|

시장보고서

상품코드

1851203

의료용 영상 워크스테이션 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Medical Imaging Workstations - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

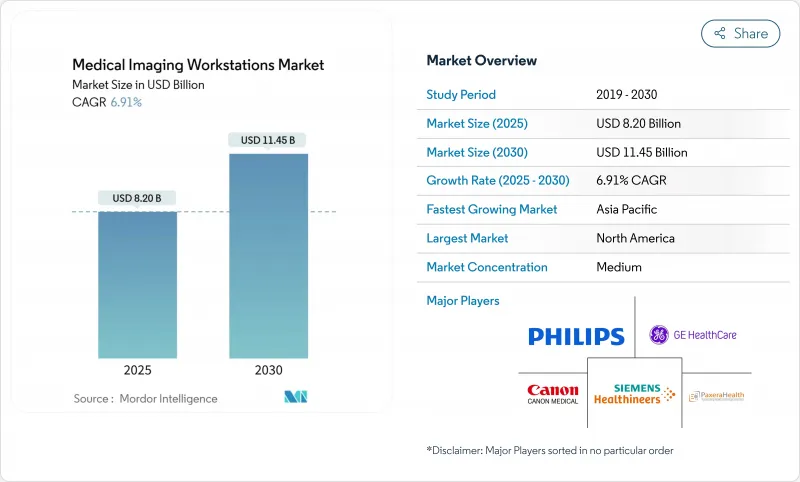

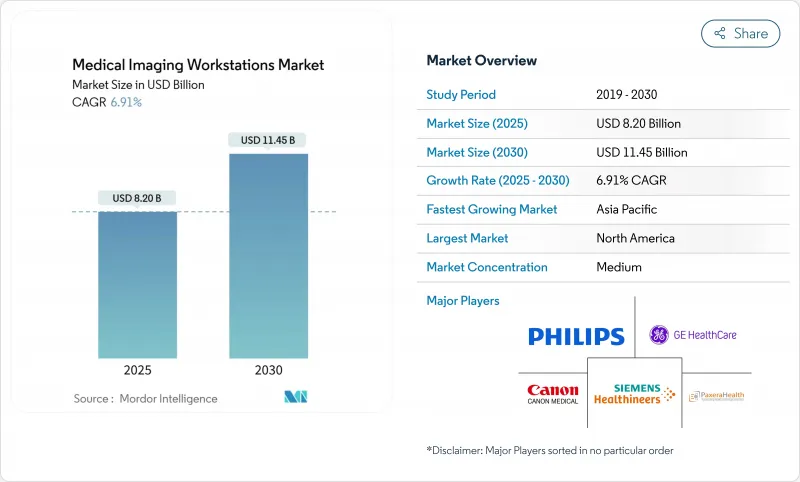

의료용 영상 워크스테이션 시장 규모는 2025년에 82억 달러로 추정되고, 예측 기간(2025-2030년)의 CAGR은 6.91%로, 2030년에는 114억 5,000만 달러에 달할 것으로 예상됩니다.

교체 사이클 가속화, 기업용 이미지 아카이브 마이그레이션, 멀티모더리티 기술의 복잡화 등이 고급 가시화 플랫폼에 대한 수요를 끌어올리고 있습니다. FDA에 의한 컴퓨터 지원 감지 소프트웨어의 클래스 II로의 재분류와 같은 규제의 명확화는 기술 혁신의 리드타임을 단축하고 진입 장벽을 저하시킵니다. 공급업체는 현재 AI를 지원하는 설계와 On-Premise 하드웨어 비용을 줄이는 클라우드 호스팅 제공 모델을 선호하고 있으며, 이 접근법은 병원 노동 부족 대응에도 도움이 됩니다. 북미는 조기 AI 도입과 성숙한 상환경로에 의해 우위를 유지하고 있지만, 아시아태평양은 대규모 디지털화 프로젝트를 배경으로 가장 빠른 이용 확대를 기록하고 있습니다. 반면에 반도체 공급 제약은 GPU의 가용성을 낮추고 하이 엔드 구성의 리드 타임을 연장하고 일부 구매자는 씬 클라이언트를 대체해야합니다.

세계의 의료용 영상 워크스테이션 시장 동향 및 인사이트

이미지 양식의 급속한 기술 진화

광자 카운팅 CT, 전신 MRI 스크리닝, 옥수수 빔 유방 CT, 자율 초음파는 워크스테이션의 업데이트 주기마다 계산 상한을 올리고 있습니다. 포톤 카운팅 스캐너는 방사선 피폭을 80%나 줄이면서 원시 데이터 양을 4배로 증가시켜 실시간 3D 재구성을 지원하는 GPU를 요구하고 있습니다. GE Healthcare와 NVIDIA의 협업은 공급업체가 AI 추론을 이미지 획득 계층에 통합하는 방법을 보여줍니다. Prenuvo의 AI 지원 전신 MRI 플랫폼은 다장기 분석으로의 이동을 강화하고, 더 높은 처리량, 더 큰 캐시, 멀티 모니터 인체공학을 갖춘 워크스테이션 설계를 공급업체에게 다가가고 있습니다.

신흥 시장에서 영상처리 건수 증가

아시아태평양의 CT 및 MRI의 지속적인 도입 프로그램으로 시각화 업그레이드에 대한 후속 수요가 발생했습니다. 인구동태의 고령화에 의해 특히 고도의 후처리에 의존하는 종양이나 심장의 영상에 있어서, 1인당의 스캔율이 상승. 캐논 메디컬의 인도 전략은 중소득 국가에 대한 제조업체의 광범위한 축 다리를 보여 주며, 보건부는 하드웨어 업데이트 사이클과 병행하여 이미지 아카이브 배포에 자금을 제공합니다. 에티오피아에서는 Teleradiology를 도입한 후 환자의 대기 시간이 71% 단축되었기 때문에 씬 클라이언트 워크스테이션이 원격지의 병원과 부족한 방사선과 의사를 어떻게 연결시키는가가 밝혀졌습니다. 따라서 확장 가능한 클라우드 액세스는 현장 IT 팀이 부족한 시설의 중심 구매 기준이 됩니다.

비싼 워크스테이션의 초기 비용과 수명 주기 비용

자본 예산은 여전히 지원 인프라보다 환자를 직접 관리하는 장비를 선호합니다. 총소유비용은 수년간의 서비스 계약 및 소프트웨어 업데이트를 포함하면 초기 가격의 두 배가 되는 경우가 많습니다. 소규모 시설에서는 공인된 정비 하드웨어에 눈을 돌리지만, 이러한 발굴물에는 최신 GPU가 탑재되어 있지 않은 경우가 많아 AI의 성능이 저하됩니다. 구독 소프트웨어는 자본 상승을 평준화할 수 있지만, 7년간의 누적 요금은 영구 라이선스를 초과할 수 있습니다. 방사선 치료에서 진료 보수의 감소는 재무적 조사를 확대하고 조달주기를 연장합니다.

부문 분석

시각화 소프트웨어가 2024년 매출의 57.83%를 차지했으며 맞춤형 하드웨어가 아닌 코드에 기능이 집계되어 있음을 보여주었습니다. 이러한 이점은 공급업체가 알고리즘 라이선스를 디스플레이 구매와 분리하여 신속한 무선 업데이트를 가능하게 함으로써 확대됩니다. 구독의 AI 세분화 플러그인은 지속적인 수익원을 창출하고 기능 리드 타임을 단축합니다. 한편, 디스플레이 유닛은 4K 및 8K 해상도가 미세 석회화 및 폐 결절 검토에서 진단 불확실성을 감소시키기 때문에 CAGR 로 가장 빠른 7.85%를 나타낼 전망입니다. EIZO의 RadiForce RX670은 600만 화소 해상도와 USB-C 도킹을 통해 케이블 산란을 최소화하는 인체공학적 이점을 갖추고 있습니다.

구성 요소의 수렴도 조달 지침입니다. 씬 클라이언트 셋업은 로컬 GPU에서 중앙 처리 노드로 가치를 이동시키고 자동 교정과 편안한 조명 기능은 디스플레이의 ASP를 높입니다. 더 많은 시설이 원격 독서를 목표로 하는 동안 병원 정보 시스템에 통합된 제로 실적 뷰어는 독점 그래픽 카드에 대한 마지막 의존성을 제거합니다. 그 결과, 의료용 영상 워크스테이션 시장에서 차지하는 소프트웨어의 비율은 어떤 하드웨어 품목보다 빠르게 성장할 것으로 보입니다.

컴퓨터 단층촬영 워크스테이션은 다장기 유틸리티와 포톤 카운팅 업그레이드를 배경으로 2024년 매출의 30.73%를 차지했습니다. 이 분야는 단일 CT 뷰어로 외상, 종양, 심장의 경우에 대응할 수 있기 때문에 기업 표준화의 혜택을 누리고 있습니다. 그러나 유방 촬영 플랫폼은 국가 검진 프로그램이 확대되고 3D 토모 신시시스가 보편화됨에 따라 CAGR 로 가장 빠른 8.13%를 나타낼 전망입니다. 옥수수 빔 유방 CT는 유방 압박을 없애므로 데이터 부하가 더욱 증가하고 워크스테이션 업데이트 투자가 정당화됩니다.

MRI 워크스테이션은 설치장소의 제약을 완화하는 헬륨 프리 자석의 출시로 기세를 늘립니다. 지금까지 하드웨어 콘솔에 설치된 초음파 검사는 원시 시네 루프에서 자동 측정을 추출하는 클라우드 기반 사후 처리를 활용합니다. 핵의학 워크스테이션의 기술 혁신은 디지털 검출기에 달려 있으며, 리콘 시간을 단축하고 선량을 줄이는 동시에 전신 PET 촬영을 가능하게 합니다.

지역 분석

북미는 미국과 캐나다의 의료기관이 AI 트리어지 툴과 자율적 이미지 수집의 조기 도입자이기 때문에 2024년 매출의 37.81%를 차지했습니다. 이 지역은 고급 절차를 상환하는 CPT 코드가 명확하게 정의되어 있기 때문에 병원은 워크스테이션에 대한 투자를 신속하게 회수할 수 있다는 장점이 있습니다. 성숙한 공급업체 생태계는 혁신 주기를 가속화하고 300개 이상의 FDA 인증 AI 알고리즘을 이미 통합할 수 있습니다.

아시아태평양은 현재 진행 중인 병원 건설, 정부 클라우드 헬스 프로그램, 급속한 고령화에 견인되어 CAGR 8.33%를 나타낼 전망입니다. 중국은 현립 병원과 3차 센터를 연결하는 지역의 원격 영상 진단 허브의 규모를 계속 확대하고 있으며, 인도의 아유슈만 발라트 계획은 2차 도시에서의 진단량을 증가시키고 있습니다. 많은 새로운 시설은 레거시 PACS를 피하고, 첫날부터 클라우드 네이티브 아카이브를 도입하고, 현지 IT 직원을 최소화하는 씬 클라이언트 아키텍처를 선호합니다.

유럽에서는 European Health Data Space 이니셔티브가 국경을 넘어 이미지 교환을 장려하고 병원을 상호 운용 가능한 뷰어로 유도하고 꾸준한 확대를 보이고 있습니다. 독일과 프랑스에서는 유방검진의 전국적인 확대가 3D 유방촬영 워크스테이션의 채용을 촉진하고 영국 NHS의 근대화 자금은 AI 지원 CT 폐검진의 시험 운용을 지원하고 있습니다. 중동 및 아프리카에서는 관민 파트너십이 주요 영상 진단센터에 자금을 공급하고 있지만 정치적 변동이나 환율 변동으로 인해 조달이 지연될 수 있습니다. 라틴아메리카에서는 지역 무역 협정에 따라 진단 하드웨어 수입 관세가 낮아지고 견인력이 증가하고 있지만 광대역 보급률이 안정적이지 않아 농촌 지역에서 씬 클라이언트 도입에 한계가 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 이미지 모달리티의 급속한 기술 진화

- 신흥 시장에서의 영상 건수 증가

- 의료비의 증대와 질병 부담 증가

- 가속하는 헬스케어의 디지털화-기업용 PACS/VNA의 이행

- 신흥 경제국 병원 및 진단센터 인프라의 지속적인 혁신

- SaaS 시각화 플러그인을 가능하게 하는 벤더 중립 API 에코시스템

- 시장 성장 억제요인

- 프리미엄 워크스테이션의 높은 초기 비용과 라이프 사이클 비용

- 방사선과 의사/고도 시각화 전문의의 부족

- 제로 트러스트 사이버 보안과 HIPAA 컴플라이언스 비용 증가

- GPU 주조 능력의 제약과 공급망 쇼크

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 구성 요소별

- 시각화 소프트웨어

- 디스플레이 장치

- 기타

- 모달리티별

- 컴퓨터 단층 촬영(CT)

- 자기 공명 영상(MRI)

- 초음파

- 유방촬영술

- 기타

- 사용 모드별

- 두꺼운 클라이언트 워크스테이션

- 얇은 클라이언트/웹 스트리밍 워크스테이션

- 최종 사용자별

- 병원

- 진단 영상 센터

- 전문 클리닉

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- GE HealthCare

- Siemens Healthineers AG

- Canon Medical Systems Corporation

- Koninklijke Philips NV

- Hologic Inc.

- Carestream Health

- Sectra AB

- PaxeraHealth

- Agfa HealthCare

- Barco NV

- Fujifilm Healthcare

- Esaote SpA

- Intelerad Medical

- Aycan Medical

- EIZO Corp.

- Viztek

- eRAD Inc.

제7장 시장 기회와 향후 전망

KTH 25.11.12The Medical Imaging Workstations Market size is estimated at USD 8.20 billion in 2025, and is expected to reach USD 11.45 billion by 2030, at a CAGR of 6.91% during the forecast period (2025-2030).

Faster replacement cycles, enterprise picture-archiving migrations, and rising multi-modality procedure complexity collectively lift demand for advanced visualization platforms. Regulatory clarity, such as the FDA's re-classification of computer-assisted detection software into Class II, has shortened innovation lead times and lowered entry barriers. Vendors now prioritize AI-ready designs and cloud-hosted delivery models that cut on-premises hardware costs, an approach that also helps hospitals cope with workforce shortages. North America keeps a performance edge through early AI adoption and mature reimbursement pathways, yet Asia Pacific records the fastest usage expansion on the back of large-scale digitization projects. Meanwhile, semiconductor supply constraints continue to throttle GPU availability, stretching lead times for high-end configurations and forcing some buyers toward thin-client alternatives.

Global Medical Imaging Workstations Market Trends and Insights

Rapid technological evolution in imaging modalities

Photon-counting CT, whole-body MRI screening, cone-beam breast CT, and autonomous ultrasound together raise the computational ceiling for every workstation refresh cycle. Photon-counting scanners cut radiation exposure by as much as 80% while quadrupling raw data volume, demanding GPUs that support real-time 3-D reconstructions. GE HealthCare and NVIDIA's collaboration shows how vendors are embedding AI inference at the image-acquisition layer, which in turn obliges workstation software to orchestrate automated segmentation, triage, and quality control. Prenuvo's AI-enabled whole-body MRI platform reinforces the shift toward multi-organ analysis, compelling vendors to design workstations with higher throughput, larger cache, and multi-monitor ergonomics.

Growing imaging procedure volumes in emerging markets

Continual CT and MRI installation programs across Asia Pacific generate follow-on demand for visualization upgrades. Demographic aging lifts per-capita scan rates, particularly for oncology and cardiac imaging, which rely on sophisticated post-processing. Canon Medical's India strategy signals manufacturers' broader pivot to mid-income countries whose health ministries are funding picture-archiving rollouts alongside hardware refresh cycles. Ethiopia's 71% reduction in patient waiting time after teleradiology deployment underscores how thin-client workstations connect remote hospitals to scarce radiologists. Scalable cloud access therefore becomes a core purchasing criterion for facilities that lack on-site IT teams.

High upfront and lifecycle costs of premium workstations

Capital budgets still favor direct patient-care devices over support infrastructure. Total cost of ownership often doubles initial price once multiyear service contracts and software renewals are included. Smaller facilities look at certified refurbished hardware, yet those bargains often lack modern GPUs, throttling AI performance. Subscription software can smooth out capital spikes; however, cumulative fees sometimes exceed perpetual licenses over a seven-year horizon. Reimbursement erosion in radiology magnifies financial scrutiny, stretching procurement cycles.

Other drivers and restraints analyzed in the detailed report include:

- Rising healthcare expenditure coupled with disease burden

- Accelerated healthcare digitization-enterprise PACS/VNA migrations

- Shortage of radiologists / advanced visualization specialists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Visualization software generated 57.83% of 2024 revenue, illustrating how functionality now sits in code rather than bespoke hardware. That dominance will widen as vendors decouple algorithm licenses from display purchases, allowing rapid over-the-air updates. Subscription AI-segmentation plug-ins create recurring revenue streams and shorten feature lead times. Display units, in contrast, post the fastest 7.85% CAGR because 4 K and 8 K resolutions reduce diagnostic uncertainty in microcalcification and lung-nodule review. EIZO's RadiForce RX670 with six-megapixel resolution and USB-C docking typifies ergonomic gains that minimize cable clutter.

Component convergence also guides procurement: thin-client setups shift value from local GPUs into centralized processing nodes, while auto-calibration and comfort-lighting features lift display ASPs. As more facilities aim for remote reading, zero-footprint viewers embedded in the hospital information system remove the last dependency on proprietary graphics cards. Consequently, software's proportion of the medical imaging workstations market will continue to grow more rapidly than any hardware line item.

Computed tomography workstations controlled 30.73% of 2024 revenue on the back of multi-organ utility and photon-counting upgrades. The segment benefits from enterprise standardization, as a single CT viewer can serve trauma, oncology, and cardiac cases. Mammography platforms, however, register the fastest 8.13% CAGR as national screening programs expand and 3-D tomosynthesis becomes common. Cone-beam breast CT's elimination of breast compression will further raise data loads and justify workstation refresh investments.

MRI workstations gain momentum from helium-free magnet launches that ease siting constraints. Ultrasound, historically attached to hardware consoles, now leverages cloud-based post-processing that extracts automated measurements from raw cine loops. Nuclear-medicine workstation innovation hinges on digital detectors, which reduce recon time and cut dose while enabling total-body PET acquisitions.

The Medical Imaging Workstations Market Report is Segmented by Component (Visualization Software, Display Units, and Others), Modality (Computed Tomography (CT), Magnetic Resonance Imaging (MRI), and More), Usage Mode (Thick-Client Workstations, Thin-Client / Web-Streaming Workstations), End User (Hospitals, and More), and Geography (North America, Europe and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 37.81% of 2024 revenue as U.S. and Canadian providers remained early adopters of AI triage tools and autonomous image acquisition. The region benefits from well-defined CPT codes that reimburse advanced procedures, allowing hospitals to recoup workstation investments quickly. A mature vendor ecosystem accelerates innovation cycles, with 300+ FDA-cleared AI algorithms already available for integration.

Asia Pacific recorded an 8.33% CAGR outlook driven by ongoing hospital build-outs, government cloud-health programs, and rapidly aging populations. China continues to scale provincial teleradiology hubs that connect county hospitals to tertiary centers, while India's Ayushman Bharat scheme boosts diagnostic volumes in secondary cities. Many new facilities bypass legacy PACS and deploy cloud-native archives from day one, favoring thin-client architectures that minimize local IT staffing.

Europe shows steady expansion as the European Health Data Space initiative encourages cross-border image exchange, nudging hospitals toward interoperable viewers. National breast-screening extensions in Germany and France stimulate adoption of 3-D mammography workstations, while UK NHS modernization funds support AI-assisted CT lung-screening pilots. In the Middle East and Africa, public-private partnerships fund flagship imaging centers, yet political volatility and exchange-rate swings can delay procurement. Latin America gains traction through regional trade agreements that cut import duties on diagnostic hardware, though inconsistent broadband coverage limits thin-client rollouts in rural sites.

- GE Healthcare

- Siemens Healthineers

- Canon

- Koninklijke Philips

- Hologic

- Carestream Health

- Sectra

- PaxeraHealth

- Agfa HealthCare

- Barco NV

- FUJIFILM

- Esaote

- Intelerad Medical

- Aycan Medical

- EIZO Corp.

- Viztek

- eRAD Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid technological evolution in imaging modalities

- 4.2.2 Growing imaging procedure volumes in emerging markets

- 4.2.3 Rising healthcare expenditure coupled with rising disease burden

- 4.2.4 Accelerated healthcare digitization-enterprise PACS/VNA migrations

- 4.2.5 Ongoing innovations in hospital and diagnostic center infrastructure in emegring economies

- 4.2.6 Vendor-neutral API ecosystems enabling SaaS visualization plug-ins

- 4.3 Market Restraints

- 4.3.1 High upfront & lifecycle costs of premium workstations

- 4.3.2 Shortage of radiologists / advanced visualization specialists

- 4.3.3 Escalating zero-trust cybersecurity & HIPAA compliance expenses

- 4.3.4 GPU foundry capacity constraints & supply-chain shocks

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Visualization Software

- 5.1.2 Display Units

- 5.1.3 Others

- 5.2 By Modality

- 5.2.1 Computed Tomography (CT)

- 5.2.2 Magnetic Resonance Imaging (MRI)

- 5.2.3 Ultrasound

- 5.2.4 Mammography

- 5.2.5 Others

- 5.3 By Usage Mode

- 5.3.1 Thick-Client Workstations

- 5.3.2 Thin-Client / Web-Streaming Workstations

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Diagnostic Imaging Centers

- 5.4.3 Specialty Clinics

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 GE HealthCare

- 6.3.2 Siemens Healthineers AG

- 6.3.3 Canon Medical Systems Corporation

- 6.3.4 Koninklijke Philips N.V.

- 6.3.5 Hologic Inc.

- 6.3.6 Carestream Health

- 6.3.7 Sectra AB

- 6.3.8 PaxeraHealth

- 6.3.9 Agfa HealthCare

- 6.3.10 Barco NV

- 6.3.11 Fujifilm Healthcare

- 6.3.12 Esaote SpA

- 6.3.13 Intelerad Medical

- 6.3.14 Aycan Medical

- 6.3.15 EIZO Corp.

- 6.3.16 Viztek

- 6.3.17 eRAD Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment