|

시장보고서

상품코드

1851133

디지털 인쇄 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Digital Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

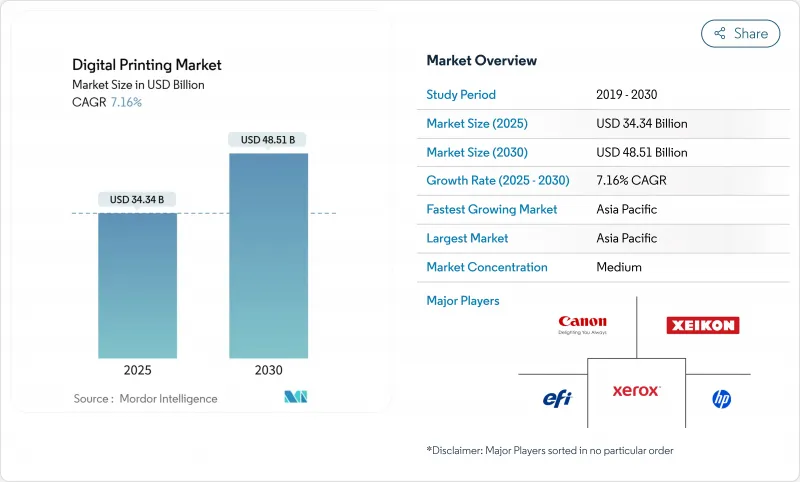

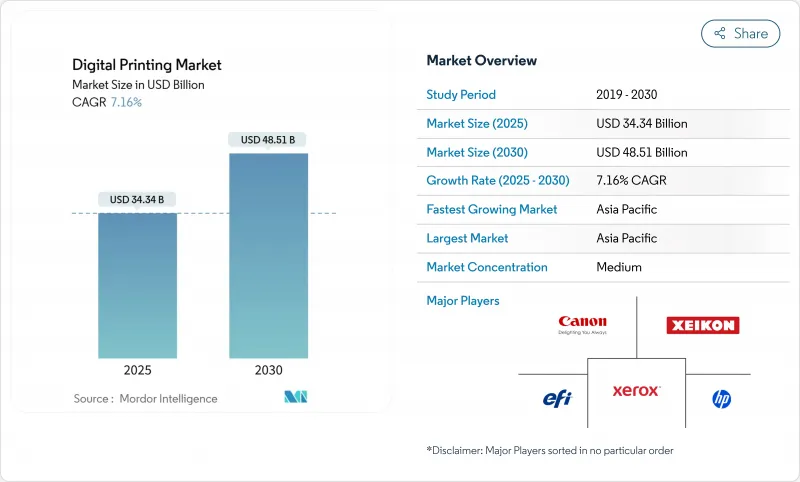

디지털 인쇄 시장 규모는 2025년에 343억 4,000만 달러, 2030년에는 485억 1,000만 달러에 이르며, 2025-2030년 CAGR은 7.16%를 나타낼 것으로 예측됩니다.

온디맨드 생산, AI 주도 워크플로우 오케스트레이션, 아날로그에서 디지털 제조로의 축족 발에 대한 견조한 수요는 공급망이 불안정한 상태라도 성장을 지속시킵니다. 시장의 매력은 마이크로 배치 생산으로 이익을 올리고 제판의 지연을 없애고 납기를 단축할 수 있어 대규모 매스 커스터마이제이션을 요구하는 컨버터나 브랜드 오너를 끌어들이고 있습니다. 휘발성 유기 화합물 및 PFAS에 대한 규제 감시가 수성 안료 및 UV 경화형 화학물질로의 전환을 가속화하는 한편, 드롭 온 디맨드 프린트 헤드의 진보가 해상도, 속도, 기재의 다양성의 최전선을 밀어 올리고 있습니다. 경쟁 전략은 내양자성 보안 모듈, 자율적 유지보수 알고리즘 및 자본 비용을 분산시키기 위한 R&D 자산을 모으는 파트너십을 중심으로 전개됩니다. 이러한 요인들이 결합되어 포장, 섬유, 산업, 상업, 장식 등의 분야에서 시장 세분화의 밑단이 확산되고 있습니다.

