|

시장보고서

상품코드

1851208

스마트 디스플레이 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Smart Display - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

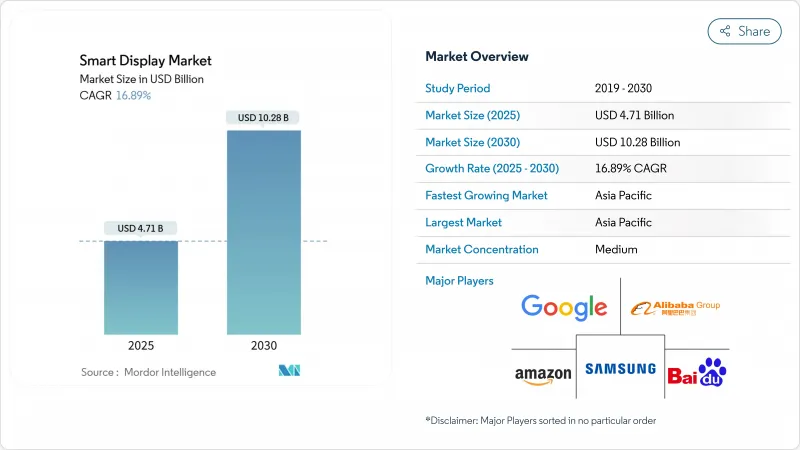

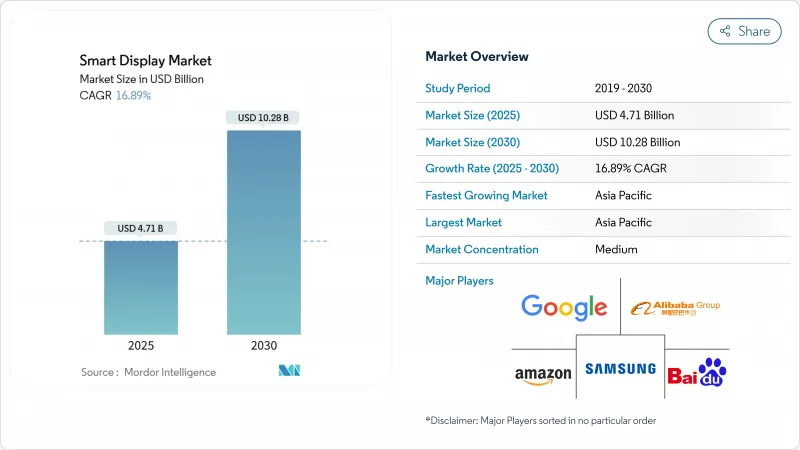

세계의 스마트 디스플레이 시장은 2025년 47억 1,000만 달러로, 2030년까지 102억 8,000만 달러에 이를 것으로 예측되며 CAGR은 16.89%로 예상됩니다.

음성 전용 스크린에서 AI 주도 멀티모달 허브로의 업그레이드 사이클은 설치 기반을 확대하면서 평균 판매 가격을 확대하고 있습니다. Matter 프로토콜을 채택하면 플랫폼 록인이 제거되고 경쟁은 생태계 독점성보다 하드웨어 혁신으로 전환하고 있습니다. 자동차 조종석, OLED의 보급, AI를 강화한 10인치 이상의 모델은 수익 상승을 강화하고 있습니다. 수직 통합 패널 제조업체는 8-10인치 LCD 부족에도 불구하고 여백을 유지합니다. 반대로 기업 구매자는 마이크 상시 연결 위험으로부터 조달 사이클을 장기화하고 있으며 단기 출하 기세를 약화시키고 있습니다.

세계 스마트 디스플레이 시장 동향과 통찰

북미에서 멀티 모달 음성 우선 스마트 홈 허브 채택 증가

스마트 디스플레이는 조명, 보안, 엔터테인먼트 시스템을 단일 인터페이스로 제어하는 시각 및 음성 하이브리드로 진화하고 있습니다. 음성 어시스턴트의 보급은 2026년까지 미국에서 1억 5,710만 사용자에 이를 것으로 예상되며, 보다 풍부한 명령을 처리하고 컨텍스트에 맞는 비주얼을 제공하는 장치의 업그레이드를 지원합니다. 일반 인공지능은 통근 데이터를 기반으로 서모스탯을 예열하는 등 적극적인 제안을 가능하게 하고 지각 가치를 높이고 있습니다. Samsung의 Vision AI 탑재 디스플레이는 2024년 프리미엄 카테고리 출하 대수의 28.3%를 획득하는데 기여했습니다. 소매업체는 디스플레이를 구독 서비스에 번들하여 지속적인 수익과 끈기를 촉진합니다. Apple이 첫 스마트 홈 디스플레이를 준비하고 생태계 기업이 매년 라인업을 업데이트하도록 촉구하는 동안 경쟁이 심화되고 있습니다.

플랫폼 상호 운용성을 가속화하는 Matter 호환 장치의 보급

Matter 1.4에서는 Wi-Fi와 Thread를 통합하는 공인 홈 라우터가 도입되어 온보딩 실패를 줄이고 설치자의 시간을 단축합니다. 2025년 중반까지는 1,000개가 넘는 Matter 인증 제품이 등장할 전망으로 소비자는 락인을 두려워하지 않고 브랜드를 혼재시킬 수 있습니다. 기업은 이 프로토콜의 안전한 커미셔닝을 제로 트러스트 지침에 대응하기 위한 한 걸음으로 간주하여 보다 광범위한 상업 전개를 촉진하고 있습니다. 유틸리티자는 수요 반응 프로그램을 지원하기 위해 Matter 기반 에너지 대시보드를 찾고 있습니다. 이 표준은 또한 기존 Wi-Fi 인프라가 배선을 변경하지 않고 스레드 테두리 라우터를 호스팅할 수 있는 접객 분야에서 리노베이션 기회를 풀어 놓았습니다.

상시 연결 마이크 보안 취약점이 B2B 조달 지연의 원인

금융기관과 병원은 공급업체가 데이터 경로를 문서화하고 장치에서 처리가 충분하다는 것을 입증할 때까지 배포를 일시중지합니다. CISO가 ISO 27001 요구사항에 따른 침입 테스트를 요구하기 때문에 조달 사이클은 최대 45일까지 연장됩니다. Matter의 옵션인 오프라인 모드는 몇 가지 우려를 완화하지만 중앙 장치 관리를 복잡하게 하고 비용과 통합의 복잡성을 높이는 하이브리드 아키텍처에 대한 요구를 촉구합니다. FedRAMP와 동등한 인증을 취득한 벤더는 조기에 계약을 획득하여 선행자 이점을 창출하고 있습니다.

부문 분석

음성 어시스턴트 기기의 스마트 디스플레이 시장 규모는 2025년 42억 달러에 달합니다. Amazon Alexa는 Fire TV와 Ring의 크로스셀 기세를 타고 2024년 시장 점유율이 33.7%에 달했습니다. Google Assistant가 Nest 허브를 통해 이에 이어 Alibaba TmallGenie는 중국어 방언을 위해 컨텐츠를 현지화하는 AI 채팅봇 통합에 힘입어 CAGR 18.7%로 성장했습니다. 음성 어시스턴트 디바이스의 스마트 디스플레이 시장 규모는 2025년에 42억 달러에 이르렀으며, 생성형 모델이 과거 대화의 기억을 가능하게 하기 때문에 교체 수요가 강해지고 있습니다. Apple이 2025년 3월에 발표한 6인치 Home Display는 iOS 가구를 HomeKit 세계로 끌어들일 수 있는 새로운 경쟁을 시사합니다.

중국에서는 Baidu DuerOS가 10.3포인트 감소에도 불구하고 모바일 스마트 스크린의 41.1%를 지배하고 있습니다. 브랜드는 비주얼 검색, 어린이 안전 모드, QR 기반 체크아웃을 연결한 멀티모달 장바구니로 차별화를 도모하고 있습니다. 이러한 움직임은 Matter가 커넥티비티의 조화를 시도하고 있음에도 불구하고 스마트 디스플레이 시장이 지역별 체험층으로 세분화되는 방법을 이야기하고 있습니다.

5-10인치 카테고리가 2024년 매출에서 52.7%를 차지한 이유는 싱크대 스페이스와 가시성의 균형이 잡혀 있기 때문입니다. 주방 조리법, 침실 경보 및 책상에서 화상 통화는 대부분이 대각선에 있으며 부품 비용을 낮게 유지합니다. 하지만 소매점, 병원, 자동차 대시보드가 더 풍부한 시각을 요구하기 때문에 10인치 이상의 집단은 CAGR 19.3%로 확대되고 있습니다. 더 넓은 패널은 동시 화상 채팅 및 스마트 홈 대시보드의 화면 분할 모드를 가능하게 하여 사용자의 참여 지표를 향상시킵니다.

대각선이 10인치를 초과하면 평균 판매 가격이 상승하고 제조업체의 이익률이 향상됩니다. 이 부문에서는 OLED의 보급률이 높고, 스마트 디스플레이 시장이 프리미엄 가격대를 획득하는데 도움이 되고 있습니다. 패널 제조업체는 대형 사이즈에 대응하기 위해 생산 능력을 8.6세대 유리 기판으로 시프트하고 있습니다. 반면에 5인치 미만의 장치는 저렴한 가격의 틈새 시장이나 침대 옆에 제공되지만, 이미 소형 화면 알림 역할을 하고 있는 웨어러블과의 경쟁으로 스마트 디스플레이 시장에서의 슬라이스는 줄어들고 있습니다.

LCD는 성숙한 공급망과 경쟁력 있는 가격으로 2024년 81.8%의 점유율을 유지합니다. 자동차 계기판은 열 안정성과 휘도의 관점에서 LTPS LCD가 채용되는 경우가 많습니다. 그러나 OLED의 CAGR 21.8%는 벤더가 깊은 흑색과 유연성을 살려 곡면과 롤러블 폼 팩터를 실현함으로써 가속하고 있습니다. 고급 호텔 스마트 미러는 OLED 라미네이트를 사용하여 반사 유리 뒤에 비활성 디스플레이를 숨기고 높은 ARPU를 요구합니다.

OLED 기반 유닛의 스마트 디스플레이 시장 규모는 한국과 중국의 6세대 플렉서블 팹에 힘입어 2030년까지 30억 달러 이상에 달할 것으로 예측됩니다. MicroLED의 조사는 인쇄 전사 기술이 비용 목표에 가까워지고 있으며, 높은 휘도와 긴 수명을 약속하고 있습니다. 제조업체는 단일 기술의 위험을 피하기 위해 특허 크로스 라이선스와 패널 포트폴리오를 혼합하여 헤지합니다.

지역 분석

아시아태평양은 2024년 매출 점유율 37.6%로 스마트 디스플레이 시장을 선도하고 2030년까지 연평균 복합 성장률(CAGR)은 17.3%로 추이할 것으로 보입니다. Baidu나 Alibaba 등 중국 벤더는 2024년 스마트 스피커 출하 대수의 25.6% 감소에 대응하기 위해 대형 언어 모델을 디스플레이에 탑재해 가치 제안을 리셋했습니다. 정부가 지원하는 AI 칩 구상은 BOM 비용을 낮추고 농촌에의 보급을 확대하는 100달러 이하의 대형 화면 모델을 가능하게 합니다. 한국 브랜드는 OLED의 기술 혁신에 주력해 현지의 패널 에코시스템을 활용해 지역 전체에 프리미엄 유닛을 수출합니다.

북미는 거의 유비쿼터스한 광대역과 높은 음성 어시스턴트의 보급률에 의해 기술 동향 세터로 남아있습니다. 가구가 1세대 스크린을 뛰어난 마이크와 엣지 AI를 갖춘 마터 대응 기종으로 교체하기 때문에 교체 사이클이 성장을 지배하고 있습니다. Amazon은 미국 스마트 스피커의 29%를 유지하고 에코 쇼의 대형 모델로 업셀을 촉구하는 Alexa의 생성형 AI 업그레이드를 전개하고 있습니다. Apple의 2025년 진입은 부유층의 iOS 기반 슬라이스를 유치하고, 벤더의 랭킹을 바꿀 수 있습니다.

유럽에서는 프라이버시와 지속가능성에 중점을 두고 있으며, 디바이스에서의 처리와 재활용 소재를 사용한 디바이스에 대한 수요가 높아지고 있습니다. 유럽의 스마트 홈 시장은 2024년에 221억 1,000만 달러에 이르렀으며, 향후 에코디자인 규칙에서 의무화되는 에너지 관리 기능으로 소비량을 감시하는 Matter 인증 허브에 조달이 진행되고 있습니다. 북유럽의 도입은 음성 어시스턴트의 언어 격차 때문에 지연되고 있지만, 규제의 명확화와 에너지 개수에 대한 보조금에 의해 잠재 수요가 파고날 것으로 기대되고 있습니다. 남미, 중동, 아프리카의 신흥 지역에서는 스마트폰 OEM이 소형 스크린을 번들로 생태계 정착을 촉진하기 때문에 점차 보급이 진행될 것으로 보이지만 가격에 대한 민감성과 연결성 불안정성이 보급을 억제하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 북미의 멀티 모달 음성 우선 스마트 홈 허브 채용 증가

- 플랫폼의 상호 운용성을 가속시키는 Matter 대응 디바이스 보급

- 자동차 OEM에 의한 스마트 미러와 기둥간 조종석 디스플레이의 통합

- AI를 활용한 컨텍스트 UI가 10인치 이상 카테고리에서 프리미엄 가격 구성을 견인하고 아시아가 주도

- 마찰없는 체크 아웃과 동적 선반 가장자리 간판에 대한 소매 기업 수요

- 병원 침대 옆 스마트 단말기가 환자 참여와 HCAHPS 점수를 개선

- 시장 성장 억제요인

- B2B 조달 지연의 원인이 되는 상시 접속 마이크의 보안 취약성

- 8-10인치 LCD 공장의 패널 부족이 계속되어 공급 탄력성이 제한

- 현지화 비용을 높이는 지역별 데이터 프라이버시의 단편화

- 음성 어시스턴트의 언어 지원 격차로 인해 북유럽과 카리브해 지역에서의 보급을 방해

제5장 생태계 분석

제6장 기술 전망

제7장 Porter's Five Forces 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제8장 시장 규모와 성장 예측

- 음성 어시스턴트별

- Amazon Alexa

- Google Assistant

- Baidu DuerOS

- Alibaba TmallGenie

- Apple Siri

- 기타

- 스크린 사이즈별

- 5인치 미만

- 5-10인치

- 10인치 이상

- 디스플레이 기술별

- 액정 디스플레이

- OLED

- 기타(마이크로 LED, 전자 종이)

- 해상도별

- HD(720p)

- 풀 HD(1080p)

- 4K 이상

- 설치 유형별

- 독립형 스마트 디스플레이

- 일체형 스마트 디스플레이(스마트 미러, 키오스크, 선반 가장자리)

- 접속성별

- Wi-Fi 전용

- Wi-Fi 셀룰러

- Wi-Fi Zigbee/Thread/Matter

- 최종 사용자 업계별

- 주택용 스마트 홈

- 자동차

- 리테일 및 호스피탈리티

- 헬스케어

- 기업 및 교육기관

- 기타(교통 허브, 공공 부문)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가(덴마크, 스웨덴, 노르웨이, 핀란드)

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 동남아시아

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동

- GCC

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제9장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amazon.com Inc.

- Google LLC

- Baidu Inc.

- Alibaba Group Holding Ltd.

- Xiaomi Corp.

- Lenovo Group Ltd.

- LG Electronics Inc.

- Samsung Electronics Co., Ltd.

- Meta Platforms Inc.(Portal)

- Sony Corp.

- TCL Tech. Group

- Hisense Group

- Sharp Corp.

- Koninklijke Philips NV

- Panasonic Holdings Corp.

- Huawei Tech. Co. Ltd.

- BOE Technology Group Co. Ltd.

- Vizio Inc.

- JBL(Harman Int'l)

- Apple Inc.

제10장 시장 기회와 장래의 전망

- 화이트 스페이스와 미충족 요구 평가

The smart display market stood at USD 4.71 billion in 2025 and is projected to reach USD 10.28 billion by 2030, reflecting a 16.89% CAGR.

The upgrade cycle from voice-only screens to AI-driven multimodal hubs is widening average selling prices while enlarging the installed base. Matter protocol adoption is dismantling platform lock-in, shifting competition toward hardware innovation rather than ecosystem exclusivity. Automotive cockpits, OLED diffusion, and AI-enhanced above 10-inch models are intensifying revenue upside. Vertically integrated panel makers have preserved margins despite 8-10-inch LCD shortages. Conversely, enterprise buyers have prolonged procurement cycles because of always-on-microphone risks, tempering short-term shipment momentum.

Global Smart Display Market Trends and Insights

Rising adoption of multimodal voice-first smart-home hubs in North America

Smart displays are evolving into visual-voice hybrids that orchestrate lighting, security, and entertainment systems from a single interface. Voice-assistant penetration is expected to reach 157.1 million U.S. users by 2026, underpinning device upgrades that handle richer commands and provide contextual visuals. Generative AI is enabling proactive suggestions-such as pre-warming thermostats based on commute data-raising perceived value. Samsung's Vision AI-equipped displays helped the company capture 28.3% of premium category shipments in 2024. Retailers are bundling displays with subscription services, driving recurring revenue and stickiness. Competitive intensity is heightening as Apple prepares its first smart home display, prompting ecosystem players to refresh line-ups annually.

Proliferation of Matter-compliant devices accelerating platform interoperability

Matter 1.4 introduced certified home routers that unify Wi-Fi and Thread, slashing onboarding failures and cutting installer time. By mid-2025 more than 1,000 Matter-certified products are expected, giving consumers confidence to mix brands without fearing lock-in. Enterprises view the protocol's secure commissioning as a step toward meeting zero-trust mandates, encouraging broader commercial rollouts. Utilities are exploring Matter-based energy dashboards to support demand-response programs. The standard also unlocks retrofit opportunities in hospitality, where existing Wi-Fi infrastructure can host Thread border routers without rewiring.

Security vulnerabilities in always-on microphones causing B2B procurement delays

Financial institutions and hospitals are pausing deployments until vendors document data pathways and prove on-device processing sufficiency. Procurement cycles have stretched by up to 45 days as CISOs demand penetration tests aligned with ISO 27001 requirements. Matter's optional offline mode eases some concerns but complicates central device management, prompting requests for hybrid architectures that add cost and integration complexity. Vendors that achieve FedRAMP-equivalent attestations are winning contracts faster, creating early-mover advantages.

Other drivers and restraints analyzed in the detailed report include:

- Automotive OEM integration of smart mirrors and pillar-to-pillar cockpit displays

- AI-powered contextual UI driving premium price mix in more than 10-inch category

- Persistent panel shortage in 8-10-inch LCD fabs limiting supply elasticity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The smart display market size for voice-assistant devices reached USD 4.2 billion in 2025. Amazon Alexa held 33.7% market share in 2024, riding cross-sell momentum from Fire TV and Ring. Google Assistant followed through Nest hubs, while Alibaba's TmallGenie grew at 18.7% CAGR, buoyed by AI chatbot integration that localizes content for Chinese dialects. The smart display market size for voice-assistant devices reached USD 4.2 billion in 2025, and replacement demand is strengthening as generative models enable memory of prior conversations. Apple's March 2025 six-inch Home Display announcement signals fresh competition that may draw iOS households into its HomeKit universe.

Continued expansion of Mandarin-optimized large language models is eroding Alexa's edge in China, where Baidu DuerOS controlled 41.1% of mobile smart screens despite a 10.3 percentage-point decline. Brands are differentiating via visual search, kid-safe modes, and multimodal shopping carts that link QR-based checkout. These moves illustrate how the smart display market is fragmenting into region-specific experience layers even as Matter attempts to harmonize connectivity.

The 5-10-inch category dominated with 52.7% revenue in 2024 because it balances countertop space and viewing comfort. Kitchen recipes, bedroom alarms, and desk video calls mostly fit this diagonal, keeping BOM costs low. Yet the >10-inch cohort is expanding at a 19.3% CAGR as retailers, hospitals, and vehicle dashboards demand richer visuals. Wider panels invite split-screen modes for simultaneous video chats and smart-home dashboards, elevating user engagement metrics.

Average selling prices jump when diagonal exceeds 10 inches, improving manufacturer margins. OLED penetration is higher in this tier, helping the smart display market command premium price points. Panel makers are shifting capacity toward Gen 8.6 glass substrates to serve the large-format rush. Meanwhile, <5-inch devices remain in budget niches and as bedside companions, but their slice of the smart display market is shrinking under competition from wearables that already occupy the small-screen notification role.

LCD retained 81.8% share in 2024, thanks to mature supply chains and competitive pricing. Automotive instrument clusters often favor LTPS LCD for thermal stability and brightness. However, OLED's 21.8% CAGR is accelerating as vendors exploit its deep blacks and flexibility to fashion curved or rollable form factors. Smart mirrors in luxury hotels use OLED laminates to hide inactive displays behind reflective glass, commanding higher ARPU.

The smart display market size for OLED-based units is forecast to exceed USD 3 billion by 2030, aided by Gen 6 flexible fabs in South Korea and China. MicroLED research promises even higher luminance and lifespan, with printed transfer techniques edging closer to cost targets. Manufacturers are hedging by cross-licensing patents and mixing panel portfolios to avoid single-technology risk.

The Smart Display Market Report is Segmented by Voice Assistant (Amazon Alexa, and More), Screen Size (5 - 10 Inches, and More), Display Technology (LCD, and More), Resolution (Full HD, and More), Installation Type (Stand-Alone, and More), Connectivity (Wi-Fi Only, and More), End-User Industry (Automotive, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific led the smart display market with 37.6% revenue share in 2024 and is set to compound at 17.3% CAGR through 2030. Chinese vendors such as Baidu and Alibaba responded to a 25.6% slump in 2024 smart-speaker shipments by layering large language models onto displays, resetting value propositions. Government-backed AI chip initiatives are lowering BOM costs, enabling sub-USD 100 large-screen models that widen rural penetration. South Korean brands focus on OLED innovation, leveraging local panel ecosystems to export premium units across the region.

North America remains a technology trendsetter with near-ubiquitous broadband and high voice-assistant uptake. Replacement cycles dominate growth as households swap first-generation screens for Matter-capable variants with superior microphones and edge AI. Amazon retained 29% of U.S. smart-speaker units, rolling out generative AI upgrades to Alexa that encourage upsells to larger Echo Show models. Apple's 2025 entry could lure a slice of the affluent iOS base, reshuffling vendor rankings.

Europe emphasizes privacy and sustainability, stimulating demand for devices with on-device processing and recycled materials. The European Smart Home market reached USD 22.11 billion in 2024, and energy-management features mandated by upcoming Ecodesign rules are steering procurement toward Matter-certified hubs that monitor consumption. Nordic adoption lags owing to voice-assistant language gaps, but regulatory clarity and subsidies for energy retrofits are expected to unlock latent demand. Emerging regions in South America, the Middle East, and Africa witness gradual uptake as smartphone OEMs bundle smaller screens to drive ecosystem stickiness, although price sensitivity and patchy connectivity temper volumes.

- Amazon.com Inc.

- Google LLC

- Baidu Inc.

- Alibaba Group Holding Ltd.

- Xiaomi Corp.

- Lenovo Group Ltd.

- LG Electronics Inc.

- Samsung Electronics Co., Ltd.

- Meta Platforms Inc. (Portal)

- Sony Corp.

- TCL Tech. Group

- Hisense Group

- Sharp Corp.

- Koninklijke Philips N.V.

- Panasonic Holdings Corp.

- Huawei Tech. Co. Ltd.

- BOE Technology Group Co. Ltd.

- Vizio Inc.

- JBL (Harman Int'l)

- Apple Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adoption of multimodal voice-first smart-home hubs in North America

- 4.2.2 Proliferation of Matter-compliant devices accelerating platform interoperability

- 4.2.3 Automotive OEM integration of smart mirrors and pillar-to-pillar cockpit displays

- 4.2.4 AI-powered contextual UI driving premium price mix in Above 10-inch category, Asia-led

- 4.2.5 Retail demand for frictionless checkout and dynamic shelf-edge signage

- 4.2.6 Hospital bedside smart terminals improving patient engagement and HCAHPS scores

- 4.3 Market Restraints

- 4.3.1 Security vulnerabilities in always-on microphones causing B2B procurement delays

- 4.3.2 Persistent panel shortage in 8-10-inch LCD fabs limiting supply elasticity

- 4.3.3 Fragmented regional data-privacy mandates raising localisation costs

- 4.3.4 Voice-assistant language support gaps curbing uptake across Nordics and Caribbeans

5 INDUSTRY ECOSYSTEM ANALYSIS

6 TECHNOLOGICAL OUTLOOK

7 PORTER'S FIVE FORCES ANALYSIS

- 7.1 Porter's Five Forces

- 7.1.1 Bargaining Power of Suppliers

- 7.1.2 Bargaining Power of Buyers

- 7.1.3 Threat of New Entrants

- 7.1.4 Threat of Substitutes

- 7.1.5 Intensity of Competitive Rivalry

8 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 8.1 By Voice Assistant

- 8.1.1 Amazon Alexa

- 8.1.2 Google Assistant

- 8.1.3 Baidu DuerOS

- 8.1.4 Alibaba TmallGenie

- 8.1.5 Apple Siri

- 8.1.6 Others

- 8.2 By Screen Size

- 8.2.1 Less than 5 Inches

- 8.2.2 5 - 10 Inches

- 8.2.3 Above 10 Inches

- 8.3 By Display Technology

- 8.3.1 LCD

- 8.3.2 OLED

- 8.3.3 Others (Micro-LED, E-Paper)

- 8.4 By Resolution

- 8.4.1 HD (= 720p)

- 8.4.2 Full HD (1080p)

- 8.4.3 4K and Above

- 8.5 By Installation Type

- 8.5.1 Stand-alone Smart Displays

- 8.5.2 Integrated Smart Displays (smart mirrors, kiosk, shelf-edge)

- 8.6 By Connectivity

- 8.6.1 Wi-Fi Only

- 8.6.2 Wi-Fi + Cellular

- 8.6.3 Wi-Fi + Zigbee/Thread/Matter

- 8.7 By End-user Industry

- 8.7.1 Residential Smart Home

- 8.7.2 Automotive

- 8.7.3 Retail and Hospitality

- 8.7.4 Healthcare

- 8.7.5 Corporate and Education

- 8.7.6 Others (Transportation Hubs, Public Sector)

- 8.8 By Geography

- 8.8.1 North America

- 8.8.1.1 United States

- 8.8.1.2 Canada

- 8.8.1.3 Mexico

- 8.8.2 Europe

- 8.8.2.1 Germany

- 8.8.2.2 United Kingdom

- 8.8.2.3 France

- 8.8.2.4 Italy

- 8.8.2.5 Spain

- 8.8.2.6 Nordics (Denmark, Sweden, Norway, Finland)

- 8.8.2.7 Rest of Europe

- 8.8.3 Asia-Pacific

- 8.8.3.1 China

- 8.8.3.2 Japan

- 8.8.3.3 South Korea

- 8.8.3.4 India

- 8.8.3.5 Southeast Asia

- 8.8.3.6 Australia

- 8.8.3.7 Rest of Asia-Pacific

- 8.8.4 South America

- 8.8.4.1 Brazil

- 8.8.4.2 Argentina

- 8.8.4.3 Rest of South America

- 8.8.5 Middle East

- 8.8.5.1 Gulf Cooperation Council Countries

- 8.8.5.2 Turkey

- 8.8.5.3 Rest of Middle East

- 8.8.6 Africa

- 8.8.6.1 South Africa

- 8.8.6.2 Nigeria

- 8.8.6.3 Rest of Africa

- 8.8.1 North America

9 COMPETITIVE LANDSCAPE

- 9.1 Market Concentration

- 9.2 Strategic Moves

- 9.3 Market Share Analysis

- 9.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 9.4.1 Amazon.com Inc.

- 9.4.2 Google LLC

- 9.4.3 Baidu Inc.

- 9.4.4 Alibaba Group Holding Ltd.

- 9.4.5 Xiaomi Corp.

- 9.4.6 Lenovo Group Ltd.

- 9.4.7 LG Electronics Inc.

- 9.4.8 Samsung Electronics Co., Ltd.

- 9.4.9 Meta Platforms Inc. (Portal)

- 9.4.10 Sony Corp.

- 9.4.11 TCL Tech. Group

- 9.4.12 Hisense Group

- 9.4.13 Sharp Corp.

- 9.4.14 Koninklijke Philips N.V.

- 9.4.15 Panasonic Holdings Corp.

- 9.4.16 Huawei Tech. Co. Ltd.

- 9.4.17 BOE Technology Group Co. Ltd.

- 9.4.18 Vizio Inc.

- 9.4.19 JBL (Harman Int'l)

- 9.4.20 Apple Inc.

10 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 10.1 White-space and Unmet-Need Assessment