|

시장보고서

상품코드

1851214

피하 면역글로불린 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Subcutaneous Immunoglobulin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

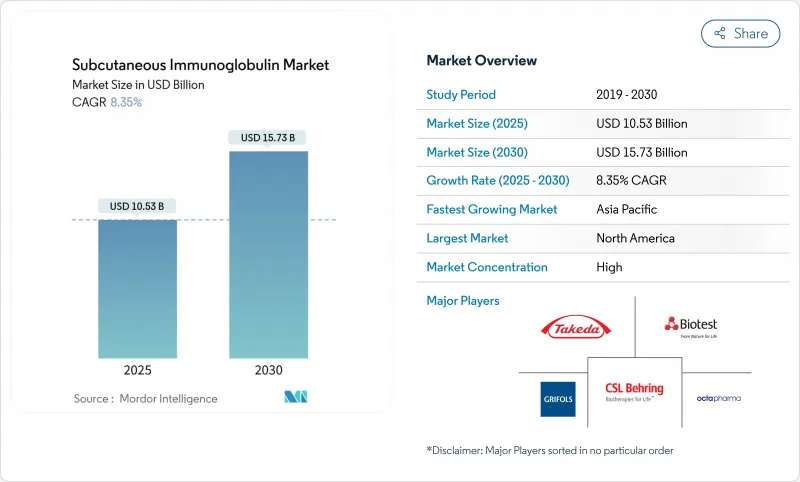

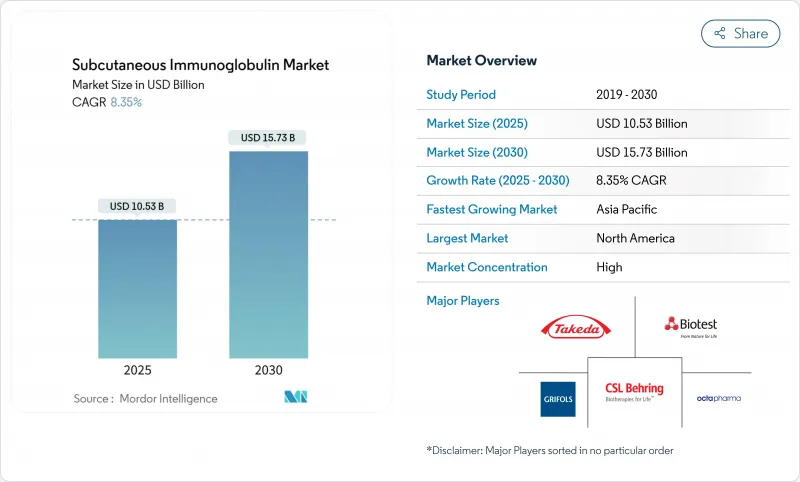

피하 면역글로불린 시장의 2025년 시장 규모는 105억 3,000만 달러로, 2030년에는 157억 3,000만 달러에 이르고, CAGR 8.35%를 나타낼 것으로 예측됩니다.

자기 관리 요법에 대한 환자의 기호, 주입 기술의 향상, 재택치료에 대한 지불자의 지원이 함께 세계의 혈장 채취 능력을 여유로 웃도는 수요 곡선을 유지하고 있습니다. 원발성 면역결핍증은 조기 진단으로 치료 대상이 확대되기 때문에 수요의 중심이며, 신경질환과 혈액질환은 꾸준히 틈새상태를 넘고 있습니다. 촉진형 제제는 1개월의 치료를 한 번에 압축하여 어드히어런스를 향상시키고 간접 비용을 절감하는 특징으로 대응 가능한 베이스를 확대합니다. 지역적으로는 북미가 소비의 주도권을 유지하고 있지만, 일본, 중국, 호주가 신제품을 개발하고 상환경로를 합리화함에 따라 아시아태평양의 궤도는 더욱 급상승합니다. 제조업체 각사는 수율 향상 프로세스, 분획 확대, 공급망을 단축하는 파트너십을 통해 만성적인 혈장 부족에 대응하고 있습니다.

세계의 피하 면역글로불린 시장 동향과 인사이트

원발성 면역결핍증의 유병률 증가가 시장 확대를 견인

대규모 전자 의료 기록 시스템에 통합된 개선된 스크리닝 알고리즘을 통해 선천성 면역결핍 환자는 1만 명당 6명으로 이전 가정을 크게 상회하는 비율로 확인되었습니다. 보다 정확한 역학은 의사가 더 빨리 보충 요법을 처방한다는 것을 의미하며, 이는 환자의 피하 제형에 대한 평생 노출 기간을 증가시킵니다. 병원 데이터에서 중증 감염으로 인한 입원의 평균 비용은 12만 2,739달러이며 보험사가 예방적 면역글로불린 요법에 자금을 제공하도록 설득하는 수준입니다. 다운증후군 및 기타 증후군 질환에서 면역 결핍도 동시에 발견되어 치료 대상이 확산되고 있습니다. COVID-19의 경험은 유행 위험으로의 유행 위험으로의 전환과 함께 취약한 그룹에 대한 IgG의 예방적 사용을 더욱 뒷받침합니다. 이러한 요인들이 결합되어 피하 면역글로불린 시장의 기준선 수요가 높아져 전년 대비 수량 성장이 안정됩니다.

환자의 선호가 IVIG에서 SCIG로의 전환을 가속화

조사 데이터에 따르면, 환자의 82%가 피하 투여를 선호하고, 84%가 자율성과 이동 부담의 경감을 이유로 재택 투여를 지지하고 있습니다. 실제 임상시험에서도 특히 만성 신경근 질환에서 전신 반응의 감소와 함께 동등한 효능이 확인되었습니다. 의료 경제적 분석에 따르면 간호사가 피하 투여에 소비하는 시간은 환자 1인당 연간 35시간인 반면 정맥내 투여에서는 그보다 훨씬 많다고 합니다. 프리필드 주사기, 수동 푸시 옵션, 소형 휴대용 펌프는 한때 치료를 주입실로 제한했던 기술적 장애물을 제거합니다. 이러한 편의성의 조합은 신규 참가자의 안정적인 흐름이 피하 면역글로불린 시장으로 직접 흐르게 합니다.

세계 혈장 공급의 제약이 시장 성장의 지속성에 도전

1리터의 혈장이 환자에게 투여되기까지 7-12개월 분획이 필요하기 때문에 수요가 적은 경우에도 재고에 부담이 듭니다. 영국은 2025년까지 혈장 자급률을 0%에서 25%로 끌어올렸고, 2031년까지 30-35%를 목표로 하고 있습니다. 제조업체는 공정을 업그레이드했으며 ADMA Biologics는 최적화된 크로마토그래피 및 바이러스 여과 단계를 사용하여 20% 수율 향상을 신청했습니다. 그러나 주요 기증자 국가에서의 회수 정책의 변화는 여전히 성장을 억제하고 있으며 지역 부족은 분획 능력이 제한된 개발 도상국에서 처음으로 나타납니다. 따라서 피하 면역글로불린 시장은 혈장 1리터당 더 늘리기 위한 끊임없는 기술 혁신에 의존하고 있습니다.

부문 분석

원발성 면역결핍증은 2024년 매출의 58.67%를 차지했고, CAGR 8.96%로 전진하고 있으며, 피하 면역글로불린 시장의 최대 슬라이스를 지원하고 있습니다. 의사의 의식 향상, 신생아 스크리닝 시험, 유전체 검사가 환자를 조기에 발견하고 치료 수명을 연장하는 것으로 이어지고 있습니다. 화학요법, 줄기세포 이식 및 항류마티스 약물과 관련된 이차성 면역결핍은 이전에 병원에서 IVIG 주입에 의존했던 대규모 코호트를 증가시켰습니다. 만성 염증성 탈수성 다발성 신경염과 다소성 운동 신경병증은 유지 요법이 가이드라인에서 지원되기 때문에 신경계에 대한 응용이 가장 빠르게 진행되고 있습니다. 성인 CIDP에 대한 껌 마가드 리퀴드의 약사 승인은 2025년에 지불자의 인지도를 넓혔습니다. 자가면역성 뇌염과 스티프퍼슨 증후군에 대한 새로운 연구는 잠재적인 환자층을 더욱 확대하고 있습니다. Precision Medicine Initiative는 혈청 바이오마커 패널과 머신러닝 알고리즘을 사용하여 피하 및 정맥 내 환자를 계층화합니다. 이러한 데이터 가이드를 기반으로 한 매칭은 자원 할당을 최적화하고, 어드히어런스를 향상시키고, 피하 면역글로불린 시장의 성장이 환자 중심이 되는 것을 보장합니다.

부문의 다양성은 탄력성을 보장합니다. 혈장이 부족하고 수량 배분이 제한되는 경우 제조업체는 핵심 면역 결핍 사용자를 버리지 않고도 가치있는 신경 부문에 공급을 재분배 할 수 있습니다. 병원, 클리닉, 재택 케어 서비스는 보다 광범위한 적응증을 반영하도록 교육 내용을 조정하여 오 투여의 위험을 줄입니다. 치료의 밑단이 확산됨에 따라 실제 임상 증거 네트워크는 안전, 효능 및 QOL(생활의 질) 결과를 수집하고 지불 측 문서에 피드백합니다. 이 피드백 루프는 계약 협상을 강화하고 수식을 보장합니다. 전반적으로, 응용의 폭은 피하 면역글로불린 산업을 단일 용도의 제품 라인이 아닌 다목적 치료 플랫폼으로 변모시킵니다.

기존의 펌프 점적은 임상 프로토콜의 정착과 폭넓은 디바이스의 이용가능성으로 인해 2024년 매출 점유율은 48.67%를 유지했습니다. 이 방법은 프로그램 가능한 유량으로 주입 부위의 불쾌감을 최소화 할 수 있기 때문에 소아와 손의 민첩성에 제한이있는 환자에게 여전히 선호되고 있습니다. 그럼에도 불구하고, 촉진 요법은 히알루로니다아제를 이용한월1회 투여에 의해 CAGR 8.89%로 급속히 확대되고 있습니다. 일주일에 한 번의 일정으로 어려움을 겪고 있는 환자는월1일 처방으로 이동하여 시간을 자유롭게 하고 말초 카테터의 소모품을 줄입니다. 신속한 푸시는 주사기 구동의 기술이며, 완벽한 컨트롤과 최소한의 도구를 선호하는 성인에게 매력적입니다. 비교 연구에서는 이러한 절차에서 약동학이 열등하지 않은 것으로 보고되었으며, 의사는 환자의 라이프 스타일에 맞는 선택을 할 수 있게 되었습니다.

기기 제조업체도 병행하여 기술 혁신을 실시했습니다. 임상 평가 중 웨어러블 체내 주사기는 대용량과 눈에 띄지 않는 폼 팩터의 양립을 목표로 하고 있습니다. 스마트폰 앱은 주입 데이터를 기록하고 어드히어런스를 지원하는 알림을 푸시합니다. 증강현실을 통해 전달되는 교육 모듈은 초기 학습 곡선을 단축하고 시작 시 병원에서의 체어 시간을 단축합니다. 지역에 따라 실천 패턴은 다르다 : 북미에서는 모든 절차 메뉴가 도입되고, 유럽에서는 성인에 대한 촉진 요법이 점점 선호되고, 아시아태평양에서는 HYQVIA의 승인 후 대량 저압 주입이 가능한 신세대 펌프가 도입되고 있습니다. 전반적으로, 절차의 다양성은 피하 면역글로불린 시장의 지속적인 확장을 지원합니다.

지역 분석

북미는 매출액의 41.26%를 차지하지만, 이는 미국이 약 15만-20만 명의 원발성 면역결핍증 환자를 진단하고 있어 상용 플랜과 메디케어 모두에서 광범위한 재택 주입 급여를 유지하고 있기 때문입니다. 캐나다에서는 각 국가의 처방전에 따라 치료비가 상환되며 병원 및 지역 프로그램을 통해 제품이 제공됩니다. 최근의 메디케어의 규칙 변경에 의해 재택 수액의 간호 시간이 환불되게 되어, 한층 더 보급이 진행되고 있습니다. 미국을 중심으로 한 견고한 혈장 채취 인프라는 국내 공급을 보장하고 국제 충격을 완충합니다.

영국은 2025년 국내 혈장 자급률 25%에 달하며 2031년까지 30-35%를 목표로 하고 있습니다. 독일은 최대 분획 능력을 가지고 있으며, 프랑스, 이탈리아, 스페인은 국내 혈장 채취를 선호합니다. 유럽 의약품청은 HYQVIA의 집중 승인과 XEMBIFY의 범 EU 라벨 확대가 나타내는 대로 촉진 제제의 조기 심사를 지원하고 있습니다. COVID-19공급 중단은 전략적 혈장 비축에 대한 투자를 촉진하고 공중 보건과 산업 정책을 동기화시켰습니다.

아시아태평양은 CAGR 9.12%로 가장 급성장하고 있는 지역으로, 일본의 2024년 HYQVIA 승인과 중국 도시에서의 상환 확대가 뒷받침하고 있습니다. 호주 국가 혈액국(National Blood Authority)은 2개월에 한 번 재택 투여용 제품을 공급하고, 피하 제제를 표준 치료에 통합하고 있습니다. 한국은 바이오 의약품 생태계를 활용하여 현지 분획 프로젝트를 추진하고 인도네시아는 세계 최초의 혈장 시설을 위해 대내 투자를 유치했습니다. 과제로는 신흥 시장에서의 단편적인 규제 프레임워크이나 한정된 도너 네트워크 등을 들 수 있지만, 다국간의 의료안보 프로그램이 기술지원을 하고 있습니다. 적격 분획 플랜트의 기반이 확대됨에 따라 피하 면역글로불린 시장의 장기 성장을 위한 내구성있는 기반이 구축됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 원발성 면역결핍증(PID)의 유병률 증가

- IVIG에서 재택 SCIG 투여로의 전환

- 고령화와 만성질환 부담 증가

- 보험 상환과 혈장 채취 프로그램의 확대

- 히알루로니다제가 촉진하는 fSCIG의 대량 도입

- 플라즈마의 분산 조달에의 대처

- 시장 성장 억제요인

- 엄격한 규제 및 품질 요건

- 높은 치료비와 상환의 마찰

- 세계의 혈장 공급의 제약

- 대체품으로서의 새로운 FcRn 억제제 생물제제

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측(금액-USD)

- 용도별

- 일차성 면역결핍증

- 이차성 면역결핍증

- 만성 염증성 탈수초성 다발신경병증(CIDP)

- 다발성 운동신경병증(MMN)

- 기타 용도

- 투여 기술별

- 기존 펌프

- 신속 주입

- 촉진(fSCIG) 요법

- 최종 사용자별

- 병원

- 홈케어

- 전문 클리닉 및 주입 센터

- 기타

- 유통 채널별

- 병원 약국

- 소매 약국

- 온라인 약국

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Takeda Pharmaceutical Company Limited

- CSL Behring

- Grifols SA

- Octapharma AG

- Kedrion SpA

- Biotest AG

- Bio Products Laboratory(BPL)

- ADMA Biologics

- GC Pharma

- Sanquin

- LFB SA

- Emergent BioSolutions

- China Biologic Products

- Kamada Ltd.

- Argenx SE

- Octapharma Plasma Inc.(US)

- Intas Pharmaceuticals

- Bioplasma Argentina

- Bharat Serums & Vaccines

- Green Cross Health

제7장 시장 기회와 향후 전망

KTH 25.11.12The subcutaneous immunoglobulin market is valued at USD 10.53 billion in 2025 and is projected to reach USD 15.73 billion by 2030, advancing at an 8.35% CAGR.

Patient preference for self-managed therapy, improved infusion technologies, and payer support for home care together sustain a demand curve that remains comfortably above global plasma-collection capacity. Primary immunodeficiency continues to anchor demand because earlier diagnosis broadens the treated population, while neurological and hematologic conditions steadily push beyond niche status. Facilitated formulations extend the addressable base by compressing a month of therapy into one session, a feature that improves adherence and reduces indirect costs. Geographically, North America retains consumption leadership, yet the Asia-Pacific trajectory rises more steeply as Japan, China, and Australia clear new products and streamline reimbursement pathways. Manufacturers respond to chronic plasma scarcity with yield-enhancement processes, fractionation expansion, and partnerships that shorten supply chains.

Global Subcutaneous Immunoglobulin Market Trends and Insights

Growing Prevalence of Primary Immunodeficiency Disorders Drives Market Expansion

Improved screening algorithms embedded in large electronic-health-record systems now identify 6 in 10,000 individuals with inborn errors of immunity, well above earlier assumptions. More accurate epidemiology means physicians prescribe replacement therapy earlier, which lengthens a patient's lifetime exposure to subcutaneous products. Hospital data place the average cost of admission for severe infections at USD 122,739, a level that persuades insurers to fund preventive immunoglobulin therapy. Parallel discoveries of immune deficits in Down syndrome and other syndromic conditions widen the treated population. COVID-19 experience further supports prophylactic IgG use for vulnerable groups as they transition from pandemic to endemic risk. Together these factors elevate baseline demand and stabilize year-on-year volume growth for the subcutaneous immunoglobulin market.

Patient Preference Accelerates IVIG-to-SCIG Migration

Survey data show that 82% of patients prefer subcutaneous delivery and 84% favor home administration, citing autonomy and reduced travel burden. Real-world studies confirm equal efficacy alongside fewer systemic reactions, particularly in chronic neuromuscular conditions. Health-economic analyses reveal that nurses spend 35 hours per patient annually on subcutaneous support versus significantly higher labor for intravenous regimens. Pre-filled syringes, manual push options, and small portable pumps remove the technical hurdles that once confined therapy to infusion suites. These combined conveniences channel a steady stream of new starters directly into the subcutaneous immunoglobulin market.

Global Plasma Supply Constraints Challenge Market Growth Sustainability

Every liter of plasma requires 7-12 months of fractionation before a dose reaches the patient, so even modest demand increments strain inventories. Governments act: the United Kingdom moved from 0% to 25% plasma self-sufficiency by 2025 and targets 30-35% by 2031. Manufacturers upgrade processes, and ADMA Biologics filed for a 20% yield enhancement that uses optimized chromatography and virus-filtration steps. Yet collection policy changes in major donor countries still cap growth, and regional shortfalls appear first in developing economies with limited fractionation capacity. The subcutaneous immunoglobulin market therefore relies on continuous innovation to stretch each liter of plasma further.

Other drivers and restraints analyzed in the detailed report include:

- Aging Demographics and Chronic Disease Burden Expand Treatment Population

- Hyaluronidase-Facilitated Therapy Transforms Administration Paradigms

- FcRn-Inhibitor Biologics Emerge as Competitive Threat

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Primary immunodeficiency held 58.67% revenue in 2024 and is advancing at an 8.96% CAGR, underpinning the largest slice of the subcutaneous immunoglobulin market. Greater physician awareness, newborn screening pilots, and genomic testing converge to catch patients earlier, which extends therapy lifespan. Secondary immunodeficiency linked to chemotherapy, stem-cell transplant, and antirheumatic medications adds a sizeable cohort that previously relied on hospital IVIG infusions. Neurological applications are rising fastest because chronic inflammatory demyelinating polyneuropathy and multifocal motor neuropathy have secured guideline support for maintenance dosing. Regulatory clearance of GAMMAGARD LIQUID for CIDP in adults widened payer recognition in 2025. Emerging research on autoimmune encephalitis and stiff-person syndrome further enlarges the potential pool. Precision-medicine initiatives use serum biomarker panels and machine-learning algorithms to stratify patients for subcutaneous versus intravenous routes. This data-guided matching optimizes resource allocation and improves adherence, ensuring that subcutaneous immunoglobulin market growth remains patient-centric.

Segment diversity secures resilience. When plasma scarcity limits volume allocation, manufacturers can redistribute supply toward high-value neurology segments without abandoning core immunodeficiency users. Hospitals, clinics, and home-care services align educational content to reflect the broader indication mix, reducing mis-administration risks. As the treated base widens, real-world evidence networks collect safety, efficacy, and quality-of-life outcomes that feed back into payer dossiers. The feedback loop strengthens contract negotiations and secures formulary placement. Overall, application breadth transforms the subcutaneous immunoglobulin industry into a versatile treatment platform rather than a single-use product line.

Conventional pump infusion retained 48.67% revenue share in 2024 on the strength of entrenched clinical protocols and broad device availability. The method remains favored for children and patients with limited manual dexterity because programmable flow rates minimize infusion-site discomfort. That said, facilitated therapy is scaling quickly at an 8.89% CAGR on the back of hyaluronidase-enabled monthly dosing. Patients who struggled with weekly schedules migrate to one-day-per-month regimens, freeing time and cutting peripheral-catheter consumables. Rapid push, a syringe-driven manual technique, appeals to adults who prefer complete control and minimalist equipment. Comparative studies report non-inferior pharmacokinetics across these techniques, empowering physicians to tailor choices to patient lifestyle.

Device firms innovate in parallel. Wearable on-body injectors under clinical evaluation aim to combine large-volume capacity with discreet form factors. Smart-phone apps log infusion data and push reminders that support adherence. Training modules delivered through augmented reality reduce the initial learning curve and shorten hospital chair time at initiation. Regional practice patterns differ: North America deploys the full menu of techniques, Europe increasingly favors facilitated therapy for adults, and Asia-Pacific installs new-generation pumps capable of high-volume, low-pressure infusions following HYQVIA approval. Collectively, technique diversity underpins sustained depth in the subcutaneous immunoglobulin market.

The Subcutaneous Immunoglobulin Market Report is Segmented by Application (Primary Immunodeficiency Diseases, Secondary Immunodeficiency, and More), Administration Technique (Conventional Pump, Rapid Push, and More), End User (Hospitals, Home Care Settings, and More), and Geography (North America, Europe, and More). Distribution Channel (Hospital Pharmacies, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America owns 41.26% revenue because the United States diagnoses roughly 150,000-200,000 primary immunodeficiency patients and maintains extensive home-infusion benefits under both commercial plans and Medicare. Canada reimburses therapy through provincial formularies and delivers product via hospital or community programs, while Mexico's public-sector tenders are enlarging to include subcutaneous options. Recent Medicare rule changes that reimburse nursing time for home infusions further strengthen adoption. Robust plasma-collection infrastructure, predominantly in the United States, guarantees local supply and buffers international shocks.

Europe positions itself as a self-sufficient producer: the United Kingdom reached 25% domestic plasma self-sufficiency in 2025 and targets 30-35% by 2031. Germany operates the largest fractionation capacity, while France, Italy, and Spain prioritize national plasma-collection drives. The European Medicines Agency supports accelerated reviews for facilitated formulations, as evidenced by HYQVIA's centralized authorization and XEMBIFY's pan-EU label expansion. COVID-19 supply disruptions prompted investment in strategic plasma reserves, synchronizing public health and industrial policy.

Asia-Pacific is the fastest-growing region at 9.12% CAGR, prompted by Japan's 2024 HYQVIA approval and widening reimbursement in urban China. Australia's National Blood Authority supplies product for home administration every two months, embedding subcutaneous formulations into standard care. South Korea leverages its biopharmaceutical ecosystem to push local fractionation projects, while Indonesia attracted inward investment for a first-of-its-kind plasma facility. Challenges include fragmented regulatory frameworks and limited donor networks in emerging markets, but multilateral health-security programs supply technical assistance. The expanding base of qualified fractionation plants lays a durable foundation for the long-term growth of the subcutaneous immunoglobulin market.

- Takeda Pharmaceuticals

- CSL Behring

- Grifols

- Octapharma

- Kedrion Biopharma

- Biotest

- Bio Products Laboratory (BPL)

- ADMA Biologics

- GC Biopharma

- Sanquin

- LFB SA

- Emergent Bio Solutions

- China Biologic Products

- Kamada Ltd.

- Argenx SE

- Octapharma Plasma Inc. (US)

- Intas Pharmaceuticals

- Bioplasma Argentina

- Bharat Serums & Vaccines

- Green Cross Health

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Prevalence of Primary Immunodeficiency Disorders (PID)

- 4.2.2 Shift from IVIG to Home-based SCIG Administration

- 4.2.3 Aging Population & Rising Chronic Disease Burden

- 4.2.4 Expanding Reimbursement & Plasma-collection Programs

- 4.2.5 Hyaluronidase-facilitated High-volume fSCIG Adoption

- 4.2.6 Decentralised Plasma Sourcing Initiatives

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory & Quality Requirements

- 4.3.2 High Therapy Cost & Reimbursement Friction

- 4.3.3 Global Plasma Supply Constraints

- 4.3.4 Emerging FcRn-inhibitor Biologics as Substitutes

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value -USD)

- 5.1 By Application

- 5.1.1 Primary Immunodeficiency

- 5.1.2 Secondary Immunodeficiency

- 5.1.3 Chronic Inflammatory Demyelinating Polyneuropathy (CIDP)

- 5.1.4 Multifocal Motor Neuropathy (MMN)

- 5.1.5 Other Applications

- 5.2 By Administration Technique

- 5.2.1 Conventional Pump

- 5.2.2 Rapid Push

- 5.2.3 Facilitated (fSCIG) Therapy

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Homecare Settings

- 5.3.3 Specialty Clinics & Infusion Centers

- 5.3.4 Others

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Takeda Pharmaceutical Company Limited

- 6.3.2 CSL Behring

- 6.3.3 Grifols SA

- 6.3.4 Octapharma AG

- 6.3.5 Kedrion SpA

- 6.3.6 Biotest AG

- 6.3.7 Bio Products Laboratory (BPL)

- 6.3.8 ADMA Biologics

- 6.3.9 GC Pharma

- 6.3.10 Sanquin

- 6.3.11 LFB SA

- 6.3.12 Emergent BioSolutions

- 6.3.13 China Biologic Products

- 6.3.14 Kamada Ltd.

- 6.3.15 Argenx SE

- 6.3.16 Octapharma Plasma Inc. (US)

- 6.3.17 Intas Pharmaceuticals

- 6.3.18 Bioplasma Argentina

- 6.3.19 Bharat Serums & Vaccines

- 6.3.20 Green Cross Health