|

시장보고서

상품코드

1851177

레드 바이오테크놀러지 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Red Biotechnology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

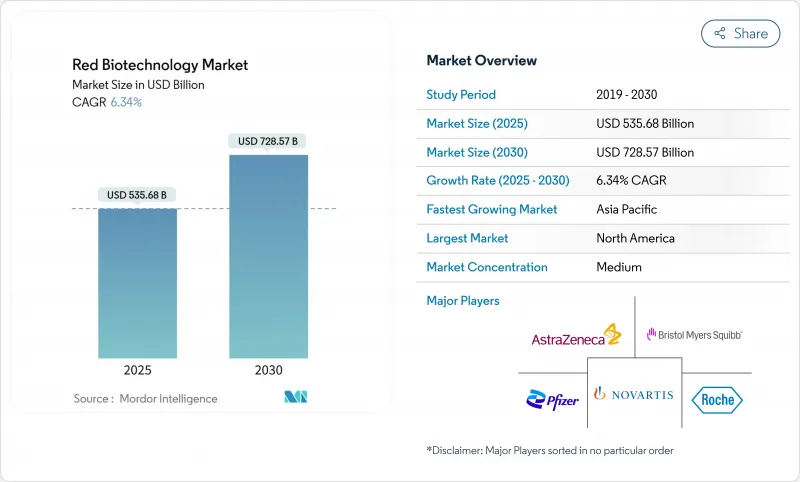

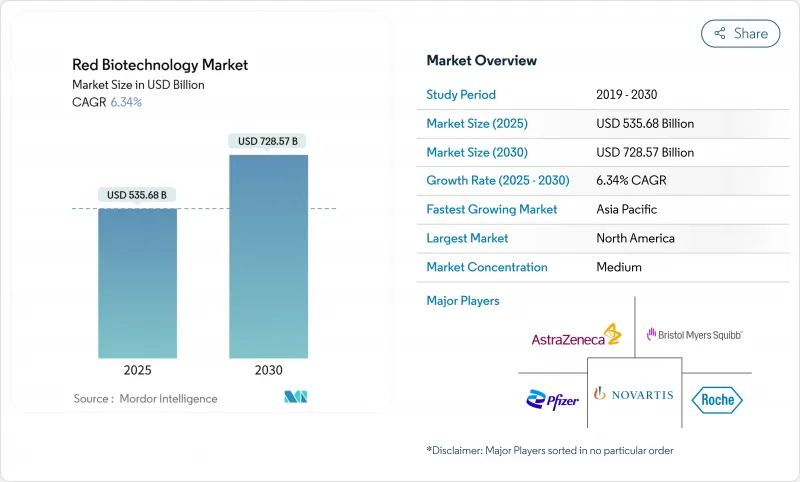

세계의 레드 바이오테크놀러지 시장 규모는 2025년 5,356억 8,000만 달러로, 2030년까지 7,285억 7,000만 달러에 달할 것으로 예측되며, CAGR은 6.34%로 예상됩니다.

팬데믹에 초점을 맞춘 백신 생산에서 세포 및 유전자 치료, 차세대 단일클론항체, 정밀 진단 등 다양한 파이프라인으로의 이행이 성장을 지지하고 있습니다. 2024년에 FDA가 발표한 24가지 생물학적 제제의 승인에서 볼 수 있듯이, 규제 당국이 심사를 가속화하는 것이 이 기세를 지원하고 있습니다. 정부의 병행 지출, 특히 2027년까지 795억 달러의 PHEMCE(Public Health Emergency Medical Countermeasures Enterprise)의 할당이 개발과 제조 양면에서 국내 능력을 강화하고 있습니다. 업계 측에서는 노스캐롤라이나주에 있는 Merck의 10억 달러의 백신 시설과 같은 대규모 자본 프로젝트가 유통에 대처하고 일반 상업 생산 사이에서 유연하게 대응할 수 있는 탄력적인 능력을 추가하고 있습니다. 이러한 요인들이 결합되어 복잡한 생물학적 제제를 확장할 수 있는 예측 가능한 환경이 구축되고, 벤처 투자 및 관민 파트너십이 촉진되고, 혁신 자산의 임상 적용까지의 시간이 단축됩니다.

세계 레드 바이오테크놀러지 시장 동향과 통찰

만성 및 희귀질환의 이환율과 유병률 상승

2024년에 8개의 신규 세포 및 유전자 치료제가 FDA의 심사를 통과해, 미충족 요구 영역이 어떻게 과학적 돌파구를 상업 자산으로 전환시키는가가 분명해졌습니다. 2024년 신규 생물학적 제제의 34%를 차지하는 암 영역에서의 승인이 계속 우세합니다. 차세대 단일클론항체와 유전자 치료에 대한 일본의 정책적 우선순위는 급속히 진행되는 고령화 사회에 대한 대응이라는 과제를 반영하고 있습니다. 2024년에 승인된 유전자 치료의 88%가 희소병용 의약품으로 지정되었듯이 희소질병용 의약품 파이프라인은 희소질병용 의약품의 우대 조치의 혜택을 받고 있습니다. FDA의 희귀질환 혁신 허브와 START 파일럿은 개발 기간을 단축하고 한때 상업적으로 매력이 없습니다고 여겨졌던 틈새 질환을 대상으로 하는 기업을 장려하고 있습니다.

헬스케어 자금 확대와 관민 파트너십

2023-2027년 PHEMCE 배분은 대책 연구개발과 국내 제조에 795억 달러가 확보되어 이전 계획 사이클보다 155억 달러 증가했습니다. BARDA의 20억 달러 BioMaP-Consortium은 수개월 이내에 항체에서 mRNA 백신으로 전환할 수 있는 유연한 시설에 공동 투자함으로써 이러한 지원을 확대합니다. 캐나다의 몬트리올에 있는 생물 제제 제조 센터는 바이러스 벡터 백신과 단백질 아단위 백신의 연간 생산 능력 2억 5,000만 회분을 추가했습니다. 유럽위원회의 GenAI4EU 프로그램은 생물 제제의 발견을 포함한 AI 프로젝트에 10억 유로를 기록하여 국경을 넘어서는 지식의 이전을 강화하고 있습니다. 인도의 BIO-E3 프레임워크는 새로운 바이오 생산 캠퍼스를 위해 양허적 자금과 합리적인 토지 취득을 제공합니다.

높은 바이오 제조 비용과 콜드체인 비용

콜드체인 실패로 인한 산업 손실은 연간 350억 달러에 달하며, 온도에 민감한 생물학적 제제의 가격 기반이 약화됩니다. CAR-T 자가면역요법은 노동 집약적인 제조와 저온 유통으로 인해 환자 1인당 50만 달러 이상의 비용이 듭니다. 부속서 1의 개정은 무균 처리 규칙을 강화하고, 아이솔레이터 기술과 환경 모니터링의 업그레이드를 강요하고, 그린필드 공장의 설비 투자가 부풀어오고 있습니다. 미국의 원료 수입의 75% 이상은 국외에서 생산되어 지정학적 충격에 노출되어 있습니다. AI를 활용한 루트플래닝 소프트웨어와 디지털 트윈은 15-25%의 물류 삭감을 약속하지만, 보급은 아직 시험적인 단계에 그치고 있으며 단기적인 구제를 늦추고 있습니다.

부문 분석

치료제는 2024년에 2,930억 달러를 창출해, 레드 바이오테크놀러지 시장 규모의 54.67%의 점유율에 상당하고, 2030년까지 연평균 복합 성장률(CAGR) 6.87%를 보일 것으로 예측됩니다. 단클론항체는 200개가 넘는 약물이 승인되고 세계 1,400개 가까이 유효한 임상 후보 화합물이 존재하는 이 범주의 중심적 존재입니다. 이중 특이성 항체는 임상에서 승인으로의 전환율이 가장 높고 BioNTech나 Bristol Myers Squibb 등이 수십억 달러 규모의 공동 개발을 진행하고 있습니다. 유전자 치료는 2024년 FDA가 8개 제품을 승인함으로써 가속화되었으며, CRISPR로 변형된 CAR-T 플랫폼은 현재 혈액 종양학의 초기 단계 임상시험을 지배하고 있습니다.

백신은 전략적 관련성을 유지하고 아웃브레이크 시 최소 콜오프 양을 보장하는 BARDA 옵션 조항에 의해 지원됩니다. 시퀀싱 시약과 액체 생검 분석이 분산 환경에서 채택되어 진단 및 조사 도구가 확장됩니다. 이와 병행하여 치료용 단백질은 항체 약물 복합체와 특정 질병 미세환경에 맞는 융합 사이토카인으로 진화하여 고정밀 타겟팅을 중시하는 레드바이오테크놀러지 시장을 반영하고 있습니다.

지역 분석

북미는 2024년 레드바이오테크놀러지 시장 규모의 39.13%를 차지했고, 2030년까지 CAGR이 6.01%로 예측되고 있습니다. 이 지역은 발견, 규제 및 산업 규모의 제조를 묶은 풀 스펙트럼 생태계의 혜택을 누리고 있습니다. BARDA의 BioMaP-Consortium과 PHEMCE의 자본 풀은 일상적인 생물 제제와 긴급 생물 제제 모두 국내 생산을 보호하고 FDA의 신속한 지정은 혁신적인 치료법의 리드 타임을 단축합니다. ACIP 회원의 재검토 등 현재 진행중인 규제 개혁은 백신 출시의 타이밍에 단기적인 불확실성을 가져오고 있습니다. 그러나 생명공학 경쟁력 강화를 위한 150억 달러를 요구하는 대규모 의회 제안은 지속적인 정치적 헌신을 강조합니다.

유럽은 2030년까지 연평균 복합 성장률(CAGR) 6.24%를 보일 것으로 예측됩니다. 임상시험규제와 호라이즌 유럽 기금을 포함한 정책개혁은 다국간 임상시험과 국경을 넘은 지식의 공유를 촉진합니다. HERA의 EUFab 인프라는 100일 이내에 mRNA 백신, 바이러스 벡터 백신 및 단백질 백신을 전환할 수 있는 경쾌한 서지 능력을 제공하여 유럽의 자율성을 높입니다. EMA의 새로운 규제로 인한 수수료 인상은 비용 압박이 되지만, 바이오시밀러 의약품 신청 서류의 합리화에 대한 동시 협의는 국가 납부자에게 보다 저가의 생물 제제에 대한 접근을 확대할 수 있습니다.

아시아태평양은 가장 기세가 높아 CAGR 7.26%로 확대되어 2030년까지 부문 가치가 2배 이상이 될 것으로 예측됩니다. 일본의 국가전략은 세액공제와 심사 절차의 가속화를 통해 2030년까지 부문 전체의 생산을 3배인 15조엔으로 하는 것을 목표로 하고 있습니다. 인도의 생명공학 가치는 2014년 100억 달러에서 2024년 1,300억 달러로 급증하여 비용면에서 우위와 세계 백신 생산량의 60% 점유율을 활용합니다. 중국은 자가면역질환을 표적으로 하는 AstraZeneca와 CSPC Pharmaceutical과의 53억 달러의 제휴에 상징되는 AI를 활용한 발견을 깊게 하고 있습니다. 지역정부는 국경을 넘는 임상시험을 용이하게 하기 위한 규제를 동조시켜 인간 최초 투여시험과 이어지는 인근 계약 공장에서의 스케일 업을 가속화하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성 질환 및 희귀질환의 이환율 및 유병률 상승

- 헬스케어 자금 확대와 관민 파트너십

- 맞춤형 의료 도입과 동반진단약 보급

- mRNA 플랫폼의 파급으로 새로운 생물 제제가 급성장

- AI에 의한 초기 단계 생물 제제 설계에서 위험 회피

- 정부 주도의 유행 대책 프로그램이 세계의 백신 제조 능력을 확대

- 시장 성장 억제요인

- 높은 바이오 제조, 콜드체인, 비용

- 복잡하고 변화하는 세계의 생물 제제 규제

- 중요 원재료공급 체인 취약성

- 차세대 유전자 치료에서 면역원성 위험

- 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력 및 소비자

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품별

- 백신

- mRNA 백신

- 바이러스 벡터 백신

- 재조합 단백질 백신

- 결합형 및 아단위 백신

- 생백신 및 불활성화백신

- 치료제

- 단클론항체

- 재조합 단백질

- 유전자 치료

- 세포치료

- RNA 치료제

- 진단 및 조사 도구

- 시퀀싱 시약 및 키트

- 동반진단 분석

- 포인트 오브 케어 분자 검사

- 백신

- 최종 사용자별

- 바이오의약품기업

- 제조 수탁 기관(CMO)

- 개발 업무 수탁 기관(CRO)

- 학술기관 및 연구기관

- 병원 및 전문 클리닉

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 경쟁 벤치마킹

- 시장 점유율 분석

- 기업 프로파일

- Amgen Inc.

- AstraZeneca PLC

- Biogen Inc.

- BioNTech SE

- Bristol Myers Squibb

- CSL Limited

- F. Hoffmann-La Roche Ltd

- Gilead Sciences Inc.

- Illumina Inc.

- Johnson & Johnson(Janssen)

- Lonza Group AG

- Merck & Co., Inc.

- Moderna Inc.

- Novartis AG

- Pfizer Inc.

- Regeneron Pharmaceuticals

- Sanofi

- Sarepta Therapeutics

- Takeda Pharmaceutical

- Thermo Fisher Scientific

- Vertex Pharmaceuticals

제7장 시장 기회와 장래의 전망

JHS 25.11.21The red biotechnology market size stood at USD 535.68 billion in 2025 and is forecast to reach USD 728.57 billion by 2030, advancing at a 6.34% CAGR.

Growth rests on a transition from pandemic-focused vaccine output toward diversified pipelines that now include cell and gene therapies, next-generation monoclonal antibodies, and precision diagnostics. Faster regulatory reviews underpin momentum, illustrated by 24 biological license approvals issued by the FDA in 2024. Parallel government spending-most notably the USD 79.5 billion Public Health Emergency Medical Countermeasures Enterprise (PHEMCE) allocation through 2027-bolsters domestic capacity for both development and manufacturing. On the industry side, large-scale capital projects such as Merck's USD 1 billion vaccine facility in North Carolina add resilient capacity that can flex between pandemic response and routine commercial production. Together, these factors create a predictable environment for scaling high-complexity biologics, encouraging venture investment and public-private partnerships that shorten time-to-clinic for innovative assets.

Global Red Biotechnology Market Trends and Insights

Rising incidence & prevalence of chronic and rare diseases

Eight novel cell and gene therapies cleared FDA review in 2024, underlining how unmet-need areas convert scientific breakthroughs into commercial assets. Oncology continued to dominate approvals, representing 34% of all new biological products in 2024. Demographic shifts intensify demand; Japan's policy priority on next-generation monoclonal antibodies and gene therapies reflects the challenge of managing a rapidly aging population. Rare-disease pipelines benefit from Orphan Drug incentives, as 88% of 2024 gene-therapy approvals carried that designation. The FDA's Rare Disease Innovation Hub and its START pilot compress development timelines, encouraging companies to target niche diseases once considered commercially unattractive.

Healthcare funding expansion & public-private partnerships

The 2023-2027 PHEMCE allocation set aside USD 79.5 billion for countermeasure R&D and domestic manufacturing, a USD 15.5 billion increase over the earlier planning cycle. BARDA's USD 2 billion BioMaP-Consortium extends this support by co-investing in flexible facilities that can pivot from antibodies to mRNA vaccines within months. Canada's Biologics Manufacturing Centre in Montreal adds 250 million-dose annual capacity for viral-vector and protein subunit vaccines. The European Commission's GenAI4EU programme earmarks EUR 1 billion for AI projects including biologics discovery, reinforcing cross-border knowledge transfer. Emerging economies mirror the model; India's BIO-E3 framework supplies concessional finance and streamlined land acquisition for new bioproduction campuses.

High biomanufacturing & cold-chain costs

Industry losses from cold-chain failures hit USD 35 billion annually, undermining affordability for temperature-sensitive biologics. CAR-T autologous therapies still cost above USD 500,000 per patient due to labor-intensive manufacture and cryogenic distribution. Annex 1 revisions tightened aseptic-processing rules, compelling upgrades to isolator technology and environmental monitoring that inflate capex for greenfield plants. Supply-chain concentration compounds the problem; more than 75% of U.S. API imports originate outside its borders, exposing production to geopolitical shocks. Although AI-enabled route-planning software and digital twins promise 15-25% logistics savings, widespread deployment remains in pilot stages, delaying near-term relief.

Other drivers and restraints analyzed in the detailed report include:

- Personalized-medicine adoption & companion diagnostics uptake

- mRNA-platform spill-over fast-tracking new biologics

- Complex, shifting global biologics regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Therapeutic drugs generated USD 293 billion in 2024, corresponding to a 54.67% share of the Red biotechnology market size, and are forecast to grow at 6.87% CAGR to 2030. Monoclonal antibodies anchor the category, boasting more than 200 approved agents and close to 1,400 active clinical candidates worldwide. Bispecific formats achieve the highest clinical-to-approval conversion, prompting companies such as BioNTech and Bristol Myers Squibb to pursue multi-billion-dollar codevelopment deals. Gene therapies accelerated following the FDA endorsement of eight products in 2024, while CRISPR-modified CAR-T platforms now dominate early-phase haem-oncology trials. mRNA therapeutics move beyond infectious disease into cardiometabolic indications, supported by circular RNA technology that multiplies in vivo protein yield.

Vaccines maintain strategic relevance, supported by BARDA option clauses that guarantee minimum call-off volumes during outbreaks. Diagnostics and research tools expand as sequencing reagents and liquid-biopsy assays gain adoption in decentralized settings. In parallel, therapeutic proteins evolve toward antibody-drug conjugates and fusion cytokines tailored to specific disease microenvironments, reflecting the Red biotechnology market emphasis on precision targeting.

The Red Biotechnology Market Report is Segmented by Product (Vaccines [mRNA Vaccines, Viral Vector Vaccines, and More], Therapeutic Drugs [Monoclonal Antibodies, Recombinant Proteins, and More], and Diagnostics & Research Tools [Sequencing Reagents & Kits and More]), End-User (Biopharmaceutical Companies and More), Aand Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 39.13% of the Red biotechnology market size in 2024, and is projected to register a 6.01% CAGR through 2030. The region benefits from a full-spectrum ecosystem that bundles discovery, regulation, and industrial-scale manufacture. BARDA's BioMaP-Consortium and the PHEMCE capital pool safeguard domestic production for both routine and emergency biologics, while the FDA's expedited designations shorten lead times for innovative therapies. Ongoing regulatory restructuring, such as the ACIP membership overhaul, introduces short-term uncertainty for vaccine launch timing. Yet, sizeable Congressional proposals seeking USD 15 billion for biotech competitiveness underscore sustained political commitment.

Europe is projected to grow at 6.24% CAGR to 2030. Policy reforms, including the Clinical Trials Regulation and Horizon Europe funds, facilitate multinational trials and cross-border knowledge sharing. HERA's EUFab infrastructure offers nimble surge capacity, capable of switching among mRNA, viral-vector, and protein vaccines within 100 days, enhancing the bloc's autonomy. Fee increases under new EMA regulations add cost pressure, but simultaneous consultation on streamlined biosimilar dossiers could broaden access to lower-priced biologics for state payers.

Asia-Pacific shows the fastest momentum, expanding at 7.26% CAGR and expected to more than double its segment value by 2030. Japan's national strategy seeks to triple sectoral output to 15 trillion yen by 2030 through tax credits and accelerated review lanes. India's biotech value rocketed from USD 10 billion in 2014 to USD 130 billion in 2024, leveraging cost advantages and a 60% share of global vaccine volume. China deepens AI-enabled discovery, epitomized by AstraZeneca's USD 5.3 billion partnership with CSPC Pharmaceutical that targets autoimmune disorders. Regional governments are synchronizing regulations to ease trans-border clinical trials, accelerating first-in-human studies and subsequent scale-up in nearby contract plants.

List of Companies Covered in this Report:

- Amgen

- AstraZeneca

- Biogen

- BioNTech

- Bristol-Myers Squibb

- CSL Behring

- Roche

- Gilead Sciences

- Illumina

- Johnson & Johnson

- Lonza Group

- Merck

- Moderna

- Novartis

- Pfizer

- Regeneron Pharmaceuticals

- Sanofi

- Sarepta Therapeutics

- Takeda Pharmaceuticals

- Thermo Fisher Scientific

- Vertex Pharmaceuticals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising incidence & prevalence of chronic and rare diseases

- 4.2.2 Healthcare funding expansion & public-private partnerships

- 4.2.3 Personalized-medicine adoption & companion diagnostics uptake

- 4.2.4 mRNA-platform spill-over fast-tracking new biologics

- 4.2.5 AI-driven de-risking of early-stage biologics design

- 4.2.6 Government-led pandemic-preparedness programmes scaling global vaccine manufacturing capacity

- 4.3 Market Restraints

- 4.3.1 High biomanufacturing & cold-chain costs

- 4.3.2 Complex, shifting global biologics regulations

- 4.3.3 Supply-chain fragility for critical raw materials

- 4.3.4 Immunogenicity risks in next-gen gene therapies

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Vaccines

- 5.1.1.1 mRNA Vaccines

- 5.1.1.2 Viral Vector Vaccines

- 5.1.1.3 Recombinant-protein Vaccines

- 5.1.1.4 Conjugate & Subunit Vaccines

- 5.1.1.5 Live-attenuated & Inactivated Vaccines

- 5.1.2 Therapeutic Drugs

- 5.1.2.1 Monoclonal Antibodies

- 5.1.2.2 Recombinant Proteins

- 5.1.2.3 Gene Therapies

- 5.1.2.4 Cell Therapies

- 5.1.2.5 RNA Therapeutics

- 5.1.3 Diagnostics & Research Tools

- 5.1.3.1 Sequencing Reagents & Kits

- 5.1.3.2 Companion-diagnostic Assays

- 5.1.3.3 Point-of-care Molecular Tests

- 5.1.1 Vaccines

- 5.2 By End-User

- 5.2.1 Biopharmaceutical Companies

- 5.2.2 Contract Manufacturing Organizations (CMOs)

- 5.2.3 Contract Research Organizations (CROs)

- 5.2.4 Academic & Research Institutes

- 5.2.5 Hospitals & Specialty Clinics

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Amgen Inc.

- 6.4.2 AstraZeneca PLC

- 6.4.3 Biogen Inc.

- 6.4.4 BioNTech SE

- 6.4.5 Bristol Myers Squibb

- 6.4.6 CSL Limited

- 6.4.7 F. Hoffmann-La Roche Ltd

- 6.4.8 Gilead Sciences Inc.

- 6.4.9 Illumina Inc.

- 6.4.10 Johnson & Johnson (Janssen)

- 6.4.11 Lonza Group AG

- 6.4.12 Merck & Co., Inc.

- 6.4.13 Moderna Inc.

- 6.4.14 Novartis AG

- 6.4.15 Pfizer Inc.

- 6.4.16 Regeneron Pharmaceuticals

- 6.4.17 Sanofi

- 6.4.18 Sarepta Therapeutics

- 6.4.19 Takeda Pharmaceutical

- 6.4.20 Thermo Fisher Scientific

- 6.4.21 Vertex Pharmaceuticals

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-needs Assessment