세계의 디지털 인쇄 시장 동향과 인사이트

짧은 실행 사용자 정의 포장 수요 증가

식품, 음료, 퍼스널케어 등의 브랜드 오너는 한정판 릴리스나 지역 고유의 라벨링 요건에 대응하기 때문에 1만개 이하의 로트 사이즈를 요구하는 케이스가 늘고 있습니다. HP Indigo 200K 인쇄기를 활용하는 컨버터는 리드 타임과 재고 위험을 줄이는 판 프리 전환을 실현하여 디지털 인쇄 시장을 민첩한 공급망에 필수적인 것으로 바꾸고 있습니다. 전자상거래의 성장은 SKU의 복잡성을 증가시키고 인쇄회사를 다운타임 없이 기재나 상자의 형식을 전환하는 워크플로우 구성으로 밀어 올리고 있습니다. 소매업체는 또한 추적 및 위조 방지 코딩을 위한 가변 데이터를 중요시하고 있으며, 이러한 기능은 도구를 추가하지 않고 인라인으로 수행됩니다. 이러한 장점은 계절 및 판촉 사이클이 격렬해질 때마다 디지털 워크플로우 선호도를 강화합니다.

마이크로 배치 주문을 위한 신속한 AI 대응 워크플로우 자동화

HP의 Nio AI 에이전트는 잉크의 레이다운, 노즐의 건전성, 기판의 전진을 실시간으로 최적화하여 변화를 통한 무인 운전과 예측 가능한 컬러를 가능하게 합니다. AI 주도의 직업 도박을 도입하고 있는 일본의 시설에서는 셋업 시트가 30% 삭감되어 가동 시간이 2 자리수 향상했습니다. 예지 보전 모델은 몇 주 전에 헤드 교체를 예측하고 예기치 않은 중단을 방지하고 까다로운 포장 계정의 품질을 안정시킵니다. 머신러닝은 또한 기판 당 ICC 프로파일을 정제하여 고급 호일과 합성수지 낭비를 줄입니다. AI는 노동 투입과 재료 오버런을 줄임으로써 마이크로볼륨층에서도 이익 풀을 확대하고, 중소 컨버터가 액세스 가능한 디지털 인쇄 시장을 확대합니다.

하이엔드 프레스를 위한 고액의 설비투자 및 연구개발비

다층 와니스와 백색 잉크를 지원하는 산업용 잉크젯 라인은 1대당 100만 달러를 초과하는 것이 일반적입니다. 공조실, 인라인 검사 카메라, RIP 서버 등을 포함하면 초기 비용이 더욱 부풀어지고, 중소의 컨버터는 최고 레벨의 스루풋으로부터 체결되어 버립니다. 급속한 진부화도 위험을 증가시킵니다. 헤드 제너레이션은 5년 이내에 새로 고쳐지기 때문에 지속적인 자본 투자를 강요하거나 금리가 줄어들 위험이 있습니다. 주요 그룹은 신디케이트 대출과 공유 서비스 센터를 통해 업그레이드 자금을 조달하고 기술 격차를 넓히고 있습니다. 이렇게 하면 통합이 가속화되고 공급자 커브의 꼬리가 깎여져 자금력 있는 기업에 볼륨이 집중됩니다.

부문 분석

잉크젯 기술은 2024년 디지털 인쇄 시장 점유율의 68.12%를 차지했고, 2030년까지의 CAGR은 11.7%를 나타낼 것으로 예측됩니다. 이 부문의 리더십은 이전보다 작은 액적량, 네이티브 1,200dpi 헤드, 다공성 및 비 다공성 미디어에 관계없이 밴딩을 줄이는 폐쇄 루프 메니스커스 컨트롤에 기인합니다. 전자사진 방식은 토너의 광택 마무리가 매력적인 오피스 문서나 사진집용의 관련성을 유지하고 있지만, 토너 정착에 의해 기재의 다양성과 에너지 효율이 제한되기 때문에 그 채용은 두드러지고 있습니다.

엡손의 Direct-to-Shape 시스템은 6축 로보틱스와 PrecisionCore 헤드를 결합하여 곡면 플라스틱이나 유리에서 35μm 이내의 정확도를 가능하게 합니다. 이 3D 물체로의 확장은 자동차 노브에서 음료 텀블러에 이르기까지 대응가능한 용도의 폭을 넓히고, 이 부문의 디지털 인쇄 시장 전체의 성장에 기여할 수 있도록 합니다. 잉크젯은 또한 다가오는 용제 금지에 대응하는 수성 안료 세트와의 조합이 용이하며, 컨버터의 설비 투자를 앞으로도 지원합니다. 파형이 점도 변동에 동적으로 적응하기 때문에 가동 시간이 연장되고 프린트 헤드의 수명이 연장됩니다.

용제계는 비닐 배너나 차량용 랩에 대한 강력한 점착성으로 2024년 매출의 49.43%를 차지했습니다. 그러나 수성 안료 시스템은 실내 그래픽과 식품 포장에서 낮은 VOC가 지지되어 CAGR 9.34%로 상승하고 있습니다. UV 경화형 잉크는 즉각적인 경화로 대기 시간과 노력을 줄일 수 있는 접이식 판지와 직접 투 오브젝트 분야에서 점유율을 확대하고, 라텍스 블렌드는 그린 프로파일과 옥외 내구성의 균형을 맞추고 있습니다.

잉크 제조업체는 PFAS와 방향족 탄화수소를 제거하기 위한 R&D 사이클을 가속화하고, Mimaki의 2025년 UV 세트는 CMR 프리 케미스트리로가는 길을 보여줍니다. 인증기관이 보다 엄격한 마이그레이션 임계값을 부과하는 동안 솔벤트 플랫폼은 재인증이 필요하며 역사적 이점에도 불구하고 양적 확장이 억제됩니다. 반대로, 수성 안료는 인라인 건조기나 고도의 프라이머에 의해 한때는 손이 닿지 않는 것으로 생각되었던 플라스틱이나 금속화 필름을 개방함으로써 이익을 얻는다. 예측 기간 동안 수성 잉크의 디지털 인쇄 시장 규모는 기존의 솔벤트 라인과의 차이를 줄이고 공급업체의 세력 다이어그램과 조달 전략을 재구성할 것으로 예측됩니다.

디지털 인쇄 시장 보고서는 인쇄 공정(전자 사진, 잉크젯), 잉크 유형(수성 안료, 용제, UV 경화형, 기타), 기재(종이 및 판지, 플라스틱·필름, 섬유·패브릭, 기타), 용도(책·출판, 상업 인쇄, 포장, 기타), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)으로 구분됩니다.

지역 분석

아시아태평양은 2024년 세계 매출의 38.56%를 차지했으며 인더스트리 4.0과 부가제조 생태계를 지원하는 국가 인센티브로 2030년까지 연평균 복합 성장률(CAGR)이 10.88%를 나타낼 전망입니다. 고가치 수출을 추진하는 중국은 고급 소비재용으로 가변 데이터와 화려한 장식을 제공하는 라벨·카톤 라인에 자본을 돌려보냅니다. 일본은 인쇄기를 MES 및 ERP 스택과 동기화하고 공장 클러스터 전체의 작업 시퀀싱을 최적화하는 AI를 통합한 워크플로우를 육성하고 있습니다. 인도의 급성장하는 중산계급이 연포장 수요를 견인해, 턴키 디지털 허브로 현지 인테그레이터와 제휴하는 세계 OEM을 끌고 있습니다.

북미는 성숙하지만 유리한 분야이며, 컨버터는 클럽 스토어 및 전자상거래 포장에서 SKU의 급증에 대응하기 때문에 오랜 시간의 플렉소에서 민첩한 디지털 라인으로 축족을 옮기고 있습니다. 미국은 브랜드 자산과 소비자 데이터를 보호하는 내양자 프린터 보안의 채택으로 선진하고 있습니다. 캐나다는 탄소의 투명성을 중시하는 규제를 통해 수성 잉크와 클로즈드 루프의 컬러 캘리브레이션으로의 전환을 추진하고, 멕시코는 니어 쇼어링에 의해 지금까지 아시아용이었던 어셈블리를 지역별 인쇄가 필요한 지역의 필필먼트 센터로 라우팅함으로써 이익을 얻고 있습니다.

유럽에서는 EU 그린 거래 하에서 지속가능성과 순환 경제에 대한 적합성이 중요합니다. 텍스타일 및 포장 디지털 제품 여권에는 아이템 레벨 인코딩이 필요하지만, 이 기능은 고해상도 잉크젯 라인에 자연스럽게 통합되어 있습니다. 독일의 기계공학 기반은 인쇄 모듈을 로봇화된 마감 셀에 통합하고 프랑스의 고급 제품 부문은 엄격한 특색 재현과 촉감이 좋은 니스 효과를 요구합니다. 영국은 크리에이티브 산업의 특주 한정 인쇄에 대한 수요를 개척해 중소기업에 컴팩트한 B2 잉크젯 유닛의 구입을 촉구하고 있습니다. 이러한 지역 역학을 종합하면 디지털 인쇄 시장은 세계의 차세대 제조업의 초석으로 강화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 활황을 나타내는 쇼트 런 커스터마이즈 포장 수요

- 마이크로 배치 주문을 위한 신속한 AI 대응 워크플로우 자동화

- EU와 미국의 디지털 섬유 마이크로팩토리 확대

- 인쇄 단가의 저하와 단납기화

- 시장 성장 억제요인

- 하이엔드 인쇄기를 위한 고액의 설비 투자와 RandD 지출

- PFAS/솔벤트 잉크 규제 강화가 재인증의 지연 촉진

- 공급망 분석

- 규제 전망

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 인쇄 프로세스별

- 전기 사진법(토너)

- 잉크젯

- 잉크 유형별

- 수성 안료

- 용제

- UV 경화형

- 라텍스

- 염료 승화

- 기판별

- 종이 및 판지

- 플라스틱 및 필름

- 섬유/직물

- 유리 및 세라믹

- 금속

- 용도별

- 도서 및 출판

- 상업 인쇄

- 포장

- 라벨

- 골판지 포장

- 판지 상자

- 연성 포장

- 경질 플라스틱 포장

- 금속 포장

- 섬유 인쇄

- 사진 및 상품 인쇄

- 간판 및 대형 그래픽

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 폴란드

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 케냐

- 나이지리아

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- HP Inc.

- Canon Inc.

- Xerox Holdings

- Ricoh Company

- Electronics For Imaging(EFI)

- Konica Minolta

- Xeikon NV

- Smurfit WestRock

- Mondi PLC

- DS Smith PLC(International Paper)

- Amcor PLC

- Multi-Color Corporation

- Avery Dennison Corporation

- Quad/Graphics Inc.

- Durst Phototechnik

- Landa Digital Printing

- Domino Printing Sciences

- Screen Holdings Co.

- Fujifilm Holdings

제7장 시장 기회와 향후 전망

KTH 25.11.20The digital printing market size is valued at USD 34.34 billion in 2025 and is forecast to reach USD 48.51 billion by 2030, advancing at a 7.16% CAGR over 2025-2030.

Robust demand for on-demand production, AI-driven workflow orchestration, and the pivot from analog to digital manufacturing keep growth resilient even as supply chains remain volatile. The market's capability to profitably execute micro-batch runs, eliminate plate-making delays, and shorten turnaround times attracts converters and brand owners seeking mass customization at scale. Regulatory scrutiny of volatile organic compounds and PFAS accelerates migration toward water-based pigment and UV-curable chemistries, while advances in drop-on-demand printheads push resolution, speed, and substrate versatility frontiers. Competitive strategies increasingly revolve around quantum-resistant security modules, autonomous maintenance algorithms, and partnerships that pool R&D assets to spread capital costs. These factors collectively widen the addressable base for the digital printing market across packaging, textile, industrial, commercial, and decor segments.

Global Digital Printing Market Trends and Insights

Booming Short-Run Customized Packaging Demand

Brand owners in food, beverage, and personal care increasingly request lot sizes below 10,000 units to support limited-edition releases and region-specific labeling requirements. Converters leveraging HP Indigo 200K presses achieve plate-free changeovers that slash lead times and inventory risk, transforming the digital printing market into a vital enabler of agile supply chains. E-commerce's growth multiplies SKU complexity, pushing printers toward workflow configurations that switch substrates and box formats without downtime. Retailers also value variable data for track-and-trace and anti-counterfeit coding, functions executed inline with no added tooling. These advantages reinforce the preference for digital workflows whenever seasonal or promotional cycles intensify.

Rapid AI-Enabled Workflow Automation for Micro-Batch Orders

HP's Nio AI agent optimizes ink laydown, nozzle health, and substrate advance in real time, enabling unattended operation and predictable color across shifts. Japanese facilities implementing AI-driven job ganging now see 30% fewer setup sheets and double-digit uptime gains. Predictive maintenance models forecast head replacements weeks in advance, preventing unplanned stops and stabilizing quality for demanding packaging accounts. Machine learning also refines ICC profiles per substrate, reducing waste on premium foils and synthetics. By collapsing labor inputs and materials overruns, AI broadens profit pools even at micro-volume tiers, enlarging the accessible digital printing market for SME converters.

High Capex and R&D Outlays for High-End Presses

Industrial inkjet lines capable of multi-layer varnish and white ink routinely exceed USD 1 million per unit. Initial spend escalates when climate-controlled rooms, inline inspection cameras, and RIP servers are included, locking smaller converters out of top-tier throughput. Rapid obsolescence compounds risk; head generations refresh within five-year windows, forcing continuous capex or risk margin erosion. Larger groups finance upgrades via syndicated loans and shared service centers, widening the technology gap. Consolidation thus accelerates, trimming the tail of the provider curve and concentrating volume among well-funded players.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Digital Textile Micro-Factories in EU and US

- Declining Per-Unit Print Cost and Faster Turnaround

- Stricter PFAS/Solvent-Ink Regulations Causing Re-Qualification Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Inkjet technology commanded 68.12% of the digital printing market share in 2024 and is projected to grow at 11.7% CAGR through 2030. The segment's leadership stems from ever-smaller drop volumes, native 1,200 dpi heads, and closed-loop meniscus control that reduce banding on porous and non-porous media alike. Electrophotography maintains relevance for office documents and photo books where toner's gloss finish appeals, yet its adoption plateaus because toner fusing limits substrate diversity and energy efficiency.

Epson's Direct-to-Shape system mates six-axis robotics with PrecisionCore heads, enabling registration accuracy within 35 µm on curved plastics and glass. This expansion into 3-D objects broadens addressable applications from automotive knobs to beverage tumblers, reinforcing the segment's contribution to overall digital printing market growth. Inkjet also pairs readily with water-based pigment sets that comply with looming solvent bans, future-proofing capex for converters. As waveforms adapt dynamically to viscosity fluctuations, uptime rises and printhead life extends, counteracting historical consumables cost concerns and deepening inkjet's entrenchment.

Solvent formulations delivered 49.43% revenue in 2024 thanks to robust adhesion on vinyl banners and fleet wraps. Yet water-based pigment systems are climbing at a 9.34% CAGR as buyers favor low-VOC credentials for indoor graphics and food packaging. UV-curable inks carve share in folding carton and direct-to-object arenas where instant curing curtails wait times and labor, while latex blends balance green profile with outdoor durability.

Ink makers accelerate R&D cycles to purge PFAS and aromatic hydrocarbons; Mimaki's 2025 UV sets show the path toward CMR-free chemistry. As certification bodies impose stricter migration thresholds, solvent platforms must re-qualify, dampening volume expansion despite historical dominance. Conversely, aqueous pigments gain from inline dryers and advanced primers that open plastics and metalized films once considered out-of-reach. Over the forecast period, the digital printing market size for water-based inks is expected to close the gap with legacy solvent lines, reshaping supplier power dynamics and procurement strategies.

The Digital Printing Market Report is Segmented by Printing Process (Electrophotography, and Inkjet), Ink Type (Water-Based Pigment, Solvent, UV-Curable and More), Substrate (Paper and Paperboard, Plastics and Films, Textiles/Fabrics and More), Application (Books and Publishing, Commercial Printing, Packaging and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa).

Geography Analysis

Asia-Pacific retained 38.56% share of global revenue in 2024 and is set to post the highest 10.88% CAGR through 2030 thanks to state incentives supporting Industry 4.0 and additive manufacturing ecosystems. China's push toward high-value exports channels capital into label and carton lines that deliver variable data and colorful embellishments for premium consumer goods. Japan nurtures AI-infused workflows that synchronize presses with MES and ERP stacks, optimizing job sequencing across factory clusters. India's fast-growing middle class drives flexible packaging demand, attracting global OEMs to partner with local integrators on turnkey digital hubs.

North America represents a mature but lucrative arena where converters pivot from long-run flexo to agile digital lines to satisfy SKU proliferation in club stores and e-commerce packaging. The United States spearheads adoption of quantum-resistant printer security that shields brand assets and consumer data. Canada's regulatory focus on carbon transparency propels migration toward water-based inks and closed-loop color calibration, while Mexico benefits from near-shoring that routes previously Asia-bound assemblies through regional fulfillment centers requiring localized print.

Europe emphasizes sustainability and circular-economy compliance under the EU Green Deal. The Digital Product Passport for textiles and packaging necessitates item-level encoding, a function naturally embedded within high-resolution inkjet lines. Germany's mechanical engineering base integrates print modules into robotized finishing cells, while France's luxury sector insists on exacting spot-color reproduction and tactile varnish effects. The United Kingdom exploits creative industries' demand for bespoke limited-run prints, encouraging SMEs to buy compact B2 inkjet units. Collectively, these regional dynamics reinforce the digital printing market as a cornerstone of next-generation manufacturing worldwide.

- HP Inc.

- Canon Inc.

- Xerox Holdings

- Ricoh Company

- Electronics For Imaging (EFI)

- Konica Minolta

- Xeikon NV

- Smurfit WestRock

- Mondi PLC

- DS Smith PLC (International Paper)

- Amcor PLC

- Multi-Color Corporation

- Avery Dennison Corporation

- Quad/Graphics Inc.

- Durst Phototechnik

- Landa Digital Printing

- Domino Printing Sciences

- Screen Holdings Co.

- Fujifilm Holdings

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Booming short-run customised packaging demand

- 4.2.2 Rapid AI-enabled workflow automation for micro-batch orders (under-the-radar)

- 4.2.3 Expansion of digital textile micro-factories in EU and US (under-the-radar)

- 4.2.4 Declining per-unit print cost and faster turnaround

- 4.3 Market Restraints

- 4.3.1 High capex and RandD outlays for high-end presses

- 4.3.2 Stricter PFAS/solvent-ink regulations causing re-qualification delays (under-the-radar)

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Printing Process

- 5.1.1 Electrophotography (Toner)

- 5.1.2 Inkjet

- 5.2 By Ink Type

- 5.2.1 Water-based pigment

- 5.2.2 Solvent

- 5.2.3 UV-curable

- 5.2.4 Latex

- 5.2.5 Dye-Sublimation

- 5.3 By Substrate

- 5.3.1 Paper and Paperboard

- 5.3.2 Plastics and Films

- 5.3.3 Textiles/Fabrics

- 5.3.4 Glass and Ceramics

- 5.3.5 Metals

- 5.4 By Application

- 5.4.1 Books and Publishing

- 5.4.2 Commercial Printing

- 5.4.3 Packaging

- 5.4.3.1 Labels

- 5.4.3.2 Corrugated Packaging

- 5.4.3.3 Cartons

- 5.4.3.4 Flexible Packaging

- 5.4.3.5 Rigid Plastic Packaging

- 5.4.3.6 Metal Packaging

- 5.4.4 Textile Printing

- 5.4.5 Photographic and Merchandise

- 5.4.6 Signage and Large-Format Graphics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Russia

- 5.5.2.9 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Kenya

- 5.5.4.2.3 Nigeria

- 5.5.4.2.4 Rest of Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 HP Inc.

- 6.4.2 Canon Inc.

- 6.4.3 Xerox Holdings

- 6.4.4 Ricoh Company

- 6.4.5 Electronics For Imaging (EFI)

- 6.4.6 Konica Minolta

- 6.4.7 Xeikon NV

- 6.4.8 Smurfit WestRock

- 6.4.9 Mondi PLC

- 6.4.10 DS Smith PLC (International Paper)

- 6.4.11 Amcor PLC

- 6.4.12 Multi-Color Corporation

- 6.4.13 Avery Dennison Corporation

- 6.4.14 Quad/Graphics Inc.

- 6.4.15 Durst Phototechnik

- 6.4.16 Landa Digital Printing

- 6.4.17 Domino Printing Sciences

- 6.4.18 Screen Holdings Co.

- 6.4.19 Fujifilm Holdings

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment