|

시장보고서

상품코드

1851201

고속 액체 크로마토그래피(HPLC) : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)High-Performance Liquid Chromatography (HPLC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

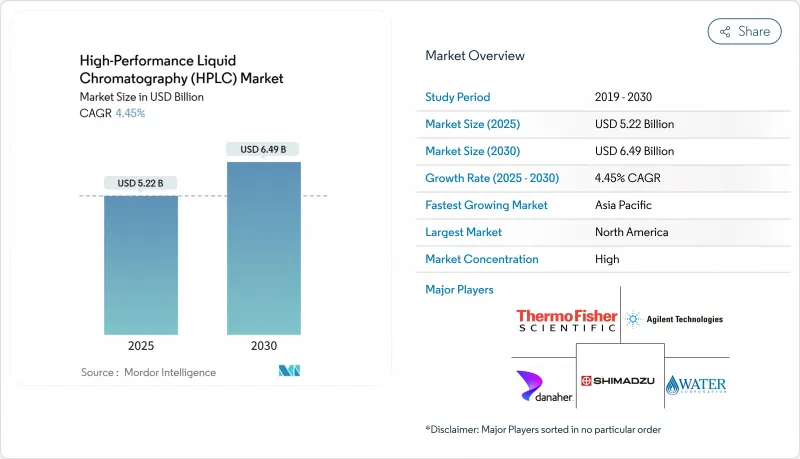

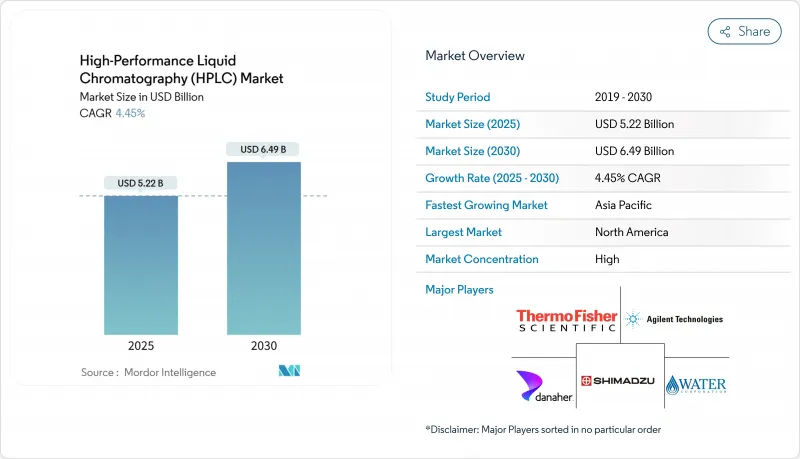

고속 액체 크로마토그래피(HPLC) 시장의 2025년 시장 규모는 52억 2,000만 달러로, 2030년에는 64억 9,000만 달러, CAGR은 4.45%를 나타낼 것으로 예측되고 있습니다.

진보하는 컬럼 케미스트리, 초고압 펌프 및 자동화 소프트웨어는 시스템 생산성을 향상시키지만 용매 사용량을 줄입니다. 의약품의 품질 관리, 실시간 바이오프로세스 모니터링, 임상 진단에 대한 폭넓은 도입이 설치 베이스를 확대하고, 새로운 과·다플루오로알킬 물질(PFAS) 규제가 환경 검사에 새로운 수요를 더하고 있습니다. 공급업체는 또한 방법 개발 시간 단축, 피크 식별 정확도 향상 및 반복 실행 횟수 감소를 위해 장비 제어 및 데이터 처리에 인공지능을 통합하려고 합니다. 특히 아시아태평양에서는 헬스케어 지출 증가와 현지 제조업 인센티브가 일치하고 있습니다.

세계의 고속 액체 크로마토그래피(HPLC) 시장 동향과 인사이트

HPLC 기술의 진보 : 소형화가 이식성 혁명을 촉진

소형 장치는 분석을 중앙 실험실에서 현장으로 옮겨 원격지에서 신속한 의사 결정을 가능하게 합니다. 태즈메이니아 대학의 자가 완결형 유닛은 실시간 영양염과 PFAS 모니터링이 용매 사용량을 최대 80% 줄일 수 있음을 보여줍니다. 휴대용 이온 크로마토 그래프의 듀얼 LED 검출기는 여러 분석 대상물을 동시에 분해하여 농업 유출 시험의 턴어라운드를 단축합니다. 보다 빠른 검출기와 2µm 이하의 컬럼은 분해능을 희생하지 않고 처리량을 향상시키고 감가상각 사이클이 끝나면서 실험실이 기존 시스템에서 전환하도록 권장합니다. 장비 제조업체는 IoT 지원 진단 기능을 추가하고 유지보수 시기를 예측하고 다운타임을 단축하며 컬럼 수명을 연장합니다. 이러한 기술 혁신은 특히 PFAS 스크리닝의 새로운 의무화에 대응해야 하는 환경기관들 사이에서 대응 가능한 밑단을 넓히고 있습니다.

의약품 및 바이오의약품의 연구개발 확대 : 생물제제의 복잡성이 고급 분석을 요구

연속 처리 워크플로우에서는 중요한 품질 속성을 관리하기 위해 실시간 데이터가 필요합니다. 시험관 내 전사 중 리보뉴클레오티드 농도를 모니터링하는 앳라인 HPLC 플랫폼은 mRNA 수율을 개선하고 배치 릴리스 시간을 단축합니다. 단클론 항체 및 항체 약물 복합체에 필수적인 번역 후 변형 특성화는 질량 분석과의 통합을 강화함으로써 강화됩니다. 규제 당국이 권장하는 공정 분석 기술의 프레임워크는 이러한 라이브 분석의 채택을 가속화하고 공정 파라미터를 개선하는 선순환 피드백 루프를 생성합니다. 중국과 인도의 생물 제제에 대한 자금 제공은 견고한 분석 플랫폼에 대한 수요를 확대하는 반면, 수탁 제조업체는 저분자 및 생물 제제 파이프라인을 모두 지원하는 다제품 제품군에 투자하고 있습니다. 그 결과 실험실은 보다 높은 점도의 샘플에 대응하고 고압 하에서도 피크 용량을 유지하는 UHPLC 시스템으로 업그레이드를 진행하고 있습니다.

높은 자본 비용과 운영 비용 : 재생 장비 시장이 전략적 선택으로 상승

UHPLC의 패키지 세트는 5만 달러를 초과할 수 있으며, 소모품과 서비스 계약은 매년 15-20%를 늘리는 경우가 많습니다. 예산에 제약이 있는 실험실에서는 성능을 희생하지 않고도 도입 비용을 낮출 수 있는 타사 재생 장치에서 테스트한 인증 중고 시스템을 살펴봅니다. 제조업체는 또한 용매 사용량을 최대 80%까지 줄이고 폐기 요금을 낮추고 펌프 씰의 수명을 연장하는 기공 컬럼의 유로를 재설계하고 있습니다. 에너지 효율적인 냉각 모듈은 열 출력을 줄이고 시설의 HVAC 부하를 줄입니다. 이러한 조치를 종합하면 운전 경비가 줄어들지 만 초기 자본 지출은 소규모 기관의 경우 여전히 장애물입니다.

부문 분석

2025-2030년 CAGR은 소모품이 7.5%로 2024년 고속 액체 크로마토그래피(HPLC) 시장 점유율의 45.1%를 차지했음에도 불구하고 장비 매출을 상회했습니다. 컬럼, 용매 및 바이알의 빈번한 교환은 자본 예산이 급박하더라도 지속적인 현금 흐름을 보장합니다. 퓨즈드 코어 파티클을 사용하는 컬럼은 낮은 배압에서 효율을 높이고 펌프 부담을 줄이고 시스템 수명을 연장합니다. 100% 재활용 가능한 해양 플라스틱과 같은 환경 친화적인 포장은 보존 안정성을 손상시키지 않으면 서 기업의 지속가능성 목표를 충족합니다. 초순수 수요는 이러한 경향을 반영하고 있으며, 2023년 의약품용수 분야 시장 규모는 398억 5,000만 달러로 HPLC 등급 시약의 보충 사이클이 견조하다는 것을 보여주었습니다.

실험실은 일반적으로 브랜드화된 하드웨어 에코시스템을 중심으로 워크플로우를 표준화하기 때문에 고속 액체 크로마토그래피(HPLC) 시장 규모에 있어서 장비는 여전히 매우 중요합니다. 시마즈 제작소의 Nexera 시리즈는 자동 이동상 블렌드, IoT 경고, 실시간 가동률을 정량화하는 분석 대시보드를 통합하고 있습니다. 유체 경로를 최적화하면 질량 분석의 피크 강도를 1.8배에서 3.8배로 높일 수 있으며 검출 한계에 직접 영향을 미칩니다. 따라서 공급업체는 피팅 키트와 레이저 에칭 튜브를 새로운 장비에 번들하여 설치 후에도 성능을 유지할 수 있습니다.

기존 플랫폼이 계속해서 최대 수익을 올리고 있지만 실험실이 런타임을 단축하는 2µm 이하의 컬럼으로 업그레이드함에 따라 UHPLC의 채용이 CAGR 8.9%를 나타낼 전망입니다. 1만 5,000psi 이상의 작동 압력은 그라디언트를 5분 이하로 압축하여 용매 소비량을 최대 70% 줄이면서 처리량을 유지합니다. 하이브리드 시스템은 UHPLC 분리와 비행 시간 검출기 또는 Orbitrap 검출기를 결합하여 단일 주입으로 종합적인 구조 해명을 가능하게 합니다. 마이크로유체 칩 HPLC 프로토타입은 실리콘 기판에 시료 정리와 분리를 통합하여 마이크로리터의 용매량을 사용하면서 벤치탑 장치에 필적하는 성능을 입증합니다.

나노 HPLC는 희귀 샘플을 다루는 단백질체학 팀에 기여하여 샘플 희석 없이 감도를 향상시킵니다. 퓨즈드 코어 파티클 컬럼은 기존의 완전 다공성 파티클과 2µm 이하의 매체의 중간 컬럼으로, 중간 정도의 배압으로 40% 높은 효율을 실현합니다. 이러한 점진적인 개선으로 초고압 펌프가 없는 시설에서도 고속 분리가 가능해졌습니다. 그 결과 중급기용 고속 액체 크로마토그래피(HPLC) 시장 규모가 확대되고, 엔트리 레벨과 플래그십 플랫폼의 갭을 메울 것으로 예측됩니다.

지역 분석

북미는 집중적인 의약품 연구개발, 강력한 바이오프로세스 기반, 고급 분석시험을 의무화하는 엄격한 규제환경에 힘입어 2024년 세계매출의 31.5%를 획득했습니다. 의약품 중 니트로소아민 불순물에 관한 FDA의 2024년 지침은 발암성 화합물을 서브ppm 수준에서 검출할 것을 실험실에 요구했으며, UHPLC-MS의 추가 설치를 촉구했습니다. 미국에 본사를 두는 장비 공급업체는 AI 지원 소프트웨어와 예지 보전 모듈의 초기 상업화를 지배하고 있으며 이 지역의 리더십을 강화하고 있습니다. 휴대용 HPLC 시스템은 환경 모니터링 분야에서도 인기를 끌고 있으며 산업 유출 후 하천 오염물질의 현장 분석을 지원합니다.

아시아태평양은 중국과 인도가 백신, 바이오시밀러 및 저분자 제조 능력을 확대함에 따라 2030년까지 연평균 복합 성장률(CAGR) 6.5%를 나타낼 것으로 예측됩니다. 국제규제조화평의회(ICH) 가이드라인에 대한 현지규제의 조화는 준거한 분석 플랫폼에 대한 투자를 기업에 촉구합니다. HPLC의 진화 150주년을 기념하여 일본 공급업체는 하드웨어 설계 혁신을 계속하고 있습니다. 실험실 근대화를 조성하는 정부 프로그램은 물과 식품의 안전 감시를 임무로 하는 지방 센터의 인수 장벽을 저하시킵니다. 중간층의 건강 관리 지출 증가는 임상 진단 실험실의 고객 기반을 더욱 확대하여 소모품에 대한 꾸준한 풀스루를 생성합니다.

유럽은 성숙하지만 기술 집약적인 수요를 보여줍니다. 유럽의약청(EEA)은 신청서류의 심사를 지연시킬 수 있는 퇴직자 증가에 임하고 있으며, 장비의 검증 스케줄에 간접적인 영향을 미치고 있습니다. 신청 중 PFAS 규정은 600개가 넘는 의약품 제형에 영향을 미칠 수 있으며, 재제제 및 추가 안정성 시험이 필요합니다. 그린 크로마토그래피에 대한 노력이 강하고 인상에 남아 있습니다. 바이오 용매를 사용하면 낮은 환경 부하에서 동등한 분리 성능을 얻을 수 있음이 조사에서 입증되었습니다. 이러한 역학을 종합하면 유럽의 고속 액체 크로마토그래피(HPLC) 시장 규모는 장비의 보급률이 여전히 높은 가운데도 유지되고 있다고 말할 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- HPLC 기술의 진보

- 의약품·바이오의약품의 연구개발 확대

- 음식의 안전과 환경에 대한 규제의 초점

- 임상 진단과 정밀의료의 성장

- 상용 바이오프로세스에서 실시간 PAT의 요구

- AI 대응 예측 및 자기 최적화 HPLC

- 시장 성장 억제요인

- 높은 자본 비용과 운영 비용

- 숙련된 크로마토그래퍼의 부족

- 대체 분리 기술에 의한 대체

- 초고순도 용매와 컬럼공급망 위험

- 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품별

- 기기

- 소모품

- 액세서리

- 기술별

- 기존 HPLC

- UHPLC

- 나노 HPLC

- 마이크로플루이딕스 칩 HPLC

- 용도별

- 의약품 품질 관리

- 임상 연구

- 바이오 의약품 제조

- 식음료 검사

- 환경 분석

- 법의학 및 독성학

- 기타 용도

- 최종 사용자별

- 제약 및 바이오테크놀러지 기업

- CRO 및 CMO

- 학술 및 연구 기관

- 임상 진단 실험실

- 식품 및 환경 시험소

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Waters Corporation

- Agilent Technologies Inc.

- Thermo Fisher Scientific Inc.

- Shimadzu Corporation

- Merck KGaA

- Danaher Corporation(Cytiva)

- Bio-Rad Laboratories Inc.

- PerkinElmer Inc.

- Gilson Inc.

- Mitsubishi Chemical Corporation

- Tosoh Corporation

- Hitachi High-Tech Corporation

- Hamilton Company

- JASCO Inc.

- KNAUER Wissenschaftliche Gerate GmbH

- Phenomenex Inc.

- YMC Co., Ltd.

제7장 시장 기회와 향후 전망

KTH 25.11.12The high-performance liquid chromatography market is valued at USD 5.22 billion in 2025 and is tracking toward USD 6.49 billion by 2030 at a 4.45% CAGR.

Advancing column chemistries, ultra-high-pressure pumps, and automation software are lifting system productivity while lowering solvent use. Wider uptake in pharmaceutical quality control, real-time bioprocess monitoring, and clinical diagnostics is widening the installed base, and new per- and polyfluoroalkyl substance (PFAS) regulations are adding fresh demand in environmental testing. Vendors are also embedding artificial intelligence into instrument control and data processing to shorten method development time, sharpen peak identification, and cut repeat runs. Together, these technologies and compliance forces are deepening replacement cycles and accelerating first-time purchases, especially in Asia Pacific, where rising healthcare spending aligns with local manufacturing incentives.

Global High-Performance Liquid Chromatography (HPLC) Market Trends and Insights

Advancements in HPLC Technologies: Miniaturization Drives Portability Revolution

Compact instruments are moving analyses from centralized labs to field sites, enabling immediate decision-making in remote locations. The University of Tasmania's self-contained units illustrate how real-time nutrient and PFAS monitoring can shrink solvent use by up to 80%. Dual LED detectors in portable ion chromatographs now resolve multiple analytes simultaneously, which shortens turnaround for agricultural runoff testing. Faster detectors and sub-2 µm columns elevate throughput without compromising resolution, encouraging laboratories to switch from traditional systems as depreciation cycles close. Instrument makers are adding IoT-enabled diagnostics that anticipate maintenance windows, reduce downtime, and lengthen column life. These innovations are broadening the addressable base, particularly among environmental agencies that must comply with new PFAS screening mandates.

Pharmaceutical & Biopharma R&D Expansion: Biologics Complexity Demands Advanced Analytics

Continuous processing workflows require real-time data to control critical quality attributes. At-line HPLC platforms monitoring ribonucleotide concentrations during in vitro transcription are improving mRNA yields and shortening batch release times. Deeper integration with mass spectrometry is enhancing characterization of post-translational modifications, essential for monoclonal antibodies and antibody-drug conjugates. Process Analytical Technology frameworks recommended by regulators are accelerating the adoption of these live analytics and creating virtuous feedback loops that refine process parameters. Funding for biologics in China and India is expanding demand for robust analytical platforms, while contract manufacturers invest in multiproduct suites that support both small-molecule and biologic pipelines. As a result, laboratories are upgrading to UHPLC systems that handle higher viscosity samples and maintain peak capacity under elevated pressures.

High Capital & Operating Costs: Refurbished Equipment Market Emerges as Strategic Alternative

A complete UHPLC package can exceed USD 50,000, and consumables plus service contracts often add 15-20% of that figure annually. Budget-constrained laboratories are turning into certified pre-owned systems tested by third-party refurbishes, which lower entry costs without sacrificing performance. Manufacturers are also redesigning flow paths for narrow-bore columns that cut solvent use by up to 80%, lowering disposal fees and extending pump seal life. Energy-efficient cooling modules reduce heat output, easing facility HVAC loads. Collectively, these measures mitigate operational expenditure, yet initial capital outlay remains a hurdle for small institutions.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Focus on Food Safety & Environment: PFAS Regulations Reshape Testing Protocols

- Growth of Clinical Diagnostics & Precision Medicine: Liquid Biopsy Advances Drive HPLC Adoption

- Shortage of Skilled Chromatographers: Industry-Academic Partnerships Address Talent Gap

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Consumables delivered 7.5% CAGR prospects for 2025-2030, surpassing instrument revenue despite instruments owning 45.1% of the high-performance liquid chromatography market share in 2024. Frequent replacement of columns, solvents, and vials ensures recurring cash flow even when capital budgets tighten. Columns with Fused-Core particles boost efficiency at lower back pressures, reducing pump strain and extending system life. Eco-conscious packaging, such as 100% recyclable ocean plastic, meets corporate sustainability goals without compromising shelf stability. Demand for ultrapure water mirrors this trend, with the pharmaceutical water segment's USD 39.85 billion size in 2023 pointing to robust replenishment cycles for HPLC-grade reagents.

Instruments remain pivotal to the high-performance liquid chromatography market size because laboratories typically standardize workflows around branded hardware ecosystems. Shimadzu's Nexera series integrates automatic mobile-phase blending, IoT alerts, and analytics dashboards that quantify utilization rates in real time. Accessories, though smaller in value, are increasingly critical; optimized fluidic paths can raise mass-spectrometric peak intensity between 1.8X and 3.8X, directly affecting detection limits. Suppliers are therefore bundling fitting kits and laser-etched tubing with new instruments to ensure performance is preserved after installation.

Conventional platforms continued to generate the largest revenue pool, yet UHPLC adoption is expanding at 8.9% CAGR as laboratories upgrade to sub-2 µm columns that shorten run times. Operating pressures above 15,000 psi compress gradients into sub-five-minute windows, preserving throughput while slashing solvent consumption by up to 70%. Hybrid systems pair UHPLC separations with time-of-flight or Orbitrap detectors, allowing comprehensive structural elucidation within a single injection. Microfluidic chip-HPLC prototypes integrate sample cleanup and separation on silicon substrates, demonstrating performance comparable to benchtop instruments while using microliter solvent volumes.

Nano-HPLC serves proteomics teams that handle scarce samples, providing heightened sensitivity without sample dilution. Fused-Core particle columns offer a midpoint between traditional fully porous particles and sub-2 µm media, delivering 40% higher efficiency at moderate backpressure. These incremental improvements democratize high-speed separations for facilities lacking ultra-high-pressure pumps. As a result, the high-performance liquid chromatography market size for mid-tier instruments is expected to widen, bridging the gap between entry-level and flagship platforms.

The High-Performance Liquid Chromatography Market is Segmented by Product Type (Instruments, Consumables, and More), Technology (Conventional HPLC, UHPLC, and More), Application (Pharmaceutical Quality-Control, Clinical Research, and Others), by End User (Pharmaceutical & Biotechnology Companies, and More), and Geography (North America, Europe, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 31.5% of global revenue in 2024 supported by intensive pharmaceutical R&D, strong bioprocessing infrastructure, and a stringent regulatory environment that mandates advanced analytical testing. The FDA's 2024 guidance on nitrosamine impurities in drug products now requires laboratories to detect carcinogenic compounds at sub-ppm levels, driving additional UHPLC-MS installations. Instrument vendors headquartered in the United States dominate early commercialization of AI-enabled software and predictive maintenance modules, reinforcing regional leadership. Portable HPLC systems are also gaining traction in environmental monitoring, supporting onsite analysis of river contaminants after industrial spills.

Asia Pacific is forecast to grow at 6.5% CAGR to 2030 as China and India expand vaccine, biosimilar, and small-molecule manufacturing capacity. Local regulatory harmonization with International Council for Harmonization (ICH) guidelines pushes companies to invest in compliant analytical platforms. Japanese suppliers continue to innovate hardware designs celebrating 150 years of HPLC evolution. Government programs that subsidize laboratory modernization lower acquisition barriers for provincial centers tasked with water and food safety oversight. Rising middle-class healthcare spending further widens the customer base for clinical diagnostic laboratories, creating steady pull-through for consumables.

Europe shows mature but technology-intensive demand. The European Medicines Agency is grappling with looming retirements that could slow dossier reviews, indirectly influencing instrument validation timelines. Pending PFAS restrictions may affect formulations of more than 600 medicines, requiring reformulation and additional stability testing. Green chromatography initiatives resonate strongly; research demonstrates that bio-based solvents can achieve equivalent separation performance with lower environmental footprints. Collectively, these dynamics sustain the high-performance liquid chromatography market size in Europe even as overall instrument penetration remains high.

- Waters Corporation

- Agilent Technologies

- Thermo Fisher Scientific

- Shimadzu

- Merck

- Danaher

- Bio-Rad Laboratories

- PerkinElmer

- Gilson

- Mitsubishi Chemical

- Tosoh

- Hitachi

- Hamilton Company

- JASCO Inc.

- KNAUER Wissenschaftliche Gerate GmbH

- Phenomenex Inc.

- YMC Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advancements in HPLC technologies

- 4.2.2 Pharmaceutical & biopharma R&D expansion

- 4.2.3 Regulatory focus on food-safety & environment

- 4.2.4 Growth of clinical diagnostics & precision-medicine

- 4.2.5 Real-time PAT needs in continuous bioprocessing

- 4.2.6 AI-enabled predictive & self-optimising HPLC

- 4.3 Market Restraints

- 4.3.1 High capital & operating costs

- 4.3.2 Shortage of skilled chromatographers

- 4.3.3 Substitution by alternate separation techniques

- 4.3.4 Supply-chain risk for ultrapure solvents & columns

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Instruments

- 5.1.2 Consumables

- 5.1.3 Accessories

- 5.2 By Technology

- 5.2.1 Conventional HPLC

- 5.2.2 UHPLC

- 5.2.3 Nano-HPLC

- 5.2.4 Microfluidic-chip HPLC

- 5.3 By Application

- 5.3.1 Pharmaceutical Quality-Control

- 5.3.2 Clinical Research

- 5.3.3 Biopharmaceutical Manufacturing

- 5.3.4 Food & Beverage Testing

- 5.3.5 Environmental Analysis

- 5.3.6 Forensic & Toxicology

- 5.3.7 Other Applications

- 5.4 By End-User

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 CROs & CMOs

- 5.4.3 Academic & Research Institutes

- 5.4.4 Clinical Diagnostic Laboratories

- 5.4.5 Food & Environmental Testing Labs

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Waters Corporation

- 6.3.2 Agilent Technologies Inc.

- 6.3.3 Thermo Fisher Scientific Inc.

- 6.3.4 Shimadzu Corporation

- 6.3.5 Merck KGaA

- 6.3.6 Danaher Corporation (Cytiva)

- 6.3.7 Bio-Rad Laboratories Inc.

- 6.3.8 PerkinElmer Inc.

- 6.3.9 Gilson Inc.

- 6.3.10 Mitsubishi Chemical Corporation

- 6.3.11 Tosoh Corporation

- 6.3.12 Hitachi High-Tech Corporation

- 6.3.13 Hamilton Company

- 6.3.14 JASCO Inc.

- 6.3.15 KNAUER Wissenschaftliche Gerate GmbH

- 6.3.16 Phenomenex Inc.

- 6.3.17 YMC Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment