|

시장보고서

상품코드

1851206

줄기세포 제조 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Stem Cell Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

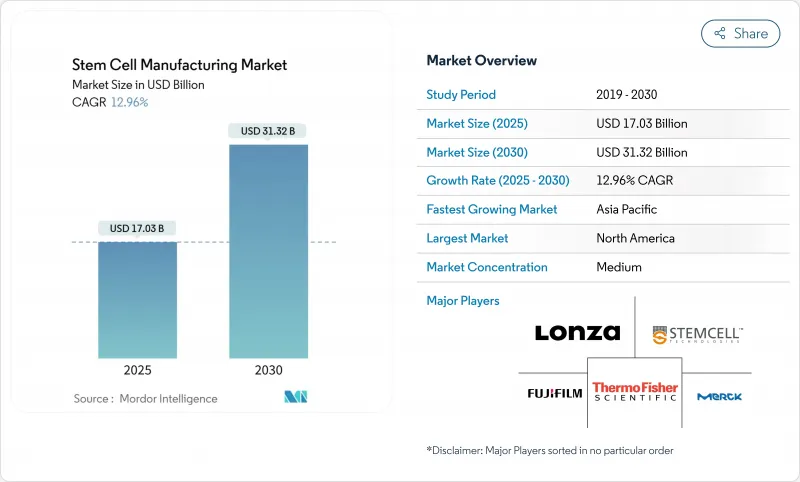

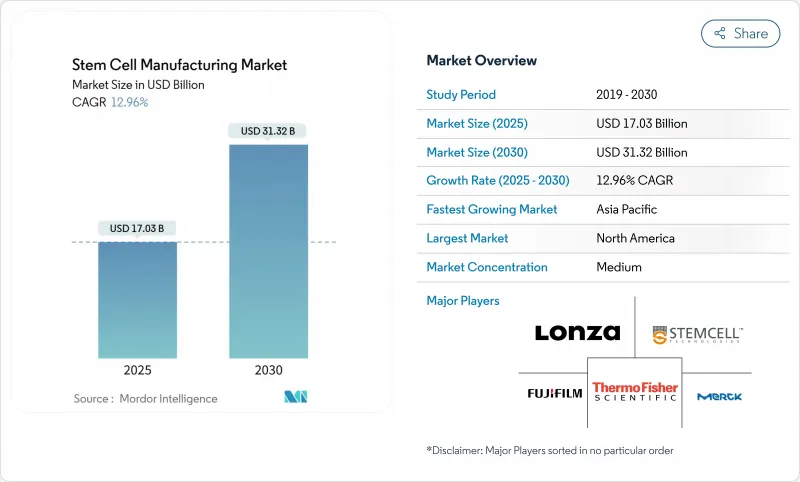

세계의 줄기세포 제조 시장 규모는 2025년까지 170억 3,000만 달러로 추정되며, 예측기간 중(2025-2030년) CAGR 12.96%를 나타낼 전망이며, 2030년까지 313억 2,000만 달러에 달할 것으로 예측됩니다.

자동화 폐쇄 시스템 바이오리액터의 채용 증가, 주요 국가의 규제 조화, 재생 치료에 대응하기 위한 대량 생산의 필요성이 이 성장 궤도를 총체적으로 지원하고 있습니다. 소모품은 제조마다 반복적으로 사용되기 때문에 여전히 가장 큰 판매 기여자입니다. 한편, 장비는 제조업체가 인력 부족을 해결하기 위해 로봇 공학과 고급 분석 기술을 도입하고 있기 때문에 가장 빠르게 확대되고 있습니다. 북미는 강력한 FDA의 틀과 지속적인 관민 자금으로 리더십을 유지하고 있지만, 아시아태평양은 일본과 중국의 정책 근대화를 배경으로 가장 빠르게 확대되고 있습니다. 수동 워크플로우에서 단일 사용 기술로의 전환은 오염 위험을 줄이고 임상 현장에 가까운 분산 제조를 가능하게 합니다. 그러나 소태아혈청 공급의 병목과 바이오프로세스 공학의 세계적인 기능 부족이 당면의 사업 운영상의 과제가 되고 있습니다.

세계 줄기세포 제조 시장 동향과 통찰

자동화 폐쇄 시스템 바이오리액터가 제조 패러다임을 변화

자동화 폐쇄 시스템 바이오리액터의 산업 전개는 줄기세포 제조 시장 전체의 생산 경제성을 재정의하고 있습니다. Lonza의 Cocoon 플랫폼은 GMP 컴플라이언스를 유지하면서 사람의 개입을 최대 70%까지 줄이고 숙련된 운영자의 세계 부족을 직접 완화합니다. 바이오프로세스 엔지니어의 구인수는 2019년부터 2023년 사이에 400% 증가했지만, 여전히 만족이 어려워 자동화의 긴급성이 부각되고 있습니다. 일회용 어셈블리는 교차 오염을 줄이고 시설 실적를 줄이고 포인트 오브 케어 딜리버리에 가까운 곳에서 생산하는 분산 생산 모델을 가능하게 합니다. Sydney Institute of Technology의 3D 프린팅 마이크로플루이딕스 수확기는 여러 단계를 단일 장치에 통합하여 배치 당 비용을 줄이고 세포 생존을 향상시킵니다. 이러한 기술 혁신을 종합하면 장기적인 생산능력 향상이 예상되며 CAGR 12.96%라는 시장 전망을 뒷받침하고 있습니다.

관민 자금 조달의 확대가 상업화를 가속

정부의 이니셔티브와 산업계의 제휴가 가속되고, 첨단 시설과 노동력 프로그램에 자본이 유입하고 있습니다. National Institute for Innovation in Manufacturing Biopharmaceuticals(NIIMBL)는 규모 확장 문제를 해결하기 위한 공동 프로젝트를 지원하고 동시에 신인 기술자에게 경험적인 교육을 제공합니다. 바이오 파운드리 모델은 종종 대학에 설치되어 반복 사이클을 단축하고 소규모 기업이 많은 자본 지출없이 최첨단 인프라를 활용할 수 있도록합니다. 이러한 자금의 흐름은 기술준비 수준을 향상시키고, 새로운 치료법을 상업적인 상시에 접근하고, 줄기세포 제조 시장 전체의 장기적 수요 기반을 견고하게 하고 있습니다.

높은 GMP 운영 비용이 시장 진입을 저해

GMP에 준거한 시설의 건설 및 운영에는 1,000만-5,000만 달러의 선행 투자가 필요하고, 운영비는 연간 매출의 15-25%를 차지하기 때문에 소규모 기업이나 신흥국에 있어서는 과제가 되고 있습니다. 선도적인 기존 기업은 규모의 경제와 다양한 제품 포트폴리오를 활용하여 이러한 비용을 흡수하고 경쟁 격차를 늘리고 있습니다. Bio-Techne의 동물 미사용 시약으로의 전환은 공급업체가 비용 억제 균형을 유지하면서 컴플라이언스 중심의 프로세스 업그레이드에 지속적으로 투자해야 한다는 것을 이야기합니다. 세포치료에 특화된 제조수탁기관(CMO)은 접근의 민주화를 시작하고 있지만 수요에 비해 생산능력은 여전히 제한되어 있습니다.

부문 분석

2024년 소모품은 줄기세포 제조 시장 점유율의 47.12%를 차지했으며, 배지, 시약, 단일 사용 어셈블리가 모든 제조 운전에 필수적임을 명확하게 보여주고 있습니다. 수요 회복은 안정적인 현금 흐름을 보장하기 때문에 공급업체는 오염 위험을 줄이는 무혈청 제제와 화학적으로 정의된 제형에 투자하여 가까워지는 소태아혈청 부족을 해결할 수 있습니다. 기기는 현재 절대적인 매출 규모가 작지만, 폐쇄계 바이오리액터, 자동 셀 분류기, AI 대응 모니터링 프로브가 시설에 도입됨에 따라 2030년까지 CAGR은 13.85%를 보일 것으로 예측됩니다. 줄기세포 제조업계에서는 장비 벤더와 치료법 개발 기업과의 전략적 제휴가 급증하고 있어 실시간으로 공정 최적화가 가능해 배치 불량이 감소하고 있습니다.

새로운 플랫폼 기술은 장비 부문의 혁신적인 특성을 보여줍니다. Ori Biotech의 IRO 시스템은 70%의 노동 절감과 50%의 비용 절감을 실현하여 스마트 하드웨어가 생산 비용 기준을 재설정할 수 있는 방법을 강조합니다. 머신러닝 모델을 바이오 리액터에 통합하면 공급 속도와 산소 공급을 다이나믹하게 조정하여 재현성을 높일 수 있습니다. 소모품 공급업체는 센서와 멸균된 가방을 번들하여 검증을 간소화하는 엔드 투 엔드 키트를 생성하여 지원합니다. 이러한 동향을 종합하면 줄기세포 제조 시장 전체의 수익 풀이 다양화되어 회복력이 강화됩니다.

지역 분석

북미는 세계 최대의 세포 치료 개발자 클러스터, 풍부한 벤처 캐피탈, 상업화 리드 타임을 단축하는 RMAT 및 조기 승인 등 FDA 패스웨이에 견인되어 2024년 매출 점유율은 41.32%를 유지했습니다. 또한 이 지역에는 CMO가 가장 집중되어 소규모 스폰서에게 유연한 용량을 제공합니다. 그러나 바이오프로세스 엔지니어의 부족은 심각하고 결원수가 유능한 후보자 수를 3대 1로 웃돌고 있으며, 인재육성의 대처가 더욱 추진되지 않는 한 건설계획이 억제될 가능성이 있습니다. 커뮤니티 칼리지, NIIMBL, 산업계의 파트너십은 기술자 양성을 가속화하고 있지만, mRNA 및 바이러스 벡터 시설과의 경쟁은 고용 압력을 강화하고 있습니다.

아시아태평양은 가장 급성장하는 지역으로 일본의 조건부 승인 제도와 중국의 대규모 지방 보조금이 현지 공장의 급속한 확대를 촉진하기 때문에 CAGR 14.22%를 보일 것으로 예측됩니다. 한국은 3유형의 줄기세포 치료를 포함한 16유형의 세포 유래 제품을 승인하고 있으며, 규제의 성숙도를 나타내며 제조 노하우의 수출국으로서의 지위를 확립하고 있습니다. 또한 중국과 인도에서는 비용 경쟁력 있는 노동력과 토지가 있기 때문에 다국적 기업이 위성 시설의 설립에 유치되어 공급망의 다양화가 진행되고 있습니다. 그러나 ASEAN 회원국 간의 승인 절차에 차이가 있기 때문에 다국적 스폰서는 시장 출시까지의 시간적 갈등이 여전히 발생하고 있으며 이를 신중하게 극복해야 합니다.

유럽은 더 엄격한 시장 환경이지만 중요한 역할을 담당합니다. 유럽 의약품청(EEA)의 ATMP의 틀은 엄격한 품질 기준을 정하고 있으며, 개발 기간을 연장하는 한편, 제품의 안전성에 대한 세계적인 신뢰를 높이고 있습니다. 유럽 약전의 세포 유래 제품에 관한 장이 시행됨으로써 분석 기준이 명확해지고 검증의 불확실성이 완화되었습니다. Horizon Europe과 각국의 프로그램에 의한 자금 지원은 인프라의 업그레이드를 계속 지원하고 있는 한편, 동물 유래 성분에 대한 사회적 회의심은 화학적으로 정의된 배지의 채용을 가속화하고 있습니다. 중동, 아프리카, 남미와 같은 소규모 지역에서는 브라질과 남아프리카 센터가 줄기세포 이식 프로그램을 시험적으로 실시하는 등 지역에서 새로운 노력이 시작되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 자동 폐쇄계 바이오리액터와 일회용 기술

- 줄기세포 연구개발에 관민출자 확대

- 만성 질환 부담 증가가 재생 수요를 촉진

- 줄기세포제품의 치료효과에 대한 사회적 인지 고조

- 유리한 규제 및 정책 지원

- 전략적 제휴와 시장 확대

- 시장 성장 억제요인

- 높은 GMP 운영 비용

- 복잡한 규제와 윤리적 장애물

- 세포 제조 바이오프로세스 기술자의 부족

- GMP 성장 인자와 벡터 공급망의 병목

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 라이벌의 격렬함

제5장 시장 규모와 성장 예측

- 제품 유형별

- 배양 배지

- 소모품

- 기기

- 줄기세포 라인

- 서비스

- 용도별

- 줄기세포 치료

- 신약개발 및 독성학

- 줄기세포 은행

- 조직 공학 및 재생 의료

- 최종 사용자별

- 제약 및 바이오테크놀러지 기업

- 학술연구기관

- 세포 및 조직은행

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Sartorius AG

- Lonza Group AG

- FUJIFILM Cellular Dynamics

- STEMCELL Technologies

- Becton, Dickinson and Company

- Corning Incorporated

- Miltenyi Biotec

- Takeda Pharmaceutical Co.

- Daiichi-Sankyo Co.

- AbbVie Inc.

- Pluri(Pluristem Therapeutics)

- Cytiva(Danaher)

- Bio-Rad Laboratories

- CellGenix GmbH

- BICO(CELLINK)

제7장 시장 기회와 장래의 전망

JHS 25.11.21The Stem Cell Manufacturing Market size is estimated at USD 17.03 billion in 2025, and is expected to reach USD 31.32 billion by 2030, at a CAGR of 12.96% during the forecast period (2025-2030).

Rising adoption of automated, closed-system bioreactors, regulatory harmonization in major economies, and the need for large-batch production to serve regenerative therapies collectively underpin this growth trajectory. Consumables remain the single largest revenue contributor, reflecting their recurring use in every production run, while instruments are scaling fastest as manufacturers deploy robotics and advanced analytics to counter talent shortages. North America retains leadership through strong FDA frameworks and sustained public-private funding, whereas Asia Pacific posts the quickest expansion on the back of policy modernization in Japan and China. The transition from manual workflows toward single-use technologies is lowering contamination risk and enabling distributed manufacturing close to clinical sites. However, bottlenecks in fetal bovine serum supply and a global skills crunch in bioprocess engineering pose near-term operational challenges.

Global Stem Cell Manufacturing Market Trends and Insights

Automated, Closed-System Bioreactors Transform Manufacturing Paradigms

Industrial deployment of automated, closed-system bioreactors is redefining production economics across the stem cell manufacturing market. Lonza's Cocoon platform cuts human intervention by up to 70% while maintaining GMP compliance, directly alleviating the global shortage of skilled operators. Job postings for bioprocess engineers climbed 400% between 2019 and 2023, yet remain difficult to fill, underscoring the urgency of automation. Single-use assemblies reduce cross-contamination and lower facility footprints, enabling distributed production models that place manufacturing closer to point-of-care delivery. The University of Technology Sydney's 3D-printed microfluidic harvester integrates multiple steps into one device, shrinking cost per batch and improving cell viability. Collectively, these innovations anchor a long-term uplift in capacity that underpins the market's 12.96% CAGR outlook.

Growing Public-Private Funding Accelerates Commercial Translation

Escalating government initiatives and industry alliances continue to channel capital into advanced facilities and workforce programs. The National Institute for Innovation in Manufacturing Biopharmaceuticals (NIIMBL) sponsors collaborative projects that de-risk scale-up challenges while offering experiential training to new technicians. Biofoundry models, often housed within academic settings, are shortening iteration cycles and enabling small firms to access state-of-the-art infrastructure without heavy capital outlay. These funding streams improve technology readiness levels and bring novel therapies closer to commercial launch, solidifying the long-term demand base across the stem cell manufacturing market.

High GMP Operational Costs Constrain Market Entry

Building and running GMP-compliant facilities requires USD 10-50 million in upfront investments, with operating expenses consuming 15-25% of annual revenue, challenging small firms and emerging nations. Larger incumbents leverage economies of scale and diversified product portfolios to absorb these costs, widening competitive gaps. Bio-Techne's transition to animal-free reagents illustrates how vendors must continuously invest in compliance-driven process upgrades while balancing cost containment. Contract manufacturing organizations (CMOs) specializing in cell therapies are beginning to democratize access, yet capacity remains limited relative to demand.

Other drivers and restraints analyzed in the detailed report include:

- Rising Chronic-Disease Burden Creates Sustained Demand Pull

- Public Awareness Drives Market Acceptance and Investment

- Complex Regulatory Frameworks Slow Global Market Development

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, consumables accounted for 47.12% of the stem cell manufacturing market share, underscoring the indispensability of media, reagents, and single-use assemblies to every production run. Recurrent demand ensures stable cashflows, allowing suppliers to invest in serum-free and chemically defined formulations that mitigate contamination risk and combat the looming fetal bovine serum shortage. Instruments, although smaller in absolute revenue today, are projected to register a 13.85% CAGR through 2030 as facilities install closed-system bioreactors, automated cell sorters, and AI-enabled monitoring probes. The stem cell manufacturing industry is witnessing a surge in strategic alliances between equipment vendors and therapy developers, enabling real-time process optimization and reducing batch failures.

Emerging platform technologies exemplify the transformational nature of the instrument segment. Ori Biotech's IRO system delivers 70% labor reduction and 50% cost savings, highlighting how smart hardware can reset production cost baselines. Integration of machine learning models into bioreactors allows dynamic adjustment of feed rates and oxygenation, elevating reproducibility. Consumable suppliers are responding by bundling sensors and pre-sterilized bags, creating end-to-end kits that simplify validation. Collectively, these trends diversify revenue pools and enhance resilience across the stem cell manufacturing market.

The Stem Cell Manufacturing Market Report is Segmented by Product Type (Culture Media, Consumables, Instruments, Stem Cell Lines, and Services), Application (Stem Cell Therapy, Drug Discovery and Toxicology, Stem Cell Banking and More), End User (Pharmaceutical and Biotechnology Companies, Cell and Tissue Banks, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 41.32% revenue share in 2024, driven by the world's largest cluster of cell therapy developers, abundant venture capital, and FDA pathways such as RMAT and accelerated approval that shorten commercialization lead times. The region also houses the highest concentration of CMOs, offering flexible capacity to smaller sponsors. Yet the acute shortfall of bioprocess engineers-vacancies outpace qualified candidates three-to-one-could restrain build-out plans unless workforce initiatives gain further traction. Partnerships among community colleges, NIIMBL, and industry accelerate technician training, but competition from mRNA and viral-vector facilities intensifies hiring pressures.

Asia Pacific is the fastest-growing territory, projected to log a 14.22% CAGR as Japan's conditional approval scheme and China's sizeable provincial subsidies encourage rapid scaling of local plants. South Korea's authorization of 16 cell-based products, including three stem cell therapies, underscores regulatory maturity and positions the peninsula as an exporter of manufacturing know-how. Furthermore, cost-competitive labor and land in China and India lure multinational firms to establish satellite facilities, diversifying supply chains. However, disparate approval procedures among ASEAN members still create time-to-market frictions that multinational sponsors must navigate carefully.

Europe commands a significant but more regulated market environment. The European Medicines Agency's ATMP framework sets stringent quality benchmarks, which extend development timelines yet elevate global confidence in product safety. Implementation of the European Pharmacopoeia chapter on cell-based products offers clearer analytical standards, easing some validation uncertainties. Funding from Horizon Europe and national programs continues to support infrastructure upgrades, while public skepticism toward animal-derived components accelerates adoption of chemically defined media. Smaller regions such as the Middle East and Africa and South America observe emergent local initiatives-Brazilian and South African centers now pilot stem cell transplant programs-yet limited capital and skills infrastructures temper near-term scale-up prospects.

- Thermo Fisher Scientific

- Merck

- Sartorius

- Lonza Group

- FUJIFILM Cellular Dynamics

- Stem Cell Technologies

- Beckton Dickinson

- Corning

- Miltenyi Biotec

- Takeda Pharmaceutical Co.

- Daiichi-Sankyo Co.

- Abbvie

- Pluri (Pluristem Therapeutics)

- Cytiva

- Bio-Rad Laboratories

- CellGenix

- BICO ( CELLINK )

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Automated, closed-system bioreactors & single-use tech

- 4.2.2 Growing public-private funding for stem-cell R&D

- 4.2.3 Rising chronic-disease burden fueling regenerative demand

- 4.2.4 Growing public awareness about the therapeutic potency of stem cell products

- 4.2.5 Favorable regulatory and policy support

- 4.2.6 Strategic collaborations and market expansion

- 4.3 Market Restraints

- 4.3.1 High GMP operational costs

- 4.3.2 Complex regulatory and ethical hurdles

- 4.3.3 Shortage of cell-manufacturing bioprocess engineers

- 4.3.4 Supply-chain bottlenecks for GMP growth factors and vectors

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Culture Media

- 5.1.2 Consumables

- 5.1.3 Instruments

- 5.1.4 Stem Cell Lines

- 5.1.5 Services

- 5.2 By Application

- 5.2.1 Stem Cell Therapy

- 5.2.2 Drug Discovery and Toxicology

- 5.2.3 Stem Cell Banking

- 5.2.4 Tissue Engineering and Regenerative Medicine

- 5.3 By End User

- 5.3.1 Pharmaceutical and Biotechnology Companies

- 5.3.2 Academic and Research Institutes

- 5.3.3 Cell and Tissue Banks

- 5.3.4 Other End Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Thermo Fisher Scientific Inc.

- 6.3.2 Merck KGaA

- 6.3.3 Sartorius AG

- 6.3.4 Lonza Group AG

- 6.3.5 FUJIFILM Cellular Dynamics

- 6.3.6 STEMCELL Technologies

- 6.3.7 Becton, Dickinson and Company

- 6.3.8 Corning Incorporated

- 6.3.9 Miltenyi Biotec

- 6.3.10 Takeda Pharmaceutical Co.

- 6.3.11 Daiichi-Sankyo Co.

- 6.3.12 AbbVie Inc.

- 6.3.13 Pluri (Pluristem Therapeutics)

- 6.3.14 Cytiva (Danaher)

- 6.3.15 Bio-Rad Laboratories

- 6.3.16 CellGenix GmbH

- 6.3.17 BICO ( CELLINK )

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment