|

시장보고서

상품코드

1851178

인공 심장 판막 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Prosthetic Heart Valve - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

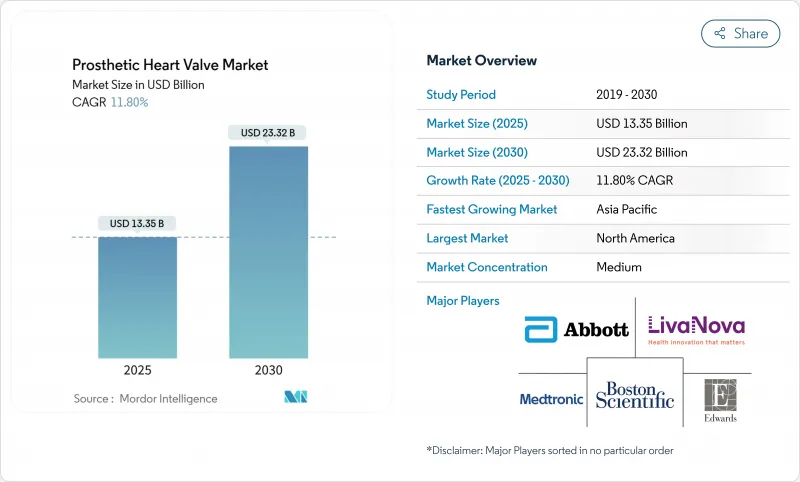

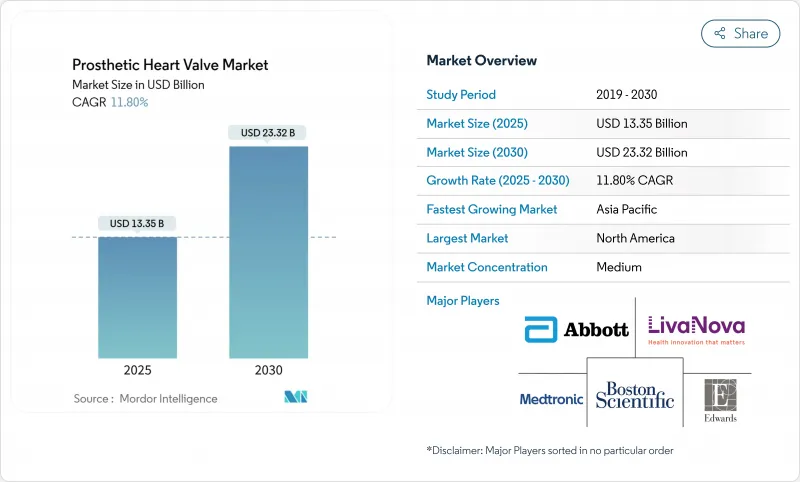

세계의 인공 심장 판막 시장은 2025년 133억 5,000만 달러에 이르고, 2030년까지 233억 2,000만 달러로 성장할 것으로 예측되며, 기간 중 CAGR은 11.8%를 기록할 것으로 보입니다.

인구 역학의 노화, 경 카테터 대동맥 판막 치환술(TAVR)의 적응 확대, 규제 당국의 심사 가속화로 인해 경 카테터 혁신이 인공 심장 판막 시장의 주요 성장 엔진으로 자리매김하고 있습니다. Edwards Lifesciences은 2025년 5월 무증상성 중증 대동맥판 협착증에서 SAPIEN 3 플랫폼의 미국 식품의약국(FDA) 승인을 받았으며, 치료가능한 환자층이 증후성 환자 이외에도 확대되었습니다. 경 카테터 심장 판막은 2024년 매출의 45.55%를 차지하며, Edwards의 EVOQUE나 Abbott의 TriClip 등의 삼첨판 시스템은 퍼스트 인 클래스의 승인 취득 후 2자리 성장에 가속하고 있습니다. 수술건수는 계속 병원이 압도적으로 많지만 외래수술센터(ASC)가 가장 급속히 확대되고 있습니다. 북미가 가장 큰 점유율을 차지하고 있지만 아시아태평양은 중국의 MicroPort의 VitaFlow Liberty Flex와 같은 현지 승인 덕분에 고성장 프론티어가 되었습니다. Edwards의 3억 달러 Innovalve 인수와 Johnson & Johnson의 17억 달러의 V-Wave 인수로 대표되는 포트폴리오 통합이 경쟁을 더욱 격화시키고 있습니다.

세계 인공 심장 판막 시장 동향과 통찰

TAVR/TAVI 적응 확대

2025년 5월, 무증상성 중증 대동맥판 협착증에 대한 Edwards의 SAPIEN 3 플랫폼이 FDA에 승인됨에 따라 '경과관찰'이라는 사고방식이 없어져 임상가는 증상발현 전에 개입할 수 있게 되었습니다. EARLY TAVR의 데이터에서 3.8년간의 추적조사에서 조기치료로 인한 부작용은 26.8%였으나 감시하에서는 45.3%였습니다. Edwards는 2025년 TAVR 매출을 41억-44억 달러로 예측했으며, Abbot과 같은 라이벌은 보다 낮은 위험의 환자를 얻기 위해 ENVISION 시험을 시작했습니다. Medicare & Medicaid Service Center(CMS)의 적용 범위 결정은 일반적으로 민간 지급자가 Medicare의 선례를 반영하기 때문에 채용을 형성합니다. 적용 범위가 넓어지면 수술 건수가 증가하고 인공 심장 판막 시장의 트랜스 카테터 우위로의 전환이 강화됩니다.

규제 당국의 조기 승인 및 브레이크스루 지정

브레이크스루 장치 지정은 2024년 9월까지 과거 최고의 1,041건에 달할 것으로 전망됐습니다. 128건의 승인 제품은 이 패스웨이가 승인을 3-5년에서 약 18-24개월로 압축하는 방법을 보여줍니다. Edwards의 EVOQUE 삼첨판 밸브는 2024년 2월 승인을 얻기 위해 돌파 상태를 활용하고 4C Medical Polymer Alta Valve는 두 가지 획기적인 라벨을 획득했습니다. 유럽도 이 절박한 상황과 유사하며, 2025년 4월에 SAPIEN M3에 세계 최초의 경대퇴승모판 CE마크를 부여하고 있습니다. 조기 지정을 받은 기업은 시장 투입 속도로 우위에 서서 인공 심장판 시장에서의 기업 수익과 브랜드 포지셔닝을 높일 수 있습니다.

고액의 TAVR 장치와 절차 비용

미국의 민간지급기관이 TAVR에 지불하는 비용의 중앙값은 7만 1,312달러로, 메디케어의 3만 7,865달러에 비해 높습니다. 구미에서는 TAVR에 연간 20억 달러 이상이 소비되어 예산을 압박하고 있습니다. 신흥 시장은 1인당 연간 건강 관리 지출을 초과할 수 있기 때문에 더 큰 장애물에 직면하고 있습니다. 스페인 1QALY당 6,952유로의 증분 비용 대 효과비가 임계값보다 낮지만 지불자의 제약으로 인해 급속한 도입에는 한계가 있습니다. 제조업체는 가치 기반 계약을 모색하고 있지만 높은 가격은 여전히 인공 심장 판막 시장의 제약입니다.

부문 분석

경 카테터 심장 판막은 2024년 매출의 45.55%를 차지했으며, 위험 프로파일을 불문하고 구제 요법에서 제1선택약으로 빠르게 이행하고 있음을 뒷받침하고 있습니다. 이 부문은 입원 기간을 단축하고 적격성을 확대하는 합리화된 기술을 통해 시장 세분화 시장을 지원합니다. 폴리머 밸브는 가장 빠르게 성장하는 틈새 분야이며 2030년까지 연평균 복합 성장률(CAGR)은 18.25%로 예상됩니다. 항응고요법을 하지 않아도 석회화하기 어려운 소재이기 때문에 활동적인 환자에게 매력적입니다. 조직 밸브는 기존 수술과의 연관성을 유지하며, 기계식 밸브는 내구성과 대조하여 평생 항응고 치료를 받아들이는 일부 청소년 사용자들에게 계속 선택됩니다. Edwards의 무증상 환자용 SAPIEN 3 및 EVOQUE 삼첨판 시스템과 같은 규제 당국의 승리는 경 카테터 솔루션의 최전선을 유지하고 있습니다. 폴리머 혁신 기업인 Foldax와 4C Medical은 내구성에 대한 기대를 재구성하고 경쟁 차별화를 촉진합니다. 장비 플랫폼이 여러 위치에 대응함으로써 임상적 수용성이 확대되고 인공 심장 판막 시장의 카테터 기반 치료에 대한 방향성이 강화됩니다.

무봉합 플랫폼은 크로스 클램프 시간을 단축하고 미래의 밸브 인 밸브 개입을 용이하게 함으로써 개복 수술과 카테터 절차의 경계를 모호하게 만듭니다. 이 하이브리드 진화는 수술의 통제를 포기하지 않고보다 빠른 절차를 요구하는 외과 의사를 끌어들입니다. LivaNova의 Perceval Plus와 같은 신속한 전개가 가능한 밸브는 처리량과 치료 성과의 균형을 중시하는 시설에 어필하고, 보다 넓은 인공 심장 밸브 시장에서의 점유율 확대를 촉진하고 있습니다.

대동맥 판막은 2024년 매출의 56.53%를 차지했으며 성숙한 증거 기반과 합리화된 상환 경로에 의해 지원됩니다. 대동맥 판막 협착증의 유병률은 나이가 들수록 증가하기 때문에 환자 수요는 계속 왕성하지만, 고소득 시장으로의 보급이 안정됨에 따라 성장은 완만해집니다. 삼첨판 인터벤션은 Edwards의 EVOQUE 승인과 Abbott의 TriClip 시험 성공에 힘입어 전체 포지션 중 가장 빠른 예측 CAGR 15.15%를 기록했습니다. 승모판 프로그램은 SAPIEN M3의 CE 마크 취득에 의해 경대퇴 접근이 해금되어 기세를 늘리고 있습니다. 전문 기업은 Venus P-valve와 같은 확장된 유출로를 위한 장치에서 폐의 요구를 충족시킵니다.

대동맥 제품의 인공 심장 판막 시장 점유율은 삼첨판과 승모판의 성장이 기존의 볼륨을 능가하기 때문에 소폭 축소가 예상됩니다. 경 카테터 삼첨판 수술의 증거 개발에서 CMS의 적용은 미국에서의 보급을 가속화할 것으로 보입니다. 동시에 아시아태평양의 기업들은 Venus Medtech의 승모판 플랫폼 등 지역 해부학적 구조에 적합한 부위 특이적 장치를 개발하여 경쟁력을 다양화하고 있습니다. 포지션 특화가 깊어짐에 따라 제조업체는 해부학적 뉘앙스에 맞는 규제 스케줄과 임상시험을 확보하여 인공심장판 시장의 지속적인 성장을 지원하고 있습니다.

지역 분석

북미는 2024년 매출액의 42.52%를 차지하며 확립된 보험상환, 견고한 임상 인프라, 조기도입자 마인드셋을 통해 주도권을 굳혔습니다. CMS의 보험 적용 확대는 치료법의 성장을 가속하고 민간 보험 회사는 일반적으로 메디케어의 자세를 반영하여 광범위한 액세스를 확보하고 있습니다. 미국은 2037년까지 8,650명의 심장 전문의가 부족하다는 문제에 직면하고 있으며, 연수 파이프라인이 가속되지 않으면 이 제약이 절차의 성장을 둔화시킬 수 있습니다. 캐나다는 주 의료 제도가 통합되어 TAVR 건수가 증가하고 있습니다. 멕시코의 현대화하는 민간 부문과 국경을 넘은 의료 관광은 틈새 성장 요인입니다.

아시아태평양은 인프라 투자, 규제 조화, 국내 기술 혁신에 힘입어 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 14.12%가 될 것으로 보입니다. 중국 국가 의료 제품 감독 관리국(NMPA)에서 MicroPort의 VitaFlow Liberty Flex 승인은 국산 경경 카테터 선택을 확대합니다. 일본과 한국은 고령화 사회와 국민 모두 보험제도를 활용하여 도입을 가속합니다. 인도는 심장치료 프로그램이 대도시 중심부 이외에도 확대되어 장기적인 가능성을 보여줍니다. 해부학적인 차이, 특히 동아시아 환자에서는 대동맥 판륜이 작기 때문에 지역 특유의 밸브 사이징이 필요하며 현지 연구 개발이 강화됩니다. 호주는 임상시험의 핵심 역할을 하며 지역 기술 이전과 증거 창출을 지원합니다.

유럽은 조정된 규제와 강력한 임상의 네트워크를 지원하며 균형 잡힌 성장 전망을 유지하고 있습니다. 독일, 영국, 프랑스, 이탈리아, 스페인은 수년간의 TAVR 프로그램과 표준화된 커리큘럼에 지원되어 수술 건수의 핵심을 이루고 있습니다. Edwards SAPIEN M3의 CE 마크는 경대 승모판 솔루션의 런치 패드로서 유럽의 역할을 강조합니다. 동유럽은 뒤쳐져 있지만 경제가 수렴하기 때문에 가능성이 있습니다. 한편, 중동, 아프리카, 남미는 작은 기반에서 성장하고 있습니다. 탁월한 센터에 대한 선택적인 투자로 의사를 양성하고 성과를 입증하는 지역의 허브가 형성되어 인공 심장 판막 시장에 대한 접근이 점차 확산되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고령화 및 VHD 유병률 상승

- TAVR/TAVI 적응 확대

- 규제 당국의 패스트 트랙과 브레이크스루 지정

- 중소득국에서의 상환 확대

- 폴리머 밸브 연구 개발의 돌파구

- AI에 의한 환자 선택과 사이징 툴

- 시장 성장 억제요인

- 높은 TAVR 장치와 수술 비용

- 젊은층에서의 내구성에 대한 우려

- Tier 1 도시 이외의 심혈관 조영실 용량은 한정적

- 밸브 인 밸브 재도입의 급증

- 기술의 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 밸브 유형별

- 기계식 심장 밸브

- 조직 및 생체 인공 심장 판막

- 경 카테터 심장 밸브(TAVR/TMVR/TTVR/TPVR)

- 폴리머 및 차세대 심장 밸브

- 포지션별

- 대동맥

- 승모판

- 삼첨판

- 폐

- 제공 방법별

- 수술(SAVR/SMVR)

- 트랜스 카테터

- 무봉합 및 신속 전개

- 최종 사용자별

- 제3차 의료 병원

- 심장 전문센터

- 외래수술센터(ASC)

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Edwards Lifesciences

- Medtronic plc

- Abbott Laboratories

- Boston Scientific Corp.

- Artivion(CryoLife)

- LivaNova PLC

- MicroPort CardioFlow

- Jenavalve Technology

- Foldax Inc.

- Lepu Medical

- On-X Life Technologies

- Terumo Corp.

- Colibri Heart Valve

- TTK Healthcare

- Meril Life Sciences

- Teleflex(Chordis)

- NaviGate Cardiac Structures

- Peijia Medical

- Xeltis NV

제7장 시장 기회와 장래의 전망

JHS 25.11.21The prosthetic heart valve market reached USD 13.35 billion in 2025 and is forecast to grow to USD 23.32 billion by 2030, registering an 11.8% CAGR over the period.

Demographic ageing, expanded indications for transcatheter aortic valve replacement (TAVR), and faster regulatory reviews position transcatheter innovation as the primary growth engine of the prosthetic heart valve market. Edwards Lifesciences obtained United States Food and Drug Administration (FDA) approval in May 2025 for the SAPIEN 3 platform in asymptomatic severe aortic stenosis, enlarging the treatable population beyond symptomatic patients. Transcatheter heart valves held 45.55% of revenue in 2024, while tricuspid systems such as Edwards' EVOQUE and Abbott's TriClip have accelerated into double-digit growth after first-in-class clearances. Hospitals continue to dominate procedure volumes, yet ambulatory surgical centers (ASCs) are expanding fastest as same-day discharge protocols reduce inpatient reliance. North America generates the largest share, but Asia-Pacific is the high-growth frontier thanks to local approvals like MicroPort's VitaFlow Liberty Flex in China. Portfolio consolidation-exemplified by Edwards' USD 300 million Innovalve purchase and Johnson & Johnson's USD 1.7 billion V-Wave deal-further intensifies competition.

Global Prosthetic Heart Valve Market Trends and Insights

Expanding Indications for TAVR/TAVI

The May 2025 FDA approval of Edwards' SAPIEN 3 platform for asymptomatic severe aortic stenosis removes the "watchful waiting" mindset, allowing clinicians to intervene before symptom onset. EARLY TAVR data showed 26.8% adverse events with early treatment versus 45.3% under surveillance during 3.8-year follow-up, validating proactive therapy and effectively doubling the addressable pool. Edwards forecasts TAVR sales of USD 4.1-4.4 billion in 2025, and rivals such as Abbott have launched the ENVISION trial to capture lower-risk patients. Centers for Medicare & Medicaid Services (CMS) coverage decisions will shape adoption because private payers typically mirror Medicare precedent. As coverage broadens, procedure volumes rise, reinforcing the prosthetic heart valve market's shift toward transcatheter dominance.

Regulatory Fast-Tracks & Breakthrough Designations

Breakthrough device designations hit a record 1,041 by September 2024; 128 authorized products demonstrate how the pathway compresses approvals from 3-5 years to around 18-24 months. Edwards' EVOQUE tricuspid valve capitalized on breakthrough status to secure February 2024 clearance, while 4C Medical's polymer AltaValve holds two breakthrough labels. Europe parallels this urgency, granting the world's first transfemoral mitral CE mark to SAPIEN M3 in April 2025. Companies that lock in early designations gain speed-to-market advantages, boosting revenue and brand positioning within the prosthetic heart valve market.

High TAVR Device & Procedure Costs

Commercial US payers reimburse a median USD 71,312 for TAVR, versus Medicare's USD 37,865; Aetna tops at USD 84,190, and prices vary two-fold between New England and Pacific regions. Europe and North America together spend over USD 2 billion annually on TAVR, pressuring budgets. Emerging markets face larger hurdles, as devices can exceed annual per-capita healthcare outlays. Spain's incremental cost-effectiveness ratio of EUR 6,952 per QALY is below threshold, but payer constraints limit immediate uptake. Manufacturers are exploring value-based contracts, yet high prices remain a brake on the prosthetic heart valve market.

Other drivers and restraints analyzed in the detailed report include:

- Polymeric Valve R&D Breakthroughs

- AI-Guided Patient Selection & Sizing Tools

- Durability Concerns in Younger Cohorts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transcatheter heart valves accounted for 45.55% of 2024 revenue, underlining their rapid shift from salvage therapy to first-line option across risk profiles. This segment anchors the prosthetic heart valve market through streamlined procedures that shorten hospital stays and widen eligibility. Polymeric valves represent the fastest-growing niche, delivering an 18.25% CAGR through 2030 because materials resist calcification without anticoagulation, appealing to active patients. Tissue valves retain relevance for conventional surgery, while mechanical devices remain the choice for select younger users who accept lifelong anticoagulation in exchange for durability. Regulatory wins-such as Edwards' SAPIEN 3 for asymptomatic patients and the EVOQUE tricuspid system-keep transcatheter solutions at the forefront. Polymeric innovators Foldax and 4C Medical are reshaping durability expectations, catalyzing competitive differentiation. Clinical acceptance broadens as device platforms address multiple positions, reinforcing the prosthetic heart valve market's direction toward catheter-based therapy.

Sutureless platforms blur the line between open surgery and catheter techniques by offering shorter cross-clamp times and facilitating future valve-in-valve interventions. This hybrid evolution attracts surgeons who seek faster procedures without relinquishing operative control. Rapid-deployment valves, such as LivaNova's Perceval Plus, appeal to institutions balancing throughput and outcomes, prompting incremental share gains within the broader prosthetic heart valve market.

Aortic valves represented 56.53% of revenue in 2024, buttressed by a mature evidence base and streamlined reimbursement pathways. Patient demand remains strong because aortic stenosis prevalence rises with age, yet growth moderates as penetration in high-income markets stabilizes. Tricuspid interventions recorded a 15.15% forecast CAGR, the fastest among all positions, buoyed by Edwards' EVOQUE approval and trial success for Abbott's TriClip. Mitral programs gain momentum as the SAPIEN M3 CE mark unlocks the transfemoral approach. Specialized firms address pulmonary needs with devices such as the Venus P-valve for enlarged outflow tracts.

The prosthetic heart valve market share for aortic products is expected to narrow modestly as tricuspid and mitral growth outpaces traditional volumes. CMS coverage under Evidence Development for transcatheter tricuspid procedures will accelerate US uptake. Simultaneously, Asia-Pacific companies craft position-specific devices suited to local anatomies, such as Venus Medtech's mitral platform, diversifying competitive dynamics. As position specialization deepens, manufacturers secure regulatory timelines and clinical trials tailored to anatomical nuance, anchoring durable growth within the prosthetic heart valve market.

The Prosthetic Heart Valve Market Report is Segmented by Valve Type (Mechanical Heart Valve, Bioprosthetic Heart Valve, and More), Position (Mitral, Aortic, Tricuspid, and Pulmonary), Delivery Method (Surgical, Transcatheter and Sutureless), End-User (Tertiary-Care Hospitals, Cardiac Specialty Centers, and More), and Geography (North America, Europe, Asia Pacific and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 42.52% of 2024 revenue, cementing its leadership through established reimbursement, robust clinical infrastructure, and early adopter mindsets. CMS coverage expansions drive procedure growth, and private insurers generally mirror Medicare's stance, ensuring broad access. The United States faces a looming 8,650-cardiologist shortfall by 2037, a constraint that may dampen procedure growth if training pipelines do not accelerate. Canada benefits from integrated provincial health systems and rising TAVR volumes. Mexico's modernizing private sector and cross-border medical tourism represent niche growth contributors.

Asia-Pacific delivers the fastest 14.12% CAGR through 2030, propelled by infrastructure investment, regulatory harmonization, and domestic innovation. China's National Medical Products Administration (NMPA) approval of MicroPort's VitaFlow Liberty Flex expands home-grown transcatheter options. Japan and South Korea leverage ageing populations and universal coverage to accelerate uptake. India exhibits long-term potential as cardiac programmes expand beyond metro hubs. Anatomical differences, notably smaller aortic annuli in East Asian patients, necessitate region-specific valve sizing and reinforce local R&D. Australia functions as a clinical trial nucleus, supporting regional skill transfer and evidence generation.

Europe sustains a balanced growth outlook, underpinned by coordinated regulation and strong clinician networks. Germany, United Kingdom, France, Italy, and Spain anchor procedural volumes, supported by long-standing TAVR programmes and standardized curricula. Edwards' SAPIEN M3 CE mark emphasises Europe's role as a launch pad for transfemoral mitral solutions. Eastern Europe lags but offers catch-up potential as economies converge. Meanwhile, the Middle East, Africa, and South America grow from a small base; selective investments in centres of excellence create regional hubs that train physicians and demonstrate outcomes, progressively widening access to the prosthetic heart valve market.

- Edward Lifesciences

- Medtronic

- Abbott Laboratories

- Boston Scientific

- Artivion (CryoLife)

- LivaNova

- MicroPort CardioFlow

- Jenavalve Technology

- Foldax Inc.

- Lepu Medical

- On-X Life Technologies

- Terumo Corp.

- Colibri Heart Valve

- TTK Healthcare

- Meril Life Sciences

- Teleflex (Chordis)

- NaviGate Cardiac Structures

- Peijia Medical

- Xeltis NV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population & Rising VHD Prevalence

- 4.2.2 Expanding Indications For TAVR/TAVI

- 4.2.3 Regulatory Fast-Tracks & Breakthrough Designations

- 4.2.4 Reimbursement Expansion In Middle-Income Countries

- 4.2.5 Polymeric Valve R&D Breakthroughs

- 4.2.6 AI-Guided Patient Selection & Sizing Tools

- 4.3 Market Restraints

- 4.3.1 High TAVR Device & Procedure Costs

- 4.3.2 Durability Concerns In Younger Cohorts

- 4.3.3 Limited Cath-Lab Capacity Outside Tier-1 Cities

- 4.3.4 Surge In Valve-In-Valve Re-Interventions

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Valve Type

- 5.1.1 Mechanical Heart Valve

- 5.1.2 Tissue/Bioprosthetic Heart Valve

- 5.1.3 Transcatheter Heart Valve (TAVR/TMVR/TTVR/TPVR)

- 5.1.4 Polymeric/Next-Gen Heart Valve

- 5.2 By Position

- 5.2.1 Aortic

- 5.2.2 Mitral

- 5.2.3 Tricuspid

- 5.2.4 Pulmonary

- 5.3 By Delivery Method

- 5.3.1 Surgical (SAVR/SMVR)

- 5.3.2 Transcatheter

- 5.3.3 Sutureless/Rapid-deployment

- 5.4 By End-user

- 5.4.1 Tertiary-care Hospitals

- 5.4.2 Cardiac Specialty Centers

- 5.4.3 Ambulatory Surgical Centers

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Edwards Lifesciences

- 6.3.2 Medtronic plc

- 6.3.3 Abbott Laboratories

- 6.3.4 Boston Scientific Corp.

- 6.3.5 Artivion (CryoLife)

- 6.3.6 LivaNova PLC

- 6.3.7 MicroPort CardioFlow

- 6.3.8 Jenavalve Technology

- 6.3.9 Foldax Inc.

- 6.3.10 Lepu Medical

- 6.3.11 On-X Life Technologies

- 6.3.12 Terumo Corp.

- 6.3.13 Colibri Heart Valve

- 6.3.14 TTK Healthcare

- 6.3.15 Meril Life Sciences

- 6.3.16 Teleflex (Chordis)

- 6.3.17 NaviGate Cardiac Structures

- 6.3.18 Peijia Medical

- 6.3.19 Xeltis NV

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment