|

시장보고서

상품코드

1851161

내시경하 혈관 채취 : 시장 점유율 분석, 산업 동향 & 통계, 성장 예측(2025-2030년)Endoscopic Vessel Harvesting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

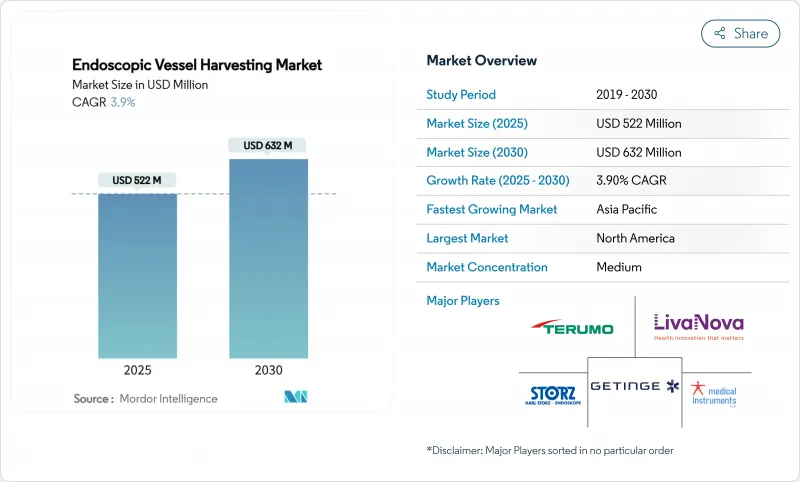

내시경하 혈관 채취 시장 규모는 2025년 5억 2,200만 달러에 이르고, CAGR 3.9%를 나타내 2030년에는 6억 3,200만 달러에 이를 것으로 예상됩니다.

심장 수술 건수 증가, 낮은 침습적인 도관 조달에 대한 외과의의 기호의 높아짐, 꾸준한 제품 혁신이 이 시장 확대를 지지하고 있습니다. 밸류 베이스 케어의 틀이 보다 짧은 입원 기간과 더 낮은 합병증 발생률에 보상하는 고소득 지역에서 수요는 여전히 가장 왕성합니다. 시각화, 배고픈, 일회용 키트를 번들로 제공하는 하이브리드 플랫폼은 조달을 간소화하고 기술의 품질을 표준화하기 위해 지지를 받고 있습니다. 반면에 최근 장비 리콜을 통해 병원은 공급업체의 품질 시스템을 더욱 엄격하게 점검하고 시장 조사 후 실적이 풍부한 공급업체로의 전환을 촉구하고 있습니다.

세계의 내시경하 혈관 채취 시장 동향과 인사이트

심혈관 질환의 세계 부담 증가

심혈관 질환은 미국 성인의 약 절반이 고통을 받고 있으며 많은 신흥 국가에서도 증가의 길을 따라가고 있습니다. 수술 건수가 증가함에 따라 효율적인 도관 채취는 희박한 병상 용량과 재입원 패널티를 관리하는 수술 프로그램에 전략적으로 필요하게 되었습니다. 내시경 기술을 도입하고 있는 병원에서는 상처 감염의 감소나 보행 속도의 향상이 보고되고 있어, 이것은 최신의 일괄 지불 인센티브에 합치한 성과입니다. 당뇨병이나 고혈압을 앓고 있는 노인층에서는 그 부담이 특히 크고, 내구성이 있는 그래프트나 이환율이 낮은 액세스 부위의 필요성이 높아지고 있습니다. 각국 정부는 심장 센터 오브 엑설런스에 자금을 투입하고 예측 가능한 학습 곡선과 직원의 이직률의 저하를 약속하는 통합 EVH 플랫폼의 조달을 촉진하고 있습니다. 장기적인 그래프트 개존성과 비용 상쇄를 증명할 수 있는 공급업체는 이러한 역학적인 추풍으로부터 최대의 이익을 얻을 것입니다.

최소 침습으로 채취에 대한 선호도 증가

근본적인 데이터에 따르면, 다리 창합 병증은 내시경 접근법에서 0.82%인 반면 개복 채취에서는 3%를 나타낼 전망입니다. 환자 보고서에 의한 결과 평가는 흉터가 최소화되고 이동이 빠르다는 것을 지속적으로 뒷받침하며, 이 지표는 현재 많은 성과 보상 대시보드에 통합되어 있습니다. 흉터 온존 프로그램을 판매하는 병원은 평판을 올리고 특히 시장 경쟁이 심한 도시에서는 소개 건수 증가로 이어집니다. 가상현실 시뮬레이션의 광범위한 채택으로 운영자의 학습 곡선이 단축되고 투시 검사에 소요되는 시간은 약 1/3로 단축되었습니다. 그럼에도 불구하고, 외과의사의 자신감을 잃게 하는 합병증의 조기 발생을 피하기 위해, 센터는 구조화된 지도에 투자해야 합니다. 기구의 설계자는 인체공학에 근거한 핸들이나 자동 절단 컨트롤로 대응해, 숙련 곡선을 한층 더 평탄화하고 있습니다.

대체 혈행 재건 요법의 가용성

복잡한 경피적 관상동맥 인터벤션 절차의 급속한 개선으로 인해 이전에 관상동맥 우회술이 기본이었던 다지 사례의 일부가 빨려 들고 있습니다. 당뇨병 환자와 확산성 질환은 CABG의 우위를 유지하지만 특정 지역에서는 개심술의 수가 감소하고 EVH 판매가 억제될 수 있습니다. 그러나 현재 남아있는 수술 사례는 낮은 침습 도관 채취가 큰 이익을 초래하는 고위험 프로파일에 편향되어 있습니다. 그러므로 장비 제조업체는 EVH를 여전히 이식편이 필요한 환자의 하위 집합에 대한 정밀한 도구로 자리매김하고, 개존성과 상처 치유에서 개심술에 대한 우위를 강조합니다.

부문 분석

EVH 시스템은 2024년 3억 4,600만 달러를 창출해 내시경하 혈관 채취 시장의 66.35%에 해당했습니다. 병원은 이러한 자본 자산을 5-7년에 한 번 구매하므로 장비 공급업체는 다년간 서비스 계약을 체결합니다. 부속품·소모품 카테고리는 절대액으로는 작은 것, 수기 회수에 맞춘 연금 형식의 수익에 의해 CAGR 8.25%를 나타낼 전망입니다. 블레이드, 스코프 및 CO2 라인이 번들된 키트는 케이스 설정을 간소화하고 호환성을 보장하며 구매 관리자가 중시하는 편리함입니다.

정기 소모품은 현장에서 멸균 능력이 없는 외래 수술 센터(ASC)에 특히 매력적입니다. 한편, 자본 시스템 간의 경쟁적 차별화는 현재 이미지 해상도, 인체공학 기반 핸드피스, 자격증명을 목적으로 사용 통계를 기록하는 분석 대시보드에 달려 있습니다. Getinge의 Hemopro 3 배포는 과거의 리콜 후 외과의사를 안심하도록 설계된 안전성이 강화된 시스템에 축발을 보여줍니다.

요골 동맥 도관은 특히 2024년 판매량의 42.53%를 차지했으며, 특히 청소년 및 당뇨병 환자에서 우수한 10년 개존율을 보였습니다. 외과의사는 양측 요골 전략을 채택하는 경우가 많아 시스템 활용도를 높이고 있습니다. 반대로, 복재 정맥 이식편은 3개 이상의 원위 표적을 우회할 필요가 있는 경우에는 여전히 필수적이며 CAGR은 7.85%를 나타낼 전망입니다. 노터치로 혈관 주위를 온존한 채취를 지지하는 근거가 정맥의 질에 관한 초기의 회의적인 견해를 완화하고 있습니다.

장비 공급업체는 내피의 외상을 줄이기 위해 더 얇은 범위와 저압 기복 프로토콜을 개발하고 긴 도관을위한 오픈 수확을 선호하는 회의론자에게 호소합니다. 현재 병원은 병렬 워크플로우를 실행하고 있습니다. 즉, 하이펜시의 요구에는 레이디얼, 멀티 그래프트 사례에는 최적화된 복재 정맥이라는 상태이며, 이 동향은 범용성이 높은 시스템 플랫폼에 대한 수요를 높이고 있습니다.

지역 분석

북미는 2024년 매출액의 42.82%를 차지했으며, 견조한 상환과 학술센터 및 지역병원에서 높은 수술밀도에 지지를 받았습니다. CMS의 보험 적용범위에서는 임상적으로 정당화되는 경우에는 일관되게 EVH가 지지되고 있으며, 번들 결제 파일럿에서는 입원기간의 단축이 평가되고 있습니다. 업그레이드된 시스템의 510(k) 허가를 포함한 지속적인 FDA 참여는 기술 혁신의 파이프라인을 활발하게 하고 있습니다. STS 및 AATS와 같은 연수 컨소시엄은 EVH 모듈을 연수의 커리큘럼에 통합하여 널리 역량을 강화하고 있습니다.

유럽에서는 데이터 주도 프로토콜과 국경을 넘은 임상시험을 통해 꾸준히 도입이 진행되고 있습니다. 그러나 단일 지불 제도의 예산 상한은 갱신주기를 지연시키고 공급업체는 비용 효과를 중시해야 합니다. 스칸디나비아 병원은 환경 지침을 충족하기 위해 재사용 가능한 범위를 선구적으로 도입했으며, 이 모델은 현재 독일과 프랑스에서 모방되고 있습니다. 자본 예산의 제약에 직면하는 지중해 연안 의료 시스템은 장비 초기 투자를 수술 당 요금으로 변환하는 서비스리스 계약에 기울고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 10.13%로 가장 빠르게 성장하는 지역으로, 일본의 고령화, 중국의 중간층 확대, 3차 심장 센터에 대한 정부 투자가 그 원동력이 되고 있습니다. 일본의 외과의사는 완전한 내시경 로봇 수술을 채용해, 지역 전체에서 칭찬되는 성능 기준을 설정하고 있습니다. 중국의 규제 당국은 공중 보건 목표에 필수적인 것으로 간주되는 심장 의료기기의 신속한 도입을 추진하고 있지만, 지방 상환에는 여전히 변동이 있습니다. 인도와 동남아시아에서는 교육 병목 현상이 잠재적인 수요를 제한하기 때문에 공급업체는 의과대학과 제휴하여 하베스팅 휄로우십을 구축하고 있습니다.

남미에서는 브라질의 관민병원 네트워크가 CABG의 대량 시행을 선도하고 완만한 성장을 기록하고 있습니다. 수입세와 환율변동이 해외에서의 진입을 막아 현지생산과의 제휴를 촉구하고 있습니다. 중동 및 아프리카는 걸프 국가와 남아프리카의 주요 심장병 연구소와 연결되는 틈새 기회를 제공하지만 보험 적용 범위가 좁아지고 외과 의사 부족이 보급을 방해합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 심장혈관 질환의 세계적 부담 증가

- 저침습 채취에의 기호의 고조

- 오프 펌프 CABG 수술의 채용 증가

- 병원 비용 절감 오픈에서 EVH로의 이동

- 몰입형 시뮬레이터를 이용한 외과의사 훈련의 보급률

- 서플라이 체인이 견인하는 오픈 디스포저블로부터의 전환

- 시장 성장 억제요인

- 대체혈행재건요법의 이용가능성

- 여러 국가에서 불리한 보험 상환

- 외과의의 신뢰를 해치는 클래스 1 리콜

- 험한 학습 곡선과 채취자 부족

- Porter's Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- EVH 시스템

- 내시경

- 액세서리 및 일회용 제품

- 혈관 유형별

- 복재정맥

- 요골동맥

- 기타

- 사용성별

- 일회용

- 재사용 가능

- 용도별

- 관상동맥질환(CAD)

- 말초동맥질환(PAD)

- 최종 사용자별

- 병원

- 외래 수술 센터(ASC)

- 심장 전문 클리닉

- 채취 기술별

- 폐쇄 터널 CO2 주입

- 비접촉식/CO2 프리

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Getinge AB

- Terumo Corp.

- LivaNova PLC

- KARL STORZ SE & Co. KG

- Saphena Medical Inc.

- Medical Instruments SpA

- Medtronic plc

- Olympus Corp.

- Conmed Corp.

- B. Braun Melsungen AG

- Cardio Medical GmbH

- Valeriot GmbH

- LeMaitre Vascular Inc.

- Boston Scientific Corp.

- Ethicon(J&J)

- Smith & Nephew plc

- Stryker Corp.

- Teleflex Inc.

- CardiMedical Inc.

제7장 시장 기회와 향후 전망

KTH 25.11.20The endoscopic vessel harvesting market size reached USD 522 million in 2025 and is projected to attain USD 632 million by 2030, reflecting a 3.9% CAGR.

Growing cardiac surgery volumes, heightened surgeon preference for minimally invasive conduit procurement, and steady product innovation all sustain this measured expansion. Demand remains most intense in high-income regions where value-based care frameworks reward shorter stays and lower complication rates. Hybrid platforms that bundle visualization, insufflation, and disposable kits are gaining traction because they simplify procurement and standardize procedural quality. Meanwhile, recent device recalls are prompting hospitals to scrutinize supplier quality systems more closely, encouraging a flight to vendors with strong post-market surveillance records.

Global Endoscopic Vessel Harvesting Market Trends and Insights

Increasing Global Burden of Cardiovascular Diseases

Cardiovascular pathology affects nearly half of U.S. adults and continues to climb in many emerging economies. Growing procedure volumes make efficient conduit harvesting a strategic necessity for surgical programs managing tight bed capacity and readmission penalties. Hospitals adopting endoscopic techniques report fewer wound infections and faster ambulation, outcomes that align with modern bundled-payment incentives. The burden remains particularly high among aging cohorts with diabetes and hypertension, reinforcing the need for durable grafts and low-morbidity access sites. Governments are channeling funds into cardiac centers of excellence, catalyzing procurement of integrated EVH platforms that promise predictable learning curves and reduced staff turnover. Vendors able to document long-term graft patency and cost offsets stand to benefit most from these epidemiological tailwinds.

Growing Preference for Minimally-Invasive Harvesting

Prospective data show leg wound complications of 0.82% with endoscopic approaches versus 3% for open extraction. Patient-reported outcome measures consistently favor minimal scarring and quicker mobility, metrics now embedded in many pay-for-performance dashboards. Hospitals marketing "scar-sparing" programs gain reputational lift that translates into higher referral volumes, especially in competitive urban catchments. Widespread adoption of virtual-reality simulation has shortened operator learning curves and cut fluoroscopy exposure times by nearly one-third. Nonetheless, centers must invest in structured mentorship to avoid early complication clusters that can erode surgeon confidence. Device designers are responding with ergonomic handles and automated cutting controls to further flatten proficiency curves.

Availability of Alternative Revascularization Therapies

Rapid improvements in complex percutaneous coronary intervention techniques are siphoning off some multi-vessel cases that once defaulted to coronary artery bypass grafting. Although CABG retains superiority in diabetics and diffuse disease, declining open-heart volumes in certain geographies could curb EVH unit sales. Yet, the remaining surgical cases now skew toward higher-risk profiles where minimally invasive conduit harvest offers outsized benefits. Device makers therefore position EVH as a precision tool for the subset of patients who still require grafts, emphasizing patency and wound-healing advantages versus open techniques.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Off-Pump CABG Surgeries

- Hospitals' Cost-Saving Shift from Open to EVH

- Unfavorable Reimbursement in Several Countries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

EVH systems generated USD 346 million in 2024, equal to 66.35% of the endoscopic vessel harvesting market. Hospitals purchase these capital assets once every 5-7 years, locking equipment vendors into multiyear service contracts. The accessories and disposables category, though smaller in absolute value, is growing at an 8.25% CAGR thanks to its annuity-style revenue that aligns with procedure counts. Bundled kits containing blades, scopes, and CO2 lines simplify case setup and ensure compatibility, a convenience that purchasing managers value.

Recurring consumables are particularly attractive to ambulatory surgical centers that lack onsite sterilization capacity. Meanwhile, competitive differentiation among capital systems now hinges on image resolution, ergonomic handpieces, and analytics dashboards that log usage statistics for credentialing purposes. Getinge's Hemopro 3 rollout exemplifies this pivot toward safety-enhanced systems designed to reassure surgeons following prior recalls.

Radial artery conduits captured 42.53% of 2024 volume owing to superior 10-year patency, especially in younger and diabetic patients. Surgeons increasingly adopt bilateral radial strategies, boosting system utilization. Conversely, saphenous vein grafting remains indispensable when three or more distal targets must be bypassed, explaining its projected 7.85% CAGR. Evidence supporting no-touch, perivascular-preserving harvest has mitigated early skepticism regarding vein quality.

Device vendors are developing slimmer scopes and lower-pressure insufflation protocols to reduce endothelial trauma, thereby appealing to skeptics who still prefer open harvest for long conduits. Hospitals now run parallel workflows: radial for high-patency needs and optimized saphenous for multi-graft cases, a trend that increases demand for versatile system platforms.

The Endoscopic Vessel Harvesting Market Report is Segmented by Product (EVH Systems and More), Vessel Type (Saphenous Vein and More), Usability (Disposable and Reusable), Application (Coronary Artery Disease and Peripheral Artery Disease), End-User (Hospitals and More), Harvesting Technique (Closed-Tunnel CO2 Insufflation and No-Touch), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 42.82% of 2024 turnover, underpinned by robust reimbursement and high procedural density across academic centers and community hospitals. CMS coverage consistently endorses EVH when clinically justified, and bundled-payment pilots reward shorter length of stay. Ongoing FDA engagement, including 510(k) clearances for upgraded systems, keeps innovation pipelines active. Training consortia such as STS and AATS integrate EVH modules into resident curricula, reinforcing widespread competence.

Europe follows with steady uptake driven by data-driven protocols and cross-border trials. Yet, budget caps in single-payer systems delay refresh cycles, compelling vendors to emphasize cost-utility. Scandinavian hospitals pioneered reusable scopes to satisfy environmental directives, a model now emulated in Germany and France. Mediterranean health systems, facing constrained capital budgets, gravitate toward service-leasing contracts that convert upfront equipment outlays into per-procedure fees.

Asia-Pacific is the fastest-growing territory at 10.13% CAGR through 2030, fueled by Japan's aging population, China's expanding middle class, and government investments in tertiary cardiac centers. Japanese surgeons have embraced totally endoscopic robotic harvests, setting performance benchmarks admired across the region. Chinese regulators increasingly fast-track cardiac devices deemed essential to public-health goals, but provincial reimbursement remains uneven. India and Southeast Asia show latent demand limited by training bottlenecks; therefore, vendors partner with medical colleges to build harvesting fellowships.

South America records moderate growth, spearheaded by Brazil's public-private hospital network that undertakes high-volume CABG. Import taxes and currency volatility challenge foreign entrants, encouraging localized production partnerships. The Middle East and Africa present niche opportunities tied to flagship cardiac institutes in the Gulf and South Africa, yet widespread adoption is hampered by limited insurance coverage and surgeon shortages.

- Getinge

- Terumo Corp.

- LivaNova

- Karl Storz

- Saphena Medical Inc.

- Medical Instruments SpA

- Medtronic

- Olympus Corp.

- Conmed

- B. Braun

- Cardio Medical GmbH

- Valeriot GmbH

- LeMaitre Vascular

- Boston Scientific

- Ethicon (J&J)

- Smiths Group

- Stryker

- Teleflex

- CardiMedical Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Global Burden Of Cardiovascular Diseases

- 4.2.2 Growing Preference For Minimally-Invasive Harvesting

- 4.2.3 Rising Adoption Of Off-Pump CABG Surgeries

- 4.2.4 Hospitals Cost Saving Shift From Open To EVH

- 4.2.5 Immersive Simulator-Based Surgeon Training Uptake

- 4.2.6 Supply-Chain Driven Switch From Open Disposables

- 4.3 Market Restraints

- 4.3.1 Availability Of Alternative Revascularization Therapies

- 4.3.2 Unfavorable Reimbursement In Several Countries

- 4.3.3 Class-I Recalls Denting Surgeon Confidence

- 4.3.4 Steep Learning Curve & Harvester Shortage

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 EVH Systems

- 5.1.2 Endoscopes

- 5.1.3 Accessories & Disposables

- 5.2 By Vessel Type

- 5.2.1 Saphenous Vein

- 5.2.2 Radial Artery

- 5.2.3 Others

- 5.3 By Usability

- 5.3.1 Disposable

- 5.3.2 Re-usable

- 5.4 By Application

- 5.4.1 Coronary Artery Disease (CAD)

- 5.4.2 Peripheral Artery Disease (PAD)

- 5.5 By End-user

- 5.5.1 Hospitals

- 5.5.2 Ambulatory Surgical Centers

- 5.5.3 Cardiac Specialty Clinics

- 5.6 By Harvesting Technique

- 5.6.1 Closed-tunnel CO? insufflation

- 5.6.2 No-touch / CO?-free

- 5.7 Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Getinge AB

- 6.3.2 Terumo Corp.

- 6.3.3 LivaNova PLC

- 6.3.4 KARL STORZ SE & Co. KG

- 6.3.5 Saphena Medical Inc.

- 6.3.6 Medical Instruments SpA

- 6.3.7 Medtronic plc

- 6.3.8 Olympus Corp.

- 6.3.9 Conmed Corp.

- 6.3.10 B. Braun Melsungen AG

- 6.3.11 Cardio Medical GmbH

- 6.3.12 Valeriot GmbH

- 6.3.13 LeMaitre Vascular Inc.

- 6.3.14 Boston Scientific Corp.

- 6.3.15 Ethicon (J&J)

- 6.3.16 Smith & Nephew plc

- 6.3.17 Stryker Corp.

- 6.3.18 Teleflex Inc.

- 6.3.19 CardiMedical Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment