|

시장보고서

상품코드

1851138

도심 항공 모빌리티(UAM) 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2040년)Urban Air Mobility - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2040) |

||||||

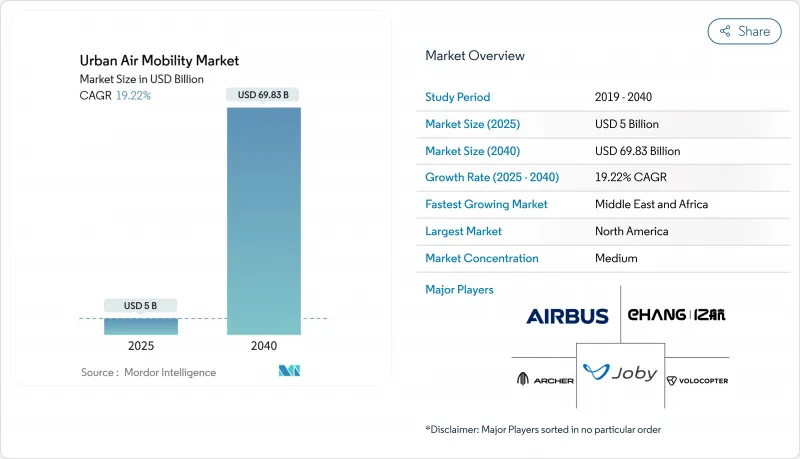

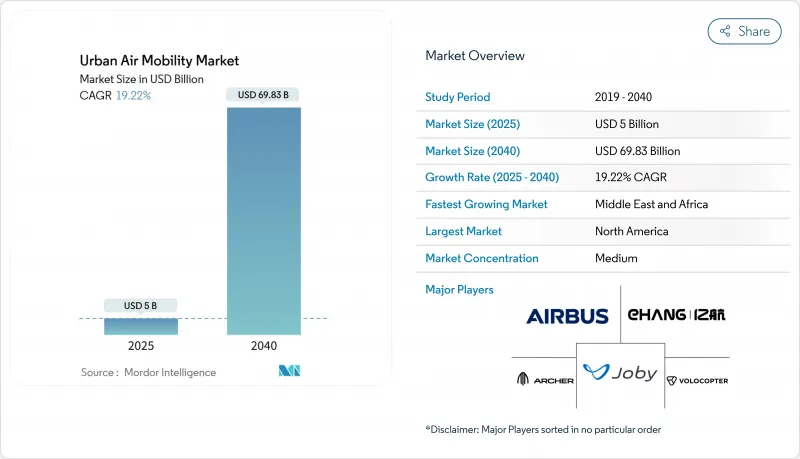

도심 항공 모빌리티(UAM) 시장 규모는 2025년에 50억 달러로 추정되고, 2040년에는 CAGR 19.22%로 성장할 전망이며, 698억 3,000만 달러에 이를 것으로 예측됩니다.

배터리 에너지 밀도의 비약적 향상으로 eVTOL의 항속 거리는 150km를 넘어 수익성이 높은 도시 간 회랑이 열려 프리미엄 서비스의 비즈니스 케이스가 강화되었습니다. 미국 연방 항공국의 파워 리프트 규칙(POWER-LIFT RULES)에 도움이 되는 인증의 신속화는 규제 위험을 낮추고 대규모 자본 도입을 촉진합니다. 항공우주의 개척자와 자동차 제조업체와의 전략적 제휴는 제조 비용을 압축하고 관민 제휴 모델은 기존 항공 인프라에서 볼 수 없었던 속도로 버티 포트 네트워크에 자금을 공급하고 있습니다. 이러한 힘이 결합되어 UAM 시장은 급속한 세계적 확대로 향하고 있습니다.

세계의 도심 항공 모빌리티 시장 동향 및 인사이트

배터리 에너지 밀도의 급속한 향상으로 eVTOL의 항속 거리가 150km를 넘습니다.

고체 전지의 에너지 밀도는 450-550Wh/kg으로 기존의 리튬 이온 전지에 비해 최대 90% 향상되었습니다. 비행 테스트는 1회 충전으로 48분의 임무를 수행할 수 있으며 수익성이 높은 도시 간 셔틀 임계값을 충족합니다. 항속거리가 길기 때문에 운행사는 여러 도시 간 수요를 집계할 수 있어 하루 항공기 이용률을 높이고 좌석 마일당 비용을 직접 낮출 수 있습니다. 이러한 성능 향상은 규제 당국이 요구하는 주요 안전 지표도 충족시켜 인증 취득의 여행을 원활하게 합니다. 그 결과, 도시 간 노선은 향후 10년간 UAM 시장 수익의 대부분을 차지할 것으로 예측됩니다.

자동차 등급 공급망이 eVTOL의 단가를 낮춥니다.

eVTOL 제조업체와 자동차 OEM간의 제휴로 양산 노하우가 항공우주 프로그램에 통합되고 있습니다. Toyota의 Joby Aviation에 투자하고 부품 조달을 공유하면 항공기 비용이 2028년까지 35% 절감될 전망입니다. 표준화된 부품, 낭비없는 조립 라인, 자동차 수준의 품질 관리 프로세스는 출시 주기를 단축하고 가격 설정을 안정시킵니다. 획득 비용의 하락은 운임의 인하로 이어지며, 이용하기 쉬운 고객 기반이 확대되어 UAM 시장 전체 수요가 강화됩니다.

Tier-1 도시에서 느린 버티포트 허용

주요 도시에서는 10개 이상의 기관이 승인 프로세스에 관여하는 것이 보통이고, 2년 이상의 타임라인을 필요로 하여 보유 비용을 늘려가고 있습니다. 로스앤젤레스의 경우, 시내의 한 곳에서 건설이 시작되기 전에 조닝, 환경, 긴급 대응 부서 간의 조정이 필요했습니다. 지연은 운영자를 교외 노드로 향하게 하고 초기 단계의 경로 밀도를 제한하며 UAM 시장의 완전한 가치 제안을 선도합니다.

부문 분석

파일럿 기계는 2024년 매출의 55.10%를 차지했으며, 이는 업계 초기 단계에서 규제 당국이 익숙한 조종석 컨셉을 선호했다는 것을 반영합니다. Joby Aviation의 S4는 2025년에 3개의 FAA 인증 단계를 통과했으며, 탑승자 플랫폼이 단기적으로 우위를 차지함을 명확히 했습니다. 이 부문은 UAM 시장에서 가장 큰 슬라이스를 얻고 대규모 인프라 네트워크가 형성되는 동안 금융 기관에 자신감을 부여합니다. 운영자는 또한 기존 파일럿 양성 파이프라인을 활용하여 고객의 지불 의향이 높은 승무원 비용을 상쇄하는 프리미엄 공항-셔틀 통로에서 서비스를 확장할 수 있습니다.

자율 내비게이션기는 현재는 작은 카테고리이지만, 2040년까지의 CAGR은 21.51%로, 모든 탈 것 유형 중에서 가장 빠르게 성장할 것으로 예측되고 있습니다. 위스크 에어로사와 NASA와의 협력은 무탑승 상업 서비스의 전제조건인 검지 및 회피 검증을 가속시킵니다. 조종사를 제거하면 직접 운항 비용을 약 26% 절감할 수 있으며, 더 넓은 지역을 커버하고 운임을 낮출 수 있습니다. AI 지원 UTM 플랫폼이 성숙함에 따라 자율성은 UAM 시장 전체의 운영 모델을 변화시키고 소프트웨어의 신뢰성과 함대 오케스트레이션에 경쟁의 초점을 옮길 것으로 예측됩니다.

100km 미만의 도시 부문은 2024년 UAM 시장 규모의 59.81%를 차지했으며, 도심과 공항을 연결하는 혼잡 완화 경로가 견인합니다. Skyport Infrastructure는 같은 해 도심에 여러 공항을 개설하여 소비자의 조기인지를 촉구했습니다. 사업자는 에너지를 대량으로 소비하는 수직 단계에서도 배터리 잔량에 여유가 있어 예측 가능한 스케줄과 신속한 자산 회전이 가능하기 때문에 이러한 단거리 홉을 선호하고 있습니다.

100km를 넘는 도시간 임무는 가장 기세가 높으며 CAGR 22.82%로 상승할 것으로 예측됩니다. 고체 배터리와 하이브리드 전기 추진은 가까운 거대한 도시를 연결하고 도로의 병목 현상을 피하기 위해 항속 거리와 적재량의 요구를 충족합니다. 중동의 지역 정부는 이러한 회랑을 관광과 분산형 경제권의 실현으로 이어질 것으로 보고 있으며, 배치의 가속화를 뒷받침하고 있습니다. 도시 간 운송의 채용은 대응 가능한 고객층을 넓히고, 네트워크 효과를 확대하며, UAM 시장의 장기적인 확대를 뒷받침합니다.

지역 분석

북미는 FAA의 명확한 인증 패스웨이와 풍부한 벤처 자금 풀에 의해 지원되며, 2024년 매출의 46.89%를 차지해, 여전히 최대 지역입니다. 고정 기반 운영자 체인의 애틀랜틱과 시그니처는 2025년 초에 주요 공항에서 버티포트 클러스터를 건설하기 시작했으며 고수량 코리도 전역에서 운항의 두께를 늘렸습니다. 미국 공군의 민첩성 프라임 프로그램은 군사 시험 데이터를 민간 인증의 증거로 바꾸어 기술의 준비 태세를 더욱 가속시킵니다. 이러한 시장 개척은 북미 UAM 시장을 지원하고 다른 지역의 양식이 됩니다.

중동 및 아프리카는 가장 가파른 성장 곡선을 나타내며 2025-2040년 CAGR 28.21%로 성장이 예측되고 있습니다. 아부다비는 아처 에비에이션사와 UAE를 세계적인 쇼케이스로 자리매김하고 최초의 상용 에어택시 서비스를 개시하는 것으로 최종 합의했습니다. 소블린 펀드가 버티포트 인프라에 많은 자금을 투입하고, 다양한 지역이 사막과 산악지대에서 매력적인 도시 간 이용 사례를 낳고 있습니다. 조기 진출자로서의 우위와 규제 당국의 강력한 백업은 UAM 시장에서 지역 리더로서의 지위를 확립할 것으로 기대됩니다.

유럽은 첨단 규제 및 지속가능성 의무화를 통해 강력한 지위를 유지하고 있습니다. EASA는 2024년에 종합적인 UAM 프레임워크를 채택하여 사업자에게 명확한 운영 규칙을 부여했습니다. 2025년에 발표된 시민 의식 조사는 eVTOL의 소음과 안전 기준을 주민들에게 설명했을 때 83%가 호의적임을 보여줍니다(easa.europa.eu). 파리와 런던과 같은 도시는 주요 국제 행사 전에 서비스를 시작하고 녹색 이동성 목표를 활용하여 인프라 자금을 모으는 것을 목표로 합니다. 이러한 협력적인 접근 방식으로 유럽은 진보하는 UAM 시장에 확고하게 통합되어 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 배터리 에너지 밀도의 급속한 향상에 의해 eVTOL의 항속 거리는 150km 초과

- 자동차급 공급망이 eVTOL의 단가를 낮춥니다.

- 버티포트 PPP 자금 조달 모델이 인프라 정비 가속

- 규제의 '샌드 박스' 회랑이 인증 취득 시기를 앞당깁니다.

- 메가허브의 확장에 의한 프리미엄 공항 셔틀 수요

- AI 대응 UTM 플랫폼이 고밀도 공역 운용 리스크 경감

- 시장 성장 억제요인

- Tier-1 도시에서의 버티포트 허가 지연

- 소음과 시각 공해에 대한 사회적 수용의 역풍

- 전지 원료 가격의 변동

- 완전 자율화 전의 파일럿 부족 병목 현상

- 밸류체인 분석

- 규제 전망

- 기술의 전망

- Porter's Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 차량 유형별

- 파일럿

- 자율

- 범위별

- 인트라시티(100km 미만)

- 인터시티(100km 이상)

- 추진 유형별

- 풀 전동

- 하이브리드

- 가솔린

- 용도별

- 여객 에어택시

- 도시 내 셔틀

- 긴급 의료 서비스

- 화물 및 물류

- 최종 사용자별

- 라이드 쉐어 사업자

- 법인 및 VIP 고객

- 전자상거래 물류기업

- 헬스케어 프로바이더

- 군 및 정부 기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 남미

- 브라질

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Airbus SE

- Joby Aero, Inc.

- Eve Holding, Inc.

- Volocopter Technologies GmbH

- Vertical Aerospace

- Archer Aviation, Inc.

- BETA Technologies, Inc.

- Wisk Aero LLC

- Guangzhou EHang Intelligent Technology Co., Ltd.

- Supernal, LLC

- Textron, Inc.

- Jaunt Air Mobility LLC

- Pivotal Aero, LLC.

- Ascendance Flight Technologies SAS

- AutoFlight Co. Ltd.

- SkyDrive Inc.

제7장 시장 기회 및 향후 전망

AJY 25.11.12The urban air mobility (UAM) market size is estimated at USD 5.00 billion in 2025, and is expected to reach USD 69.83 billion by 2040, at a CAGR of 19.22% during the forecast period.

Battery-energy-density breakthroughs have extended eVTOL range beyond 150 km, opening profitable intercity corridors and strengthening the business case for premium services. Faster certification, helped by the Federal Aviation Administration's powered-lift rule, lowers regulatory risk and encourages large capital deployments. Strategic alliances between aerospace pioneers and automotive manufacturers are compressing production costs, while public-private-partnership models are financing vertiport networks at a pace not seen in legacy aviation infrastructure. Together, these forces are positioning the UAM market for rapid global scale-up.

Global Urban Air Mobility Market Trends and Insights

Rapid Battery-Energy-Density Gains Push eVTOL Range Beyond 150 km

Solid-state cells now deliver 450-550 Wh/kg, up to 90% higher than earlier lithium-ion chemistries. Flight tests have shown 48-minute, single-charge missions, meeting the threshold for profitable intercity shuttles. Longer range lets operators aggregate demand across multiple city pairs and raises daily aircraft utilization, directly lowering cost per seat-mile. These performance gains also satisfy key safety metrics regulators require, smoothing the certification journey. As a result, intercity routes are forecast to capture a progressively larger slice of the UAM market revenue over the coming decade.

Automotive-Grade Supply Chains Drive Down eVTOL Unit Costs

Partnerships between eVTOL builders and automobile OEMs are embedding mass-production know-how into aerospace programs. Toyota's investment in Joby Aviation and shared component sourcing will cut airframe costs by 35% before 2028. Standardized parts, lean assembly lines, and automotive-quality control processes shorten ramp-up cycles and stabilize pricing. Lower acquisition costs feed through to reduced fares, expanding the accessible customer base and reinforcing demand across the UAM market.

Slow Vertiport Permitting in Tier-1 Cities

Approval processes in major metros routinely involve more than ten agencies, driving timelines well past two years and inflating holding costs. In Los Angeles, a single downtown site required coordination among zoning, environmental, and emergency-response departments before construction could start. Delays push operators toward suburban nodes, limiting early-stage route density and postponing the full value proposition of the UAM market.

Other drivers and restraints analyzed in the detailed report include:

- Vertiport PPP Financing Models Unlock Infrastructure Rollout

- Regulatory "Sandbox" Corridors Accelerate Certification Timelines

- Public-Acceptance Headwinds on Noise and Visual Pollution

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Piloted aircraft controlled 55.10% of 2024 revenue, reflecting regulators' preference for familiar cockpit concepts during the industry's opening phase. Joby Aviation's S4 advanced through three FAA certification stages in 2025, underscoring the near-term dominance of crewed platforms. This segment captured the largest slice of the UAM market, giving financiers confidence while larger infrastructure networks take shape. Operators also leverage existing pilot-training pipelines to scale services in premium airport-shuttle corridors, where customer willingness to pay offsets higher crew costs.

Autonomous craft, now a smaller category, is forecast to grow at a 21.51% CAGR to 2040, the fastest of any vehicle type. Wisk Aero's collaboration with NASA accelerates detect-and-avoid validation, a prerequisite for uncrewed commercial service. Removing pilots could cut direct operating expenses by about 26%, translating into wider geographic coverage and lower fares. As AI-enabled UTM platforms mature, autonomy is expected to alter operating models across the UAM market, shifting the competitive focus to software reliability and fleet orchestration.

Intracity segments under 100 km held 59.81% of the UAM market size in 2024, driven by congestion-relief routes linking city centers to airports. Skyports Infrastructure opened several downtown vertiports that year, anchoring early consumer awareness. Operators favor these short hops because battery reserves remain generous even with energy-intensive vertical phases, enabling predictable schedules and rapid asset turns.

Intercity missions above 100 km show the highest momentum, projected to rise at a 22.82% CAGR. Solid-state batteries and hybrid-electric propulsion now meet range and payload needs for linking close megacities and bypassing road bottlenecks. Regional governments in the Middle East see these corridors as enablers of tourism and decentralized economic zones, supporting accelerated deployment. Intercity adoption widens the addressable customer pool and magnifies network effects, reinforcing long-term expansion of the UAM market.

The Urban Air Mobility (UAM) Market Report is Segmented by Vehicle Type (Piloted and Autonomous), Range (Intracity and Intercity), Propulsion Type (Fully Electric, Hybrid Electric, and Gasoline), Application (Passenger Air Taxi, Intra-City Shuttle, and More), End User (Ride-Sharing Operators, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America remained the largest region, accounting for 46.89% of 2024 revenue, supported by the FAA's clear certification pathway and deep venture funding pools. Fixed-base-operator chains Atlantic and Signature began constructing vertiport clusters at major airports during early 2025, adding operational depth across high-yield corridors. The United States Air Force's Agility Prime program further accelerates technology readiness, turning military test data into civilian certification evidence. These developments anchor the North American UAM market and provide a template for other regions.

The Middle East and Africa region shows the steepest growth curve, projected at a 28.21% CAGR from 2025 to 2040. Abu Dhabi finalized an agreement with Archer Aviation to launch the first commercial air-taxi services, positioning the UAE as a global showcase. Sovereign funds channel significant capital into vertiport infrastructure, and diverse geography creates compelling intercity use cases over desert and mountain terrain. Early mover advantage and cohesive regulatory backing promise to propel regional leadership within the UAM market.

Europe retains a strong position through progressive regulation and sustainability mandates. EASA adopted a comprehensive UAM framework in 2024, giving operators clear operational rules. Public-acceptance surveys published in 2025 indicate 83% positive sentiment when residents are informed about eVTOL noise and safety standards, easa.europa.eu. Cities like Paris and London aim to debut services before major international events, leveraging green mobility goals to attract infrastructure funding. This coordinated approach keeps Europe firmly embedded in the advancing UAM market.

- Airbus SE

- Joby Aero, Inc.

- Eve Holding, Inc.

- Volocopter Technologies GmbH

- Vertical Aerospace

- Archer Aviation, Inc.

- BETA Technologies, Inc.

- Wisk Aero LLC

- Guangzhou EHang Intelligent Technology Co., Ltd.

- Supernal, LLC

- Textron, Inc.

- Jaunt Air Mobility LLC

- Pivotal Aero, LLC.

- Ascendance Flight Technologies S.A.S

- AutoFlight Co. Ltd.

- SkyDrive Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid battery-energy-density gains push eVTOL range beyond 150 km

- 4.2.2 Automotive-grade supply chains drive down eVTOL unit costs

- 4.2.3 Vertiport PPP financing models unlock infrastructure rollout

- 4.2.4 Regulatory "sandbox" corridors accelerate certification timelines

- 4.2.5 Premium airport-shuttle demand from mega-hub expansions

- 4.2.6 AI-enabled UTM platforms de-risk high-density airspace operations

- 4.3 Market Restraints

- 4.3.1 Slow vertiport permitting in tier-1 cities

- 4.3.2 Public-acceptance headwinds on noise and visual pollution

- 4.3.3 Battery raw-material price volatility

- 4.3.4 Pilot-shortage bottleneck before full autonomy

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Vehicle Type

- 5.1.1 Piloted

- 5.1.2 Autonomous

- 5.2 By Range

- 5.2.1 Intracity ( Less than 100 km)

- 5.2.2 Intercity (Greater than 100 km)

- 5.3 By Propulsion Type

- 5.3.1 Fully Electric

- 5.3.2 Hybrid Electric

- 5.3.3 Gasoline

- 5.4 By Application

- 5.4.1 Passenger Air Taxi

- 5.4.2 Intra-city Shuttle

- 5.4.3 Emergency Medical Services

- 5.4.4 Cargo and Logistics

- 5.5 By End User

- 5.5.1 Ride-Sharing Operators

- 5.5.2 Corporate and VIP Clients

- 5.5.3 E-commerce and Logistics Firms

- 5.5.4 Healthcare Providers

- 5.5.5 Military and Government Agencies

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 South Korea

- 5.6.3.4 India

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 United Arab Emirates

- 5.6.4.1.2 Saudi Arabia

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Rest of Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Airbus SE

- 6.4.2 Joby Aero, Inc.

- 6.4.3 Eve Holding, Inc.

- 6.4.4 Volocopter Technologies GmbH

- 6.4.5 Vertical Aerospace

- 6.4.6 Archer Aviation, Inc.

- 6.4.7 BETA Technologies, Inc.

- 6.4.8 Wisk Aero LLC

- 6.4.9 Guangzhou EHang Intelligent Technology Co., Ltd.

- 6.4.10 Supernal, LLC

- 6.4.11 Textron, Inc.

- 6.4.12 Jaunt Air Mobility LLC

- 6.4.13 Pivotal Aero, LLC.

- 6.4.14 Ascendance Flight Technologies S.A.S

- 6.4.15 AutoFlight Co. Ltd.

- 6.4.16 SkyDrive Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment