|

시장보고서

상품코드

1851235

오토클레이브 기포 콘크리트(AAC) : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Autoclaved Aerated Concrete (AAC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

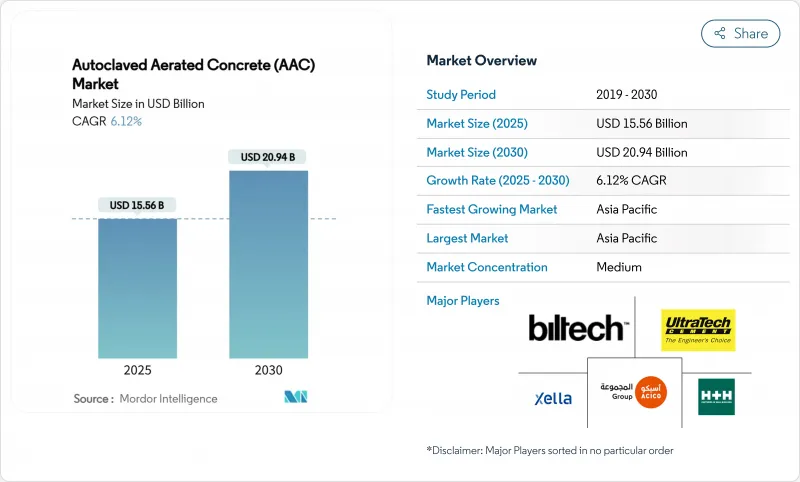

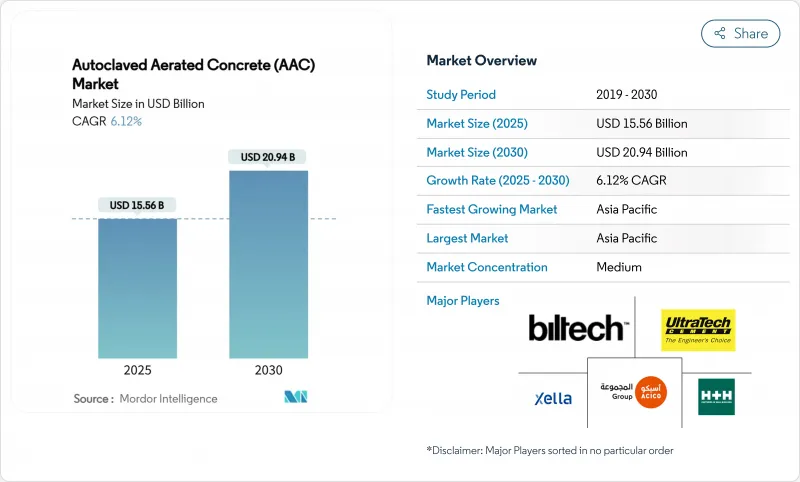

2025년 오토클레이브 기포 콘크리트(AAC) 시장 규모는 155억 6,000만 달러로 추정되고, 예측 기간(2025-2030년)의 CAGR은 6.12%로, 2030년에는 209억 4,000만 달러에 달할 것으로 예상됩니다.

성장의 원동력이 되는 것은 그린빌딩의 의무화, 내진구조에 대한 수요가 높아지고, 모듈건축의 급속한 보급 등으로, 이들 모두가 AAC의 경량으로 에너지 효율이 높은 특성을 두드러지게 하고 있습니다. 전통적인 벽돌의 주류는 여전히 블록이지만, 조립식으로 인해 프로젝트 일정이 검토됨에 따라 패널도 기세를 늘리고 있습니다. 아시아태평양은 도시화와 인프라 정비를 배경으로 세계 수요의 절반 가까이를 차지하고 있으며, 북미와 유럽은 엄격한 에너지 규제와 내진 규제를 배경으로 하고 있습니다. 제조업체는 수요 급증에 대응하고 비용 구조를 개선하고 지역 공급망을 강화하기 위해 생산 능력을 확대하고 공장을 자동화하고 있습니다.

세계의 오토클레이브 기포 콘크리트(AAC) 시장 동향과 인사이트

신축·개축 공사 수요 증가

신흥경제국에서의 주택 및 상업시설의 착공 급증으로 기초하중을 줄이고 프로젝트 사이클을 단축하는 경량 소재가 필수적입니다. AAC는 자중을 30-40% 삭감하여 기초의 슬림화와 바닥에서 바닥으로의 빠른 이동을 가능하게 합니다. 인도에서는 주택 건설이 활발해 국내 제조업체인 BigBloc Construction사는 도시의 주택 인가 증가에 대응하기 위해 생산 능력을 확대하고 있습니다. AAC의 정밀한 블록은 구조선을 개조하지 않고도 개조를 간소화할 수 있기 때문에 개조 계획도 AAC를 선호합니다. 4시간 내화성능은 상업시설의 개조에 있어서 컴플라이언스를 높이고, 그 방 곰팡이 매트릭스는 습기찬 기후로 어필합니다. 이러한 요인은 오토클레이브 기포 콘크리트(AAC) 시장의 지속적인 성장을 지원합니다.

엄격한 그린 빌딩 규정과 LEED 채용

구현 탄소의 억제를 목적으로 한 정책은 전 세계적으로 재료의 선택을 바꾸고 있습니다. 미국 정부는 지속 가능한 재료 벤치마크를 위해 1억 6,000만 달러의 자금을 제공하고 AAC의 도입을 명확히 장려하고 있습니다. EPA(미국 환경보호청)의 2024년 저탄소 라벨은 제조업체에게 기후 변화에 대한 우위를 정량화하는 명확한 경로를 제공하여 공공 프로젝트의 입찰 점수를 향상시켰습니다. HH UK는 EU의 탈탄소화 목표에 따라 2050년까지 인터넷 제로 운영을 목표로 하고 있습니다. 두께 200mm로 R값 1.43의 AAC는 10-20%의 운용 에너지 삭감을 실현하고 리사이클 플라이 애쉬를 내장하고 있어 서큘러 이코노미의 기준을 충족하고 있습니다.

높은 초기 비용과 점토 및 콘크리트 블록의 비교

건설업체가 라이프사이클 절감보다 구매가격을 선호하는 경우 가격이 비싸다는 인식이 AAC의 보급을 방해합니다. 그러나 인도의 주요 도시에서는 최근 전통적인 붉은 벽돌 가격이 AAC보다 약 20% 높아졌으며 구매자는 가벼운 대체품으로 흐르게 되었습니다. 2025년 관세 인상으로 철강은 10-25%, 콘크리트는 3-7% 상승하여 AAC의 비용차가 줄어들었습니다. 지역에 따라서는 한정된 공장 밖에 없기 때문에 납품 가격이 15-20% 상승합니다. 30%의 에너지 비용 절감과 노동력 감소를 강조하는 교육 캠페인은 총 소유 비용에 중점을 둔 조달 결정을 점차 검토하고 있습니다.

부문 분석

블록은 2024년 매출의 54.78%를 차지하며 수십년에 걸친 계약자의 익숙함과 광범위한 유통망을 반영했습니다. 이와 병행하여, 건축업자가 조립식 외벽에 축발을 옮기고 있기 때문에 패널은 2030년까지 7.81%의 연평균 복합 성장률(CAGR)을 기록합니다. 패널 붐은 건설 업계의 산업화 추진을 구현하고 있습니다. 공장에서 절단된 모듈이 현장에서 바로 사용할 수 있는 상태로 도착하므로 폐기물이 줄어들고 일정이 단축됩니다. 고층 주택에 패널이 선호되는 것은 피팅가 적기 때문에 열외피가 조밀해져 침입 손실이 적어지기 때문입니다.

특히 노동력이 풍부하고 현장 기술이 우위를 차지하는 시장에서는 저층 주택의 중심은 여전히 블록 부문입니다. 그러나 패널의 혁신은 머무는 곳을 모릅니다. 보강된 벽 패널이 내하중 책무를 담당하게 되어, 열전도율 0.11 W/mK의 지붕 모듈이 제로 에너지 건축의 목표를 달성하고 있습니다. 자동화된 제재 라인과 로봇 핸들링은 패널 제조 비용을 절감하고 오토클레이브 기포 콘크리트(AAC) 시장의 장인적인 블록 부설에서 산업적인 패널 조립으로의 변화를 지원하고 있습니다.

지역 분석

아시아태평양은 2024년 세계 매출의 46.78%를 차지했고, 2030년까지의 CAGR은 7.28%를 나타낼 전망입니다. 중국과 인도는 수요의 중심이며 주거 메가 프로젝트와 국가 인프라 파이프라인이 견인하고 있습니다. 저탄소 건축법에 대한 정부의 우대조치는 AAC에 대한 사양을 더욱 기울입니다. 일본과 한국은 내진 안전성을 위해 AAC를 채택하고 호주는 가정용 에너지 기준으로 꾸준한 보급을 유지하고 있습니다. 아시아태평양의 원재료 자급률의 높이와 오토메이션화의 진전이 단가 경쟁력을 유지해 아시아태평양의 우위성을 확고하게 하고 있습니다.

북미에서는 미국 서부의 산불에 대한 내성 요건과 기후대를 넘은 건축 외피의 엄격화에 의해 AAC 사용의 르네상스가 일어나고 있습니다. EPA(미국 환경보호청)의 저배출 탄소 라벨은 공공 조달을 촉진하고 캐나다의 에너지 기준 개정은 그 기세를 가속화하고 있습니다. 멕시코 주택 자극 방법은 이 지역의 상황을 보완하고 오토클레이브 기포 콘크리트(AAC) 시장의 견조한 궤도를 제공합니다.

유럽의 성숙한 상황은 엄격한 탄소 목표의 혜택을 받고 있습니다 : 독일과 영국은 적극적으로 건물을 개조하고 북유럽 시장은 제로 에너지에 가까운 기준으로 향하고 있습니다. EU의 녹색 거래 대출은 플랜트 업그레이드 및 신설 라인을 지원합니다. 중유럽과 동유럽에서는 활기 넘치는 물류와 데이터센터 건설이 내화성과 열효율이 높은 쉘을 요구하고 있기 때문에 화이트 스페이스가 성장하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 신축·개축 수요의 확대

- 엄격한 그린 빌딩 규제와 LEED의 채용

- 저탄소 재료에 대한 정부의 인센티브

- 모듈식 오프사이트 건축의 보급

- 내진 경량 블록 수요

- 시장 성장 억제요인

- 점토·콘크리트 블록에 비해 높은 초기 비용

- 내하중 용도에 있어서 구조적 한계

- 알루미늄 분말 발포제공급과 가격의 변동성

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 제품 유형별

- 블록

- 패널

- 린텔

- 타일

- 기타(U 블록, 바닥/지붕 요소)

- 시공 방법별

- 현장 조적

- 조립/모듈

- 용도별

- 주택용

- 상업용

- 산업용

- 기타 용도(도로, 유틸리티 인클로저, 방음벽)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- ASEAN

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 폴란드

- 네덜란드

- 루마니아

- 체코 공화국

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 이스라엘

- 카타르

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- ACICO Group

- AERCON AAC

- Asahi Kasei Corporation

- Bauroc AS

- Biltech Building Elements Limited

- BirlaNu Limited

- Eastland Building Materials Co., Ltd

- Eco Green

- Ecostone AAC

- HH UK Limited

- JK Lakshmi Cement Ltd.

- Renacon

- SOLBET

- Starken AAC Sdn Bhd

- STT Turk Gazbeton

- Thomas Armstrong(Concrete Blocks) Ltd

- UAL Industries Limited

- UltraTech Cement Ltd.

- Xella International

제7장 시장 기회와 향후 전망

KTH 25.11.12The Autoclaved Aerated Concrete Market size is estimated at USD 15.56 billion in 2025, and is expected to reach USD 20.94 billion by 2030, at a CAGR of 6.12% during the forecast period (2025-2030).

Growth is fueled by tightening green-building mandates, rising demand for seismic-resilient structures, and the rapid adoption of modular construction, all of which highlight AAC's lightweight, energy-efficient profile. Blocks continue to dominate traditional masonry, yet panels are gaining momentum as prefabrication revamps project timelines. Asia-Pacific commands nearly half of global demand on the back of urbanization and infrastructure outlays, while North America and Europe capitalize on strict energy and seismic codes. Manufacturers are scaling capacity and automating plants to match demand spikes, improve cost structures, and strengthen regional supply chains.

Global Autoclaved Aerated Concrete (AAC) Market Trends and Insights

Growing Demand from New-Build & Renovation Construction

Surging residential and commercial starts in emerging economies have made lightweight materials indispensable because they lower foundation loads and shorten project cycles. AAC cuts dead weight by 30-40%, enabling slimmer foundations and quicker floor-to-floor progress, which is vital in dense city cores. India's housing drive illustrates the trend; domestic producer BigBloc Construction is expanding capacity to keep pace with elevated urban housing approvals. Renovation schemes also prefer AAC because its precision blocks streamline retrofits without reforging structure lines. Four-hour fire ratings boost compliance in commercial refurbishments, and its mold-proof matrix appeals in humid climates. Together, these factors underpin sustained Autoclaved Aerated Concrete market growth.

Stringent Green-Building Codes & LEED Adoption

Policies aimed at curbing embodied carbon are reshaping material selection worldwide. The US government's USD 160 million funding for sustainable-materials benchmarking explicitly encourages AAC uptake. EPA's 2024 low-carbon label gives manufacturers a clear route to quantify climate advantages, enhancing bid scores on public projects. Europe mirrors the shift; H+H UK is targeting net-zero operations by 2050, in line with EU decarbonization goals. With an R-value of 1.43 for 200 mm thickness, AAC delivers 10-20% operational energy savings and incorporates recycled fly ash, satisfying circular-economy criteria.

High Upfront Cost vs. Clay & Concrete Blocks

Perceptions of premium pricing hinder AAC's penetration where contractors prioritize purchase price over life-cycle savings. However, traditional red bricks recently became roughly 20% more expensive than AAC in key Indian metros, nudging buyers toward the lighter alternative. Material-price volatility is reshaping comparisons; 2025 tariffs elevated steel by 10-25% and concrete by 3-7%, eroding AAC's cost differential. Limited local plants in some regions still inflate delivered prices by 15-20%. Education campaigns stressing 30% energy-bill reductions and lower labor needs are gradually reframing procurement decisions around total cost of ownership.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Low-Carbon Materials

- Modular Off-Site Construction Uptake

- Volatile Supply & Price of Aluminum Powder Foaming Agent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Blocks held 54.78% of 2024 revenue, reflecting decades of contractor familiarity and broad distribution networks. In parallel, panels are charting a 7.81% CAGR through 2030 as builders pivot toward prefabricated envelopes. The panel boom embodies the construction industry's industrialization push: factory-cut modules arrive field-ready, reducing waste and compressing schedules. Developers favor panels in tall residential towers because fewer joints mean tighter thermal envelopes and lower infiltration losses.

The blocks segment remains central to low-rise housing, especially in markets where labor is abundant and on-site techniques dominate. Yet panel innovation is relentless. Reinforced wall panels now handle load-bearing duties, and roof modules with thermal conductivity of 0.11 W/mK meet zero-energy-building targets. Automated saw lines and robotic handling have cut panel-fabrication costs, underpinning an Autoclaved Aerated Concrete market shift from craft-based block laying to industrial panel assembly.

The Autoclaved Aerated Concrete Market Report is Segmented by Product Type (Block, Panel, Lintel, Tile, Others), Construction Method (On-Site Masonry, Prefabricated/Modular), Application (Residential, Commercial, Industrial, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 46.78% of global revenue in 2024 and is accelerating at 7.28% CAGR to 2030. China and India anchor demand, driven by housing mega-projects and state infrastructure pipelines. Government incentives for low-carbon building methods further tip specifications toward AAC. Japan and South Korea adopt AAC for seismic safety, while Australia's home-energy codes sustain steady uptake. High regional self-sufficiency in raw materials and rising automation keep unit costs competitive, cementing Asia-Pacific's dominance.

North America is experiencing a renaissance in AAC usage, propelled by wildfire resilience requirements in the western United States and stricter building envelopes across climate zones. The EPA's low-embodied-carbon label is catalyzing public procurement, and Canada's national energy code revision amplifies momentum. Mexico's housing stimulus complements the regional picture, leading to a robust Autoclaved Aerated Concrete market trajectory.

Europe's mature landscape benefits from stringent carbon targets: Germany and the UK aggressively retrofit buildings, while Nordic markets edge toward near-zero-energy codes. EU Green Deal financing supports plant upgrades and new lines. Central and Eastern Europe provide white-space growth as booming logistics and data-center construction seek fire-safe, thermally efficient shells.

- ACICO Group

- AERCON AAC

- Asahi Kasei Corporation

- Bauroc AS

- Biltech Building Elements Limited

- BirlaNu Limited

- Eastland Building Materials Co., Ltd

- Eco Green

- Ecostone AAC

- H+H UK Limited

- JK Lakshmi Cement Ltd.

- Renacon

- SOLBET

- Starken AAC Sdn Bhd

- STT Turk Gazbeton

- Thomas Armstrong (Concrete Blocks) Ltd

- UAL Industries Limited

- UltraTech Cement Ltd.

- Xella International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand from new-build & renovation construction

- 4.2.2 Stringent green-building codes & LEED adoption

- 4.2.3 Government incentives for low-carbon materials

- 4.2.4 Modular off-site construction uptake

- 4.2.5 Demand for seismic-resilient lightweight blocks

- 4.3 Market Restraints

- 4.3.1 High upfront cost vs. clay & concrete blocks

- 4.3.2 Structural limitations in load-bearing applications

- 4.3.3 Volatile supply & price of aluminum powder foaming agent

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Block

- 5.1.2 Panel

- 5.1.3 Lintel

- 5.1.4 Tile

- 5.1.5 Others (U-blocks, floor/roof elements)

- 5.2 By Construction Method

- 5.2.1 On-site masonry

- 5.2.2 Prefabricated/modular

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Other Applications (roads, utility enclosures, noise-barrier walls)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Australia and New Zealand

- 5.4.1.6 ASEAN

- 5.4.1.7 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Poland

- 5.4.3.8 Netherlands

- 5.4.3.9 Romania

- 5.4.3.10 Czech Republic

- 5.4.3.11 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Israel

- 5.4.5.3 Qatar

- 5.4.5.4 South Africa

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 ACICO Group

- 6.4.2 AERCON AAC

- 6.4.3 Asahi Kasei Corporation

- 6.4.4 Bauroc AS

- 6.4.5 Biltech Building Elements Limited

- 6.4.6 BirlaNu Limited

- 6.4.7 Eastland Building Materials Co., Ltd

- 6.4.8 Eco Green

- 6.4.9 Ecostone AAC

- 6.4.10 H+H UK Limited

- 6.4.11 JK Lakshmi Cement Ltd.

- 6.4.12 Renacon

- 6.4.13 SOLBET

- 6.4.14 Starken AAC Sdn Bhd

- 6.4.15 STT Turk Gazbeton

- 6.4.16 Thomas Armstrong (Concrete Blocks) Ltd

- 6.4.17 UAL Industries Limited

- 6.4.18 UltraTech Cement Ltd.

- 6.4.19 Xella International

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment