|

시장보고서

상품코드

1851204

로봇 내시경 기기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Robotic Endoscopy Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

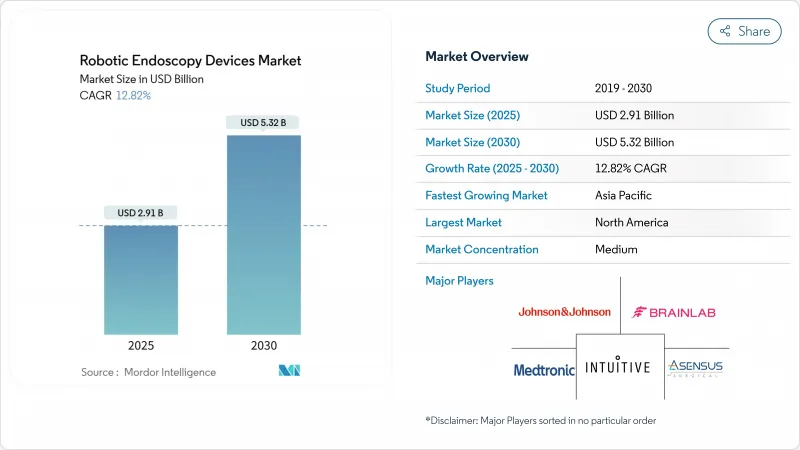

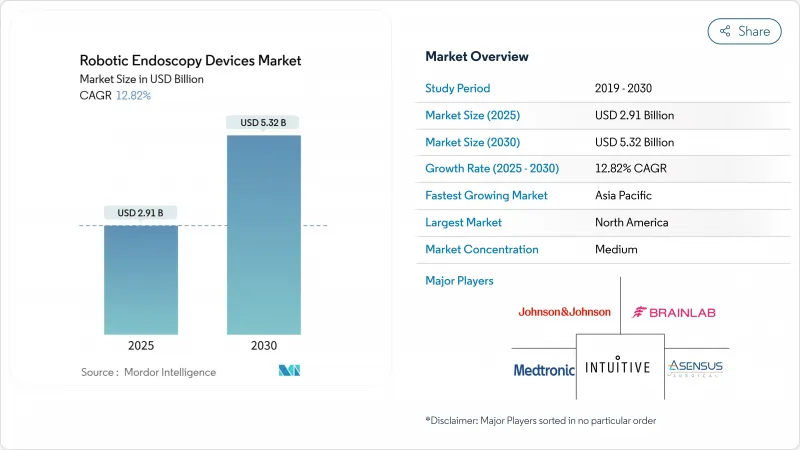

로봇 내시경 기기 시장은 2025년에 29억 1,000만 달러에 이르고, 2030년에는 53억 2,000만 달러에 달할 것으로 예측됩니다.

저침습 수술의 채용 확대, 화상 처리와 내비게이션에의 인공지능의 급속한 통합, 원내 감염률 억제의 필요성 등이 수요를 뒷받침하고 있습니다. 또한 의료시스템은 로봇기술을 입원기간 단축과 총수술비용 절감을 위한 루트로 간주하여 설비투자에 유리한 경제성을 창출하고 있습니다. 특허 절벽이 핵심 기술을 민주화하고 있으며, 모듈형, 저비용 플랫폼이 시장에 등장함에 따라 경쟁의 치열성이 커지고 있습니다. 한편, 일회용 스코프가 교차 오염의 위험을 배제한다는 것이 입증되고 있으며, 외래 환자에 대한 가치 제안이 강화되고 있습니다. 이러한 요인들이 결합되어 로봇 내시경 기기 시장은 향후 10년간 2자리 성장을 유지할 것으로 보입니다.

세계의 로봇 내시경 기기 시장 동향과 인사이트

낮은 침습 로봇 수술의 급속한 보급

임상 증거에 따르면 로봇 지원 수술은 기존 기술에 비해 합병증 발생률을 50% 줄이고 회복 시간을 40% 단축했습니다. 병원은 밸류 베이스 케어의 의무화에 대응하기 위해 이러한 성과를 우선하는 경향이 강해지고 있으며, 플랫폼의 도입 확대와 수법 메뉴의 확충으로 이어지고 있습니다. 인테이티브 서지컬사의 2025년 1분기 수술건수는 17% 증가하여 세계적인 기세를 보이고 있습니다. 향상된 3D 비전, 떨림 필터링 및 인체공학을 기반으로 하는 콘솔은 외과 의사의 피로를 줄여 외래에서 더 길고 복잡한 사례를 가능하게 합니다. 이러한 장점을 종합하면 대상 환자층이 확대되고 로봇 내시경 기기 시장의 경제적 매력이 강화됩니다.

AI를 활용한 내비게이션과 이미징이 진단 수율을 높입니다.

딥러닝 모델을 통해 로봇 기관지경 검사의 진단 수율은 기존의 67.8%를 크게 상회하는 85% 이상이 되었습니다. 존슨 엔드 존슨의 MONARCH QUEST 플랫폼은 260% 향상된 컴퓨팅 능력과 AI 주도 경로 계획을 통합하여 병변 타겟팅을 실시간으로 개선합니다. 올림푸스 CADDIE와 같은 클라우드 기반 시스템은 결장 스크리닝에도 비슷한 이점을 제공하며 AI는 추가 처리 시간 없이 선종의 검출을 향상시킵니다. 더 높은 정확도는 재수술을 줄이고 치료 의사 결정을 가속화하며 플랫폼 소유자에게 명확한 경쟁력을 부여합니다.

로봇 플랫폼의 높은 자본 비용과 절차별 비용

시스템의 정가는 150만 달러에서 250만 달러이며, 연간 서비스 요금은 10만 달러 이상이기 때문에 소규모 시설의 경우 장애물이 높습니다. 비교 연구에 따르면 살서제 탈장의 로봇 수술은 2,810유로(3,242.01달러)에 비해 복강경 수술은 726유로(837.62달러)가 걸렸습니다. CMR Surgical과 같은 신규 진출기업들은 레거시 시스템보다 낮은 가격의 모듈식 아키텍처에서 이 격차를 노리고 있지만, 저소득 지역에서는 예산의 제약이 확산되고 있으며, 여전히 보급이 억제되고 있습니다.

부문 분석

치료용 로봇 내시경은 2024년 로봇 내시경 기기 시장의 55.52%를 차지하고 진단 및 개입을 한 번에 수행하는 시스템에 대한 의료 제공업체 수요를 뒷받침했습니다. 주요 제품은 내시경 점막 하층 박리술과 자연 개구 경관 수술과 같은 복잡한 조작을 수행하여 환자와 지불자 모두에게 호소하는 흉터없는 결과를 가능하게합니다. 존슨 엔드 존슨의 MONARCH 플랫폼은 이러한 프리미엄 포지셔닝을 보여주며 EndoQuest는 위장관 치료를 위한 유연한 단일 포트 개념을 추구하고 있습니다. AI를 활용한 가시화에 의해 암의 조기 발견이 가능하게 되어, 진단 기기의 매출은 CAGR 15.25%를 나타낼 전망입니다. 캡슐 시스템과 하이브리드 이미지 프로세싱 로봇이 액세스를 확장하고 하나의 콘솔이 모든 관리 경로를 관리하는 미래의 수렴을 제안합니다. 치료 시스템의 로봇 내시경 기기 시장 규모는 꾸준히 확대될 것으로 예상되지만, 예방 의료가 정책적으로 우선적으로 됨에 따라 진단 혁신이 뛰어납니다.

진단 플랫폼 시장 규모는 여전히 작지만 투자자들은 무선 캡슐 로봇과 치료 시간을 단축하는 클라우드 대응 분석에 자금을 투자하고 있습니다. 삼키는 펌프 제트 카메라와 같은 초기 단계의 프로젝트는 소화관 스크리닝의 범위를 확장하고 특히 완전한 실험실이 부족한 지역에서는 효과적입니다. 이러한 장비가 규제 당국의 허가를 받을수록 진단 솔루션의 로봇 내시경 기기 시장 점유율이 상승하고 동업자의 치료 장비와의 수익 격차가 줄어들 것으로 예측됩니다.

지역별 분석

북미는 2024년 매출의 38.82%를 차지하며, 메디케어 지불 명확화와 성숙한 외과의사의 인재 수영장에 지지되었습니다. 미국의 플래그십 센터에서는 차세대 콘솔이 허가 후 몇 개월에 도입되는 경우가 많으며 업그레이드 사이클이 견고합니다. 캐나다도 비슷한 패턴을 취하고 있으며, 멕시코의 민간 병원은 의료 관광객에게 첨단 시설 도입을 위한 자금을 공급하고 있습니다.

유럽 점유율은 크지 만 규제의 역풍과 일회용 플라스틱에 대한 녹색 정책 모니터링에 직면하고 있습니다. 독일, 프랑스, 영국이 압도적인 설치 대수를 자랑하고 있지만, 의료기기 규제 하에서 여러 해에 걸친 적합성 평가가 신규 참가 기업 시장 진입을 늦추고 있습니다. 북유럽의 의료 시스템은 로봇에 의한 탈장 수리의 이점을 조사하고 있지만 비용 효과에 대한 의문이 남아 급속한 스케일 업을 억제하고 있습니다.

아시아태평양의 CAGR은 13.62%를 나타낼 전망입니다. 중국은 구미의 동업 타사에 비해 30%-40%의 할인 가격으로 콘솔을 제공하는 국내 챔피언을 통해 기세를 유지하고, 제3차 병원 전체 채용에 박차를 가하고 있습니다. 일본은 독자적인 플랫폼과 5G 대응 원격 수술의 데모를 개척해, 한국은 국가의 암 검진 프로토콜로 로봇 공학을 중시하고 있습니다. 신흥 ASEAN 국가와 인도의 민간 체인은 로보틱스를 인바운드 의료 관광의 차별화 요인으로 파악하고 적극적인 투자를 하고 있습니다. 결과적으로 아시아태평양의 로봇 내시경 기기 시장 규모는 전망 기간이 끝날 때 유럽을 추월할 것으로 예측됩니다.

중동 및 아프리카는 기함 병원 건설에 로봇 공학을 포함한 걸프 협력 회의 프로젝트에 견인되어 초기이지만 유망한 섭취를 기록하고 있습니다. 사하라 이남에서는 남아프리카가 선진을 끊는다. 라틴아메리카에서는 브라질과 칠레에서 꾸준한 도입이 보이지만, 환율 변동이 보급을 억제하고 있습니다. 이 지역에서는 공급업체 금융과 절차를 기반으로 리스 모델이 수요 증가를 이끌어내는 데 중요합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 저침습 로봇 수술의 급속한 보급

- 노년 인구, 비만 인구, 당뇨병 인구 증가

- 로봇 소화기·폐 인터벤션에 대한 유리한 상환금

- AI를 활용한 내비게이션과 이미징이 진단 수율 증대

- 외래 전용 로봇 기관지경 검사실의 급증

- 감염증 억제를 위한 단회 사용 로봇 내시경 수요

- 시장 성장 억제요인

- 로봇 플랫폼의 높은 자본 비용과 1기술당 비용

- 환자 안전을 위한 엄격한 규제 승인

- 로봇 내시경 훈련을 받은 외과의 부족

- 일회용 로봇 스코프에 대한 지속가능성의 추진

- 기술의 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품별

- 진단용 로봇 내시경

- 캡슐 로봇

- 영상/시각화 로봇

- 치료용 로봇 내시경

- 수술용 내시경 플랫폼

- 로봇 기관지경

- 복강경 및 경관로 로봇

- 진단용 로봇 내시경

- 용도별

- 복강경 검사

- 기관지경 검사

- 대장 내시경 검사

- 기타 용도

- 최종 사용자별

- 병원

- 외래 수술 센터(ASC)

- 전문 클리닉

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Intuitive Surgical Inc.

- Johnson & Johnson(Auris Health)

- Medtronic PLC

- Olympus Corporation

- Asensus Surgical Inc.

- CMR Surgical Ltd

- Medrobotics Corporation

- Brainlab AG

- Avatera Medical GmbH

- AKTORmed GmbH

- Virtuoso Surgical

- Noah Medical

- EndoQuest Robotics

- Microbot Medical

- Titan Medical

- Fujifilm Holdings Corp.

- SHINVA Medical

- Apollo Endosurgery

- Stryker Corp.

- Karl Storz SE

제7장 시장 기회와 향후 전망

KTH 25.11.12The robotic endoscopy devices market reached USD 2.91 billion in 2025 and is forecast to climb to USD 5.32 billion by 2030, reflecting a sturdy 12.82% CAGR over the period.

Growing adoption of minimally invasive surgery, rapid integration of artificial intelligence into imaging and navigation, and the need to curb hospital-acquired infection rates collectively propel demand. Health systems also view robotic technology as a route to shorten hospital stays and lower total procedure costs, creating favorable economics for capital investment. Competitive intensity is rising as patent cliffs democratize core technologies and modular, lower-cost platforms reach the market. Meanwhile, mounting evidence that single-use scopes eliminate cross-contamination risk strengthens the value proposition for outpatient settings. Together, these forces position the robotic endoscopy devices market for sustained double-digit expansion through the decade.

Global Robotic Endoscopy Devices Market Trends and Insights

Rapid Adoption Of Minimally-Invasive Robotic Procedures

Clinical evidence shows robotic-assisted surgeries cut complication rates by 50% and trim recovery times by 40% compared with traditional techniques. Hospitals increasingly prioritize these outcomes to meet value-based care mandates, leading to wider platform installs and broader procedural menus. Intuitive Surgical reported 17% procedure growth in Q1 2025, underscoring global momentum. Enhanced 3-D vision, tremor filtration, and ergonomic consoles also mitigate surgeon fatigue, allowing longer and more complex cases in outpatient settings. Collectively, these gains expand the eligible patient pool and reinforce the economic attractiveness of the robotic endoscopy devices market.

AI-Augmented Navigation & Imaging Boosts Diagnostic Yield

Deep-learning models now lift diagnostic yield in robotic bronchoscopy to over 85%, well above the 67.8% baseline of conventional scopes. Johnson & Johnson's MONARCH QUEST platform integrates 260% more compute power with AI-driven path-planning, improving lesion targeting in real time. Cloud-based systems such as Olympus CADDIE extend similar benefits to colorectal screening, where AI raises adenoma detection without extra procedure time. Higher accuracy reduces repeat procedures and accelerates therapeutic decision-making, giving platform owners a clear competitive edge.

High Capital & Per-Procedure Cost of Robotic Platforms

System list prices between USD 1.5 million and USD 2.5 million, plus annual service fees above USD 100,000, impose steep hurdles for smaller centers. Comparative studies show robotic inguinal hernia repair costs EUR 2,810 (USD 3,242.01) versus EUR 726 (USD 837.62) for laparoscopic alternatives, underscoring payback challenges where reimbursement lags. New entrants like CMR Surgical target this gap with modular architecture priced below legacy systems, yet widespread budget constraints in lower-income regions continue to suppress uptake.

Other drivers and restraints analyzed in the detailed report include:

- Favorable Reimbursement for Robotic GI & Pulmonary Interventions

- Demand for Single-Use Robotic Endoscopes to Curb Infections

- Stringent Regulatory Approvals for Patient Safety

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Therapeutic robotic endoscopes accounted for 55.52% of the robotic endoscopy devices market in 2024, underscoring provider demand for systems that combine diagnosis and intervention in a single sitting. Leading products execute complex maneuvers such as endoscopic submucosal dissection and natural-orifice transluminal surgery, enabling scar-free outcomes that appeal to both patients and payers. Johnson & Johnson's MONARCH platform illustrates this premium positioning, while EndoQuest pursues flexible, single-port concepts for GI procedures. Although therapeutic dominance prevails, diagnostic devices show greater headroom; AI-enhanced visualization lifts early cancer detection, pushing diagnostic unit sales at a 15.25% CAGR. Capsule systems and hybrid imaging robots widen access, hinting at future convergence where one console manages full care pathways. The robotic endoscopy devices market size for therapeutic systems is projected to broaden steadily, but diagnostic innovation is set to outpace as preventive medicine becomes policy priority.

Diagnostic platforms remain a smaller slice, yet investors funnel capital into wireless capsule robots and cloud-enabled analytics that shorten procedure times. Early-stage projects such as swallowable pump-jet cameras expand the reach of gastrointestinal screening, particularly in rural regions where full theaters are scarce. As these devices secure regulatory clearance, the robotic endoscopy devices market share for diagnostic solutions is expected to climb, narrowing the revenue gap versus therapeutic peers.

The Robotic Endoscopy Devices Market Report is Segmented by Product (Diagnostic Robotic Endoscopes [Capsule Robots and Imaging Robots], Therapeutic Robotic Endoscopes), Application (Laparoscopy, Bronchoscopy, and More), End User (Hospitals, Ambulatory Surgical Centers, and Specialty Clinics) and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 38.82% of 2024 revenue, supported by Medicare payment clarity and a mature surgeon talent pool. Flagship centers in the United States routinely adopt next-generation consoles within months of clearance, sustaining robust upgrade cycles. Canada follows similar patterns, while Mexico's private hospitals court medical tourists to finance advanced installations.

Europe holds significant share but confronts regulatory headwinds and green-policy scrutiny of single-use plastics. Germany, France, and the United Kingdom dominate installed bases, yet multi-year conformity assessments under the Medical Device Regulation delay market entry for new entrants. Nordic health systems investigate robotic hernia repair benefits, but cost-effectiveness questions remain open, tempering rapid scale-up.

Asia-Pacific exhibits the fastest regional CAGR at 13.62%. China anchors momentum through domestic champions offering consoles at discounts of 30%-40% relative to Western peers, spurring adoption across tertiary hospitals. Japan pioneers unique platforms and 5G-enabled telesurgery demonstrations, while South Korea emphasizes robotics in national cancer-screening protocols. Emerging ASEAN economies and India's private chains invest aggressively, seeing robotics as a differentiator for inbound medical tourism. Consequently, the robotic endoscopy devices market size for Asia-Pacific is forecast to overtake Europe near the end of the outlook window.

Middle East & Africa record nascent but promising uptake, led by Gulf Cooperation Council projects that bundle robotics into flagship hospital build-outs. South Africa spearheads sub-Saharan adoption. Latin America witnesses steady installations in Brazil and Chile, though currency volatility constrains wider diffusion. Across these regions, vendor financing and procedure-based leasing models are critical in unlocking incremental demand.

- Intuitive Surgical

- Johnson & Johnson (Auris Health)

- Medtronic

- Olympus

- Asensus Surgical

- CMR Surgical

- Medrobotics

- Brain Lab

- Avatera Medical

- AKTORmed

- Virtuoso Surgical

- Noah Medical

- EndoQuest Robotics

- Microbot Medical

- Titan Medical

- Fujifilm Holdings Corp.

- SHINVA Medical

- Apollo Endosurgery

- Stryker

- Karl Storz SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption Of Minimally-Invasive Robotic Procedures

- 4.2.2 Rising Geriatric, Obese & Diabetic Population

- 4.2.3 Favorable Reimbursement For Robotic GI & Pulmonary Interventions

- 4.2.4 AI-Augmented Navigation & Imaging Boosts Diagnostic Yield

- 4.2.5 Surge In Dedicated Outpatient Robotic Bronchoscopy Suites

- 4.2.6 Demand For Single-Use Robotic Endoscopes To Curb Infections

- 4.3 Market Restraints

- 4.3.1 High Capital & Per-Procedure Cost Of Robotic Platforms

- 4.3.2 Stringent Regulatory Approvals For Patient-Safety

- 4.3.3 Shortage Of Surgeons Trained On Robotic Endoscopy

- 4.3.4 Sustainability Push Against Disposable Robotic Scopes

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Diagnostic Robotic Endoscopes

- 5.1.1.1 Capsule Robots

- 5.1.1.2 Imaging/Visualization Robots

- 5.1.2 Therapeutic Robotic Endoscopes

- 5.1.2.1 Surgical Endoscopy Platforms

- 5.1.2.2 Robotic Bronchoscopes

- 5.1.2.3 NOTES & Transluminal Robots

- 5.1.1 Diagnostic Robotic Endoscopes

- 5.2 By Application

- 5.2.1 Laparoscopy

- 5.2.2 Bronchoscopy

- 5.2.3 Colonoscopy

- 5.2.4 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Specialty Clinics

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Intuitive Surgical Inc.

- 6.3.2 Johnson & Johnson (Auris Health)

- 6.3.3 Medtronic PLC

- 6.3.4 Olympus Corporation

- 6.3.5 Asensus Surgical Inc.

- 6.3.6 CMR Surgical Ltd

- 6.3.7 Medrobotics Corporation

- 6.3.8 Brainlab AG

- 6.3.9 Avatera Medical GmbH

- 6.3.10 AKTORmed GmbH

- 6.3.11 Virtuoso Surgical

- 6.3.12 Noah Medical

- 6.3.13 EndoQuest Robotics

- 6.3.14 Microbot Medical

- 6.3.15 Titan Medical

- 6.3.16 Fujifilm Holdings Corp.

- 6.3.17 SHINVA Medical

- 6.3.18 Apollo Endosurgery

- 6.3.19 Stryker Corp.

- 6.3.20 Karl Storz SE

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment