|

시장보고서

상품코드

1851140

자율운항선박 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Autonomous Ships - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

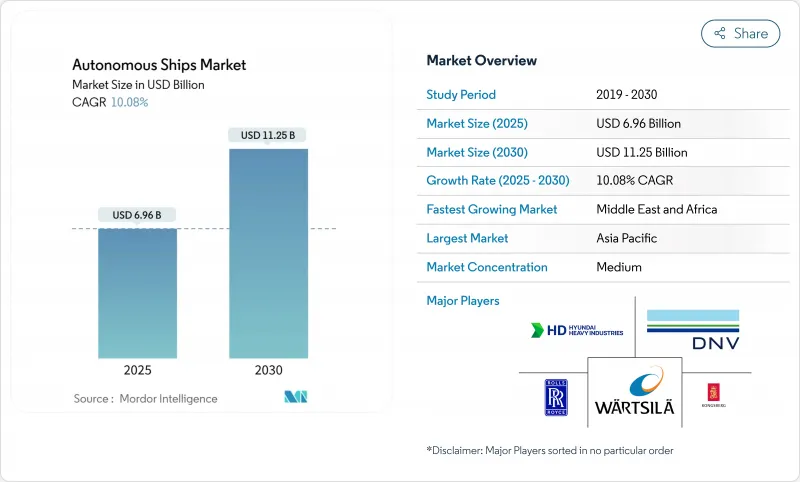

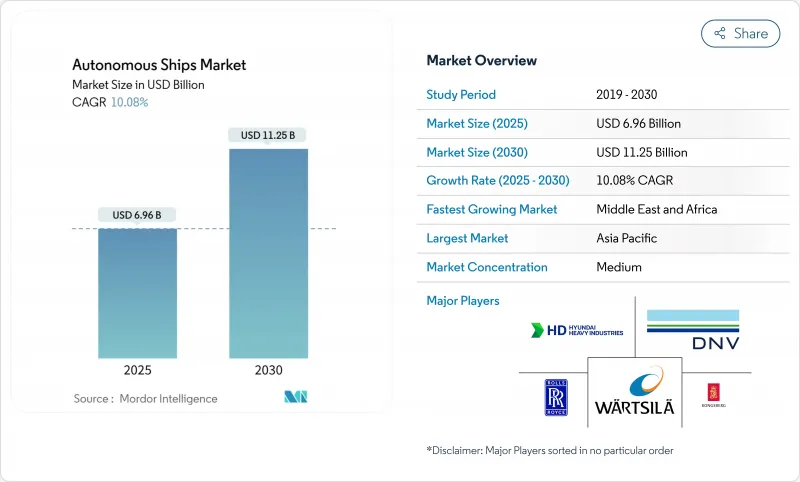

자율운항선박 시장 규모는 2025년에 69억 6,000만 달러로 추정되고, 2025-2030년 CAGR 10.08%로 성장할 전망이며, 2030년까지 112억 5,000만 달러로 상승할 것으로 예측됩니다.

승무원 관련 비용 절감을 요구하는 운영자의 압력, 배출 규제 강화, 인공지능의 급속한 진보는 상용 선단을 점차 높은 자동화 수준으로 밀어 올리고 있습니다. IMO의 향후 해상자율형 수상선박(MASS) 코드, 무인수상선박에 대한 국방비, 신뢰성이 높은 5G/LEO 위성 링크는 외항선박과 연안선박의 채용 스케줄을 총체적으로 단축합니다. 한국, 중국, 일본 조선소가 기술이 가득한 프로토타입을 시작하면서 아시아태평양은 여전히 주요 수혜자입니다. 동시에 중동은 자유로운 테스트 항로와 스마트 포트에 대한 투자를 활용하여 외국인 조종사를 유치하고 있습니다. 경쟁의 중심은 센서 퓨전 및 엣지 프로세싱을 결합한 통합 항법 제품군으로, 처음부터 전용 플랫폼에 투자하지 않으려는 운영자에게 매력적인 후속 패키지를 생성합니다.

세계의 자율운항선박 시장 동향 및 인사이트

데이터 중심의 플릿 최적화 및 원격 조작

오퍼레이터는 현재 인공지능(AI)의 항해 계획 엔진을 육상 제어 센터와 연계시켜 속도 프로파일의 미세 조정, 유지 보수 일정, 승무원의 재배치를 보다 효율적으로 실시했습니다. 스테나라인은 예측 항로 분석을 도입한 후 연료비를 절감하고 정시 운항률을 향상시켰습니다. 삼성중공업은 승무원 없이 1,500km의 대양횡단 항해를 실시하여 원격 감시 항행을 안전하게 실시할 수 있다는 업계의 신뢰를 강화하였습니다. 레이더, LiDAR, 광학, 음향 등의 멀티 센서 퓨전은 인간이 브리지에서 모니터링하는 것보다 더 풍부한 운항 상황을 제공하여 알고리즘이 혼잡한 실레인과 악천후를 실시간으로 피할 수 있도록 합니다.

탈탄소화 및 연료 효율

자율 제어 로직은 속도, 부하 및 최적의 배터리 배분을 조화시켜 시너지 효과로 단거리 항로 및 셔틀 서비스에서 진정한 제로 방출의 잠재력을 제공합니다. 2026년에 예정된 노르웨이 배터리 전용 페리는 항속 거리 불안으로 인한 페널티를 받지 않고 듀티 사이클을 충족시키기 위해 알고리즘에 의한 에너지 버짓을 채택하고 있습니다. Wartsila사는 하이브리드 개수로 15-25%의 연료 절감을 기록하고 있어 자율 모드에서 불필요한 스로틀 진동을 억제하면 그 효과는 더욱 높아집니다. Yara Birkeland의 7MWh 팩은 동등한 디젤 피더에 비해 운항 비용을 90% 절감했습니다.

원격 네비게이션 스택의 사이버 보안 취약점

머스크와 코스코가 피해를 입은 악성코드 사건은 그 위험성을 이야기합니다. Astaara는 해양 사이버 리스크 전용 커버를 2,500만 달러로 두배로 늘려 테러 관련 공격을 포함하도록 특약을 확대했습니다. 자율 자산은 쇼어 센터, VSAT 빔, 에지 프로세서와 같은 침입 지점을 늘리고 선주들은 중층 방어 및 지속적인 침입 테스트를 전개해야합니다.

부문 분석

부분 자율 시스템은 2024년 매출의 74.35%를 차지했으며, 선주가 브리지 승무원이 자동 충돌 회피와 동적 위치 결정을 감독할 수 있도록 단계적인 향상을 선호하고 있음을 나타냅니다. 완전 자율운항선박은 오늘날의 자율운항선박 시장의 일부만을 차지하고 있지만 CAGR 19.58%로 확대를 견인하고 있습니다. DARPA(국방고등연구계획국)의 크루레스 디파이언트의 배경에는 수용 블록을 없애는 것으로 페이로드가 해방되어 OpEx가 삭감되는 것이 확인되고 있습니다. IMO의 4단계 분류법은 운영자가 선상 지원에서 원격 감시로, 궁극적으로 무인 항로로 이동할 때 개조 지침을 제공합니다. 규제의 명확화 및 센서 비용의 저하는 완전 자율 항해가 파일럿 프로젝트에서 정기선 일정으로 이동하는 변곡점을 나타냅니다.

자율항해 기술 공급자는 육상 제어, 암호화 링크, 디지털 플릿 트윈을 구독 패키지에 번들하여 하드웨어 초기 비용을 상쇄합니다. 원격 조종 훈련 커리큘럼이 등장해, 새로운 해사 캐리어 패스가 탄생합니다. 보험 언더라이터는 부분적인 자율성과 완전한 자율성의 위험 풀을 분리하는 경향이 강해지고 있으며, 예측 가능한 거래에서 완전 자동화를 위한 설비 투자 사례를 강화하고 있습니다. 보다 많은 시장 진출 기업들이 운항 데이터를 수집함에 따라 장거리 무인 항로에 대한 신뢰가 높아지고, 2020년대 후반에는 보다 자율성이 높은 계층으로 점유율의 대부분이 서서히 이동하고 있습니다.

레이더 어레이, 통합 브리지 및 추진 제어는 안전 운항에 필수적이기 때문에 2024년 지출의 62.78%는 여전히 하드웨어가 차지하고 있습니다. 그러나 머신러닝 모델은 수 테라바이트의 수문 기상 데이터를 캡처하고 가장자리에서 항로 권장 사항을 제공하기 때문에 소프트웨어 수익은 거의 3배 빠르게 증가하고 있습니다. L3Harris와 같은 기업은 단일 콘솔에서 전체 선단을 지휘하는 AMORPHOUS C2 스위트를 출하합니다. 하드웨어 OEM은 현재 애플리케이션 프로그래밍 인터페이스를 공개하고 있으며, 타사는 센서를 교체하지 않고 인식 및 경로 계획 모듈을 업데이트할 수 있으므로 운영자의 수명 주기 비용을 낮출 수 있습니다.

표준화된 오픈 아키텍처 키트는 레트로핏 비즈니스를 촉진하고 2028년 이후 업그레이드의 자율적 선박 시장 규모가 30억 달러의 대대를 넘으면 이 부문은 새로운 패키지를 능가할 수 있습니다. 한편, 벤처기업은 클라우드 기반 시뮬레이션을 활용하여 검증 시간을 단축하고 있습니다. 플릿이 원시 로그를 구조화된 트레이닝 세트로 변환함에 따라 소프트웨어 개발자는 최소한의 해상 테스트로 동작 트리를 반복할 수 있게 되어 성능 향상이 가속화되고 코드가 주요 가치 드라이버로 정착합니다.

지역 분석

아시아태평양의 2024년 판매 점유율은 38.98%에 달했으며, 이는 제조업 심화, 정부 보조금 조정, 삼성 중공업 무인 1,500km 항해와 같은 성공 스토리 덕분입니다. 중국 Jin Dou Yun 0 Hao는 기존의 동업업체에 비해 건조비를 20%, 연료 소비량을 15% 절약하고 비용편익의 가정을 검증했습니다. 일본의 MEGURI2040 연합은 야드, 전기통신, 소프트웨어의 신흥기업을 공통의 테스트 코리도하에서 연계시켜, 이 지역의 체계적인 어프로치를 실증하고 있습니다.

중동 및 아프리카 부문은 가장 빠른 CAGR 14.01%로 확대되고 있습니다. 아랍에미리트(UAE)(UAE)은 미국 최초의 Over the Horizon USV인 후구로 사의 페가수스(Pegasus)를 승인했으며, 아부다비 항구는 스마트 태그 운영을 시험적으로 시작했습니다. 두바이의 원격 조종선을 위한 맞춤형 제어는 관료적인 마찰을 줄이고 걸프를 세계 벤더에게 매력적인 모래장으로 만듭니다.

노르웨이의 선구적인 배터리 페리와 적극적인 선급 협회에 참여함으로써 유럽은 자율운항선박 시장의 주목할만한 슬라이스를 유지하고 있습니다. EU는 AI와 해상 안전에 관한 규칙을 동시에 제정하고 세계 표준의 확립을 목표로 하고 있습니다. 북미는 미국 해군 지출, 캐나다의 북극권 물류, 실리콘 밸리의 연결 생태계에 의해 지원되고 있지만 여전히 영향력을 유지하고 있습니다. 이 지역에서의 방위 및 민생 배치의 수렴은 향상된 피드백 루프를 제공합니다. 즉, 방위는 초기 연구 개발에 자금을 제공하고 민생 사업자는 성숙한 구성 요소를 낮은 단가로 채택합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 데이터 주도의 플리트 최적화 및 원격 오퍼레이션

- 탈탄소화 및 연비 효율

- 고급 상황 인식 정장에 대한 수요

- 차세대 자율운항선박 개발

- 해군에서 무인 수상 함정의 방위 추진

- 엣지 AI와 5G/LEO 접속의 브레이크스루가 선박의 리얼타임 자율성 초래

- 시장 성장 억제요인

- 원격 네비게이션 스택의 사이버 보안 취약점

- 규제의 세분화 및 기국의 차이

- 높은 리노베이션 자본 지출

- 해상보험 및 배상책임의 불확실성

- 밸류체인 분석

- 규제 전망

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력 및 소비자

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 자율성 레벨별

- 부분 자율형

- 원격 조작

- 완전 자율형

- 컴포넌트별

- 하드웨어

- 소프트웨어

- 선박 유형별

- 화물

- 승객

- 해외 지원 및 에너지

- 방위

- 특별 목적

- 최종 사용자별

- 상업용

- 정부 및 군관계

- 추진력별

- 풀 전동

- 하이브리드

- 기존

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- ABB Ltd.

- BAE Systems plc

- DNV AS

- Fugro NV

- Hanwha Corporation

- HD Hyundai Heavy Industries Co. Ltd.

- Kongsberg Gruppen ASA

- L3Harris Technologies, Inc.

- Marine AI Ltd.

- MITSUI E&S Group

- Praxis Automation Technology BV

- Rolls-Royce plc

- Sea Machines Robotics, Inc.

- Samsung Heavy Industries Co., Ltd.

- Wartsila Corporation

- Vigor Industrial LLC

제7장 시장 기회 및 향후 전망

AJY 25.11.12The autonomous ships market size was recorded at USD 6.96 billion in 2025 and is forecasted to rise to USD 11.25 billion by 2030, reflecting a 10.08% CAGR over 2025-2030.

Operator pressure to cut crew-related expenses, tightening emissions rules, and rapid gains in artificial intelligence propel commercial fleets toward progressively higher automation levels. The IMO's upcoming Maritime Autonomous Surface Ships (MASS) Code, national defense spending on unmanned surface vessels, and reliable 5G/LEO satellite links collectively shorten the adoption timetable for ocean-going and littoral vessels. Asia-Pacific remains the principal beneficiary as South Korean, Chinese, and Japanese yards launch technology-laden prototypes. At the same time, the Middle East leverages liberal test corridors and smart-port investments to attract foreign pilots. Competitive activity centers on integrated navigation suites that pair sensor fusion with edge processing, creating attractive retrofit packages for operators unwilling to invest in purpose-built platforms at the outset.

Global Autonomous Ships Market Trends and Insights

Data-driven fleet optimisation and remote operations

Operators now link Artificial Intelligence (AI) voyage-planning engines with shore control centers to fine-tune speed profiles, schedule maintenance, and redeploy crews more efficiently. After rolling out predictive routing analytics, Stena Line trimmed fuel costs and improved on-time performance. Samsung Heavy Industries' 1,500 km transoceanic run without an onboard crew strengthened industry confidence that remote-supervised passages can be executed safely. Multi-sensor fusion-radar, LiDAR, optical, and acoustic-delivers a richer operational picture than a human bridge watch, allowing algorithms to dodge congested sea lanes and inclement weather in real time.

Decarbonisation and fuel efficiency

Autonomous control logic harmonises speed, load, and optimal battery dispatch, a synergy that unlocks true zero-emission potential on short-sea and shuttle services. Norway's battery-only ferries scheduled for 2026 rely on algorithmic energy budgeting to meet duty cycles without range-anxiety penalties. Wartsila documented 15-25% fuel savings on hybrid retrofits, gains that rise further when autonomous modes trim unnecessary throttle oscillations. The Yara Birkeland's 7 MWh pack slashed operating expense by 90% versus a comparable diesel feeder.

Cyber-security vulnerabilities of remote navigation stacks

The malware incidents that sidelined Maersk and COSCO illustrate the stakes. Astaara doubled its dedicated maritime cyber-risk cover to USD 25 million and broadened clauses to include terror-linked attacks, a sign that insurers view ransomware as a systemic threat. Autonomous assets multiply entry points-shore centers, VSAT beams, edge processors-forcing owners to deploy layered defences and continuous penetration tests.

Other drivers and restraints analyzed in the detailed report include:

- Demand for advanced situational-awareness suites

- Development of next-generation autonomous vessels

- Regulatory fragmentation and flag-state variance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Partially autonomous systems claimed 74.35% of revenue in 2024, evidence that shipowners prefer step-wise enhancements allowing bridge crews to oversee automated collision avoidance and dynamic positioning. Fully autonomous craft, while representing only a sliver of today's autonomous ships market, are pacing the expansion with a 19.58% CAGR. DARPA's crewless Defiant backdrop confirms that eliminating accommodation blocks frees payload and cuts OpEx. The IMO's four-stage taxonomy guides retrofits as operators move from on-board support to remote supervision and finally to unmanned routes. Growing regulatory clarity and falling sensor costs indicate an inflection point where fully autonomous voyages transition from pilot projects to liner schedules.

Autonomous technology providers bundle shore control, encrypted links, and digital fleet twins into subscription packages that offset upfront hardware expense. Remote operator training curricula are emerging, creating new maritime career paths. Insurance underwriters increasingly separate partial and full autonomy risk pools, reinforcing the capex case for fuller automation in predictable trades. As more autonomous ships market participants collect operational data, confidence in long-haul unmanned passages will mount, gradually shifting the majority share toward higher autonomy tiers by the late 2020s.

Hardware still anchors 62.78% of 2024 spend because radar arrays, integrated bridges, and propulsion controls remain compulsory for safe operations. Yet software revenues are growing almost three times faster as machine-learning models ingest terabytes of hydro-meteorological data to deliver route recommendations at the edge. Companies such as L3Harris ship AMORPHOUS C2 suites that orchestrate entire flotillas from a single console, an efficiency play that captivates fleet managers. Hardware OEMs now publish application programming interfaces so third parties can update perception or path-planning modules without replacing sensors, lowering operator lifecycle costs.

Standardized open-architecture kits encourage retrofit business, a segment that could eclipse newbuild packages once the autonomous ships market size for upgrades passes the USD 3 billion mark after 2028. Meanwhile, venture-backed firms exploit cloud-based simulation to shorten validation time. As fleets convert raw logs into structured training sets, software developers can iterate on behaviour trees with minimal sea trials, accelerating performance improvements and cementing code as the main value driver.

The Autonomous Ships Market Report is Segmented by Autonomy Level (Partially Autonomous, Remotely Controlled, and More), Component (Hardware and Software), Ship Type (Cargo, Passenger, Defense, and More), End User (Commercial, Government and Military), Propulsion (Fully Electric, Hybrid, and Conventional), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific posted 38.98% revenue share in 2024, thanks to manufacturing depth, coordinated government grants, and success stories such as Samsung Heavy Industries' unmanned 1,500 km voyage. China's Jin Dou Yun 0 Hao saved 20% on construction and 15% on fuel burn versus conventional peers, validating cost-benefit assumptions. Japan's MEGURI2040 coalition demonstrates the region's systemic approach, aligning yards, telecoms, and software start-ups under common test corridors.

The Middle East and Africa segment is expanding at the fastest 14.01% CAGR. The UAE green-lit Fugro's Pegasus, the first over-the-horizon USV on its registry, and Abu Dhabi ports pilot smart-tug operations. Dubai's bespoke controls for remotely piloted craft reduce bureaucratic friction, making the Gulf an attractive sandbox for global vendors.

Due to Norway's trailblazing battery ferries and proactive class-society engagement, Europe retains a notable slice of the autonomous ships market. The EU's concurrent AI and maritime safety rules aim to anchor global standards. North America-underpinned by US Navy outlays, Canadian Arctic logistics and Silicon Valley's connectivity ecosystems-remains influential. The convergence of defense and civil deployments in these regions provides a reinforcing feedback loop: defense funds prime early R&D, and commercial operators adopt matured components at lower unit costs.

- ABB Ltd.

- BAE Systems plc

- DNV AS

- Fugro NV

- Hanwha Corporation

- HD Hyundai Heavy Industries Co. Ltd.

- Kongsberg Gruppen ASA

- L3Harris Technologies, Inc.

- Marine AI Ltd.

- MITSUI E&S Group

- Praxis Automation Technology B.V.

- Rolls-Royce plc

- Sea Machines Robotics, Inc.

- Samsung Heavy Industries Co., Ltd.

- Wartsila Corporation

- Vigor Industrial LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Data-driven fleet optimization and remote operations

- 4.2.2 Decarbonization and fuel efficiency

- 4.2.3 Demand for advanced situational-awareness suites

- 4.2.4 Development of next-generation autonomous vessels

- 4.2.5 Defense push for unmanned surface vessels in navies

- 4.2.6 Edge-AI and 5G/LEO connectivity breakthroughs enabling real-time vessel autonomy

- 4.3 Market Restraints

- 4.3.1 Cyber-security vulnerabilities of remote navigation stacks

- 4.3.2 Regulatory fragmentation and flag-state variance

- 4.3.3 High retrofit capital outlay

- 4.3.4 Marine-insurance and liability uncertainties

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Autonomy Level

- 5.1.1 Partially Autonomous

- 5.1.2 Remotely Controlled

- 5.1.3 Fully Autonomous

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.3 By Ship Type

- 5.3.1 Cargo

- 5.3.2 Passenger

- 5.3.3 Offshore Support and Energy

- 5.3.4 Defense

- 5.3.5 Special Purpose

- 5.4 By End User

- 5.4.1 Commercial

- 5.4.2 Government and Military

- 5.5 By Propulsion

- 5.5.1 Fully Electric

- 5.5.2 Hybrid

- 5.5.3 Conventional

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Russia

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 BAE Systems plc

- 6.4.3 DNV AS

- 6.4.4 Fugro NV

- 6.4.5 Hanwha Corporation

- 6.4.6 HD Hyundai Heavy Industries Co. Ltd.

- 6.4.7 Kongsberg Gruppen ASA

- 6.4.8 L3Harris Technologies, Inc.

- 6.4.9 Marine AI Ltd.

- 6.4.10 MITSUI E&S Group

- 6.4.11 Praxis Automation Technology B.V.

- 6.4.12 Rolls-Royce plc

- 6.4.13 Sea Machines Robotics, Inc.

- 6.4.14 Samsung Heavy Industries Co., Ltd.

- 6.4.15 Wartsila Corporation

- 6.4.16 Vigor Industrial LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment