|

시장보고서

상품코드

1851250

스마트 서모스탯 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Smart Thermostat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

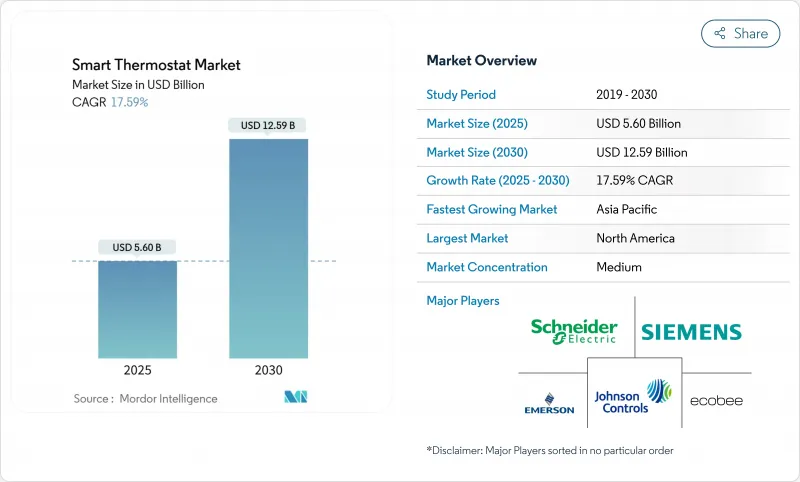

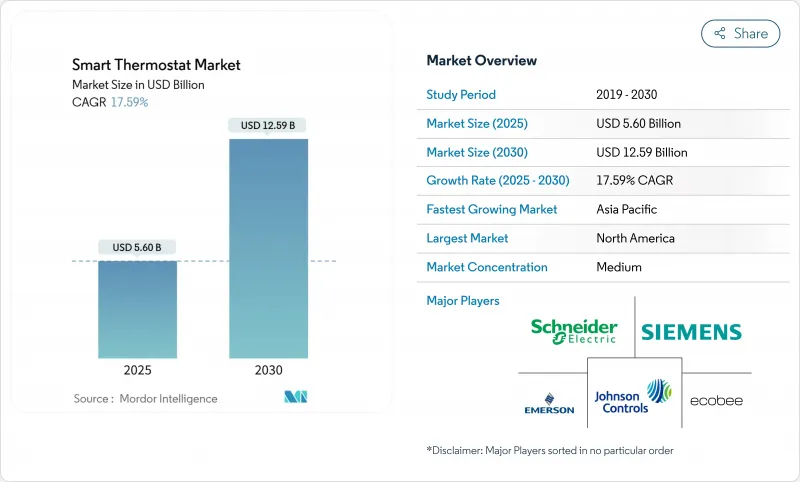

스마트 서모스탯 시장은 2025년에 56억 달러, 2030년에는 125억 9,000만 달러에 달할 것으로 예상되며, 예측 기간 중 CAGR은 17.59%를 나타낼 전망입니다.

성장의 주요 원동력은 에너지 효율에 중점을 둔 정책 강화, 꾸준한 그리드 현대화 투자, 생태계 봉쇄를 제거하는 Matter 상호 운용성 표준의 보급입니다. 유틸리티 회사는 연결된 서모스탯을 그리드 자산으로 취급하고 가상 발전소에 등록하여 피크 수요를 줄이고 예비 마진 비용을 줄입니다. 동시에 제조업체는 순수하게 하드웨어 가격으로 경쟁하는 것보다 프리미엄 소프트웨어 기능을 중시함으로써 반도체 및 구리 비용 상승을 흡수합니다.

세계의 스마트 서모스탯 시장 동향과 인사이트

정부 인센티브가 시장 보급 가속을 뒷받침

두꺼운 보조금 시스템과 동적 탈리프로 스마트 서모스탯 시장은 조기 어댑터의 영역을 넘어서고 있습니다. 캘리포니아는 저소득 가구에 지능형 HVAC 제어 장치를 설치하기 위해 5,000만 달러를 기록하여 에너지 공정성과 유연한 로드 채택을 연결합니다. 프랑스, 독일, 한국에서도 비슷한 리베이트 제도가 도입되어 대부분의 가정에서 투자 회수 기간이 3년 미만으로 단축되고 있습니다. 이러한 시책은 전력가격이 높고, 기후정책 목표도 높은 지역에서의 보급을 촉진하고, 개수 프로젝트의 양적 성장을 강화하고, 신축 주택에 미리 설치된 제어 장치에 대한 빌더 수요를 환기합니다.

스마트홈 에코시스템 통합이 가치 제안 확대

2024년 후반에 출시된 스레드 1.4는 자격 증명 공유 및 자체 복구 메시 네트워킹을 가정용 IoT의 표준 기능으로 사용합니다. 애플, 구글, 아마존은 2026년까지 자체 허브 제품에서 스레드 1.4를 지원할 것을 약속했으며 공급업체 앱 없이 크로스 플랫폼 페어링을 보장합니다. 소비자는 초기 설정 시 온보딩이 빨라지고 탈락이 줄어들어 구독 기반 에너지 서비스 플랜의 지속률이 높아집니다. 상업시설에서 오픈 API는 기존 빌딩 관리 소프트웨어와의 통합을 단순화하고 설치자의 교육 시간을 단축합니다. 이러한 네트워크 효과는 단일 인터페이스에서 조명, 보안 및 HVAC에 걸친 생태계를 보상함으로써 대응 가능한 수요를 확대합니다.

공급망 및 비용 인플레이션이 저렴한 압박

반도체 부족과 구리 가격 변동은 2024년과 2025년 사이에 연결된 서모스탯의 재료비를 15-20% 상승시켰습니다. 미국이 중국제 스마트 홈 디바이스에 부과한 관세는 이 비용 상승을 더욱 가속화하고, 각 브랜드는 박리 다매 또는 선반 가격 상승의 선택을 강요받게 됩니다. 일부 제조업체는 무역 장벽을 피하고 공급 위험을 분산시키기 위해 최종 조립을 대만, 베트남, 멕시코로 이동합니다. 설치업체의 보고에 따르면 인건비를 포함한 보수비용은 합계로 400달러를 넘는 경우가 많아 신흥국의 지불 의향을 상회하고 있습니다. 그 결과, 일부 공급업체는 판매 포털에 대출 및 전력 회사 리베이트 관련 자료를 번들하여 초기 지출을 완화하고 있습니다.

부문 분석

Wi-Fi 대응 기기는 2024년 출하 대수의 64.30%를 차지했습니다. 이것은 라우터가 거의 보편적으로 보급되고 설치 워크 플로우가 간단하다는 것을 반영합니다. 이 아성을 통해 Wi-Fi 시장 점유율은 기준 연도에서 단일 최대가 되었습니다. 이 분야는 계속해서 주택용 교체 증가로부터 혜택을 받지만, 메쉬 대응 Thread 칩의 양산이 시작되면 성장은 완만해집니다. Thread 디바이스는 2030년까지 연평균 복합 성장률(CAGR) 21.05%를 나타내고, 저소비 전력, 원활한 온보드, 자동 네트워크 힐링을 제공하는 것으로 Wi-Fi의 리드를 꾸준히 침식할 것으로 예측됩니다. 반면 Zigbee는 레거시 BMS 소프트웨어와 깔끔하게 통합할 수 있기 때문에 상업적 리노베이션에서는 여전히 인기가 있습니다. Z-Wave는 서브GHz 대역 간섭이 없는 링크를 선호하는 보안 시스템 설치업체들 사이에서 틈새 시장을 유지하고 있습니다. Wi-Fi 및 Thread 트래픽을 교차하는 Matter 컨트롤러의 능력이 높아짐에 따라 미래의 주택이 소유자를 하나공급업체에 고정하지 않고 비용, 통신 거리 및 배터리 수명을 최적화하는 혼합 스택 배치가 될 것이라고 제안합니다.

2세대 Thread 실리콘은 이미 듀얼 스택 기능을 탑재하고 있어 보더 라우터가 고장난 경우 2.4GHz Wi-Fi로 폴백할 수 있습니다. 애플이 2026년까지 Thread 1.4 펌웨어를 셋톱 박스에 출시할 것을 약속했기 때문에 주소 지정 가능한 허브는 수천만 대 규모로 확대될 것으로 보입니다. 상업시설에서 Thread의 결정성 대기 시간과 다중 경로 라우팅은 드롭 아웃에 민감한 거주자 편안함 용도의 신뢰성을 향상시킵니다. 이 변화를 예측한 공급업체는 모바일 링크 앱에 Thread 링크 상태를 강조하는 네트워크 품질 대시보드를 설치하여 설치자의 문제 해결을 용이하게 하며 기업 시설 관리자의 신뢰를 강화합니다.

2024년 유닛 수요의 57.80%는 개량 프로젝트이며, 교환이 가능한 표준 프로그래머블 서모스탯의 방대한 설치 베이스를 활용했습니다. 이러한 활동을 통해 복고풍은 예측 기간 동안 스마트 서모스탯 시장 규모의 가장 큰 부분을 차지합니다. 이 카테고리는 장비 제조업체가 주택 소유자가 30분 미만으로 자체 설치할 수 있는 범용 설치 플레이트와 C 배선 어댑터를 도입함으로써 번성합니다. 이와 병행하여 건축기준법의 개정과 그린본드에 의한 우대조치가 신축 수요를 가속화하고 2025년 이후에 건설되는 주택의 사전설치 시스템의 CAGR은 20.21%를 나타낼 전망입니다. 대규모 집합 주택 개발자는 오픈 프로토콜 서모스탯을 지정하는 경우가 많으며, 부동산 관리 소프트웨어가 포트폴리오 전체의 에너지 데이터를 집계할 수 있기 때문에 ESG 보고의 신뢰성이 높아집니다.

현재, 상업시설의 개수가 주목받고 있는 것은 하나의 오피스 타워가 주말에 1,000대의 기존 월스타트와의 교환을 실시해, 즉각적으로 에너지 삭감과 신속한 투자 회수를 실현할 수 있기 때문입니다. 지역 전력 회사는 부하 이동 지표가 검증되면 프로젝트 비용의 최대 30%를 환불하는 성능 기반 리베이트로 제안을 달게 합니다. 신축 빌딩에서 통합 설계 접근 방식은 서모스탯을 조명 및 입퇴실 관리 및 공유 IP 백본에 배치하여 시운전을 단순화합니다. 따라서 시장 진출기업은 제품 라인을 세분화하고 있습니다. 즉, 저가의 DIY 유닛은 주택 소유자를 타겟으로 하고, 프로 사양의 BACnet 대응 모델은 대규모 프로젝트의 입찰을 실시하는 계약자를 만족시킵니다.

스마트 서모스탯 시장 보고서는 연결 유형(유선 및 무선), 설치 유형(신축 및 리노베이션), 제품 유형(연결/프로그램 가능, 연결/프로그래밍 가능, 기타), 최종 사용자(주택, 상업, 기타), 연결 프로토콜(Wi-Fi, Zigbee, Z-Wave, 기타), 제품 인텔리전스 수준(학습형 스마트 서모스탯), 연결/프로그램

지역 분석

북미는 에너지 스타 라벨링, 주 수준 수요 반응 인센티브, 높은 1인당 HVAC 보급률에 힘입어 2024년 매출 점유율 38.60%로 최고를 기록했습니다. 그 후 유럽은 2030년까지 건물 에너지의 대폭적인 개조를 의무화하는 Fit-for-55 패키지에 견인되었습니다. 그러나 아시아태평양이 CAGR 17.66%로 가장 빠른 성장을 기록할 것입니다. 중국은 2024년에 1억 8,500만 대의 에어컨을 출하하여 연결형 컨트롤러로의 업그레이드를 촉진하는 방대한 설치 기반을 제공했습니다. 일본의 탄소 중립 로드맵은 기존 주택 스톡의 효율적인 업그레이드를 요구하고 있으며, 한국의 스마트 홈 세액 공제는 통합 HVAC 제어 비용을 낮추고 있습니다.

급속히 도시화가 진행되는 동남아시아에서는 중산계급의 가정이 스마트 서모스탯을 스테이터스 심볼로, 또 계절적인 열파시의 에너지 절약 툴로서 파악하고 있습니다. 태국과 말레이시아 정부 보조금 풀에는 현재 연결형 HVAC가 대상 장비로 포함되어 있으며 대응 가능한 수요가 확대되고 있습니다. 기타 라틴아메리카는 완만한 성장을 보이고 있으며, 브라질은 넷미터링 개혁을 활용하고, 멕시코는 신축 상업시설에 스마트 에너지 규범을 채택하고 있습니다. 중동 바이어는 유리로 덮인 타워의 높은 냉각 부하를 제어하는 데 중점을 두고 있지만, 저소득층에서는 여전히 비용이 많이 듭니다. 지역 격차는 제조업체가 채널 전략을 조정하고 신흥 국가에서 저렴한 SKU를 제공하며 성숙 시장에서 클라우드 서비스를 업셀링해야 함을 의미합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 에너지 절약 장비에 대한 수요 증가

- 정부의 인센티브와 다이나믹한 관세 도입

- 스마트 홈 에코시스템과 IoT 허브의 급속한 보급

- 수요 반응에 의한 가상 발전소(VPP)의 수익화

- Matter 프로토콜이 상호 운용성의 장벽 완화

- AI를 활용한 HVAC의 예측 유지보수 구독

- 시장 성장 억제요인

- 제품 및 설치의 높은 초기 비용

- 데이터 프라이버시와 사이버 보안에 대한 우려

- 레거시 HVAC 배선의 단편화

- 성숙시장에서 조기 어댑터의 포화

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 연결 기술별

- 무선

- Wi-Fi

- Zigbee

- Z-Wave

- Thread

- Bluetooth

- 유선

- 무선

- 설치 유형별

- 신축 건물

- 리모델링

- 제품 유형별

- 학습형 스마트 서모스탯

- 연결형/프로그래밍 가능

- 독립형/앱 전용

- 최종 사용자별

- 주택용

- 단독 주택

- 다세대 주택

- 상업용

- 사무실

- 소매 및 접객

- 의료시설

- 교육시설

- 산업 및 기타

- 경공업

- 데이터센터

- 주택용

- 접속 프로토콜별

- Wi-Fi

- Zigbee

- Z-Wave

- Thread(Matter 지원)

- Bluetooth/BLE

- 독점 915 MHz/서브 GHz RF

- 이더넷/이더넷 전원 공급(PoE)

- 제품 지능 수준별

- 학습형 스마트 서모스탯

- 독립형/앱 전용(휴대폰 중심)

- 연결형/프로그래밍 가능

- 다중 센서 환경 인식형

- 음성 어시스턴트 일체형

- 예측 유지보수/자가진단 컨트롤러

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주

- 동남아시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- GCC

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Nest Labs Inc.(Google)

- Resideo Technologies Inc.

- ecobee Inc.

- Emerson Electric Co.(Sensi)

- Lennox International Inc.

- Alarm.com Inc.

- LUX Products Corp.

- APX Group Inc.(Vivint)

- Johnson Controls plc

- Netatmo SA

- Tantalus Systems Corp.

- tado GmbH

- Centrica Hive Ltd.

- Siemens AG

- Amazon.com Inc.

- Schneider Electric SE

- Bosch Thermotechnology

- Carrier Global Corp.

- Trane Technologies plc

- Daikin Industries Ltd.

- Copeland LP

- Robertshaw Controls Co.

제7장 시장 기회와 향후 전망

KTH 25.11.12The smart thermostat market stands at USD 5.60 billion in 2025 and is projected to reach USD 12.59 billion by 2030, reflecting a solid 17.59% CAGR through the forecast period.

Growth is primarily driven by a tightening policy focus on energy efficiency, steady grid-modernization investments, and the spread of the Matter interoperability standard that removes ecosystem lock-in. Utilities are treating connected thermostats as grid assets, enrolling them in virtual power plants to shave peak demand and reduce reserve-margin costs.Uptake is further supported by falling sensor prices, the availability of Wi-Fi and Thread dual-band chips, and AI-based optimization that fine-tunes HVAC operation to weather forecasts and occupancy patterns. At the same time, manufacturers are absorbing higher semiconductor and copper costs by emphasizing premium software features rather than competing purely on hardware prices.

Global Smart Thermostat Market Trends and Insights

Government Incentives Drive Accelerated Market Penetration

Generous subsidy programs and dynamic tariffs are moving the smart thermostat market beyond early adopters. Japan's "Energy Saving 2025 Project" covers high-efficiency connected heating systems and offers bonus payments for removing legacy equipment, influencing replacement cycles in condominiums and single-family homes.California has earmarked USD 50 million for low-income households to install intelligent HVAC controls, linking energy equity to flexible-load adoption. Similar rebate structures appear in France, Germany, and South Korea, trimming payback periods to less than three years for most households. Together, these measures lift adoption in regions with both high power prices and climate-policy targets, reinforcing volume growth among retrofit projects and spurring builder demand for pre-installed controls in new homes.

Smart-Home Ecosystem Integration Amplifies Value Proposition

Thread 1.4, released in late 2024, makes credential sharing and self-healing mesh networking standard features for home IoT. The update lets thermostats serve as border routers, routing traffic when Wi-Fi falters and improving whole-home reliability.Apple, Google, and Amazon have publicly committed to Thread 1.4 support in their hub products by 2026, guaranteeing cross-platform pairing without vendor apps. Consumers experience faster onboarding and fewer drop-offs during initial setup, which translates to higher retention for subscription-based energy-services plans. For commercial facilities, open APIs simplify integration with existing building-management software and reduce installer training time. These network effects enlarge addressable demand by rewarding ecosystems that can span lighting, security, and HVAC in a single interface.

Supply Chain Cost Inflation Pressures Affordability

Semiconductor shortages and copper-price swings raised bill-of-materials costs for connected thermostats by 15-20% between 2024 and 2025. U.S. tariffs on Chinese-made smart-home devices compound the increase, leaving brands with a choice of thinner margins or higher shelf prices. Some producers are shifting final assembly to Taiwan, Vietnam, and Mexico to navigate trade barriers and diversify supply risk. Installers report that total retrofit costs, including labor, frequently exceed USD 400, outpacing willingness-to-pay in emerging economies. As a result, several vendors now bundle financing or utility rebate documentation inside their sales portals to soften the initial outlay.

Other drivers and restraints analyzed in the detailed report include:

- Virtual Power Plant Monetization Creates New Revenue Streams

- Matter Protocol Standardization Eliminates Interoperability Friction

- Cybersecurity Vulnerabilities Undermine Consumer Confidence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wi-Fi-enabled units accounted for 64.30% of shipments in 2024, reflecting near-universal router penetration and straightforward installation workflows. This stronghold gives Wi-Fi the single-largest smart thermostat market share in the base year. The segment continues to benefit from higher residential replacement activity, but growth moderates as mesh-capable Thread chips enter mass production. Thread devices are expected to post 21.05% CAGR through 2030, steadily eroding Wi-Fi's lead by offering lower power draw, seamless onboarding, and automatic network healing. Meanwhile, Zigbee remains popular in commercial retrofits because it integrates cleanly with legacy BMS software. Z-Wave keeps a niche among security-system installers that prioritize sub-GHz interference-free links. The rising ability of Matter controllers to bridge Wi-Fi and Thread traffic suggests future homes will carry mixed-stack deployments that optimize cost, range, and battery life without locking owners into one vendor.

Second-generation Thread silicon already embeds dual-stack capability, allowing fallback to 2.4 GHz Wi-Fi if border routers fail. Apple's commitment to release Thread 1.4 firmware to its set-top boxes by 2026 will enlarge the potential addressable base by tens of millions of hubs. For commercial properties, Thread's deterministic latency and multi-path routing improve reliability for occupant-comfort applications, which are sensitive to dropouts. Vendors anticipating this shift are loading mobile apps with network-quality dashboards that highlight Thread link status, easing installer troubleshooting and reinforcing confidence among corporate facility managers.

Retrofit projects represented 57.80% of 2024 unit demand, capitalizing on the vast installed base of standard programmable thermostats ready for replacement. This activity positions retrofit as the largest slice of the smart thermostat market size across the forecast window. The category prospers as device makers introduce universal mounting plates and C-wire adapters that let homeowners self-install in under 30 minutes. In parallel, building-code revisions and green-bond incentives accelerate new-construction demand, driving a 20.21% CAGR for pre-installed systems in homes built after 2025. Larger multifamily developers often specify open-protocol thermostats so that property-management software can aggregate energy data portfolio-wide, enhancing ESG reporting credibility.

Commercial retrofits now draw attention because a single office tower can swap 1,000 conventional wall stats in a weekend, generating immediate energy reductions and fast payback. Regional utilities sweeten the proposition with performance-based rebates that refund up to 30% of project cost once load-shifting metrics are validated. In new buildings, integrated design approaches place thermostats on a shared IP backbone with lighting and access control, simplifying commissioning. Market participants therefore segment their product lines: value-priced do-it-yourself units target homeowners, while professional-grade, BACnet-compatible models satisfy contractors bidding large projects.

Smart Thermostat Market Report is Segmented by Connectivity Type (Wired and Wireless), Installation Type (New Construction and Retrofit), Product Type (Connected/Programmable, Connected/Programmable, and More), End-User (Residential, Commercial, and More), Connectivity Protocol (Wi-Fi, Zigbee, Z-Wave, and More), Product Intelligence Level (Learning Smart Thermostats, Connected/Programmable, and More), and Geography.

Geography Analysis

North America posted the highest 2024 revenue with 38.60% share, aided by Energy Star labeling, state-level demand-response incentives, and high per-capita HVAC penetration. Europe followed, driven by the Fit-for-55 package that compels deep building-energy retrofits by 2030. The Asia Pacific region, however, will record the fastest gains at 17.66% CAGR. China shipped 185 million air-conditioner units in 2024, providing a vast install base that primes upgrades to connected controllers. Japan's carbon-neutrality roadmap requires efficiency upgrades in existing housing stock, and South Korea's smart-home tax credits lower the cost of integrated HVAC controls.

In rapidly urbanizing Southeast Asia, middle-class households view smart thermostats as both status symbols and energy-saving tools during seasonal heatwaves. Government subsidy pools in Thailand and Malaysia now include connected HVAC as eligible equipment, expanding addressable demand. Elsewhere, Latin America posts moderate growth, with Brazil leveraging net-metering reforms and Mexico adopting smart-energy codes for new commercial builds. Middle East buyers focus on controlling the high cooling loads in glass-clad towers, yet cost remains a hurdle in lower-income segments. Regional disparities mean manufacturers must tailor channel strategies, offering budget SKUs in emerging economies while upselling cloud services in mature markets.

- Nest Labs Inc. (Google)

- Resideo Technologies Inc.

- ecobee Inc.

- Emerson Electric Co. (Sensi)

- Lennox International Inc.

- Alarm.com Inc.

- LUX Products Corp.

- APX Group Inc. (Vivint)

- Johnson Controls plc

- Netatmo SA

- Tantalus Systems Corp.

- tado GmbH

- Centrica Hive Ltd.

- Siemens AG

- Amazon.com Inc.

- Schneider Electric SE

- Bosch Thermotechnology

- Carrier Global Corp.

- Trane Technologies plc

- Daikin Industries Ltd.

- Copeland LP

- Robertshaw Controls Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing demand for energy-saving devices

- 4.2.2 Government incentives and dynamic tariff roll-outs

- 4.2.3 Rapid adoption of smart-home ecosystems and IoT hubs

- 4.2.4 Virtual-power-plant (VPP) monetisation via demand response

- 4.2.5 Matter protocol lowers interoperability barriers

- 4.2.6 AI-driven HVAC predictive-maintenance subscriptions

- 4.3 Market Restraints

- 4.3.1 High upfront product and installation cost

- 4.3.2 Data-privacy and cybersecurity concerns

- 4.3.3 Legacy HVAC wiring fragmentation

- 4.3.4 Early-adopter saturation in mature markets

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Connectivity Technology

- 5.1.1 Wireless

- 5.1.1.1 Wi-Fi

- 5.1.1.2 Zigbee

- 5.1.1.3 Z-Wave

- 5.1.1.4 Thread

- 5.1.1.5 Bluetooth

- 5.1.2 Wired

- 5.1.1 Wireless

- 5.2 By Installation Type

- 5.2.1 New Construction

- 5.2.2 Retrofit

- 5.3 By Product Type

- 5.3.1 Learning Smart Thermostats

- 5.3.2 Connected/Programmable

- 5.3.3 Stand-alone/App-only

- 5.4 By End-User

- 5.4.1 Residential

- 5.4.1.1 Single-family Homes

- 5.4.1.2 Multi-family Units

- 5.4.2 Commercial

- 5.4.2.1 Offices

- 5.4.2.2 Retail and Hospitality

- 5.4.2.3 Healthcare Facilities

- 5.4.2.4 Education Campuses

- 5.4.3 Industrial and Others

- 5.4.3.1 Light Industrial

- 5.4.3.2 Data Centres

- 5.4.1 Residential

- 5.5 By Connectivity Protocol

- 5.5.1 Wi-Fi

- 5.5.2 Zigbee

- 5.5.3 Z-Wave

- 5.5.4 Thread (Matter-ready)

- 5.5.5 Bluetooth / BLE

- 5.5.6 Proprietary 915 MHz / Sub-GHz RF

- 5.5.7 Ethernet / Power-over-Ethernet

- 5.6 By Product Intelligence Level

- 5.6.1 Learning Smart Thermostats

- 5.6.2 Stand-alone/App-only (phone-centric)

- 5.6.3 Connected/Programmable

- 5.6.4 Multi-sensor Environment-Aware

- 5.6.5 Voice-assistant-integrated

- 5.6.6 Predictive-maintenance / Self-diagnostic Controllers

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 South Korea

- 5.7.4.4 India

- 5.7.4.5 Australia

- 5.7.4.6 South-East Asia

- 5.7.4.7 Rest of Asia Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 GCC

- 5.7.5.1.2 Turkey

- 5.7.5.1.3 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Nest Labs Inc. (Google)

- 6.4.2 Resideo Technologies Inc.

- 6.4.3 ecobee Inc.

- 6.4.4 Emerson Electric Co. (Sensi)

- 6.4.5 Lennox International Inc.

- 6.4.6 Alarm.com Inc.

- 6.4.7 LUX Products Corp.

- 6.4.8 APX Group Inc. (Vivint)

- 6.4.9 Johnson Controls plc

- 6.4.10 Netatmo SA

- 6.4.11 Tantalus Systems Corp.

- 6.4.12 tado GmbH

- 6.4.13 Centrica Hive Ltd.

- 6.4.14 Siemens AG

- 6.4.15 Amazon.com Inc.

- 6.4.16 Schneider Electric SE

- 6.4.17 Bosch Thermotechnology

- 6.4.18 Carrier Global Corp.

- 6.4.19 Trane Technologies plc

- 6.4.20 Daikin Industries Ltd.

- 6.4.21 Copeland LP

- 6.4.22 Robertshaw Controls Co.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment