|

시장보고서

상품코드

1851190

자동차 배터리 관리 시스템 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Battery Management Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

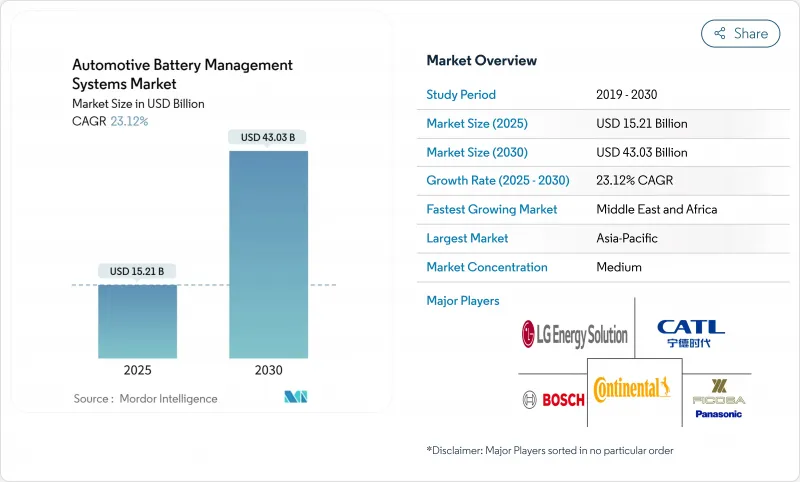

세계의 자동차 배터리 관리 시스템 시장 규모는 2025년 152억 1,000만 달러로, 2030년까지 430억 3,000만 달러에 이를 것으로 예측됩니다.

이 확장은 내연 엔진에서 전동화 추진으로의 세계적인 움직임을 반영한 것으로, 배터리 관리 시스템(BMS)이 차량의 중추 신경계로서 기능합니다. 2024년 신차종에 적용되는 ISO 21434 사이버 보안 규정으로 대표되는 규제 압력은 사이버 보안 설계에 대한 수요를 가속화하고 있습니다. 동시에 하드 와이어에서 모듈러 및 무선 토폴로지로의 급속한 전환으로 하네스의 경량화, 에너지 밀도 향상, 조립 시간 단축이 진행되고 있습니다. 2025년 OEM 시험용으로 출시된 NXP 초광대역 BMS와 같은 무선 솔루션은 차세대 아키텍처가 안전성, 효율성 및 비용 목표를 어떻게 일치시킬 수 있는지 보여줍니다. 전기차(EV) 판매 목표 증가, 배터리 팩 비용 감소, 리튬 철 인산염(LFP) 화학물질의 주류 채용은 셀 및 모듈 수준에서 더 많은 인텔리전스를 배치하는 설계 업그레이드를 계속 자극하며 자동차 배터리 관리 시스템 시장의 견조한 성장 경로를 강화하고 있습니다.

세계 자동차 배터리 관리 시스템 시장 동향과 통찰

세계적으로 확대되는 EV 판매 의무

EU 및 캘리포니아 주와 같은 지역에서 ZEV 정책이 시행되어 내구성, 항속 거리 유지, 배터리 건전성 투명성에 대한 기준치가 높아집니다. Euro 7 규제는 2026년에 발효되며, 캘리포니아 주 첨단 클린카 II는 15만 마일 주행으로 80%의 항속 거리 유지를 요구하고 있기 때문에 BMS 공급업체는 보다 정교한 건전성 분석과 열화 모델링을 도입할 필요가 있습니다. 규칙의 조화는 세계 플랫폼이 하나의 컴플라이언스 대응 아키텍처를 채용하는 동기부여가 되고, OEM이 지역 고유의 설계를 회피함으로써, 자동차 배터리 관리 시스템 시장을 상승시킵니다. 이미 적응 알고리즘을 통합한 공급업체는 선수를 치지만 레거시 공급자는 검증 주기와 비용 증가에 직면합니다.

배터리 팩 비용 저하

리튬 이온 배터리 팩 가격의 급속한 하락은 비용 구조를 재구성하고 있습니다. 주류 LFP 팩은 2024년에는 1kWh당 평균 75달러가 되고, 나트륨 이온의 시험 운용에서는 1kWh당 10달러라는 저비용이 입증되었습니다. 셀이 저렴해짐에 따라 OEM은 배터리 예산의 대부분을 하드웨어 비용 절감에만 집중하는 것이 아니라 예측 분석 및 무선 연결과 같은 더 스마트한 BMS 기능에 할당할 수 있습니다. 이러한 팩당 가치가 높은 컨텐츠로의 전환은 자동차 배터리 관리 시스템 시장 전반에 걸쳐 고급 배터리 관리 솔루션에 대한 수요를 강화하고 있습니다.

열폭주 리콜에 의한 보증충당금 증가

주목을 받은 화재 사고는 대규모 리콜로 이어지며, 자동차 제조업체는 보증 충당금의 증대와 보수적인 팩 설계의 채용을 강요하고 있습니다. Samsung SDI의 다중 브랜드 리콜과 Hyundai Mobis의 자기 소화 모듈 개발은 업계의 긴급성을 강조합니다. 절연, 화재 억제, 중복 센서의 추가 비용은 실험적인 BMS 기능의 전개를 지연시키고 자동차 배터리 관리 시스템 시장의 당면 성장을 억제할 수 있습니다.

부문 분석

배터리 센서는 2024년 자동차 배터리 관리 시스템 시장 점유율의 35.41%를 차지했고, 2030년까지 CAGR 24.66%로 예측됩니다. 온도, 압력, 오프 가스 및 습도를 다루는 다중 물리 감지의 보급으로 OEM은 수동 보호에서 실시간 예측 진단으로 전환 할 수 있습니다. 규제 당국이 열폭주 감지 강화를 요구하고, 플릿 오퍼레이터가 듀티 사이클과 보증 범위를 최적화하기 위해 세밀한 데이터를 요구함에 따라 채용이 가속화됩니다. CO2 및 H2 센서를 모듈 레벨 보드에 통합하면 조기 경고 기능이 향상되고 비용이 많이 드는 리콜 및 다운타임을 피할 수 있습니다. EV 팩의 전압이 800V를 초과하면 고해상도 션트 센서 및 홀 효과 센서가 정확한 충전 상태와 건강 상태를 추정하는 데 필수적이므로 이 부문의 장기적인 확장이 보장됩니다.

셀 레벨 전압 정확도는 현재 -2mV에 도달하여 보다 미세한 충전 밸런스와 팩 수명의 연장을 가능하게 하므로 IC 정확도가 결정적인 구매 기준이 됩니다. 선도적인 칩 제조업체는 측정, 밸런싱 및 통신 블록을 단일 다이에 융합시켜 보드 풋 프린트를 줄이고 차량 자격을 단순화합니다. 열전도성 갭 필러, 에어로겔 시트 및 상변화 복합재료를 포함한 ``기타 전자 및 재료'' 버킷은 에너지 밀도가 증가함에 따라 계속 확대되고 뛰어난 열확산 및 절연 솔루션이 요구되고 있습니다.

2024년 자동차 배터리 관리 시스템 시장 점유율의 48.95%는 모듈형입니다. 센싱과 액추에이션을 박스 레벨로 분리함으로써 상용 플릿이나 가동률이 높은 라이드 헤일링 차량에 적합한 내장해성을 실현합니다. 또한 하드웨어 블록의 증분화를 통해 라인 측에서 신속한 교환이 가능해 차량 가동 시간이 향상됩니다.

무선 설계는 급속히 확장되고 있으며, 안테나의 소형화, 보안 메쉬 프로토콜, 인증된 RF 스택의 생산 성숙에 따라 2025-2030년의 CAGR은 35.17%에 달할 전망입니다. 데이지 체인 하네스를 제거하면 팩의 무게가 줄어들고 활성 냉각 플레이트와 여분의 셀을 위해 귀중한 입방 센티미터가 열립니다. 한편, 틈새 분산 아키텍처는 모터스포츠 및 항공우주 크로스오버 프로그램의 극단적인 중복성 요구에 대응하여 자동차 배터리 관리 시스템 시장 내 제품의 다양성을 완화하고 있습니다.

지역 분석

아시아태평양은 2024년 자동차 배터리 관리 시스템 시장에서 61.33%의 압도적인 점유율을 유지했습니다. 중국은 업스트림 정화에서 최종 차량 조립에 이르기까지 수직 통합 배터리의 밸류체인로 비용 구조를 압축하고 설계 반복을 가속화하고 있습니다. 정부의 구매 장려금, 대도시의 유리한 번호판 정책, 성숙한 충전 생태계가 EV의 보급을 촉진하고 BMS 출하량을 증가시킵니다. 중국의 셀 모듈 공급업체가 폴란드, 헝가리, 네바다에 공장을 개설하고, 관세가 걸리지 않는 액세스를 확보하고, 물류 레인을 단축하고 있기 때문에 공급 체인의 레버리지는 유럽과 북미에까지 확장하고 있습니다.

중동 및 아프리카은 저수준에서 벗어나 2030년까지 연평균 복합 성장률(CAGR)이 27.55%로 가장 급성장할 있는 지역입니다. 두바이, 리야드, 카이로에서는 e-bus 코리도와 내열 BMS 설계를 필요로 하는 마지막 마일 배송의 전기 목표가 전개되고 있습니다. 관민 제휴에 의해 계통 연계 축전지에 대한 투자가 촉진되어 재이용되는 차량 팩이나 중고 BMS 소프트웨어의 인접 판매가 창출됩니다.

인플레이션 억제법이 국내 셀과 모듈 제조에 활력을 주고 북미가 기세를 늘립니다. BMW, Toyota, Hyundai에 의한 캐롤라, 조지아, 온타리오의 투자는 아시아의 수입품에 대한 의존도를 줄이고 BMS 기판의 현지 조달을 지원합니다. 유럽은 여전히 규제의 선구자이며, 향후 예정된 배터리 패스포트 시스템의 복잡성과 소프트웨어의 내용을 증가시키는 추적성 기능을 추진하고 있습니다. 이러한 요구사항은 차량 1대당 수익을 높이고 안전한 클라우드 파이프라인을 준비하는 공급업체를 차별화하며 자동차 배터리 관리 시스템 시장의 건전한 전반적인 전망을 유지합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계적으로 확대되는 EV 판매 의무

- 배터리 팩의 비용 저하

- 집중형에서 모듈형, 무선형 토폴로지로의 이행

- 고급 액티브 밸런싱을 필요로 하는 LFP 화학 수요 급증

- ISO 21434 주도의 「사이버 보안 BMS」 수요

- IP 로열티 비용 절감을 위해 BMS ASIC 설계를 내제화하는 OEM의 움직임

- 시장 성장 억제요인

- 열폭주 리콜로 보증충당금 인상한다

- 심각한 파워 반도체 부족

- 2027년 이후 EU 「배터리 패스포트」 추적 가능성의 오버헤드

- AI 기반 예측 BMS는 아직 기능 안전 인증이 부족

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 컴포넌트별

- 배터리 IC

- 배터리 센서

- 기타 일렉트로닉스 및 재료

- 토폴로지별

- 집중형

- 모듈러

- 분산형

- 무선

- 추진 유형별

- 하이브리드 전기자동차(HEV)

- 플러그인 하이브리드 자동차(PHEV)

- 배터리 전기자동차(BEV)

- 연료전지 전기자동차(FCEV)

- 차량 유형별

- 승용차

- 소형 상용차

- 중대형 상용차

- 이륜차 및 삼륜차

- 오프 하이웨이 및 특수 차량

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 이집트

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- LG Energy Solution

- CATL

- Panasonic(Ficosa)

- Robert Bosch GmbH

- Continental AG

- Texas Instruments

- Analog Devices

- Infineon Technologies

- NXP Semiconductors

- Renesas Electronics

- Hitachi Astemo

- Mitsubishi Electric

- Denso Corporation

- Preh GmbH

- Eaton Mobility(Eatron)

- Lithium Balance

- Sensata Technologies

- Eberspacher Vecture

- Rimac Technology

제7장 시장 기회와 장래의 전망

JHS 25.11.21The automotive battery management system market size is valued at USD 15.21 billion in 2025 and is forecast to climb to USD 43.03 billion in 2030, reflecting a vigorous 23.12% CAGR.

This expansion mirrors the global pivot from internal-combustion engines toward electrified propulsion, where a battery management system (BMS) functions as the vehicle's central nervous system. Regulatory pressure, notably ISO 21434 cybersecurity rules that came into force for new vehicle models in 2024, is accelerating demand for cyber-secure designs. At the same time, rapid migration from hard-wired to modular and wireless topologies is trimming harness weight, boosting energy density, and shortening assembly time. Wireless solutions such as NXP's ultra-wideband BMS, released for OEM trials in 2025, exemplify how next-generation architectures can align safety, efficiency, and cost goals. Heightened electric-vehicle (EV) sales targets, falling battery pack cost, and mainstream adoption of lithium-iron-phosphate (LFP) chemistries continue to stimulate design upgrades that place more intelligence at the cell and module level, reinforcing a robust growth path for the automotive battery management system market.

Global Automotive Battery Management Systems Market Trends and Insights

EV sales mandates widening globally

Binding ZEV policies in regions such as the EU and California raise the baseline for durability, range retention, and transparency of battery health. Euro 7 rules will be effective in 2026, and California's Advanced Clean Cars II demands 80% range retention for 150,000 miles, compelling BMS suppliers to incorporate more refined state-of-health analytics and degradation modeling. Harmonizing rules incentivize global platforms to adopt one compliance-ready architecture, elevating the automotive battery management system market as OEMs avoid region-specific designs. Suppliers that already embed adaptive algorithms gain a head start, whereas legacy providers face added validation cycles and cost.

Falling cost of battery packs

Rapid declines in lithium-ion battery-pack prices are reshaping cost structures. Mainstream LFP packs averaged USD 75 per kWh in 2024, and pilot sodium-ion runs have demonstrated costs as low as USD 10 per kWh. As cells get cheaper, OEMs can allocate larger portions of the battery budget to smarter BMS functions, such as predictive analytics and wireless connectivity, rather than focusing solely on hardware cost reduction. This shift toward higher value content per pack reinforces demand for advanced battery management solutions across the automotive battery management system market.

Thermal-runaway recalls raising warranty reserves

High-profile fire events have led to sizable recalls, forcing automakers to boost warranty accruals and adopt conservative pack design. Samsung SDI's multi-brand recall and Hyundai Mobis' development of self-extinguishing modules underscore industry urgency. Added cost for insulation, fire suppression, and redundant sensors can slow deployment of experimental BMS functions, tempering near-term growth in the automotive battery management system market.

Other drivers and restraints analyzed in the detailed report include:

- Shift from centralized to modular and wireless topologies

- Soaring demand for LFP chemistry requiring advanced active balancing

- Acute power-semiconductor shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Battery Sensors captured 35.41% of the automotive battery management system market share in 2024, and the segment is forecast to post a 24.66% CAGR through 2030. Wider deployment of multi-physics sensing, covering temperature, pressure, off-gas, and humidity, allows OEMs to move from passive protection toward real-time predictive diagnostics. Adoption accelerates as regulators demand enhanced thermal-runaway detection and as fleet operators seek granular data to optimize duty cycles and warranty coverage. Integrating CO2 and H2 sensors into module-level boards improves early-warning capabilities, helping avoid costly recalls and downtime. As EV packs scale above 800 V, high-resolution shunt and Hall-effect sensors become indispensable for accurate state-of-charge and state-of-health estimation, cementing the segment's long-term expansion path.

Tight cell-level voltage accuracy, now reaching +-2 mV, enables finer charge balancing and extended pack life, making IC precision a decisive purchase criterion. Leading chipmakers have fused measurement, balancing, and communication blocks onto single dies, shrinking board footprints and simplifying automotive qualifications. The residual "Other electronics and materials" bucket, encompassing thermally conductive gap fillers, aerogel sheets, and phase-change composites, continues to broaden as energy density rises, calling for superior heat-spreading and insulation solutions.

In 2024, Modular arrangements accounted for 48.95% of the automotive battery management system market share, reflecting OEM preference for scalable sub-battery modules that can be rearranged without wholesale redesign. Box-level isolation of sensing and actuation delivers fault tolerance suited to commercial fleets and high-utilization ride-hailing vehicles. Incremental hardware blocks also facilitate rapid line-side replacement, lifting vehicle uptime.

Wireless designs are scaling rapidly, showing a 35.17% CAGR across 2025-2030 as antenna miniaturization, secure mesh protocols, and certified RF stacks reach production maturity. Eliminating daisy-chain harnesses cuts pack weight and opens valuable cubic centimeters for active cooling plates or extra cells. Centralized topologies continue in entry-price passenger cars, where minimal components trump expandability, whereas niche distributed architectures meet extreme redundancy mandates in motorsports and aerospace crossover programs, cushioning product diversity inside the automotive battery management system market.

The Automotive Battery Management System Market Report is Segmented by Component (Battery IC, Battery Sensors, and More), Topology (Centralized, Modular, and More), Propulsion Type (Hybrid Electric Vehicle (HEV), Battery Electric Vehicle (BEV), and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained a commanding 61.33% share of the automotive battery management system market in 2024. China's vertically integrated battery value chain-from upstream refining to final vehicle assembly-compresses cost structures and quickens design iterations. Government purchase incentives, favorable license-plate policies in megacities, and a mature charging ecosystem lift EV penetration and reinforce BMS unit shipments. Supply-chain leverage even extends to Europe and North America, as Chinese cell and module suppliers open factories in Poland, Hungary, and Nevada to secure tariff-free access and shorten logistics lanes.

The Middle East and Africa region, although emerging from a low base, is the fastest-growing region with a 27.55% CAGR through 2030. Dubai, Riyadh, and Cairo are rolling out e-bus corridors and last-mile delivery electrification targets that demand heat-tolerant BMS designs. Public-private alliances channel investment into grid-tied battery storage, creating adjacent sales for repurposed vehicle packs and second-life BMS software.

North America gains momentum as the Inflation Reduction Act galvanizes domestic cell and module manufacturing. Investments by BMW, Toyota, and Hyundai in the Carolinas, Georgia, and Ontario shrink reliance on Asian imports and underpin local sourcing of BMS boards. Europe remains a regulatory trailblazer, with the upcoming battery passport pushing traceability features that increase system complexity and software content. Such requirements elevate per-vehicle revenue and differentiate suppliers ready with secure cloud pipelines, sustaining a healthy overall outlook for the automotive battery management system market.

- LG Energy Solution

- CATL

- Panasonic (Ficosa)

- Robert Bosch GmbH

- Continental AG

- Texas Instruments

- Analog Devices

- Infineon Technologies

- NXP Semiconductors

- Renesas Electronics

- Hitachi Astemo

- Mitsubishi Electric

- Denso Corporation

- Preh GmbH

- Eaton Mobility (Eatron)

- Lithium Balance

- Sensata Technologies

- Eberspacher Vecture

- Rimac Technology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV sales mandates widening globally

- 4.2.2 Falling cost of battery packs

- 4.2.3 Shift from centralized to modular and wireless topologies

- 4.2.4 Soaring demand for LFP chemistry requiring advanced active balancing

- 4.2.5 ISO 21434-driven "cyber-secure BMS" demand

- 4.2.6 OEM move to in-house BMS ASIC design to cut IP royalty cost

- 4.3 Market Restraints

- 4.3.1 Thermal-runaway recalls raising warranty reserves

- 4.3.2 Acute power-semiconductor shortages

- 4.3.3 Post-2027 EU "battery-passport" traceability overheads

- 4.3.4 AI-based predictive BMS still lacks functional-safety certification

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Component

- 5.1.1 Battery IC

- 5.1.2 Battery Sensors

- 5.1.3 Other Electronics and Materials

- 5.2 By Topology

- 5.2.1 Centralized

- 5.2.2 Modular

- 5.2.3 Distributed

- 5.2.4 Wireless

- 5.3 By Propulsion Type

- 5.3.1 Hybrid Electric Vehicle (HEV)

- 5.3.2 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.3.3 Battery Electric Vehicle (BEV)

- 5.3.4 Fuel-Cell Electric Vehicle (FCEV)

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Medium and Heavy Commercial Vehicles

- 5.4.4 Two and Three-Wheelers

- 5.4.5 Off-Highway and Specialty Vehicles

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 LG Energy Solution

- 6.4.2 CATL

- 6.4.3 Panasonic (Ficosa)

- 6.4.4 Robert Bosch GmbH

- 6.4.5 Continental AG

- 6.4.6 Texas Instruments

- 6.4.7 Analog Devices

- 6.4.8 Infineon Technologies

- 6.4.9 NXP Semiconductors

- 6.4.10 Renesas Electronics

- 6.4.11 Hitachi Astemo

- 6.4.12 Mitsubishi Electric

- 6.4.13 Denso Corporation

- 6.4.14 Preh GmbH

- 6.4.15 Eaton Mobility (Eatron)

- 6.4.16 Lithium Balance

- 6.4.17 Sensata Technologies

- 6.4.18 Eberspacher Vecture

- 6.4.19 Rimac Technology

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment