|

시장보고서

상품코드

1851151

상업 인쇄 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Commercial Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

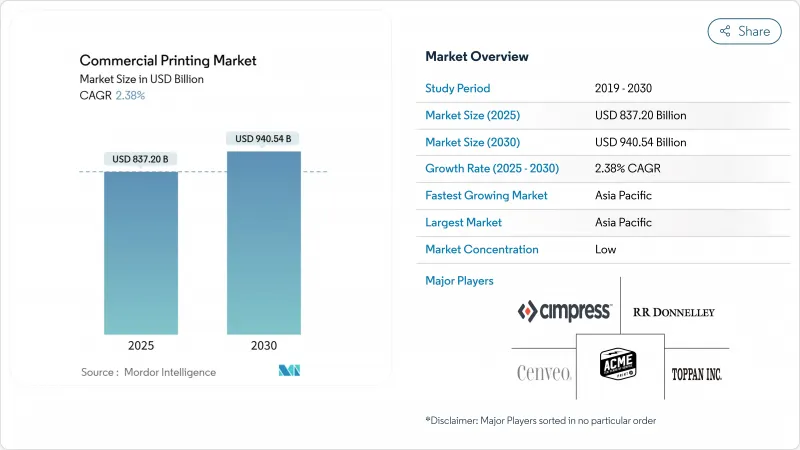

상업 인쇄 시장 규모는 2025년에 8,372억 달러로 추정되고, 2030년에는 9,405억 4,000만 달러에 이를 것으로 예측되며, CAGR 2.38%로 추이할 전망입니다.

이 실적은 상업 인쇄 시장이 패키징, 가변 데이터 서비스 및 지속 가능한 기판의 성장을 활용하면서 디지털 디스랩션에 적응하고 있음을 보여줍니다. 전자상거래에서 인쇄 패키징에 대한 지속적인 수요, 식물성 잉크로의 꾸준한 이동, 온디맨드 디지털 워크플로우의 광범위한 이용은 여전히 전통적인 출판 업무에 영향을 미치는 수익 압력을 완화하고 있습니다. 인쇄 워크플로우 자동화를 위한 인공지능에 대한 투자와 소비자의 거점 근처에 위치한 마이크로 팩토리 구상은 상업 인쇄 시장의 많은 진출기업에게 처리 능력 향상 및 수익성 개선이 기대됩니다. 동시에 대기업은 소프트웨어 벤더와 제휴하여 실시간 데이터 분석을 통합하려고 노력하고 있으며, 지역 전문가들은 DTP 및 소형 로트 프로모션 용도에서 틈새 위치를 개척하고 있습니다.

세계의 상업 인쇄 시장 동향 및 인사이트

주문형 포장 인쇄의 폭발적인 성장

전자상거래 브랜드는 신속한 제품 출시 및 지역 프로모션을 지원하므로 단기간에 더 자주 패키징을 선호합니다. 이 추세는 아시아태평양에서 가장 빠르게 진행되고 있으며, 현지화된 완성 센터에서는 소비자 가까이에서 인쇄되는 포장이 필요하며 재고 비용을 줄이고 진부화를 줄입니다.

개인화된 마케팅을 위한 가변 데이터 인쇄 채택 증가

북미와 유럽 광고주는 퍼스트 파티 데이터와 연결되는 맞춤형 메일러 및 패키지를 요청합니다. 대일본 인쇄는 2025년 '페르소나 인사이트' AI 툴을 도입하여 정부 인구통계 및 인쇄 워크플로우를 결합하여 단일 생산 경로에서 독특한 디자인 변형을 생성하고 있습니다. 데이터 분석과 디지털 인쇄기를 통합한 인쇄 회사는 프리미엄으로 서비스가 풍부한 계약을 획득했으며 기존 상업 인쇄 작업의 납기 지연을 보완하고 있습니다.

광고비의 디지털 미디어 채널로 계속적 이동

브랜드 소유자는 온라인 비디오 및 소셜 미디어에 예산을 배분하고 잡지 및 신문 인쇄 주문의 성장을 억제합니다. 인쇄 회사는 오프라인에서 온라인으로 원활하게 참여할 수 있는 QR 코드를 통합한 패키지 및 직접 메일 형식을 강조함으로써 이러한 감소를 상쇄합니다.

부문 분석

플렉소플랫폼은 연포장의 장척 인쇄에 유리한 경제성에 힘입어 2024년 매출의 41.07%를 유지했습니다. 디지털 잉크젯 솔루션의 상업용 인쇄 시장 규모는 브랜드가 빠른 아트웍 변경과 개별 캠페인을 요구하기 때문에 2030년까지 연평균 복합 성장률(CAGR) 3.45%로 확대될 것으로 예측됩니다. 지역 컨버터에서는 플렉소의 백색 레이어와 가변 잉크젯 컬러를 결합한 하이브리드 라인의 도입이 진행되고 있어 셋업 시간과 낭비를 삭감하고 있습니다. 2028년까지는 중간 규모의 디지털 비용이 동등해질 것으로 예상되며, 음료 라벨과 같은 SKU가 많은 분야에서는 플렉소의 우위성이 상실됩니다.

인공지능 가이드와의 조정 및 자동 작업 전환의 진보로 노동 투입량을 줄이고 가동 시간을 극대화하고 있습니다. Multi-Label Tech-Print의 Domino N610i와 같은 투자는 중규모 컨버터가 6색, 600dpi 엔진을 활용하여 메탈릭과 고농도 흰색을 1패스로 인쇄하는 방법을 보여줍니다. 수성 잉크젯 용액은 용매 기반 플렉소 블렌드보다 VOC 배출량이 적기 때문에 인쇄 회사는 엄격한 대기질 규제를 충족시킬 수 있습니다.

패키징은 2024년 상업 인쇄 시장 점유율의 44.08%를 차지했으며, 전자상거래의 소포량과 브랜드 프리미엄화를 배경으로 CAGR 3.07%로 상승할 전망입니다. 접이식 판지 및 플렉서블 파우치는 화장품, 영양 보조 식품, 조리된 식품 등 선명한 선반 진열에 의존하는 분야에서 사용됩니다. 신문, 잡지, 소프트 커버 서적 등의 출판물은 특히 북미와 서유럽에서 판매량이 감소하고 있습니다. 그러나 재생지에 인쇄된 만화와 작은 로트 문예서는 환경 의식이 높은 소비자들 사이에서 틈새 성장을 기록하고 있습니다.

상업 인쇄 산업의 벤더는 골판지 상자, 매장 디스플레이, 개인화된 인서트 카드를 묶은 '캠페인 키트'를 제공함으로써 다양화를 도모하고 있습니다. 패키지에 내장된 인쇄 전자 제품은 온도 모니터링 및 위조 방지를 가능하게 하며, 아시아태평양 제약 회사 및 고급 브랜드에서 높은 평가를 받고 있습니다. 포장의 탄력성은 다른 부문에서 주기적인 광고 지출 패턴을 상쇄하고 인쇄 회사에 수익의 기둥을 제공합니다.

상업 인쇄 시장 보고서는 인쇄 유형별(오프셋 리소그래피, 디지털 잉크젯, 플렉소 인쇄, 스크린 등), 용도별(패키징, 광고, 출판, 기타), 인쇄 소재별(종이 및 골판지, 직물 및 섬유 등), 형식별(대형 인쇄, 기타), 지역별(북미, 유럽, 아시아태평양, 남미, 중동, 아프리카)로 구분됩니다.

지역 분석

아시아태평양은 2024년에 45.64%의 매출을 차지하였고, 2030년까지 CAGR 3.28%로 성장이 예측됩니다. 이는 소비자 포장 상품 생산, 국내 전자상거래 양, 인프라 프로젝트에 대한 정부의 자극책이 인쇄 수요를 확대하기 때문입니다. 중국만으로도 연간 수백 개의 골판지 가공 라인이 증설되는 한편, 인도의 라벨 부문은 GST의 전개에 의해 물류 채널 전체에서 표준화된 바코드 식별이 의무화되어 혜택을 받습니다. 지역 브랜드는 QR 코드가 있는 스마트 패키징을 적극적으로 지정하여 모바일 퍼스트 소비자의 로열티를 높이고 있습니다.

북미는 성장이 완만하지만 세계 생산량의 상당 부분을 유지하고 있습니다. 미국의 상업 인쇄 시장 규모는 수요가 데이터 주도의 다이렉트 메일, 의약품 접힌 전단지, 고급 패키지로 이동하고 있기 때문에 안정되어 있습니다. 캐나다의 인쇄회사는 국산 인쇄 컨텐츠를 지지하는 교육 출판 지령에 힘입어 작은 로트의 서적 생산에 주력하고 있습니다.

유럽에서는 일반 상업 인쇄의 수량이 평평하지만 C2C 재활용 가능한 기판과 식물성 오일 잉크에 대한 투자가 가속화되고 있습니다. 독일에서는 종이 기반 커피 컵의 보증금 리턴 시스템을 시험적으로 도입했으며, 컨버터는 퇴비화 가능성이 인증된 장벽 코팅 보드 테스트에 박차를 가하고 있습니다. 일회용 플라스틱 팩의 포맷에 관한 EU 규정은 중기적으로 파이버 보드에 수량 증가를 초래할 것으로 보입니다.

라틴아메리카와 중동 및 아프리카는 상업 인쇄 시장에서 차지하는 비율은 작지만 큰 상승 여지가 있습니다. 브라질의 PET 재활용률은 2025년에 56.4%로 추정되며, 식품 브랜드가 PCR을 많이 사용한 라벨이나 플렉서블 파우치로 전환할 수 있게 되어 그 결과 인쇄 수량이 창출됩니다. 걸프 협력 회의 국가는 유제품, 음료 및 개인 관리 클러스터에 서비스를 제공하는 패키징 공장을 보유한 새로운 산업 지대를 건설하고 있으며 오프셋 인쇄기 및 그라비아 인쇄기 당면 수요를 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 온디맨드 포장 인쇄의 폭발적 성장

- 개인화된 마케팅을 위한 가변 데이터 프린팅 채택 증가

- 소매 및 CPG 브랜드로부터의 판촉 인쇄물에 대한 지속적 수요

- 친환경 기재 및 식물성 잉크로의 이행

- 프린티드 일렉트로닉스(RFID, NFC)의 포장 라벨에 대한 통합

- 고객에 가까운 마이크로 공장 '서비스로서의 프린트' 허브의 출현

- 시장 성장 억제요인

- 광고비의 디지털 미디어 채널로의 시프트가 진행중

- 종이, 잉크, 에너지 투입 가격의 변동

- 기존 잉크에 대한 엄격한 VOC 규제 및 화학물질 사용 규제

- 신형 디지털 인쇄기용 반도체 부품의 부족

- 공급망 분석

- 규제 상황

- 기술의 전망

- 투자 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 인쇄 유형별

- 오프셋 리소그래피

- 디지털 잉크젯

- 플렉소 인쇄

- 스크린

- 그라비아

- 기타 인쇄 유형

- 용도별

- 패키지

- 광고

- 출판

- 서적

- 잡지

- 신문

- 기타 출판

- 기업 및 거래 인쇄

- 기타 용도

- 인쇄 재료별

- 종이 및 골판지

- 플라스틱 및 합성 기재

- 원단 및 섬유

- 금속 박

- 기타 소재

- 포맷별

- 대형 인쇄

- 소판 인쇄

- 직접 오브젝트 인쇄

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주, 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 케냐

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Toppan Inc.

- Dai Nippon Printing Co., Ltd.

- RR Donnelley & Sons Company

- Quad/Graphics Inc.

- Transcontinental Inc.

- Cenveo Worldwide Limited

- Cimpress plc

- Deluxe Corporation

- Shutterfly LLC

- LSC Communications LLC

- Mondi Group

- Printpack Inc.

- Multi-Color Corporation

- ACME Printing

- O'Neil Printing

- Xerox Corporation(Print Services)

- Smurfit Westrock(Print and Packaging)

- Berry Global Group(Graphics Services)

- Seiko Epson Corporation(Commercial Inkjet Systems)

- HP Inc.(PageWide Industrial)

제7장 시장 기회 및 향후 전망

AJY 25.11.12The commercial printing market size is valued at USD 837.20 billion in 2025 and is forecast to reach USD 940.54 billion by 2030, advancing at a 2.38% CAGR.

This performance indicates that the commercial printing market is adapting to digital disruption while capitalizing on growth in packaging, variable-data services, and sustainable substrates. Ongoing demand for printed packaging in e-commerce, a steady shift toward vegetable-based inks, and wider use of on-demand digital workflows are cushioning revenue pressures that still affect traditional publishing work. Investments in artificial intelligence for print workflow automation, together with micro-factory concepts located near consumer hubs, are expected to raise throughput and improve profitability for many participants in the commercial printing market. At the same time, larger firms are pursuing alliances with software vendors to integrate real-time data analytics, while regional specialists are carving out niche positions in direct-to-object and short-run promotional applications.

Global Commercial Printing Market Trends and Insights

Explosive Growth in On-Demand Packaging Print Runs

E-commerce brands increasingly favor shorter, more frequent packaging runs to support fast product launches and regional promotions. A 2024 installation of a Domino N610i digital label press by Multi-Label Tech-Print in Ahmedabad underscores the migration toward high-throughput digital lines able to process hundreds of SKUs with minimal changeover time.The trend is advancing most rapidly in Asia-Pacific, where localized fulfillment centers require packaging that is printed close to consumers, limiting inventory costs and reducing obsolescence.

Rising Adoption of Variable-Data Printing for Personalized Marketing

Advertisers in North America and Europe are demanding individualized mailers and packaging tied to first-party data. Dai Nippon Printing introduced its "Persona Insight" AI tool in 2025, combining government demographic statistics with print workflows that generate unique design variants in one production pass. Printers that integrate data analytics and digital presses are securing premium, service-rich contracts that offset slower run lengths in traditional commercial jobs.

Ongoing Shift of Advertising Spend to Digital Media Channels

Brand owners allocate budget toward online video and social media, curbing growth in magazine and newspaper print orders. Printers offset the decline by emphasizing packaging and direct mail formats that integrate QR codes for seamless offline-to-online engagement.

Other drivers and restraints analyzed in the detailed report include:

- Sustained Demand for Promotional Print from Retail and CPG Brands

- Transition Toward Eco-Friendly Substrates and Vegetable-Based Inks

- Volatile Prices of Paper, Ink and Energy Inputs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flexographic platforms retained 41.07% revenue in 2024, underpinned by favorable economics for long runs on flexible packaging. The commercial printing market size for digital inkjet solutions is projected to widen by 3.45% CAGR to 2030 as brands demand quicker artwork changes and individualized campaigns. Regional converters increasingly deploy hybrid lines, marrying flexo white layers with variable inkjet color to cut setup times and waste. Digital cost parity at mid-length runs is expected before 2028, eroding flexo's historical edge in SKU-rich sectors such as beverage labels.

Advances in AI-guided registration and automated job changeovers are shrinking labor input and maximizing uptime. Investments like Multi-Label Tech-Print's Domino N610i show how medium-sized converters leverage six-color, 600 dpi engines to print metallics and high-opacity whites in one pass. Environmental compliance is another driver: water-borne inkjet fluids emit lower VOCs than solvent-based flexo blends, helping printers satisfy tightening air-quality rules.

Packaging held 44.08% of commercial printing market share in 2024 and will rise at a 3.07% CAGR on the back of e-commerce parcel volumes and brand premiumization. Folding cartons and flexible pouches serve cosmetics, nutraceuticals, and ready-to-eat meals, sectors that rely on vivid shelf appeal. Publishing work-newspapers, magazines, softcover books-experiences ongoing volume erosion, especially in North America and Western Europe. Yet manga and small-batch literary titles printed on recycled paper are registering niche growth among environmentally conscious consumers.

Commercial printing industry vendors diversify by offering "campaign kits" that bundle corrugated shipper boxes, point-of-sale displays, and personalized insert cards. Printed electronics embedded in packages enable temperature monitoring and anti-counterfeiting, features valued by pharmaceutical and luxury brands in Asia-Pacific. Packaging's resilience gives printers an anchor revenue stream, offsetting cyclical ad-spend patterns in other segments.

The Commercial Printing Market Report is Segmented by Printing Type (Offset Lithography, Digital Inkjet, Flexographic, Screen, and More), Application (Packaging, Advertising, Publishing, and More), Print Material (Paper and Cardboard, Fabric and Textiles, and More), Format (Large-Format Printing, and More) and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa).

Geography Analysis

Asia-Pacific dominated revenue with 45.64% in 2024 and is projected to post a 3.28% CAGR through 2030 as consumer packaged goods output, domestic e-commerce volumes, and government stimulus for infrastructure projects expand print demand. China alone adds hundreds of corrugated converting lines annually, while India's label sector benefits from GST roll-out mandating standardized barcode identification across logistics channels. Regional brands actively specify QR-code smart packaging to build loyalty among mobile-first consumers.

North America maintains a sizeable slice of global output, although growth is modest. The commercial printing market size in the United States is steady as demand migrates toward data-driven direct mail, pharmaceutical inserts, and luxury packaging. Canada's printers focus on short-run book production fueled by educational publishing mandates favoring domestically printed content.

Europe shows flat volume in general commercial work but accelerating investment in C2C recyclable substrates and vegetable-oil inks. Germany is piloting deposit-return systems for paper-based coffee cups, spurring converters to test barrier-coated boards certified for compostability. EU regulations on single-use plastic pack formats will likely channel incremental volume to fiberboard over the medium term.

Latin America and the Middle East & Africa together account for a smaller proportion of the commercial printing market but represent meaningful upside. Brazil's PET recycling rate reached 56.4% in 2025, allowing food brands to switch to PCR-rich labels and flexible pouches, which in turn creates print volume. Gulf Cooperation Council states are building new industrial zones that house packaging plants serving dairy, beverage, and personal-care clusters, underpinning near-term demand for offset and gravure equipment.

- Toppan Inc.

- Dai Nippon Printing Co., Ltd.

- R.R. Donnelley & Sons Company

- Quad/Graphics Inc.

- Transcontinental Inc.

- Cenveo Worldwide Limited

- Cimpress plc

- Deluxe Corporation

- Shutterfly LLC

- LSC Communications LLC

- Mondi Group

- Printpack Inc.

- Multi-Color Corporation

- ACME Printing

- O'Neil Printing

- Xerox Corporation (Print Services)

- Smurfit Westrock (Print and Packaging)

- Berry Global Group (Graphics Services)

- Seiko Epson Corporation (Commercial Inkjet Systems)

- HP Inc. (PageWide Industrial)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive growth in on-demand packaging print runs

- 4.2.2 Rising adoption of variable-data printing for personalized marketing

- 4.2.3 Sustained demand for promotional print from retail and CPG brands

- 4.2.4 Transition toward eco-friendly substrates and vegetable-based inks

- 4.2.5 Integration of printed electronics (RFID, NFC) into packaging and labels

- 4.2.6 Emergence of micro-factory "print-as-a-service" hubs close to customers

- 4.3 Market Restraints

- 4.3.1 Ongoing shift of advertising spend to digital media channels

- 4.3.2 Volatile prices of paper, ink and energy inputs

- 4.3.3 Stringent VOC and chemical-use regulations on conventional inks

- 4.3.4 Shortage of semiconductor components for new digital presses

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Investment Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Printing Type

- 5.1.1 Offset Lithography

- 5.1.2 Digital Inkjet

- 5.1.3 Flexographic

- 5.1.4 Screen

- 5.1.5 Gravure

- 5.1.6 Other Printing Types

- 5.2 By Application

- 5.2.1 Packaging

- 5.2.2 Advertising

- 5.2.3 Publishing

- 5.2.3.1 Books

- 5.2.3.2 Magazines

- 5.2.3.3 Newspapers

- 5.2.3.4 Other Publishing

- 5.2.4 Corporate and Transactional Printing

- 5.2.5 Other Application

- 5.3 By Print Material

- 5.3.1 Paper and Cardboard

- 5.3.2 Plastic and Synthetic Substrates

- 5.3.3 Fabric and Textiles

- 5.3.4 Metal and Foils

- 5.3.5 Other Materials

- 5.4 By Format

- 5.4.1 Large-Format Printing

- 5.4.2 Small-Format Printing

- 5.4.3 Direct-to-Object Printing

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Kenya

- 5.5.4.2.4 Rest of Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Toppan Inc.

- 6.4.2 Dai Nippon Printing Co., Ltd.

- 6.4.3 R.R. Donnelley & Sons Company

- 6.4.4 Quad/Graphics Inc.

- 6.4.5 Transcontinental Inc.

- 6.4.6 Cenveo Worldwide Limited

- 6.4.7 Cimpress plc

- 6.4.8 Deluxe Corporation

- 6.4.9 Shutterfly LLC

- 6.4.10 LSC Communications LLC

- 6.4.11 Mondi Group

- 6.4.12 Printpack Inc.

- 6.4.13 Multi-Color Corporation

- 6.4.14 ACME Printing

- 6.4.15 O'Neil Printing

- 6.4.16 Xerox Corporation (Print Services)

- 6.4.17 Smurfit Westrock (Print and Packaging)

- 6.4.18 Berry Global Group (Graphics Services)

- 6.4.19 Seiko Epson Corporation (Commercial Inkjet Systems)

- 6.4.20 HP Inc. (PageWide Industrial)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment