어링은 냉각 페어링 쉘을 의무화하는 하이브리드 전기 실증 테스트에 의한 증분 성장을 집중하고 있습니다.

새로운 모빌리티 플랫폼은 신속한 제조로 설계 브리핑을 왜곡합니다. 위치타 주립 대학의 조사에 따르면 UAV 운영자는 몇 주가 아닌 며칠 만에 인쇄 가능한 모듈식 페어링을 선호합니다. 도이체 에어크래프트사의 D328eco 계약은 동체와 착륙 장치의 문을 하나의 계약으로 정리한 것으로, 공급업체를 통합한 패키지를 목표로 하는 OEM의 움직임을 나타내고 있습니다. 이러한 번들은 광범위한 설계 도구 세트와 테스트 기사 능력을 갖춘 공급업체에게 유리합니다.

CFRP의 점유율이 63.48%인 것은 와이드 바디, 내로우 바디, 심지어 회전익기 프로그램에 이르기까지 CFRP의 지위가 확립되어 있음을 나타냅니다. 그러나 열가소성 컴포지트와 부가제조 폴리머는 연간 9.39% 성장해 오토클레이브의 병목을 해소하고 부품수의 통합을 가능하게 하여 조립노력을 삭감하고 있습니다. 경량 UAV 페어링에서는 비용에 민감한 유리 섬유를 채용하고 있지만, 손상에 강한 중요한 부위(몸통 하부의 차인 패널 등)에서는 여전히 알밀리튬 합금을 채용하고 있습니다.

헥셀의 HexAM PEKK 레이저 소결 플랫폼은 기존의 가공에 불가능한 복잡한 페어링 브래킷을 인쇄하여 스크랩과 무게를 동시에 줄입니다. EU가 자금을 지원하는 DOMMINIO의 이니셔티브는 열가소성 플라스틱 페어링에 구조 건전성 센서를 내장하여 디지털 실을 확장하고 선별 장비에 직접 지식 무결성 모니터링을 제공합니다. 결국, 라미네이트 CFRP의 표피와 인쇄된 열가소성 플라스틱의 리브를 결합하는 혼합 재료 스택은 항공기 페어링 시장을 독점할 수 있습니다.

지역 분석

북미는 2024년 항공기 페어링 시장 점유율의 36.54%를 차지하며 보잉 생산 회복과 미국 여러 주에서 복합재 생산 능력을 증강하는 GE 에어로 스페이스의 10억 달러 생산 위탁에 지지를 받았습니다. 워싱턴 주와 사우스 캐롤라이나 주에는 오랜 역사를 가진 클러스터가 있으며 공급업체에게 성숙한 생태계를 제공합니다. RTX의 20억 달러를 투자한 설비 확장은 당분간의 사업 환경이 인플레이션 기조에 있다고는 해도 OEM의 지속적 수요에 대한 신뢰를 부각하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 8.83%로 가장 급성장하고 있는 지역입니다. 중국의 C919와 인도의 HTT-40과 같은 국산화 계획은 구미 Tier-1 기업을 합작 공장으로 끌어들여 국산화의 필요성을 강화하고 있습니다. 스트라타 매뉴팩처링은 38%의 생산 증가를 기록하고, 에어버스와 보잉 모델에서 1만 1,774기의 구조체를 수출, 복합재 대국이 된다는 걸프의 야심을 보여줍니다. 한화 에어로스페이스는 GE와 롤스 로이스의 부품을 생산하는 10만 평방미터의 베트남의 신거점으로 이 변화를 더욱 실증하고 있습니다.

유럽은 에어버스 생산 템포의 혜택을 받아 녹색 소재에 주력하고 있습니다. 에어버스 헬리콥터 페어링을 위한 바이오 탄소섬유의 실현 가능성 테스트는 탄소 중립 공급망을 위한 초기 단계를 보여줍니다. 일본은 고품질 탄소섬유 공급업체로서의 틈새를 유지하고 미쓰비시화학은 미래의 모빌리티 프로그램으로 12%의 복합재 성장을 목표로 하고 있습니다. 반면 중동 및 아프리카 시장은 자유무역지역과 장거리 노선에 대한 근접성을 활용하여 OEM에서 오프셋 작업을 획득하고 있습니다. 그러나 구미의 동업 타사와 동등한 인증을 취득하는 것은 현재도 계속되고 있는 과제입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 연비 목표 달성을 향한 복합재 채용의 급증

- 노후화한 항공기의 플릿 전체에서의 급속한 갱신

- UAV, 고급 항공 기동성, eVTOL 플랫폼의 보급

- 교환용 페어링에 대한 애프터마켓 MRO 지출의 성장

- 새로운 페어링 설계에 박차를 가하는 하이브리드 전기 항공기 계획

- 기록적인 상업용 단통로의 수주 잔이 생산의 전망을 뒷받침

- 시장 성장 억제요인

- 탄소섬유, 에폭시 수지, 고온 수지의 가격 상승과 변동

- 엄격한 인증 사이클이 새로운 페어링 기술을 지연

- 공급망의 통합에 의한 조달의 선택의 감소와 이익의 축소

- 지정학적 무역 마찰과 관세가 원재료 비용 상승 촉진

- 밸류체인 분석

- 규제와 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 용도별

- 동체

- 랜딩 기어

- 날개

- 조종면

- 엔진

- 재료별

- 탄소섬유 강화 플라스틱(CFRP)

- 유리 섬유 복합재

- 금속 합금

- 열가소성 복합재료

- 적층 제조 열가소성 플라스틱

- 항공기 유형별

- 상업용

- 협폭 상용 항공기

- 광폭 상용 항공기

- 군사용

- 전투

- 비전투

- 일반 항공기

- 무인 시스템

- 상업용

- 판매 채널별

- OEM

- 애프터마켓 MRO

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Airbus Aerostructures(Airbus SE)

- Boeing Aerostructures Australia(The Boeing Company)

- Collins Aerospace(RTX Corporation)

- FACC AG

- GKN Aerospace

- Spirit AeroSystems, Inc.

- Saab AB

- Strata Manufacturing PJSC

- LATECOERE SA

- Kaman Corporation

- CTRM Sdn. Bhd.

- ShinMaywa Industries, Ltd.

- Royal Engineered Composites

- FDC Composites Inc.

제7장 시장 기회와 향후 전망

KTH 25.11.20The aircraft fairings market stands at USD 1.96 billion in 2025 and is on track to reach a market size of USD 2.76 billion by 2030, reflecting a 7.06% CAGR over the forecast horizon.

Robust production backlogs exceeding 15,000 commercial jets, rising fuel-efficiency mandates, and an accelerated push to replace aging fleets provide long-term demand visibility. Composite innovation is central to this growth pattern: carbon-fiber-reinforced polymer (CFRP) already accounts for 70% of fairing materials in service, a shift that cuts structural weight and improves corrosion resistance. Rising dependence on narrow-body programs, which contributed 48% of volumes in 2024, favors suppliers that can scale production while controlling costs. Meanwhile, the surge of UAV and eVTOL concepts-each prioritizing rapid prototyping and small-batch runs-creates premium niches that command higher margins per unit. As a result, the aircraft fairings market keeps bifurcating into high-volume commercial programs and fast-moving advanced-air-mobility demand pools, compelling suppliers to hedge capacity across both segments.

Global Aircraft Fairings Market Trends and Insights

Surging Composite Adoption to Meet Fuel-Efficiency Targets

Airlines under acute fuel-cost pressure are switching from aluminum to CFRP fairings, lifting composite content on next-generation aircraft from 13% on legacy A330s to more than 50% today. Airbus' Multifunctional Fuselage Demonstrator shows that thermoplastic skins can cut a further 10% weight while supporting automated welding for 100-per-month build rates. Economic benefits remain compelling: lifetime fuel savings can offset 15-20% of an aircraft's purchase price when installed composite fairings. Yet this transition demands heavy capital outlays for autoclaves, robotic lay-up cells, and specialized labor, heightening entry barriers and prompting OEMs to favor partners owning mature composite ecosystems

Rapid Fleet-Wide Replacement of Aging Aircraft

More than 700 jets retire yearly, triggering component harvesting and refurbishment demand that enlarges the retrofit market. Wide-body fairings see sharper wear from long-haul cycles, pushing operators toward aerodynamic upgrade kits rather than new-build orders amid delivery delays. Circular-economy programs that reclaim composite fairings for secondary markets, exemplified by Sumitomo's tie-up with Werner Aero, are gaining traction but face the hard reality that CFRP recycling is limited and cost-intensive.

High and Volatile Prices of Carbon-Fiber, Epoxy, and High-Temperature Resins Compress Supplier Margins

Carbon-fiber demand in aerospace is projected to grow 17% annually, but capacity additions require expensive, long-cycle investments. Geopolitical tension and tariff exposure complicate price forecasting, prompting suppliers to adopt cost-plus contracts yet forcing smaller firms into untenable working-capital positions.

Other drivers and restraints analyzed in the detailed report include:

- Hybrid-Electric Aircraft Programs Spur New Fairing Designs

- Record Commercial Single-Aisle Backlog Underpins Production Visibility

- Stringent Certification Cycles Delaying New Fairing Technologies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fuselage fairings generated 33.24% of the aircraft fairings market size in 2024, thanks to their complex wing-body junction geometries and high OEM integration hurdles. Demand remains sticky because any design change obliges full aerodynamic retesting, making incumbent suppliers difficult to displace. Landing-gear fairings are accelerating at 7.15% CAGR, propelled by tighter airport noise limits and eVTOL program requirements for retractable struts. Wing-body and control-surface fairings stay aligned with mainstream build rates, whereas engine fairings pick up incremental growth from hybrid-electric demonstrators that mandate cooled fairing shells.

Emerging mobility platforms skew design briefings toward rapid manufacturing. Wichita State University's research shows UAV operators prefer printable modular fairings in days, not weeks. Deutsche Aircraft's D328eco contract bundling fuselage and landing-gear doors into a single award underlines OEM moves toward integrated supplier packages. Such bundling favors vendors with broad design toolsets and test-article capacity.

CFRP's 63.48% share underscores its entrenched status across wide-body, narrow-body, and even rotorcraft programs. Yet thermoplastic composites and additively manufactured polymers-growing 9.39% annually-remove autoclave bottlenecks and enable part-count consolidation that slashes assembly labor. For lightweight UAV fairings, cost sensitivity keeps glass fiber viable, while critical damage-tolerant locations (such as lower fuselage chine panels) still rely on aluminum-lithium alloys.

Hexcel's HexAM PEKK-laser-sintering platform prints complex fairing brackets that are impossible to machine conventionally, cutting scrap and weight simultaneously. EU-funded DOMMINIO efforts extend this digital thread by embedding structural-health sensors into thermoplastic fairings, bringing predictive integrity monitoring directly to line-fit installations. Over time, blended material stacks that mate laminated CFRP skins to printed thermoplastic ribs could dominate the aircraft fairings market.

The Aircraft Fairings Market Report is Segmented by Application (Fuselage, Landing Gear, Wings, Control Surfaces, and Engine), Material (Glass-Fiber Composites, Metal Alloys, Thermoplastic Composites, and More), Aircraft Type (Commercial, Military, and More), Sales Channel (OEM Production and Aftermarket MRO), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 36.54% of the aircraft fairings market share in 2024, supported by Boeing's production recovery and a USD 1 billion GE Aerospace manufacturing commitment that boosts composite capacity in multiple US states. Long-established clusters in Washington and South Carolina give suppliers a mature ecosystem, although tariff policies and skilled-labor gaps continue to strain cost bases. RTX's USD 2 billion facilities expansion highlights OEM faith in sustained demand even as the near-term operating environment remains inflationary.

Asia-Pacific is the fastest-growing region, showing 8.83% CAGR to 2030. Indigenous programs such as China's C919 or India's HTT-40 intensify localization mandates, drawing Western tier-1s into joint-venture factories. Strata Manufacturing recorded 38% output growth, exporting 11,774 structures across Airbus and Boeing models, signaling the Gulf's ambition to become a composites powerhouse. Hanwha Aerospace's new 100,000 m2 Vietnam site for GE and Rolls-Royce components further validates the shift.

Europe benefits from Airbus' production tempo and focuses on green materials. Airbus' bio-based carbon-fiber feasibility trials for helicopter fairings mark early steps toward carbon-neutral supply chains. Japan preserves a niche as a high-grade carbon-fiber supplier, with Mitsubishi Chemical targeting 12% composite growth on future mobility programs. Meanwhile, Middle East and Africa markets leverage free-trade zones and proximity to long-haul routes to win offset work from OEMs. However, achieving certification parity with Western peers remains an ongoing task.

- Airbus Aerostructures (Airbus SE)

- Boeing Aerostructures Australia (The Boeing Company)

- Collins Aerospace (RTX Corporation)

- FACC AG

- GKN Aerospace

- Spirit AeroSystems, Inc.

- Saab AB

- Strata Manufacturing PJSC

- LATECOERE S.A

- Kaman Corporation

- CTRM Sdn. Bhd.

- ShinMaywa Industries, Ltd.

- Royal Engineered Composites

- FDC Composites Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging composite adoption to meet fuel-efficiency targets

- 4.2.2 Rapid fleet-wide replacement of aging aircraft

- 4.2.3 Proliferation of UAV, advanced air mobility, and eVTOL platforms

- 4.2.4 Growth of aftermarket MRO expenditure on replacement fairings

- 4.2.5 Hybrid-electric aircraft programs spur new fairing designs

- 4.2.6 Record commercial single-aisle backlog underpins production visibility

- 4.3 Market Restraints

- 4.3.1 High and volatile prices of carbon fiber, epoxy, and high-temperature resins

- 4.3.2 Stringent certification cycles delaying new fairing technologies

- 4.3.3 Supply-chain consolidation reducing sourcing optionality and compressing margins

- 4.3.4 Geopolitical trade tensions and tariffs inflating raw-material costs

- 4.4 Value Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Fuselage

- 5.1.2 Landing Gear

- 5.1.3 Wings

- 5.1.4 Control Surfaces

- 5.1.5 Engine

- 5.2 By Material

- 5.2.1 Carbon-Fiber Reinforced Polymer (CFRP)

- 5.2.2 Glass-Fiber Composites

- 5.2.3 Metal Alloys

- 5.2.4 Thermoplastic Composites

- 5.2.5 Additively-Manufactured Thermoplastics

- 5.3 By Aircraft Type

- 5.3.1 Commercial

- 5.3.1.1 Narrow-Body Commercial Aircraft

- 5.3.1.2 Wide-Body Commercial Aircraft

- 5.3.2 Military

- 5.3.2.1 Combat

- 5.3.2.2 Non-Combat

- 5.3.3 General Aviation

- 5.3.4 Unmanned Systems

- 5.3.1 Commercial

- 5.4 By Sales Channel

- 5.4.1 OEM Production

- 5.4.2 Aftermarket MRO

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Airbus Aerostructures (Airbus SE)

- 6.4.2 Boeing Aerostructures Australia (The Boeing Company)

- 6.4.3 Collins Aerospace (RTX Corporation)

- 6.4.4 FACC AG

- 6.4.5 GKN Aerospace

- 6.4.6 Spirit AeroSystems, Inc.

- 6.4.7 Saab AB

- 6.4.8 Strata Manufacturing PJSC

- 6.4.9 LATECOERE S.A

- 6.4.10 Kaman Corporation

- 6.4.11 CTRM Sdn. Bhd.

- 6.4.12 ShinMaywa Industries, Ltd.

- 6.4.13 Royal Engineered Composites

- 6.4.14 FDC Composites Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment