|

시장보고서

상품코드

1906886

로봇 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Robotics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

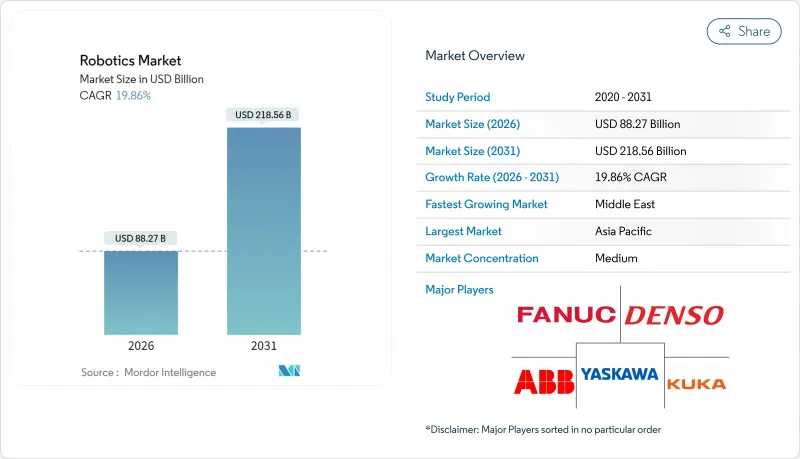

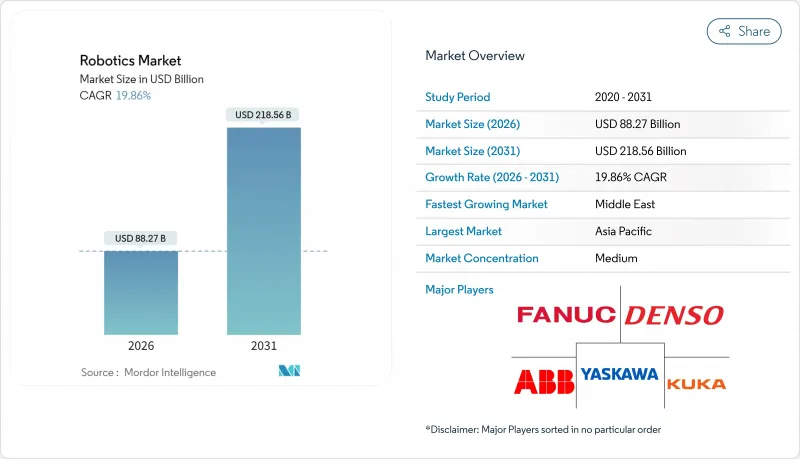

로봇 시장 규모는 2026년 882억 7,000만 달러로 추정되고, 2025년 736억 4,000만 달러에서 성장이 예상됩니다. 2031년 예측에서는 2,185억 6,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 19.86%로 확대될 전망입니다.

이러한 성장 궤도는 선진국의 구조적 노동력 부족, 자동화 하드웨어의 체계적인 비용 절감, 그리고 로봇을 임의의 자본재보다 전략적 인프라로 자리매김하는 정부 주도의 리쇼어링 정책을 반영합니다. 대기업은 임금 압력 속에서 생산을 안정화시키기 위해 도입을 가속시키고 중소기업도 협동 로봇 시스템과 Robot-as-a-Service 계약을 통해 액세스를 획득하고 있습니다. 지역별 기세는 변화하고 있습니다. 아시아태평양은 수량 기준으로 선두를 유지하고 있지만 중동은 주권 기금에 의한 기술 주도의 다각화 추진으로 가장 급속한 성장을 보이고 있습니다. 공급측에서는 부품 비용의 저하와 로우코드 프로그래밍 플랫폼이 밸류체인을 소프트웨어 인텔리전스로 재구축하여 인공지능 기반 제어 기술을 습득한 벤더에게 지속적인 수익원을 가져오고 있습니다. 사이버 보안 취약점, 수출 관리 마찰, 소규모 사용자의 기술 격차는 여전히 억제요인이지만, 특히 안전한 도입과 수명 주기 지원을 중심으로 전문 서비스 분야의 틈새 시장을 개척할 수 있는 기회도 창출하고 있습니다.

세계의 로봇 시장 동향 및 인사이트

노동력 부족 심각화가 자동화 수요 견인

일본, 미국, 서유럽 국가에서 인구 동태의 역풍으로 인해 자동화는 비용 절감에서 생산 능력 확보 모드로 전환하고 있습니다. 2024년에는 G7 국가의 제조업에서 200만 명 이상의 공장 구인 부족이 발생해 일본의 로봇 도입 밀도는 직원 1만 명당 399대로 과거 최고를 기록했습니다. 스텔란티스 등 자동차 제조업체는 반복성 스트레스 장애를 경감하면서 인원을 확보하는 인간 중심의 로봇 셀을 채용해, 협조적인 도입을 향한 미묘한 추진을 나타내고 있습니다. 이러한 구조적 격차는 경제 사이클을 통해 지속되기 때문에 공급업체에게 GDP 변동과 분리된 예측 가능한 수요 기반이 되어 세계의 로봇 시장이 혜택을 누리고 있습니다.

기능 시간당 평균 로봇 가격 하락

부품의 코모디티화 및 양산화에 의해 협동 로봇의 가격은 2024년 이후 연간 약 15% 저하되었습니다. 반면 소프트웨어 업그레이드로 인해 가격 대 성능 비율이 두 배로 증가했습니다. 중국 업체들은 엔트리 레벨 휴머노이드 로봇을 19만 9,000위안(2만 7,512달러)으로 판매하여 중소공장 자본 예산 내에서 로봇 도입을 가능하게 했습니다. 하드웨어 비용이 낮아짐에 따라 중소규모 제조업체 및 신흥 시장 제조업체의 도입 곡선이 가파르게 되어 세계 로봇 시장의 잠재 고객층이 확대됩니다.

중소기업에서 지속적인 통합 기술 부족

중소기업의 68%는 여전히 로봇 도입을 위한 기술 인력이 부족하여 투자 회수 기간이 장기화되고 가동률이 저하되고 있습니다. 시스 스킬 개발의 가속화 및 턴키 서비스 모델이 없으면, 세계의 로봇 시장에서는 방대한 잠재 수요가 미개척 그대로 남게 됩니다.

부문 분석

2025년 시점에서 산업용 로봇은 세계 로봇 시장의 71.04%를 차지해, 고생산성의 자동차 및 전자기기 조립 라인으로부터의 지속적인 수요에 지지되고 있습니다. 그러나 협동 로봇은 안전 인증을 취득한 역각 센서 기술과 3만 달러 미만의 가격대에 따라 중소기업의 예산 범위 내가 된 것을 배경으로 2031년까지 연평균 복합 성장률(CAGR) 25.64%로 확대를 계속하고 있습니다. 이 전환은 가로장으로 둘러싸인 라인이 아니라 유연한 인간 감시형 셀이 세계 로봇 시장의 다음 도입파를 견인한다는 것을 시사하고 있습니다.

중국제 협동 로봇 제조업체의 급증으로 2017-2024년 국내 점유율은 35%에서 73%로 상승했으며, 가격 경쟁을 격화시키는 동시에 세계 대수 성장을 가속화하고 있습니다. 서비스 로봇 분야도 계속 성장하고 있으며, 2025년에는 외과 수술 시스템 시장이 41억 8,000만 달러를 돌파했습니다. 의료 분야가 가장 급성장하는 최종 용도임을 재확인했습니다. 이 다양화는 세계 로봇 시장의 경기 변동성을 완화하고 하드웨어 벤더를 단일 분야 부진으로부터 보호합니다.

2025년 지출에 차지하는 하드웨어의 비율은 여전히 63.12%였지만 인공지능이 주요 가치 드라이버가 되는 가운데 소프트웨어 수익은 연률 22.91%의 성장이 예상됩니다. 고차원 제어 스택에는 클라우드 분석 및 강화 학습이 통합되어 ABB의 OmniCore 플랫폼에서 사이클 시간이 25% 단축되고 전력 소비량이 20% 감소되었습니다. 구독형 'Robot-as-a-Service' 세계 시장 규모는 고객이 자본 지출에서 운영 지출 모델로 전환함에 따라 2031년까지 3배로 확대될 것으로 예측됩니다.

통합, 원격 모니터링, 예지 보전을 다루는 서비스 수익은 공급업체 잠금을 더욱 강화합니다. 그 결과 소프트웨어 및 서비스의 경계가 모호해지고 업데이트 권한과 사이버 보안 패치가 여러년계약에 통합됩니다. 이 추세는 이익 구조를 재구성하고 세계 로봇 시장에서 순수하게 하드웨어 중심 과제에 대한 진입 장벽을 높입니다.

지역별 분석

아시아태평양은 2025년 세계 로봇 시장의 37.72%를 차지했으며, 중국에서 연간 43만대의 산업용 로봇 도입 실적과 전 세계 로봇 특허 허가 건수의 3분의 2가 이를 지원하고 있습니다. 중국 공장에서는 리튬 이온 배터리와 민생 전자 기기의 생산 라인에 로봇이 통합되어 국내 브랜드는 수출을 확대함으로써 지역의 비용 경쟁력을 세계 로봇 시장에 통합하고 있습니다. 일본에서는 2024년 화낙이 중국 수요 회복과 국내 인구 구조적 압력으로 1,802억 엔(16억 4,000만 달러)의 이익을 기록했습니다. 한국에서는 26억 달러의 관민공동 프로그램에 의해 휴머노이드 기술이 전지 공장의 자동화에 활용되어 전략적 우선도의 높이를 나타내고 있습니다.

중동 지역은 2031년까지 21.31%라는 최고 수준의 CAGR로 추이할 전망입니다. 이는 정부계 펀드가 석유 및 가스 잉여 자금을 산업 디지털화, 물류, 의료용 로봇 분야로 전환하고 있기 때문입니다. 아랍에미리트(UAE)의 자유 무역 지역에서는 지역 EC 물류에 대응하는 창고용 자율 이동 로봇(AMR)의 시험 운용이 실시되어, 계절 노동자에 대한 과도한 의존을 경감하고 있습니다. 국가 프로그램은 또한 선진 제조 거점에 자금을 제공하고 세계의 시스템 통합자를 유치하여 세계 로봇 시장의 잠재 고객 기반을 확대하고 있습니다.

북미의 수요는 견조를 유지하고 있으며, CHIPS법에 근거한 반도체 제조공장과 안듀릴사에 대한 6억 4,220만 달러 규모의 해군 대 드론 계약 등의 방위 계약이 견인하고 있습니다. 유럽에서는 안전한 인간과 로봇의 협동 기준과 지속가능성 목표에 주력하고 있으며 독일이 인공지능 통합에 연간 6,900만 유로(7,500만 달러)를 기여하고 있는 것이 뒷받침되고 있습니다. 두 지역 모두 고부가가치 소프트웨어 및 통합 기술 투자를 확대하는 반면, 범용 서브어셈블리 생산을 아시아로 아웃소싱하는 경향이 커지고 있으며, 이는 세계 로봇 시장의 바벨 전략을 반영합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 노동력 부족의 심각화에 따른 자동화 수요 증가

- 기능 시간당 평균 로봇 가격 저하

- 로우코드 로봇 프로그래밍 플랫폼의 보급

- G7 국가에서 제조업의 국내 회귀에 대한 재정적 우대 조치

- 전자상거래 3PL 사업자에 의한 창고용 자율 이동 로봇(AMR)의 도입 상황

- 국가 수준의 인형 로봇 연구 개발 미션(예 : 중국 2025)

- 시장 성장 억제요인

- 지속적인 중소기업 통합의 스킬 갭

- 고급 서보 모터에 대한 지정학적 수출 규제

- 희토류 자석의 가격 변동성

- ROS 도입에 있어서 사이버 보안의 취약성

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 시장의 거시 경제 동향 평가

제5장 시장 규모 및 성장 예측

- 로봇 유형별

- 산업용 로봇

- 서비스 로봇

- 협동 로봇(코봇)

- 모바일/AMR

- 컴포넌트별

- 하드웨어

- 소프트웨어

- 서비스(통합, RaaS)

- 용도별

- 제조 및 조립

- 물류 및 창고업

- 의료 및 외과

- 방위 및 보안

- 점검 및 유지보수

- 세정 및 위생 관리

- 최종 사용자 업계별

- 자동차

- 전자기기 및 반도체

- 식품 및 음료

- 의료 제공업체

- 군 및 방위

- 기타 최종 사용자 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- ABB Ltd.

- Fanuc Corporation

- Yaskawa Electric Corporation

- KUKA AG

- Kawasaki Heavy Industries Ltd

- Universal Robots A/S(Teradyne)

- Denso Corporation

- Mitsubishi Electric Corporation

- Omron Corporation

- Staubli International AG

- Epson Robots(세이코 Epson)

- Comau SpA

- Nachi-Fujikoshi Corp.

- Toshiba Corporation

- Intuitive Surgical Inc.

- Stryker Corporation

- iRobot Corporation

- Boston Dynamics Inc.

- Locus Robotics Corp.

- DJI Technology Co. Ltd

제7장 시장 기회 및 장래 전망

AJY 26.01.26Robotics market size in 2026 is estimated at USD 88.27 billion, growing from 2025 value of USD 73.64 billion with 2031 projections showing USD 218.56 billion, growing at 19.86% CAGR over 2026-2031.

This growth trajectory reflects structural labor shortages in advanced economies, systematic cost deflation in automation hardware, and government-backed reshoring programs that treat robots as strategic infrastructure rather than optional capital goods. Large enterprises accelerate adoption to stabilise production amid wage pressure, while small and medium firms now gain access through collaborative systems and Robot-as-a-Service contracts. Regional momentum is shifting: Asia-Pacific retains volume leadership, but the Middle East shows the quickest pace as sovereign funds pursue technology-driven diversification. On the supply side, declining component costs and low-code programming platforms reshape the value chain toward software intelligence, setting up recurring revenue streams for vendors that master artificial-intelligence-based control. Cyber-security weaknesses, export-control friction, and skill gaps among smaller users remain braking forces, yet they also open specialist service niches, especially around secure deployment and lifecycle support.

Global Robotics Market Trends and Insights

Rising Labour-Shortage Led Automation Demand

Demographic headwinds in Japan, the United States, and much of Western Europe have shifted automation from cost-saving to capacity-assurance mode. Unfilled factory vacancies topped 2 million roles across G-7 manufacturing in 2024, while Japan's robot density reached 399 units per 10,000 employees, the highest on record. Automakers such as Stellantis adopted human-centric robotic cells that trim repetitive strain injuries yet safeguard headcount, signalling a nuanced push toward collaborative deployment. The global robotics market benefits because these structural gaps persist through economic cycles, giving vendors a predictable demand base that decouples from GDP volatility.

Declining Average Robot Price Per Functional Hour

Component commoditisation and scale production cut collaborative robot prices by roughly 15% a year post-2024, while software upgrades doubled performance relative to price. Chinese suppliers even marketed entry-level humanoids at CNY 199,000 (USD 27,512), placing robots within small-factory capital budgets. As hardware costs slide, adoption curves steepen among small and emerging-market manufacturers, thereby widening the addressable pool for the global robotics market.

Persistent SME Integration Skill-Gap

Sixty-eight percent of SMEs still lack engineering talent for robotics deployment, prolonging payback periods and dampening utilisation rates. Integrators cluster in urban hubs, leaving regional firms underserved. Without accelerated skills development or turnkey service models, the global robotics market leaves considerable latent demand untapped.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Low-Code Robot-Programming Platforms

- Fiscal Incentives for Reshoring Manufacturing in G-7

- Geopolitical Export-Control on Advanced Servos

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial robots accounted for 71.04% of the global robotics market in 2025, riding sustained demand from high-throughput automotive and electronics assembly lines. Yet collaborative robots expand at a 25.64% CAGR to 2031, underpinned by safety-certified force-sensing and sub-USD 30,000 price tags that place them within SME budgets. This pivot signals that flexible, human-supervised cells, rather than fenced-off lines, will drive the next deployment wave of the global robotics market.

A surge in Chinese cobot makers lifted their domestic share from 35% to 73% between 2017 and 2024, heightening price competition and accelerating worldwide unit growth. Service-robot niches also flourish: surgical systems surpassed USD 4.18 billion in 2025, reaffirming healthcare as the fastest-rising end-use. This diversification reduces cyclicality for the global robotics market and cushions hardware vendors against single-sector downturns.

Hardware still represented 63.12% of 2025 spending, but software revenue is set to grow 22.91% annually as artificial intelligence becomes the primary value driver. Higher-level control stacks now incorporate cloud analytics and reinforcement learning that deliver 25% faster cycle times with 20% lower electricity use on ABB's OmniCore platform. The global robotics market size for subscription-based Robot-as-a-Service is projected to treble by 2031 as customers migrate from capital expenditure toward operating expenditure models.

Service revenues, covering integration, remote monitoring, and predictive maintenance, further solidify vendor lock-in. As a result, software and services blur, embedding update rights and cyber-security patches into multi-year contracts. This trend rewires profit pools and raises entry barriers for purely hardware-centric challengers within the global robotics market.

The Robotics Market Report is Segmented by Robot Type (Industrial Robots, Service Robots, and More), Component (Hardware, Software, and Services), Application (Manufacturing and Assembly, Logistics and Warehousing, Medical and Surgical, and More), End-User Industry (Automotive, Electronics and Semiconductor, Food and Beverage, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific secured 37.72% of global robotics market share in 2025, anchored by China's 430,000 annual industrial-robot installations and two-thirds of worldwide robotics patent grants. Chinese factories integrate robots into lithium-ion battery and consumer-electronics lines, while domestic brands escalate exports, embedding regional cost competitiveness into the global robotics market. Japan posted JPY 180.2 billion (USD 1.64 billion) profit at Fanuc in 2024 on revived Chinese demand and domestic demographic pressure. South Korea's USD 2.6 billion public-private programme channels humanoid expertise toward battery-plant automation, underscoring strategic prioritisation.

The Middle East registers the highest 21.31% CAGR to 2031 as sovereign wealth vehicles divert hydrocarbons surplus into industrial digitalisation, logistics, and healthcare robotics. Free-trade zones in the United Arab Emirates trial warehouse AMRs to service regional e-commerce flows, reducing over-reliance on seasonal migrant labour. National programmes additionally fund advanced manufacturing hubs that attract global integrators, amplifying the addressable base for the global robotics market.

North American demand remains resilient, propelled by CHIPS-Act-backed fabs and defence contracts such as the USD 642.2 million Navy counter-drone award to Anduril. Europe focuses on safe human-robot collaboration standards and sustainability targets, helped by EUR 69 million (USD 75 million) in annual German funding for artificial-intelligence integration. Both regions increasingly outsource commodity sub-assemblies to Asia while investing in high-value software and integration, reflecting a barbell strategy within the global robotics market.

- ABB Ltd.

- Fanuc Corporation

- Yaskawa Electric Corporation

- KUKA AG

- Kawasaki Heavy Industries Ltd

- Universal Robots A/S (Teradyne)

- Denso Corporation

- Mitsubishi Electric Corporation

- Omron Corporation

- Staubli International AG

- Epson Robots (Seiko Epson)

- Comau SpA

- Nachi-Fujikoshi Corp.

- Toshiba Corporation

- Intuitive Surgical Inc.

- Stryker Corporation

- iRobot Corporation

- Boston Dynamics Inc.

- Locus Robotics Corp.

- DJI Technology Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising labour-shortage led automation demand

- 4.2.2 Declining average robot price per functional hour

- 4.2.3 Proliferation of low-code robot-programming platforms

- 4.2.4 Fiscal incentives for reshoring manufacturing in G-7

- 4.2.5 Warehouse AMR roll-outs by e-commerce 3PLs

- 4.2.6 Nation-level humanoid RandD missions (e.g., China 2025)

- 4.3 Market Restraints

- 4.3.1 Persistent SME integration skill-gap

- 4.3.2 Geopolitical export-control on advanced servos

- 4.3.3 Rare-earth magnet price volatility

- 4.3.4 Cyber-security vulnerabilities in ROS deployments

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Robot Type

- 5.1.1 Industrial Robots

- 5.1.2 Service Robots

- 5.1.3 Collaborative (Cobots)

- 5.1.4 Mobile/AMR

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services (Integration, RaaS)

- 5.3 By Application

- 5.3.1 Manufacturing and Assembly

- 5.3.2 Logistics and Warehousing

- 5.3.3 Medical and Surgical

- 5.3.4 Defense and Security

- 5.3.5 Inspection and Maintenance

- 5.3.6 Cleaning and Sanitation

- 5.4 By End-User Industry

- 5.4.1 Automotive

- 5.4.2 Electronics and Semiconductor

- 5.4.3 Food and Beverage

- 5.4.4 Healthcare Providers

- 5.4.5 Military and Defense

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Fanuc Corporation

- 6.4.3 Yaskawa Electric Corporation

- 6.4.4 KUKA AG

- 6.4.5 Kawasaki Heavy Industries Ltd

- 6.4.6 Universal Robots A/S (Teradyne)

- 6.4.7 Denso Corporation

- 6.4.8 Mitsubishi Electric Corporation

- 6.4.9 Omron Corporation

- 6.4.10 Staubli International AG

- 6.4.11 Epson Robots (Seiko Epson)

- 6.4.12 Comau SpA

- 6.4.13 Nachi-Fujikoshi Corp.

- 6.4.14 Toshiba Corporation

- 6.4.15 Intuitive Surgical Inc.

- 6.4.16 Stryker Corporation

- 6.4.17 iRobot Corporation

- 6.4.18 Boston Dynamics Inc.

- 6.4.19 Locus Robotics Corp.

- 6.4.20 DJI Technology Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment