|

시장보고서

상품코드

1851228

미생물 검사 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Microbiology Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

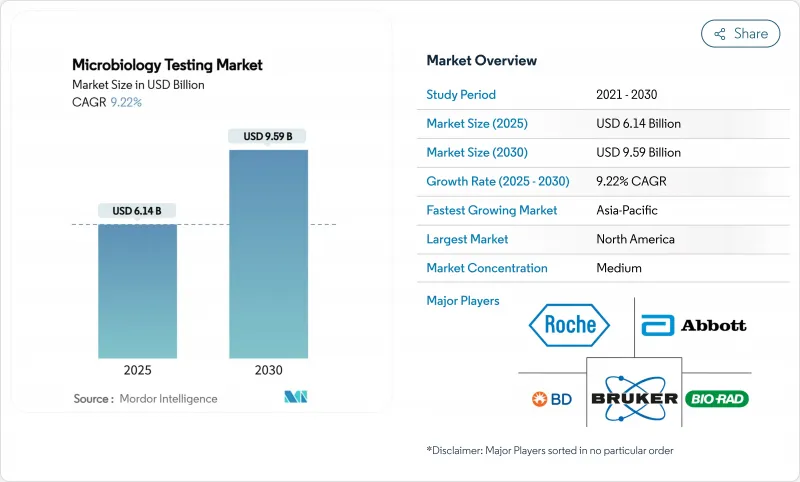

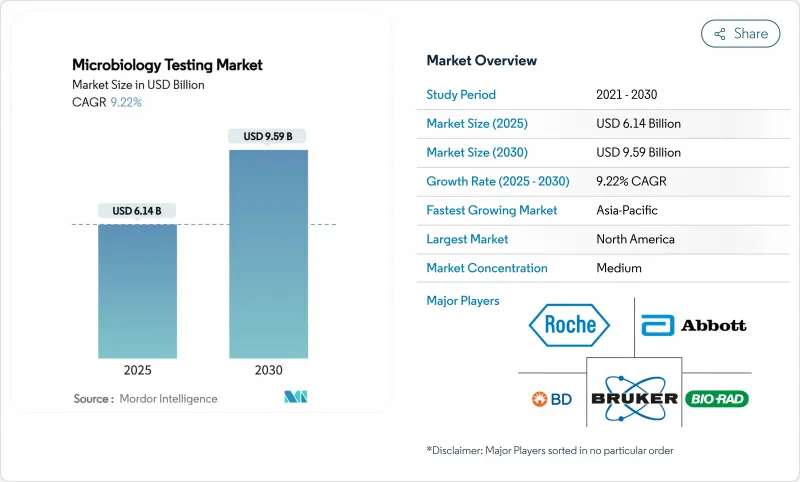

미생물 검사 시장 규모는 2025년에 61억 4,000만 달러에 달하고, CAGR 9.22%를 나타내, 2030년에는 95억 9,000만 달러까지 수익을 올릴 것으로 예측되고 있습니다.

보다 신속한 병원체 식별에 대한 임상 수요, 항균제 내성의 확산, 실험실 자동화의 가속화가 가장 강력한 성장 촉임베디드니다. 각국 정부는 의약품, 식품, 퍼스널케어공급망에 대한 규제 감독을 강화해, 일상적인 미생물 품질 관리의 빈도와 범위를 인상하고 있습니다. 동시에 AI를 활용한 질량 분석계와 분자 플랫폼은 납기를 단축하고, 병원은 며칠이 아닌 몇 시간 이내에 표적 치료를 개시할 수 있게 됩니다. 두 자리 결원률에 직면한 실험실은 만성적 인원 부족에 대한 가장 현실적인 해결책으로 실험실의 완전 자동화를 고려합니다. 신속 진단에 연결성, 분석 및 원격 지원 기능을 결합할 수 있는 제조업체는 미생물 검사 시장에서 미래 입찰에서 불균형한 점유율을 획득할 것으로 보입니다.

세계의 미생물 검사 시장 동향과 인사이트

진단 기술과 자동화의 진보

실험실 자동화는 AI 가이드가 있는 이미징 시스템과 로봇의 조합을 통해 미생물학 워크플로우를 재구성합니다. MALDI-TOF와 같은 질량분석 플랫폼은 2일이 걸린 수작업 대신 몇 분 안에 생물종 수준을 확인할 수 있는 머신러닝 모델을 통합합니다. 완전 자동화된 '다크라보'는 인력 부족이나 COVID-19와 같은 위기 시에도 소등 변화를 조작하여 필수적인 검사를 계속합니다. 병원 정보 시스템과의 상호 운용성은 원활한 데이터 흐름을 가능하게 하며 감염 관리 대시보드 및 항균제 관리 경고를 지원합니다. 하드웨어, 시약 및 클라우드 기반 애널리틱스를 서비스 계약에 번들하는 공급업체는 소유 비용을 낮추면서 가동 시간을 개선하고 미생물 검사 시장에서의 혜택의 매력을 높입니다.

감염증 증가와 항균제 내성

약물 내성 병원체가 증가함에 따라, 임상의는 환자의 입원으로부터 중요한 시간 내에 확인 및 내성 마커를 제공할 수 있는 배양에 의존하지 않는 검사를 채용할 필요가 있습니다. 미국만으로도 건강관리 관련 감염으로 연간 200억 달러 이상의 비용이 들고 있으며, 광역 항생제의 과도한 사용을 막는 신속 진단의 도입이 병원에의 압력이 되고 있습니다. 모기가 매개하는 감염이 기후의 영향을 받아 확대되는 동안 공존하는 아르보바이러스를 감별할 수 있는 분자 패널에 대한 기본적인 수요가 높아지고 있습니다. 표적 치료가 사망률과 입원 기간을 감소시킨다는 증거는 1시간의 멀티플렉스 PCR 분석에 대한 관심을 높입니다. 정책 입안자는 적시에 미생물학적 데이터에 의존하는 감시 네트워크에 자금을 돌리고, 그 결과 미생물 검사 시장 전체의 고도 시스템의 설치 기반이 확대됩니다.

높은 설비 투자 및 운영 비용

실험실 자동화 시스템은 시설당 200만 달러에서 500만 달러의 초기 투자가 필요하며 소규모 지역 병원과 독립 실험실이 클리어하기 위해 고생하는 장애물입니다. MALDI-TOF 장비는 검사당 비용을 줄이지만 여전히 하드웨어 및 연간 데이터베이스 라이선스 비용에 50만 달러 이상을 요구합니다. 분자 시약 팩의 가격은 패널 당 100-200 달러로 배양 방법의 10-20 달러의 소모품을 능가합니다. 시설은 관리되는 환경실, 중복 전원 공급 장치, 특수 IT 인프라에도 예산을 부과해야 합니다. 수량 기준 할인이 없으면 신흥 시장 실험실의 대부분은 차세대 플랫폼에서 잠겨 남아 시장 세분화 시장의 진입 가능한 부문을 좁힐 것입니다.

부문 분석

임상진단제는 2024년 매출액의 31.34%를 차지했는데, 이는 병원이 당일 병원체를 확인하고 헬스케어 관련 감염을 억제하는 것을 우선하고 있음을 반영했습니다. 의약품 품질 관리는 cGMP 규정에 따라 무균 보증 시험 후에만 배치 릴리스가 의무화되었기 때문에 금액에서 2위를 차지했습니다. 식음료 가산업자는 여러 체크포인트에서 병원체 스크리닝을 의무화하는 위험 분석 중요 관리점(Hazard Analysis and Critical Control Point) 기준을 채택했습니다. 환경 모니터링은 보다 엄격한 폐수 및 복구 규칙으로 꾸준히 확대되고 있습니다.

화장품 검사는 CAGR 11.45%로 가장 급속히 확대되었는데, 이는 EU 규칙 1223/2009가 안전성 서류를 의무화하고 있으며, 방부제가 적은 '클린 라벨' 처방으로의 변화가 오염 위험을 높이고 있기 때문입니다. 브랜드가 식물 유래 성분을 추진함에 따라 미생물 장애물이 상승하고 도전 시험 및 방부제 효능 시험에 대한 수요를 촉진하고 있습니다. 퍼스널케어 미생물학에 특화된 수탁 실험실이 새로운 아웃소싱 계약을 획득하여 미생물 검사 시장 규모 내에서 발자취를 확대합니다.

시약 및 소모품은 2024년 지출액의 73.56%를 차지했습니다. 이는 배양 및 분자 생물학적 검사를 할 때마다 배지, 패널, 디스크, 카트리지가 소비되어 안정적인 보충 사이클이 확보되기 때문입니다. COVID-19 위기 때 품절의 두려움은 조달 팀이 공급자의 다양화와 재고 완충의 건설을 확신하게 했습니다. 멀티플렉스 호흡기 패널, 발색성 배지, AST 카드는 미생물 검사 시장의 제조 업체들에게 현금 흐름 기반을 지원하는 주요 수익원으로 계속되고 있습니다.

실험실이 워크플로우 시간을 단축하는 높은 처리량 스트리커, 인큐베이터 및 질량 분석기로 업그레이드함에 따라 장비 매출은 11.89%의 연평균 복합 성장률(CAGR)로 증가합니다. 2024년에만 550대 이상의 VITEK MS PRIME 시스템이 도입되었는데, 이는 정확성을 희생하지 않고 식별을 가속화하려는 수요를 반영했습니다. LIS 미들웨어와 결합된 자동 민감성 플랫폼은 실시간 보고 및 항균제 관리에 대한 알림을 제공합니다. 서비스 계약 및 소프트웨어 라이선스는 하드웨어 판매에 연금층을 추가하여 평생 고객 가치를 높입니다.

지역 분석

북미는 2024년 매출의 42.43%를 차지하며, 고급 병원 인프라, 감염 제어 가이드라인의 의무화, 신규 진단약에 대한 명확한 규제 경로에 지지되었습니다. 식품안전근대화법은 광범위한 병원체 모니터링을 의무화하고 있으며 식품 가산업자와 기준실 수요를 자극하고 있습니다. 신속 진단을 상환하는 연방 정부 프로그램은 프리미엄 분자 패널의 비즈니스 사례를 강화하고이 지역의 미생물 검사 시장의 리더십을 강화하고 있습니다.

유럽은 2위를 차지하고 있으며 식품에 대해서는 규칙 2073/2005에 따라 엄격한 기준이 유지되고 의약품에 대해서는 cGMP의 틀이 충분히 강화되고 있습니다. 독일, 프랑스, 북유럽 국가가 설치된 자동화 라인의 대부분을 차지하고, 규제1223/2009에 의해 화장품 검사 실험실은 유럽 전역에서 바쁘다. 유럽 질병 예방 관리 센터(European Centre for Disease Prevention and Control)를 통한 공동 감시는 아웃 브레이크 대응의 조화를 도모해 간접적으로 선진 검사 시스템의 범 지역적 도입을 촉진하고 있습니다.

아시아태평양은 중국, 인도, 동남아시아 국가들이 공중 보건 회복력을 지원하는 검사 네트워크에 자본을 투입하고 있기 때문에 CAGR 10.54%로 가장 급성장하고 있는 지역입니다. 생물 제제와 백신 제조의 대규모 확장은 환경 모니터링과 무균 시험의 안정적인 요구를 야기합니다. POC(Point of Care) 분자검사장치를 재빨리 도입한 일본 병원은 신속 진단의 업무상의 이점을 소개하고 지역의 동업기관에 추종을 촉구합니다. 인프라가 정비됨에 따라, 이전에는 충분한 서비스를 받지 못했던 지방 시장이 개척되어, 지역 전체에서 대응 가능한 미생물 검사 시장 규모가 확대됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 진단 기술과 자동화의 진보

- 감염증 증가와 항균제 내성

- 공적·민간 헬스케어 자금의 확대

- 신속 검사 및 POC(Point-of-Care) 검사 솔루션에 대한 수요 증가

- 제품의 안전성과 품질에 관한 엄격한 규제 기준

- 의약품, 식품, 환경 검사에 있어서 용도의 다양화

- 시장 성장 억제요인

- 높은 설비 투자 및 운영 비용

- 신규 검사의 상환과 가격 설정 과제

- 숙련된 임상검사기사의 부족

- 중요 시약 및 소모품 공급망 혼란

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 용도별

- 임상 진단

- 의약품 제조 품질 관리

- 식음료 검사

- 환경 모니터링

- 화장품 검사

- 산업품질관리

- 제품별

- 기기 및 장비

- 시약 및 소모품

- 소프트웨어 및 서비스

- 기술별

- 배양 기반 검사

- 분자진단(PCR/NAAT)

- 질량 분석법(MALDI-TOF)

- 신속/자동화 방법

- 바이오센서 및 나노 기반 분석

- 최종 사용자별

- 병원 및 진단실험실

- 제약 및 바이오테크놀러지 기업

- 식음료 기업

- CRO 및 CMO

- 학술 및 연구 기관

- 환경 시험소

- 화장품 및 퍼스널케어 연구소

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Bio-Rad Laboratories Inc.

- Abbott Laboratories

- Becton Dickinson & Company

- F. Hoffmann-La Roche Ltd

- Bruker Corporation

- Hologic Inc.

- Danaher Corp(Cepheid)

- bioMerieux SA

- Thermo Fisher Scientific Inc.

- Agilent Technologies Inc.

- Merck KGaA

- Shimadzu Corporation

- NEOGEN Corporation

- Charles River Laboratories Intl. Inc.

- QIAGEN NV

- Siemens Healthineers AG

- Lonza Group AG

- QuidelOrtho Corporation

- 3M Company

- Luminex Corp(DiaSorin)

- Eurofins Scientific

- Beckman Coulter MicroScan

제7장 시장 기회와 향후 전망

KTH 25.11.12The microbiology testing market size reached USD 6.14 billion in 2025 and is forecast to register a CAGR of 9.22%, lifting revenue to USD 9.59 billion by 2030.

Clinical demand for faster pathogen identification, the spread of antimicrobial resistance, and accelerating laboratory automation are the strongest growth catalysts. Governments have tightened regulatory oversight of pharmaceutical, food, and personal-care supply chains, which raises the frequency and scope of routine microbial quality control. At the same time, AI-enabled mass-spectrometry and molecular platforms shorten turnaround times, allowing hospitals to start targeted therapy within hours instead of days. Laboratories facing double-digit vacancy rates view total laboratory automation as the most practical remedy for chronic staffing shortages. Manufacturers that can combine rapid diagnostics with connectivity, analytics, and remote-support features will capture a disproportionate share of future tenders in the microbiology testing market.

Global Microbiology Testing Market Trends and Insights

Advancements in Diagnostic Technologies and Automation

Laboratory automation reshapes microbiology workflows by pairing robotics with AI-guided imaging systems that cut plating and reading times by around 40%, a clear benefit when vacancy rates in clinical labs hover near 25%. Mass-spectrometry platforms such as MALDI-TOF now integrate machine-learning models capable of species-level identification in minutes, replacing manual techniques that once required up to two days. Fully automated "dark labs" operate lights-out shifts to keep essential testing running during staffing shortages or crises like COVID-19. Interoperability with hospital information systems enables seamless data flow that supports infection-control dashboards and antimicrobial-stewardship alerts. Vendors that bundle hardware, reagents, and cloud-based analytics under service contracts improve uptime while lowering ownership costs, enhancing the attractiveness of their offers in the microbiology testing market.

Growing Incidence of Infectious Diseases and Antimicrobial Resistance

Rising drug-resistant pathogens push clinicians to adopt culture-independent tests that can deliver identification and resistance markers inside the first critical hours of patient admission. Healthcare-associated infections in the United States alone cost more than USD 20 billion annually, intensifying pressure on hospitals to deploy rapid diagnostics that prevent broad-spectrum antibiotic overuse. Climate-driven expansion of mosquito-borne diseases increases the baseline demand for molecular panels that can differentiate co-circulating arboviruses. Evidence that targeted therapy lowers mortality and length of stay amplifies interest in one-hour multiplex PCR assays. Policy makers channel funding toward surveillance networks that rely on timely microbiology data, which in turn enlarges the installed base of advanced systems across the microbiology testing market.

High Capital Investment and Operational Costs

Total laboratory automation systems require upfront outlays of USD 2-5 million per site, a hurdle that smaller community hospitals and independent labs struggle to clear. MALDI-TOF instruments cut per-test costs but still demand more than USD 500,000 for hardware plus annual database licensing fees. Molecular reagent packs priced at USD 100-200 per panel dwarf the USD 10-20 consumable spend of culture methods, limiting routine use in low-volume settings. Facilities must also budget for controlled-environment rooms, redundant power, and specialized IT infrastructure. Without volume-based discounts, many emerging-market labs remain locked out of next-generation platforms, constraining the reachable segment of the microbiology testing market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Public and Private Healthcare Funding

- Rising Demand for Rapid and Point-of-Care Testing Solutions

- Shortage of Skilled Laboratory Personnel

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clinical diagnostics delivered 31.34% of 2024 revenue, reflecting hospitals' priority to curtail healthcare-associated infections with same-day pathogen confirmation. Pharmaceutical-quality control ranked second in value because cGMP rules obligate batch release only after sterile assurance testing. Food and beverage processors adopted Hazard Analysis and Critical Control Point standards that mandate pathogen screening at multiple checkpoints. Environmental monitoring tract steadily due to stricter wastewater and remediation rules.

Cosmetic testing posts the quickest expansion at an 11.45% CAGR as EU Regulation 1223/2009 compels safety dossiers, and the shift toward preservative-light "clean label" formulas raises contamination risk. As brands promote plant-based ingredients, microbial hurdles climb, driving demand for challenge testing and preservative-efficacy studies. Contract labs specializing in personal-care microbiology capture new outsourcing contracts, enlarging their footprint within the microbiology testing market size.

Reagents and consumables controlled 73.56% of 2024 spending because every culture or molecular run consumes media, panels, discs, or cartridges, ensuring steady replenishment cycles. Stock-out scares during the COVID-19 crisis convinced procurement teams to diversify suppliers and build inventory buffers. Multi-plex respiratory panels, chromogenic media, and AST cards remain staple revenue generators, anchoring the cash-flow base for manufacturers in the microbiology testing market.

Instrumentation revenue rises at an 11.89% CAGR as laboratories upgrade to high-throughput streakers, incubators, and mass-spectrometry analyzers that compress workflow times. More than 550 VITEK MS PRIME systems were installed in 2024 alone, reflecting demand for faster identification without sacrificing accuracy. Automated susceptibility platforms that pair with LIS middleware unlock real-time reporting and antimicrobial-stewardship notifications. Service contracts and software licenses add an annuity layer to hardware sales, enhancing lifetime customer value.

The Microbiology Testing Market Report is Segmented by Application (Clinical Diagnostics, and More), Product (Instruments & Equipment, and More), Technology (Culture-Based Testing, and More), End User (Hospitals & Diagnostic Laboratories, Pharmaceutical & Biotech Companies, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 42.43% of 2024 revenue, underpinned by advanced hospital infrastructure, mandatory infection-control guidelines, and a clear regulatory pathway for novel diagnostics. The Food Safety Modernization Act obliges extensive pathogen monitoring, stimulating demand from food processors and reference labs. Federal programs that reimburse rapid diagnostics strengthen the business case for premium molecular panels, reinforcing leadership of the microbiology testing market in the region.

Europe ranks second and upholds stringent standards under Regulation 2073/2005 for foodstuffs and the well-enforced cGMP framework for pharmaceuticals. Germany, France, and the Nordics account for the bulk of installed automation lines, and Regulation 1223/2009 keeps cosmetic-testing laboratories busy across the bloc. Collaborative surveillance through the European Centre for Disease Prevention and Control harmonizes outbreak response, indirectly encouraging pan-regional adoption of advanced testing systems.

Asia-Pacific is the fastest-growing territory with a 10.54% CAGR as China, India, and Southeast Asian countries pour capital into laboratory networks that underpin public-health resilience. Massive expansions in biologics and vaccine manufacturing create steady need for environmental monitoring and sterility testing. Japanese hospitals, early adopters of point-of-care molecular devices, showcase the operational gains of rapid diagnostics, prompting regional peer institutions to follow suit. As infrastructure improves, previously underserved rural markets open, enlarging the total addressable microbiology testing market size across the region.

- Bio-Rad Laboratories

- Abbott Laboratories

- Beckton Dickinson

- Roche

- Bruker

- Hologic

- Danaher Corp (Cepheid)

- bioMerieux

- Thermo Fisher Scientific

- Agilent Technologies

- Merck

- Shimadzu

- Neogen

- Charles River Laboratories Intl. Inc.

- QIAGEN

- Siemens Healthineers

- Lonza Group

- QuidelOrtho

- 3M

- Luminex Corp (DiaSorin)

- Eurofins

- Beckman Coulter MicroScan

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advancements in Diagnostic Technologies and Automation

- 4.2.2 Growing Incidence of Infectious Diseases and Antimicrobial Resistance

- 4.2.3 Expansion of Public and Private Healthcare Funding

- 4.2.4 Rising Demand for Rapid and Point-of-Care Testing Solutions

- 4.2.5 Stringent Regulatory Standards for Product Safety and Quality

- 4.2.6 Diversifying Applications in Pharmaceutical, Food, and Environmental Testing

- 4.3 Market Restraints

- 4.3.1 High Capital Investment and Operational Costs

- 4.3.2 Reimbursement and Pricing Challenges For Novel Tests

- 4.3.3 Shortage of Skilled Laboratory Personnel

- 4.3.4 Supply Chain Disruptions for Critical Reagents and Consumables

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Application

- 5.1.1 Clinical Diagnostics

- 5.1.2 Pharmaceutical Manufacturing QC

- 5.1.3 Food & Beverage Testing

- 5.1.4 Environmental Monitoring

- 5.1.5 Cosmetic Testing

- 5.1.6 Industrial Quality Control

- 5.2 By Product

- 5.2.1 Instruments & Equipment

- 5.2.2 Reagents & Consumables

- 5.2.3 Software & Services

- 5.3 By Technology

- 5.3.1 Culture-based Testing

- 5.3.2 Molecular Diagnostics (PCR/NAAT)

- 5.3.3 Mass Spectrometry (MALDI-TOF)

- 5.3.4 Rapid/Automated Methods

- 5.3.5 Biosensors & Nano-based Assays

- 5.4 By End User

- 5.4.1 Hospitals & Diagnostic Laboratories

- 5.4.2 Pharmaceutical & Biotech Companies

- 5.4.3 Food & Beverage Companies

- 5.4.4 CROs & CMOs

- 5.4.5 Academic & Research Institutes

- 5.4.6 Environmental Testing Labs

- 5.4.7 Cosmetics & Personal-Care Labs

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Bio-Rad Laboratories Inc.

- 6.3.2 Abbott Laboratories

- 6.3.3 Becton Dickinson & Company

- 6.3.4 F. Hoffmann-La Roche Ltd

- 6.3.5 Bruker Corporation

- 6.3.6 Hologic Inc.

- 6.3.7 Danaher Corp (Cepheid)

- 6.3.8 bioMerieux SA

- 6.3.9 Thermo Fisher Scientific Inc.

- 6.3.10 Agilent Technologies Inc.

- 6.3.11 Merck KGaA

- 6.3.12 Shimadzu Corporation

- 6.3.13 NEOGEN Corporation

- 6.3.14 Charles River Laboratories Intl. Inc.

- 6.3.15 QIAGEN N.V.

- 6.3.16 Siemens Healthineers AG

- 6.3.17 Lonza Group AG

- 6.3.18 QuidelOrtho Corporation

- 6.3.19 3M Company

- 6.3.20 Luminex Corp (DiaSorin)

- 6.3.21 Eurofins Scientific

- 6.3.22 Beckman Coulter MicroScan

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment