|

시장보고서

상품코드

1851173

소화관 출혈 치료 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Gastrointestinal Bleeding Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

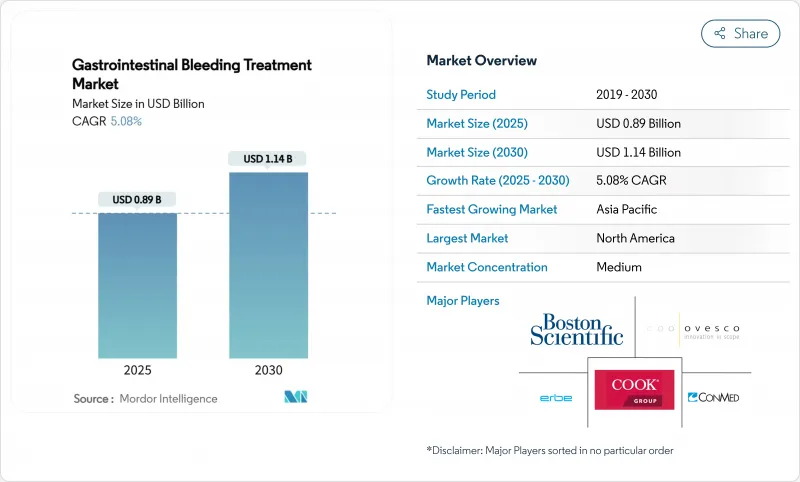

세계의 소화관 출혈 치료 시장 규모는 2025년 8억 9,000만 달러로, 2030년까지 11억 4,000만 달러에 이르고, CAGR 5.08%를 보일 것으로 예측됩니다.

이 기세는 복잡한 상부 소화관 증례의 꾸준한 증가, 저침습 지혈법의 광범위한 채용, 재원일수를 단축할 수 있는 기술에 보답하는 진료보수제도에 따릅니다. 병원이 지출의 중심임에 변함이 없지만, 외래수술센터(ASC)가 투자를 끌고 있는 것은 메디케어가 내시경 수술의 대상을 확대해, 과거에는 입원 환자용이었던 수익을 외래 환자가 획득할 수 있게 되었기 때문입니다. 내시경용 기계 클립은 여전히 수술 건수의 대부분을 차지하고 있지만, 국소 지혈 스프레이, 캡슐 내시경, AI 지원 리스크 계층화 도구가 가장 급속히 확대되고 있는 틈새 분야입니다. 지역별로는 북미가 수요의 중심이며 아시아태평양은 병원이 새로운 내시경 검사실을 설치하고 전문의를 육성하고 있기 때문에 가장 높은 성장률을 보이고 있습니다.

세계 소화관 출혈 치료 시장 동향과 통찰

상부 소화관 출혈 사례 증가

상부 소화관 출혈의 발생률은 성인 10만명당 84-160명에 그치고, 사망률은 새로운 치료법에도 불구하고 여전히 10% 가까이입니다. 고령화된 코호트에서 항응고제를 사용하면 위험이 증가하고 임상의는 비용이 많이 드는 재출혈을 억제하기 위해 내시경 검사 시 지혈 키트를 병용할 것을 권장합니다. 병원은 신속한 지혈로 외과적 전환을 피함으로써 절약을 정량화하고, 수술 시간을 단축하고 클립의 유지를 강화하는 기기에 대한 수요를 높이고 있습니다. 따라서 제조업체는 클립, 스프레이 및 주입 카테터를 모듈식 키트에 통합하여 모든 출혈 표현형에 대응할 수 있습니다. 인두 분담 모델을 채택한 의료 시스템은 변동을 없애고 결과 보고서를 개선하기 위해 시설 간에 이러한 키트를 표준화하는 경향이 커지고 있습니다.

저침습 내시경 지혈법으로의 이동

오버 스코프 클립과 싱글 채널 봉합 시스템은 이전에 개복 수술이 필요한 모든 층 벽 결함을 밀봉하여 입원 일수 및 마약 사용량을 줄일 수 있습니다. Boston Scientific의 OverStitch NXT는 표준 위장 카메라에 연결되어 적은 경로로 봉합 패턴을 완성하기 때문에 바쁜 실험실에서 회전이 빨라집니다. 초기 데이터는 특히 섬유성 궤양의 경우 열응고법보다 30일 후 재출혈률이 낮은 것으로 나타났습니다. 그러나 스킬의 격차가 있기 때문에 시뮬레이션 기반의 스킬업이 필요하며, VR 대응 트레이닝 모듈 시장도 병렬로 개척되고 있습니다. 고급 도구와 엄격한 자격 증명을 결합한 병원에서는 긴급 반송 감소와 성과 보상 계약에서 품질 점수를 향상시킬 수 있습니다.

신흥 시장에서 숙련된 내시경 기사 부족

아시아태평양에는 매년 수천 개의 내시경 검사실이 추가로 설치되고 있지만 고급 폐쇄 장비 교육을 받은 공인 직원이 부족하여 프리미엄 솔루션의 도입이 지연되고 있습니다. ESGE는 교육주기를 연장하는 객관적인 능력 지표를 권장하지만, 국가 예산에 부담을 주고 도시와 지방의 격차를 넓히고 있습니다. 공급업체는 단순 클립 어플리케이터와 원격 교육 플랫폼에서 지원되지만 자격 취득 지연은 계속됩니다. 결과적으로 조달위원회는 기술 파이프라인이 성숙할 때까지 하이엔드 키트 구매를 연기하고 저소득 국가의 소화관 출혈 치료 시장을 억제하고 있습니다.

부문 분석

2024년 소화관 출혈 치료 시장에서 기계 클립은 45.35%의 점유율을 차지합니다. 이 부문의 장점은 지속적인 소형화와 강력한 파지력으로 인한 사례당 클립 수를 줄입니다. 국소 스프레이 시장 규모는 작지만, 파우더는 확산성 출혈에 대응하고, 응고 상태에 관계없이 기능하기 때문에 CAGR 12.25%로 확대합니다. 열 프로브 및 주입 카테터는 정맥류 관리를 위한 틈새 역할을 유지하고 퍼스트 패스 지혈을 보장하기 위한 조합 키트에 자주 번들로 제공됩니다.

Boston Scientific의 MANTIS 클립은 기존 제품에 비해 클립 수가 4개 적고, 소요 시간도 5분 가까이 단축되어 있습니다. 조류를 원료로 하는 생체적합성 지혈재는 면역원성을 감소시켜 면역억제 코호트에서의 사용을 가능하게 합니다. 제조업체 각사는 미리 장전된 회전 제어의 핸들 디자인, 하이브리드 수술중의 투시 확인을 돕는 X선 불투과성 마커에 의해 차별화를 도모하고 있습니다.

지역 분석

북미는 2024년 세계 매출의 40.71%를 차지했는데, 이는 메디케어가 입원 환자용과 ASC 기반 양쪽 지혈술에 모두 보험 적용하여 의료 제공업체의 현금흐름을 안정시키고 있기 때문입니다. 또한 미국의 의료 시스템은 긴급 내시경 검사 대기 시간을 단축하고 조기 개입을 촉진하는 AI 지원 트리아지를 시험적으로 도입하고 있습니다. 캐나다의 단일 지불 제도는 지혈 파우더의 국가 일괄 구매에 자금을 제공하고, 균일한 접근을 보장하고, 예측 가능한 조달주기를 추진하고 있습니다. 멕시코는 내시경 치료를 위한 국경을 넘는 의료 투어리즘으로부터 이익을 얻고 있으며, 특히 저렴한 치료비를 요구하는 미국의 무보험 환자들 사이에서 두드러집니다.

아시아태평양은 CAGR 8.61%에서 가장 급성장하고 있는 지역으로 소화기암과 항응고제 처방의 급증을 반영하고 있습니다. 중국은 국가 의료 개혁 하에 현 수준의 병원에 투시 검사실과 캡슐 내시경 판독 장치를 설치하고, 일본은 초고령화 사회에 대응한 로봇 지원 봉합 플랫폼을 상품화하고 있습니다. 인도의 민간 병원은 보험에 가입하는 중간층에 대한 고급 소화 시스템 서비스를 확대하고 걸프 국가에서 의료 관광객을 얻기 위해 재출혈 회피 지표에 중점을 둡니다.

유럽에서는 ESGE 가이드라인을 통한 교육의 조화와 병원 컨소시엄 전체의 장비 대량 구매가 뒷받침되고 안정적인 성장을 유지합니다. 독일에서는 스코프 외 클립의 외래 진료 보상이 선구적으로 도입되어 영국에서는 국민 보건 서비스의 응급 4시간 목표를 달성하기 위해 신속 접근 소화관 출혈 유닛이 확대되었습니다. EU의 새로운 의료기기 규정은 승인까지의 기간을 늘리는 반면 사회적 신용을 높이고 병원이 CE 마크를 획득한 혁신적인 의료기기에 투자하도록 장려합니다.

중동 및 아프리카와 남미는 제3차 의료기관이 내시경 검사 전용 유닛을 개설하고 있기 때문에 점유율은 작지만 2자리 수량 성장을 보이고 있습니다. 높은 수입 관세가 여전히 장애물이 되어 출혈과 폴립 절제 모두의 이용 사례를 커버하는 다용도 기기로 시설을 유도하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 상부 소화관 출혈 증례 증가

- 저침습 내시경적 지혈법으로의 전환

- 차세대 지혈 클립과 스프레이의 이용 가능성

- 항응고제를 사용하는 고령자 인구의 확대

- AI에 의한 출혈 위험 예측 알고리즘

- 연중무휴인 소화관 출혈 대응 팀에 대한 병원의 인센티브

- 시장 성장 억제요인

- 신흥 시장에서 숙련된 내시경의 부족

- 첨단 내시경 기기의 고비용

- 특수 금속과 분말공급 체인의 병목

- 예방적 PPI에서 항균약 적정 사용 지원의 제한

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품별

- 내시경 기계장치

- 내시경 열 장치

- 내시경 주사 장치

- 국소지혈 스프레이

- 병용 요법 키트

- 기타 제품

- 소화관부별

- 상부 소화관

- 소장 및 중부 소화관

- 하부 소화관

- 최종 사용자별

- 병원 및 클리닉

- 외래수술센터(ASC)

- 소화관 전문센터

- 진단 실험실

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Boston Scientific Corporation

- Olympus Corporation

- Medtronic PLC

- Cook Group(Cook Medical)

- CONMED Corporation

- ERBE Elektromedizin GmbH

- Ovesco Endoscopy AG

- STERIS PLC

- Pfizer Inc.

- US Medical Innovations

- Fujifilm Holdings Corp.

- HOYA Corp.(Pentax Medical)

- Johnson & Johnson(Ethicon)

- Baxter International Inc.

- Teleflex Incorporated

- B. Braun Melsungen AG

- Takeda Pharmaceutical Co.

- Novo Nordisk A/S

- Smith & Nephew plc

- Ferring Pharmaceuticals

제7장 시장 기회와 장래의 전망

JHS 25.11.21The gastrointestinal bleeding treatment market size is USD 0.89 billion in 2025 and is forecast to reach USD 1.14 billion by 2030, advancing at a 5.08% CAGR.

Momentum comes from the steady rise in complex upper-GI cases, broader adoption of minimally invasive hemostasis, and a reimbursement climate that rewards technology capable of shortening hospital stays. Hospitals remain the spending core, yet ambulatory surgical centers (ASCs) attract investment because Medicare now reimburses an expanded list of endoscopic procedures, allowing outpatient sites to capture revenue that once defaulted to inpatient settings. Endoscopic mechanical clips still dominate procedure volumes, but topical hemostatic sprays, capsule endoscopy, and AI-assisted risk stratification tools are the fastest-scaling niches. Regionally, North America anchors demand, while Asia-Pacific delivers the highest incremental growth as hospitals equip new endoscopy suites and train specialists.

Global Gastrointestinal Bleeding Treatment Market Trends and Insights

Rising Incidence Of Upper GI Bleeding Cases

Upper-GI bleeding rates remain 84-160 per 100,000 adults, with mortality still near 10% despite newer therapies. Anticoagulant uptake in aging cohorts magnifies risk and pushes clinicians to deploy combination hemostasis kits during the index endoscopy to curb costly rebleeds. Hospitals quantify savings when rapid hemostasis avoids surgical conversion, strengthening demand for devices that shorten procedure time and enhance clip retention. Manufacturers therefore package clips, sprays, and injection catheters in modular kits to ensure readiness for any bleeding phenotype. Health systems with capitated payment models increasingly standardize these kits across sites to cut variation and improve outcomes reporting.

Shift Toward Minimally-Invasive Endoscopic Hemostasis

Over-the-scope clips and single-channel suturing systems now seal full-thickness wall defects once referred for open surgery, reducing hospital days and narcotic use. Boston Scientific's OverStitch NXT connects to a standard gastroscope and completes suture patterns in fewer passes, allowing faster turnover in busy labs. Early data show lower 30-day rebleed rates relative to thermal coagulation, especially for fibrotic ulcers. The skill gap, however, necessitates simulation-based upskilling and has opened a parallel market for VR-enabled training modules. Hospitals that couple advanced tools with rigorous credentialing enjoy fewer emergency transfers and better quality scores under pay-for-performance contracts.

Shortage Of Skilled Endoscopists In Emerging Markets

Asia-Pacific adds thousands of endoscopy rooms annually, yet lacks certified staff trained in advanced closure devices, delaying uptake of premium solutions. ESGE recommends objective competence metrics that extend training cycles, placing strain on national budgets and widening urban-rural gaps. Vendors respond with simplified clip applicators and tele-mentoring platforms, but credentialing backlogs persist. Consequently, procurement committees defer purchase of high-end kits until skill pipelines mature, tempering the gastrointestinal bleeding treatment market in lower-income countries.

Other drivers and restraints analyzed in the detailed report include:

- Availability Of Next-Generation Hemostatic Clips & Sprays

- Expanding Elderly Population Using Anticoagulants

- High Cost Of Advanced Endoscopic Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mechanical clips held 45.35% of the gastrointestinal bleeding treatment market in 2024 thanks to decades-long clinician familiarity and multi-lesion versatility. The segment benefits from continuous miniaturization and stronger grasp forces that cut clip counts per case. The gastrointestinal bleeding treatment market size for topical sprays, though smaller, expands at a 12.25% CAGR because powders address diffuse bleeding and function regardless of coagulation status. Thermal probes and injection catheters maintain niche roles for variceal management and are frequently bundled in combination kits to guarantee first-pass hemostasis.

Performance metrics now focus on deployment speed; Boston Scientific's MANTIS clip requires 4 fewer clips and nearly 5 fewer minutes than predecessors, freeing lab capacity for additional cases. Biocompatible hemostatic agents sourced from algae reduce immunogenicity, opening use in immunosuppressed cohorts. Manufacturers differentiate via pre-loaded, rotation-controlled handle designs and radiopaque markers that aid fluoroscopic confirmation during hybrid procedures.

The Gastrointestinal Bleeding Treatment Market Report is Segmented by Product (Endoscopic Mechanical Devices, Endoscopic Thermal Devices, Endoscopic Injection Devices, and More), GI Tract Division (Upper GI Tract, Small Bowel, and Lower GI Tract), End User (Hospitals, Ambulatory Surgical Centers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 40.71% of global revenue in 2024 because Medicare reimburses both inpatient and ASC-based hemostasis, stabilizing cash-flows for providers. U.S. health systems also pilot AI-guided triage that decreases emergency endoscopy wait times and promotes early intervention. Canada's single-payer framework funds national bulk buys of hemostatic powders, ensuring uniform access and driving predictable procurement cycles. Mexico benefits from cross-border medical tourism for endoscopic treatment, particularly among uninsured U.S. patients seeking lower procedure costs.

Asia-Pacific is the fastest-growing region at 8.61% CAGR, reflecting a sharp rise in gastrointestinal cancers and anticoagulant prescriptions. China upgrades county-level hospitals with fluoroscopy suites and capsule endoscopy readers under national health reforms, whereas Japan commercializes robot-assisted suturing platforms that cater to a super-aged population. India's private hospitals expand advanced GI services for an insured middle class and focus on rebleed-avoidance metrics to compete for medical tourists from the Gulf.

Europe posts stable growth, aided by ESGE guidelines that harmonize training and drive collective device purchasing across hospital consortia. Germany pioneers outpatient reimbursement for over-the-scope clips, while the United Kingdom expands rapid-access GI bleed units to meet the National Health Service's 4-hour emergency target. The new EU Medical Device Regulation lengthens approval timelines but lifts public confidence, encouraging hospitals to invest in CE-marked innovations.

The Middle East and Africa plus South America occupy smaller shares yet report double-digit volume growth as tertiary centers open dedicated endoscopy units. High import tariffs remain a hurdle, steering facilities toward multipurpose devices that cover both bleeding and polypectomy use-cases.

- Boston Scientific

- Olympus

- Medtronic

- Cook Group

- Conmed

- Erbe Elektromedizin

- Ovesco Endoscopy

- STERIS

- Pfizer

- U.S. Medical Innovations

- Fujifilm Holdings Corp.

- HOYA Corp. (Pentax Medical)

- Johnson & Johnson

- Baxter

- Teleflex

- B. Braun

- Takeda Pharmaceutical Co.

- Novo Nordisk

- Smiths Group

- Ferring Pharmaceuticals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence Of Upper GI Bleeding Cases

- 4.2.2 Shift Toward Minimally-Invasive Endoscopic Hemostasis

- 4.2.3 Availability Of Next-Generation Hemostatic Clips & Sprays

- 4.2.4 Expanding Elderly Population Using Anticoagulants

- 4.2.5 AI-Driven Bleeding-Risk Prediction Algorithms

- 4.2.6 Hospital Incentives For 24/7 GI-Bleed Response Teams

- 4.3 Market Restraints

- 4.3.1 Shortage Of Skilled Endoscopists In Emerging Markets

- 4.3.2 High Cost Of Advanced Endoscopic Devices

- 4.3.3 Supply-Chain Bottlenecks In Specialty Metals & Powders

- 4.3.4 Antimicrobial-Stewardship Limits On Prophylactic PPIs

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Endoscopic Mechanical Devices

- 5.1.2 Endoscopic Thermal Devices

- 5.1.3 Endoscopic Injection Devices

- 5.1.4 Topical Hemostatic Sprays

- 5.1.5 Combination Therapy Kits

- 5.1.6 Other Products

- 5.2 By GI Tract Division

- 5.2.1 Upper GI Tract

- 5.2.2 Small Bowel / Mid GI Tract

- 5.2.3 Lower GI Tract

- 5.3 By End User

- 5.3.1 Hospitals / Clinics

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Specialized GI Centers

- 5.3.4 Diagnostic Laboratories

- 5.3.5 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Boston Scientific Corporation

- 6.3.2 Olympus Corporation

- 6.3.3 Medtronic PLC

- 6.3.4 Cook Group (Cook Medical)

- 6.3.5 CONMED Corporation

- 6.3.6 ERBE Elektromedizin GmbH

- 6.3.7 Ovesco Endoscopy AG

- 6.3.8 STERIS PLC

- 6.3.9 Pfizer Inc.

- 6.3.10 US Medical Innovations

- 6.3.11 Fujifilm Holdings Corp.

- 6.3.12 HOYA Corp. (Pentax Medical)

- 6.3.13 Johnson & Johnson (Ethicon)

- 6.3.14 Baxter International Inc.

- 6.3.15 Teleflex Incorporated

- 6.3.16 B. Braun Melsungen AG

- 6.3.17 Takeda Pharmaceutical Co.

- 6.3.18 Novo Nordisk A/S

- 6.3.19 Smith & Nephew plc

- 6.3.20 Ferring Pharmaceuticals

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment