|

시장보고서

상품코드

1851136

박막 봉지 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년) |

||||||

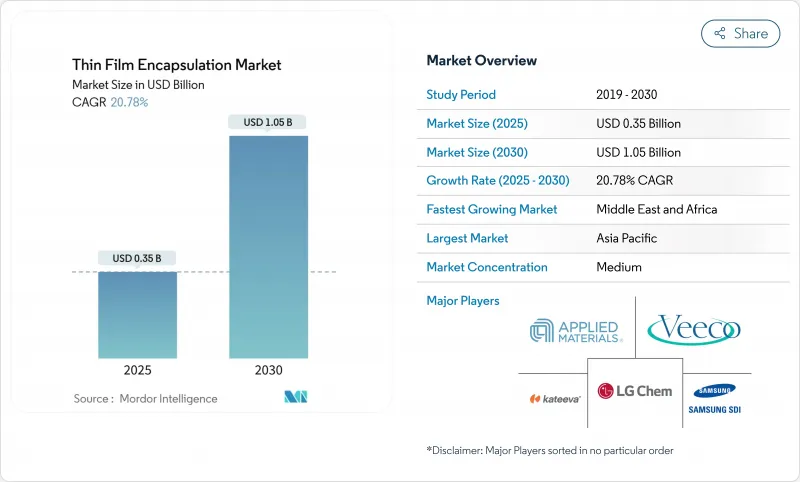

박막 봉지 시장 규모는 2025년 3억 5,000만 달러, 2030년 10억 5,000만 달러에 이를 것으로 예상되며, CAGR은 20.78%를 나타낼 전망입니다.

유연한 OLED 디스플레이의 급속한 채용, 접을 수 있는 소비자 디바이스 수요 급증, 아시아태평양의 적극적인 생산 능력 증강으로 성장 궤도가 급경사를 유지하고 있습니다. 제조업체는 10-6 g/m2/day 이하의 수증기 투과율을 달성하는 원자층 증착(ALD) 장벽을 선호하고 있어 폼 팩터의 유연성을 유지하면서 디바이스의 장수명화를 가능하게 하고 있습니다. 프리커서 부족과 자본 집약적인 6세대 ALD 라인이 역풍이 되는 가운데서도, 곡면 콕핏 디스플레이의 자동차 의무화와 롤 to 롤 ALD 필름의 의료 인증은 응용 범위를 넓히고 있습니다. '뉴디스플레이' 보조금에 추진된 중국 기업들이 생산량을 확대하고 한국의 우위를 침식하고 있기 때문에 경쟁의 치열성이 커지고 있습니다.

세계의 박막 봉지 시장 동향과 인사이트

한국과 중국의 AMOLED 생산능력 확대가 ALD-TFE 장비 수주 촉진

삼성디스플레이는 2026년 생산을 목표로 하는 8.6세대 IT OLED 라인에 30억 달러를 할당, BOE는 동등한 공장에 87억 달러를 할당했습니다. 이 프로젝트는 ALD 밀봉 도구의 구매 주문을 증가 시켰습니다. 이 기술은 차세대 IT 및 자동차 패널에 필요한 저온, 균일하고 핀홀이 없는 장벽을 제공하기 때문입니다. 경쟁의 격화는 한국의 출하 주도권을 부활시켰지만 동시에 아시아태평양 주조소 전체의 ALD 수요를 확대시켰습니다.

EU와 북미에서 자동차용 곡면 디스플레이의 의무화

완벽한 계기 클러스터를 권장하는 규제 지침은 곡면 OLED 대시보드 디자인 인을 가속화합니다. 이 모듈에는 진동, 자외선 조사 및 -40°C 사이클을 견딜 수있는 밀봉 스택이 필요합니다. 삼성이 고도의 방습 배리어를 갖춘 탠덤 OLED를 채용한 것은 이 변화를 상징하는 것으로, 2026년까지 차재 디스플레이의 총 비용이 모니터 패널의 매출을 몰아낼 것으로 예측되는 가운데, 회사는 수익을 얻는 입장에 있습니다.

6세대 ALD 클러스터 라인의 고액 설비 투자

차세대 ALD 스택은 라인당 미화 1억 달러 이상의 설비 투자를 필요로 하기 때문에 중견업체는 존경받고 기술의 보급이 늦어지고 있습니다. 아시아의 많은 팹은 여전히 오래된 클러스터 도구를 상각하고 있기 때문에 수율의 이점이 분명하더라도 업그레이드의 경제성이 복잡해지고 있습니다. 이 비용 장벽은 박막 봉지 시장 전체에서 동급 최고의 캡슐화의 균일한 채택을 늦추고 있습니다.

부문 분석

ALD는 26.4%의 연평균 복합 성장률(CAGR)을 기록했지만, PECVD는 2024년에 39.3%의 매출을 기록해 박막 봉지 시장의 이행기를 나타냈습니다. ALD 막의 수증기량은 10-6g/m2/day에 이르고 OLED의 수명을 연장하고 접을 수 있는 기판을 지원합니다. 롤 투 롤 ALD는 처리량을 웨어러블 생산에 적합한 웹 속도로 향상시키고 공간 ALD는 기판 크기의 한계를 극복하고 있습니다. PECVD는 여전히 대량 생산이 필요한 리지드 패널에 선호됩니다. VTE와 OVPD는 재료의 호환성이 장벽의 극한성보다 우선하는 틈새 발광 스택에서 계속됩니다. 2023년 SID에서 수여한 저온 ALD 화학은 대량 폴 더블용 폴리이미드 기판을 개발하여 기술 믹스를 심화시켰습니다. 그 결과 ALD 도구 제공업체는 기록적인 수주 잔여를 즐길 수 있어 한국, 중국, 미국의 각 지역에서 공급업체의 생태계가 강화되었습니다.

박막 봉지 시장은 레거시 TFT 라인과 원활하게 통합할 수 있는 반응기이기 때문에 비용에 중점을 둔 SKU는 PECVD에 의존하고 있습니다. Kateeva가 선명하게 한 잉크젯 봉지 인쇄는 유기 재료의 폐기를 줄이고 스마트 시계의 다이얼을위한 패터닝 된 장벽을 가능하게했습니다. VTE는 디바이스 수율이 처리량보다 우선하는 작은 영역의 마이크로 디스플레이에 중요합니다. 파일럿 테스트에서 공간 ALD가 15세대 기판을 횡단하고 있기 때문에 PECVD와 ALD경쟁 구도은 엄격해지고, 양 방법을 활용한 하이브리드 생산 플로어가 추진될 것으로 예측됩니다.

파릴렌 C와 ALD Al2O3를 결합한 하이브리드 스택은 응력 완화와 수분 차단의 균형이 입증됨에 따라 2024년에 47.3%의 매출을 확보했습니다. 이러한 다이어드는 105g/m2/day 이하의 WVTR을 달성하는 동시에 프리미엄 스마트폰에서 요구되는 사양인 10,000회 이상의 굴곡 사이클을 유지했습니다. 그러나 단층 장벽은 현재 가장 빠른 29.1%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 이는 실비온 블렌드 하이브리머 필름이 증착 시퀀싱 길이를 절반으로 함으로써 동등한 보호를 제공하고 롤러블 패널의 택트 타임을 단축하기 때문입니다.

무기 다층막은 비교할 수 없는 내산소성을 발휘하지만, 인장 응력 하에서 균열이 발생할 위험이 있으며, 접이식 패널에의 채용은 제한됩니다. 유기 다층막은 굴곡성이 우수하지만 수명 목표에 도달하는 것은 거의 없습니다. 스마트폰에는 하이브리드 다이가 채용되고 자동차 클러스터에는 트리플 무기 캡이 필요합니다. 부품 공급업체는 인접한 층간의 굴절률, 탄성률, 점착성을 조화시키는 모듈러 재료 키트로 대응해, 수율 90% 이상의 라인의 신뢰성을 확보하고 있습니다.

박막 봉지 시장은 기술별(플라즈마 인핸스트 화학 기상 성장법, 원자층 증착법, 기타), 층 구조별(무기 다층 배리어, 유기 다층 배리어, 기타), 용도별(플렉서블 OLED 디스플레이, 기타), 성막 장치 유형별(클러스터 PECVD 시스템, 기타), 최종 이용 산업별(가전, 재생에너지, 기타), 지역별로 분류됩니다.

지역별 분석

아시아태평양은 2024년 69.5%의 매출 점유율을 유지, 한국과 중국의 팹 확장과 통합 공급 생태계가 견인했습니다. 봉지의 자본 비용을 다루는 정부 우대 조치가 ALD 클러스터의 설치를 가속화했고, 한국의 선수들은 마진을 지키기 위해 고가치 제품과 탠덤 스택으로 축발을 옮겼습니다. 지역 금형 제조업체 및 화학 제조업체가 ALD 제조 공장 근처에 거점을 두고 인증주기를 단축하여 박막 봉지 시장 전체의 우위성을 강화했습니다.

유럽은 자동차와 BIPV 수요에 힘입어 탄탄한 성장을 보였습니다. EU의 엄격한 자동차 안전 지령이 곡면 OLED 조종석 채용을 가속화, 탄소 중립 건축 규칙이 태양 정면에서 ALD 배리어 채용에 박차를 가했습니다. 연구 컨소시엄은 저온 ALD 전구체를 진보시켜 성능을 원형 이코노미의 목표에 부합시켰습니다.

중동 및 아프리카는 UAE와 사우디아라비아와 같은 국가들이 경제 다양화를 위해 전자 클러스터에 자금을 제공했기 때문에 작은 기반에서 최고의 CAGR 27.2%를 나타낼 전망입니다. 가혹한 사막 기후로 인해 디스플레이와 태양전지 제품의 견고한 밀봉이 필요했고 ALD 기반 무기층에 대한 프리미엄 수요가 탄생했습니다. 아시아 OEM과의 기술 이전 파트너십은 현지 생산 능력을 향상시키고 세계 브랜드의 단일 지역 의존도를 감소시켰습니다.

북미는 패널 생산이 제한적이었음에도 불구하고 재료과학의 리더십과 장비 수출을 통해 영향력을 유지했습니다. 자동차용 지령과 양자점 microLED의 연구개발이 특수한 배리어 노하우에 대한 수요를 지지하는 한편, 롤·투·롤 ALD의 신흥 기업이 벤처 자금을 활용해 웨어러블 라인을 상품화했습니다. 지역 팹은 머신러닝에 의한 프로세스 제어로 대학과 협력하여 막의 균일성과 처리량을 향상시켰습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 한국과 중국의 AMOLED 생산 능력 증강이 ALD-TFE 툴의 수주를 뒷받침

- EU와 NA에 있어서 자동차용 곡면 디스플레이의 의무화

- 롤 투 롤 ALD에 의한 의료용 웨어러블 인증의 해정

- 무기 장벽을 높이는 EU의 탄소 중립 BIPV 추진

- SID상 수상 저온 ALD 재료가 폴더블 가능

- 중국 '신형 디스플레이' 보조금이 봉지 설비 투자를 커버

- 시장 성장 억제요인

- 제6세대 ALD 클러스터 라인의 고액 설비 투자

- -40℃ 이하에서의 자동차 사이클의 신뢰성에 관한 고장

- 초박형 플렉서블 유리와의 경쟁

- 전구체 공급의 병목(예 : DEZ)

- 밸류체인 분석

- 규제와 기술 전망

- 주요 실적 지표의 벤치마크

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 거시 경제 요인이 시장에 미치는 영향 평가

제5장 시장 규모와 성장 예측

- 기술별

- 플라즈마 강화 화학 기상 증착(PECVD)

- 원자층 증착(ALD)

- 잉크젯 프린팅

- 진공 열 증발(VTE)

- 유기 기상 증착(OVPD)

- 롤 투 롤 ALD

- 기타 신흥기술(파릴렌, 졸겔)

- 층 구조별

- 무기 다층 차단막

- 유기 다층 차단막

- 하이브리드(유기+무기) 차단막

- 단층 캡슐화

- 용도별

- 플렉서블 OLED 디스플레이

- 박막 태양광 발전

- 플렉서블 OLED 조명

- 웨어러블 및 의료용 일렉트로닉스

- 자동차용 디스플레이 및 조명

- 양자점 및 마이크로 LED 디바이스

- 인쇄 센서 및 IoT 디바이스

- 증착 장비 유형별

- 클러스터 PECVD 시스템

- 잉크젯 캡슐화 프린터

- ALD 반응기

- 롤 투 롤 진공 시스템

- 레이저 보조 증착 장비

- 최종 이용 산업별

- 소비자 일렉트로닉스

- 신재생에너지

- 자동차 및 운송

- 헬스케어 및 웨어러블

- 산업 및 항공우주

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 한국

- 일본

- 인도

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Samsung SDI Co., Ltd.

- LG Chem Ltd.

- Universal Display Corporation

- Applied Materials Inc.

- Veeco Instruments Inc.

- 3M Inc.

- Toray Industries Inc.

- Kateeva

- BASF(Rolic) AG

- Meyer Burger Technology AG

- Encapsulix SAS

- Forge Nano Inc.

- Aixtron SE

- Angstrom Engineering Inc.

- Forge Nano Inc.

- Beneq Oy

- Picosun Oy

- Canon Tokki Corporation

- AP Systems

- EMD Electronics(Merck KGaA)

- Idemitsu Kosan Co.

- Encapsulix SAS

- Wonik IPS

- Vitriflex Inc.

제7장 시장 기회와 향후 전망

KTHThe thin film encapsulation market size was valued at USD 0.35 billion in 2025 and is forecast to reach USD 1.05 billion by 2030, reflecting a robust 20.78% CAGR.

Rapid adoption of flexible OLED displays, surging demand for bendable consumer devices, and aggressive capacity additions in Asia-Pacific have kept the growth trajectory steep. Manufacturers are prioritizing atomic layer deposition (ALD) barriers that achieve water-vapor transmission rates below 10-6 g/m2/day, enabling longer device lifetimes while preserving form-factor flexibility. Automotive mandates for curved cockpit displays and medical certification of roll-to-roll ALD films are widening application scope, even as precursor shortages and capital-intensive Gen-6 ALD lines present headwinds. Competitive intensity is rising as Chinese firms, buoyed by "New Display" subsidies, scale output and erode Korean dominance.

Global Thin Film Encapsulation Market Trends and Insights

AMOLED capacity expansions in South Korea and China are fueling ALD-TFE tool orders

Samsung Display allocated USD 3 billion for an 8.6-generation IT OLED line targeting 2026 production, while BOE committed USD 8.7 billion for a comparable plant. These projects multiplied purchase orders for ALD encapsulation tools because the technology offers uniform, pinhole-free barriers at low temperatures, a necessity for next-generation IT and automotive panels. Heightened competition has revived Korean shipment leadership but simultaneously broadened ALD demand across Asia-Pacific foundries.

Automotive curved-display mandates in the EU and North America

Regulatory guidance favoring seamless instrument clusters has sparked accelerated design-ins of curved OLED dashboards. These modules need encapsulation stacks that withstand vibration, UV exposure, and -40 °C cycling. Samsung's adoption of tandem OLED with advanced moisture barriers exemplified the shift, positioning the firm to capture revenue as total automotive display spend is forecast to overtake monitor panel sales by 2026.

High CapEx of Gen-6 ALD cluster lines

Next-generation ALD stacks demand more than USD 100 million per line, sidelining mid-tier producers and slowing technology diffusion. Many Asian fabs still amortize older cluster tools, complicating upgrade economics even where yield benefits are clear. This cost barrier delays uniform adoption of best-in-class encapsulation across the thin film encapsulation market.

Other drivers and restraints analyzed in the detailed report include:

- Roll-to-roll ALD unlocking certified medical wearables

- EU carbon-neutral BIPV push boosting inorganic barriers

- Reliability failures under -40 °C automotive cycling

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

ALD recorded a 26.4% CAGR outlook while PECVD held 39.3% revenue in 2024, illustrating a transition phase within the thin film encapsulation market. ALD films reached water-vapor rates at 10-6 g/m2/day that extend OLED life spans and support foldable substrates. Roll-to-roll ALD upgraded throughput to web speeds suitable for wearable production, while spatial ALD is overcoming substrate-size limits. PECVD remains preferred for rigid panels needing high volume. VTE and OVPD continue in niche emissive stacks where material compatibility overrides barrier extremity. Low-temperature ALD chemistries awarded by SID in 2023 unlocked polyimide substrates for mass foldables, deepening the technology mix. Consequently, ALD tool providers enjoy record order backlogs, lifting regional supplier ecosystems across South Korea, China, and the United States.

The thin film encapsulation market continues to rely on PECVD for cost-sensitive SKUs because the reactors integrate seamlessly with legacy TFT lines. Inkjet encapsulation printing, spearheaded by Kateeva, decreased organic material waste and enabled patterned barriers for smartwatch dials. VTE retains relevance for small-area microdisplays where device yield trumps throughput. With spatial ALD crossing 15 gen substrates in pilot tests, the competitive landscape between PECVD and ALD is expected to tighten, driving hybrid production floors that leverage both methods.

Hybrid stacks combining parylene C with ALD Al2O3 secured 47.3% sales in 2024, thanks to a proven balance of stress relief and moisture blocking. These dyads achieved sub-105 g/m2/day WVTR while sustaining flex cycles exceeding 10,000 bends, a specification demanded by premium smartphones. Single-layer barriers, however, now post the fastest 29.1% CAGR because silbione-blended hybrimer films offer comparable protection at half the deposition sequence length, cutting takt time for rollable panels.

Inorganic multi-layers deliver unmatched oxygen resistance but risk crack formation under tensile stress, limiting adoption in foldables. Organic multi-layers excel in bendability yet rarely reach lifetime targets alone. Commercial lines consequently calibrate layer architecture by product class: smartphones accept hybrid dyads, automotive clusters need triple inorganic caps, while e-textiles increasingly lean on advanced organic chemistries. Component suppliers respond with modular material kits that harmonize refractive index, modulus, and stickiness across adjoining layers, ensuring line reliability beyond 90% yield.

Thin Film Encapsulation Market is Segmented by Technology (Plasma-Enhanced Chemical Vapor Deposition, Atomic Layer Deposition, and More), by Layer Structure (Inorganic Multilayer Barriers, Organic Multilayer Barriers, and More), by Application (Flexible OLED Displays, and More), by Deposition Equipment Type (Cluster PECVD Systems, and More), by End-Use Industry (Consumer Electronics, Renewable Energy, and More), and by Geography.

Geography Analysis

Asia-Pacific retained 69.5% revenue share in 2024, driven by South Korea's and China's fab expansions and integrated supply ecosystems. Government incentives covering encapsulation capital costs accelerated ALD cluster installations, while Korean players pivoted toward high-value products and tandem stacks to defend margins. Regional tooling and chemical suppliers co-located near fabs, shortening qualification cycles and reinforcing dominance across the thin film encapsulation market.

Europe posted healthy gains built on automotive and BIPV demand. Strict EU vehicle safety directives accelerated curved OLED cockpit adoption, and carbon-neutral building rules spurred ALD barrier uptake in solar facades. Research consortia advanced low-temperature ALD precursors, aligning performance with circular-economy objectives.

The Middle East and Africa exhibited the highest 27.2% CAGR outlook from a small base, as nations like the UAE and Saudi Arabia funded electronics clusters to diversify their economies. Harsh desert climates necessitated robust encapsulation for display and solar products, creating premium demand for ALD-based inorganic layers. Technology transfer partnerships with Asian OEMs seeded local capacity, reducing single-region dependency for global brands.

North America maintained influence through materials science leadership and equipment exports despite limited panel production. Automotive mandates and quantum-dot microLED research and development anchored demand for specialized barrier know-how, while roll-to-roll ALD startups leveraged venture funding to commercialize wearable lines. Regional fabs collaborated with universities on machine-learning process control, enhancing film uniformity and throughput.

- Samsung SDI Co., Ltd.

- LG Chem Ltd.

- Universal Display Corporation

- Applied Materials Inc.

- Veeco Instruments Inc.

- 3M Inc.

- Toray Industries Inc.

- Kateeva

- BASF (Rolic) AG

- Meyer Burger Technology AG

- Encapsulix SAS

- Forge Nano Inc.

- Aixtron SE

- Angstrom Engineering Inc.

- Forge Nano Inc.

- Beneq Oy

- Picosun Oy

- Canon Tokki Corporation

- AP Systems

- EMD Electronics (Merck KGaA)

- Idemitsu Kosan Co.

- Encapsulix SAS

- Wonik IPS

- Vitriflex Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AMOLED Capacity Expansions in South Korea and China Fueling ALD-TFE Tool Orders

- 4.2.2 Automotive Curved-Display Mandates in EU and NA

- 4.2.3 Roll-to-Roll ALD Unlocking Certified Medical Wearables

- 4.2.4 EU Carbon-Neutral BIPV Push Boosting Inorganic Barriers

- 4.2.5 SID Award-Winning Low-Temp ALD Materials Enabling Foldables

- 4.2.6 China "New Display" Subsidies Covering Encapsulation Capex

- 4.3 Market Restraints

- 4.3.1 High Capex of Gen-6 ALD Cluster Lines

- 4.3.2 Reliability Failures under -40 °C Automotive Cycling

- 4.3.3 Competition from Ultra-Thin Flexible Glass

- 4.3.4 Precursor Supply Bottlenecks (e.g., DEZ)

- 4.4 Value Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Key Performance Indicators Benchmarked

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Impact of Macroeconomic factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Plasma-Enhanced Chemical Vapor Deposition (PECVD)

- 5.1.2 Atomic Layer Deposition (ALD)

- 5.1.3 Inkjet Printing

- 5.1.4 Vacuum Thermal Evaporation (VTE)

- 5.1.5 Organic Vapor Phase Deposition (OVPD)

- 5.1.6 Roll-to-Roll ALD

- 5.1.7 Other Emerging Techniques (Parylene, Sol-Gel)

- 5.2 By Layer Structure

- 5.2.1 Inorganic Multilayer Barriers

- 5.2.2 Organic Multilayer Barriers

- 5.2.3 Hybrid (Organic+Inorganic) Barriers

- 5.2.4 Single-Layer Encapsulation

- 5.3 By Application

- 5.3.1 Flexible OLED Displays

- 5.3.2 Thin-Film Photovoltaics

- 5.3.3 Flexible OLED Lighting

- 5.3.4 Wearable and Medical Electronics

- 5.3.5 Automotive Displays and Lighting

- 5.3.6 Quantum-Dot and MicroLED Devices

- 5.3.7 Printed Sensors and IoT Devices

- 5.4 By Deposition Equipment Type

- 5.4.1 Cluster PECVD Systems

- 5.4.2 Inkjet Encapsulation Printers

- 5.4.3 ALD Reactors

- 5.4.4 Roll-to-Roll Vacuum Systems

- 5.4.5 Laser-Assisted Deposition Tools

- 5.5 By End-Use Industry

- 5.5.1 Consumer Electronics

- 5.5.2 Renewable Energy

- 5.5.3 Automotive and Transportation

- 5.5.4 Healthcare and Wearables

- 5.5.5 Industrial and Aerospace

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 France

- 5.6.3.3 United Kingdom

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 South Korea

- 5.6.4.3 Japan

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Samsung SDI Co., Ltd.

- 6.4.2 LG Chem Ltd.

- 6.4.3 Universal Display Corporation

- 6.4.4 Applied Materials Inc.

- 6.4.5 Veeco Instruments Inc.

- 6.4.6 3M Inc.

- 6.4.7 Toray Industries Inc.

- 6.4.8 Kateeva

- 6.4.9 BASF (Rolic) AG

- 6.4.10 Meyer Burger Technology AG

- 6.4.11 Encapsulix SAS

- 6.4.12 Forge Nano Inc.

- 6.4.13 Aixtron SE

- 6.4.14 Angstrom Engineering Inc.

- 6.4.15 Forge Nano Inc.

- 6.4.16 Beneq Oy

- 6.4.17 Picosun Oy

- 6.4.18 Canon Tokki Corporation

- 6.4.19 AP Systems

- 6.4.20 EMD Electronics (Merck KGaA)

- 6.4.21 Idemitsu Kosan Co.

- 6.4.22 Encapsulix SAS

- 6.4.23 Wonik IPS

- 6.4.24 Vitriflex Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment