|

시장보고서

상품코드

1851251

폐암 치료제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Lung Cancer Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

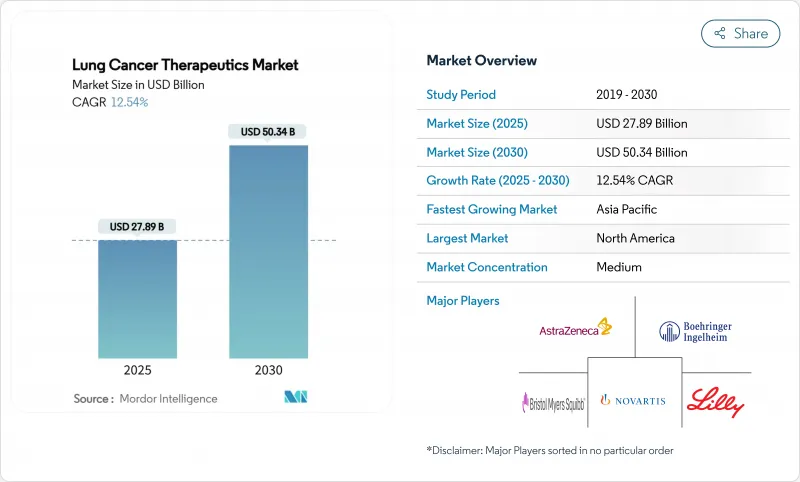

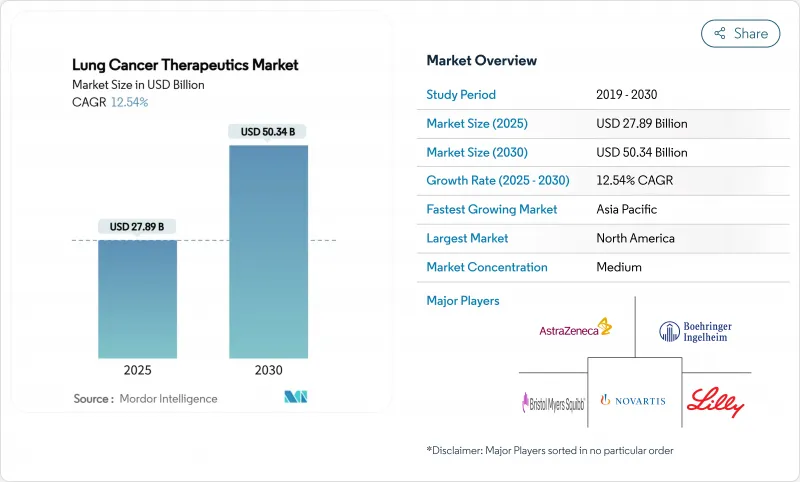

폐암 치료제 시장 규모는 2025년 278억 9,000만 달러, 2030년 503억 4,000만 달러에 달할 것으로 예상되며 CAGR은 12.54%를 나타낼 전망입니다.

급속한 신장은 면역 종양학의 돌파구, 이중특이적 항체, 세계적인 보험 상환의 보급에 의해 초래되며, 이들은 총체로서 치료량을 증가시킵니다. 규제 당국이 2024년 이후에 새롭게 11개의 비소세포암의 승인을 신속화한 것은 개발 스케줄을 단축하고 경쟁을 격화시키는 혁신 사이클을 명확하게 보여주었습니다. 프리시전 바이오마커 검사가 전문가로부터 주류로 이행하여 돌연변이에 적합한 약제 선택이 가능해져 지금까지 치료가 어려웠던 환자의 연주효율이 향상되었습니다. 아시아태평양과 라틴아메리카에서는 보험 적용 범위가 확대되어 구입하기 쉬워지는 한편, 성숙 시장에서는 가격 압력이 계속되고, 제조업체 각사는 밸류 베이스 계약으로 조타를 끊고 있습니다. 주요 특허 절벽이 오기 전에 각 회사가 포지션을 지키려고 하기 때문에 제형 플랫폼을 둘러싼 전략적 통합이 가속화되고 있습니다.

세계의 폐암 치료제 시장 동향과 인사이트

면역 종양학 및 표적 치료의 급속한 보급

체크포인트 억제제와 새로운 표적의 조합은 기존의 화학요법을 뛰어넘는 생존기간의 연장을 기대합니다. 탈라타맙과 같은 이중특이적 T 세포 인게이저는 전처리가 많은 소세포암에서 40%의 객관적 주효를 보였으며, 다토포타맙 델쿠스테칸과 같은 항체 약물 복합체는 EGFR 돌연변이가 있는 비소세포암에서 45%의 주효에 도달했습니다. 2024년에만 13개의 폐암 적응증이 FDA의 촉진 경로를 클리어하고, 상시 사이클이 단축되어 경쟁이 격화되었습니다. 면역 활성화와 돌연변이 특이적 차단의 조합에 의해 이스케이프 메커니즘을 둔화시키기 위해, 병용 요법이 파이프라인의 주류가 되고 있습니다. 바이오마커 주도의 선택은 현재 대부분의 1차 치료를 결정하여 더 높은 효능 심도와 더 긴 무증악 기간을 가능하게 합니다. 새로운 치료법이 제일 선택됨에 따라, 화학요법은 단독요법이 아니고, 다제 병용 프로토콜에서의 기간적인 역할로 이동하고 있습니다.

프리시전 메디신 바이오마커 검사의 보급

종합적인 분자 프로파일 링이 조직학 기반 선택을 대체합니다. Oncomine Dx Express Test와 같은 FDA 인증 진단제가 지원하는 차세대 시퀀싱 패널은 지역 종양 의사의 표준이되고 있습니다. EGFR, ALK, ROS1, KRAS, HER2, MET 및 BRAF를 포함하는 실용적인 돌연변이는 현재 비소세포 암 사례의 60% 이상의 선택에 정보를 제공합니다. 리퀴드 바이옵시는 실시간 내성 모니터링을 확대하여 임상 진행 전에 치료법을 전환할 수 있습니다. 시퀀싱 비용의 감소와 지불자의 상환으로 고소득 아시아태평양 시장에서는 바이오 마커 검사가 일상 진료에 통합됩니다. 보다 광범위한 패널은 표적 약물의 새로운 상업적 틈새 시장을 창출하고 검사 채택과 약물 개발의 선순환을 강화합니다.

높은 치료 비용과 가격 압력

연간 치료비는 20만 달러를 넘는 경우가 많아 지급자와 환자를 괴롭히고 있습니다. 듀발바맙의 약가는 생존기간 연장효과가 있음에도 불구하고 세계적인 보급을 늦추었으며 비용효과 분석은 자원이 부족한 지역에서는 불리한 비율을 보였습니다. 펨브롤리주맙과 니볼루맙의 바이오시밀러 의약품 파이프라인은 가격 결정력을 깎을 것으로 예상되며, 오리지네이터는 가치 기반 거래를 강요합니다. 병용 요법은 비용을 증가시키고 다년간의 치료 기간은 예산에 미치는 영향을 확대합니다. 유럽과 라틴아메리카의 기준 가격 프레임 워크는 할인에 대한 기대를 강화하고 있습니다. 제조업체 각사는 결과 보증이나 단계적 가격 설정에 의해 대응하고 있지만, 저소득 국가에서의 액세스 격차는 여전히 남아 있습니다.

부문 분석

비소세포암은 바이오마커에 기반한 광범위한 선택과 높은 이환율의 혜택을 받아 폐암 치료제 시장 점유율에서 2024년 매출의 77.23%를 차지했습니다. 소세포 영역은 퍼스트 인 클래스의 이중특이성 탈라타맙과 체크포인트의 추가로 2030년까지의 CAGR은 13.21%를 나타낼 것으로 예측되고 있습니다. 따라서 소세포암 치료의 폐암 치료제 시장 규모는 낮은 앵커 포인트에서 급속히 상승할 것으로 예측됩니다. EGFR 억제제와 KRAS 억제제와 같은 NSCLC에서의 고정밀 접근법은 이 부문의 규모를 유지하고 있지만 파이프라인의 기세는 SCLC를 경시에서 기회로 눈에 보이게 이동시키고 있습니다.

SCLC의 기술 혁신의 지속은 역사적인 생존 기간의 격차를 줄입니다. 탈라타맙은 전치료가 많은 코호트에서 40%의 객관적 효과를 달성했고, 듀발바맙은 제한된 병기 설정으로 전체 생존 기간 중앙값을 55.9개월로 밀어 올렸습니다. NSCLC의 파이프라인은 HER2 억제제와 MET 억제제 외에도 저항성을 재 억제하는 항체 약물 복합체를 추가하고 볼륨 리더십을 유지합니다. 두 분야를 합치면 기존 기업에 포트폴리오 확대를 촉구하는 동시에 전문적인 기업을 끌어들이는 다양화를 보여줍니다.

화학요법은 여전히 2024년 매출의 43.21%를 차지했지만, 면역요법은 CAGR 13.24%로 상승하여 화학요법 단제에 대한 의존도를 저하시킬 것으로 예측되고 있습니다. 체크포인트 억제제는 PD-L1 양성의 1차 치료에, 바이스페시픽 약물은 SCLC의 2차 치료 프로토콜의 선두에 서 있습니다. 면역요법에 할당되는 폐암 치료제 시장 규모는 10년간 두배로 될 것으로 예측됩니다. 표적 약물은 뚜렷하게 정의된 바이오마커에 초점을 맞추어 한 자릿수 중반의 안정적인 성장을 나타냅니다.

병용 요법이 증가하고 있습니다. 듀르발맙과 화학요법의 병용은 한국기 SCLC의 생존기간을 연장하고, 화학요법과 IO의 병용은 비소세포암 1차 치료의 주류가 되고 있습니다. T 세포 인게이저와 항체 약물 복합체의 파이프라인이 충실함에 따라 면역요법의 대상은 바이오마커의 낮은 집단까지 퍼져, 대응 가능한 수요가 확대됨과 동시에 안전성 관리의 규범이 재구성됩니다.

지역 분석

북미는 2024년 세계 매출의 39.19%를 차지했습니다. 첨단 임상시험 인프라를 통해 시험에서 실천으로 신속하게 전환할 수 있습니다. 보험 제도는 고비용의 처방에 자금을 공급하고 있지만, 바이오시밀러가 다가오는 가운데, 가격 협상은 엄격해지고 있습니다. 아카데믹 센터는 가이드라인 업데이트를 가속화하고 채용 곡선을 가파르게 유지합니다. 캐나다와 멕시코는 국경을 넘는 임상시험에 참여하여 환자 접근을 확대하고 있습니다.

아시아태평양은 CAGR 13.56%를 나타낼 전망입니다. 중국의 보험 상환 확대와 지역 혁신이 더블 팀에서 억제된 수요를 개방합니다. 일본에서는 우선 치료제의 심사를 6개월로 단축하는 가속 프로그램이 도입되어 호주에서는 미충족 요구가 높은 암에 대해 빠른 패스웨이가 활용되고 있습니다. 인도와 동남아시아에서는 3차 병원에 NGS 패널을 설치하여 진단 능력을 확대합니다. 경제 발전과 도시 오염은 공동으로 폐 부담을 증가시키고 수량 성장을 유지합니다.

유럽은 한 자리 대 중반의 꾸준한 성장을 보여줍니다. EMA(유럽 의약품청)의 일원적인 승인이 동시상시를 가속시키지만, 상환 결정은 여전히 국가마다 다릅니다. 의료기술평가기관은 가치의 역치를 중시하고 제조업체를 매니지드 엔트리 계약으로 유도합니다. 동유럽 시장은 암 영역의 인프라 정비를 위한 EU의 결속 자금을 통해 추구하고 있습니다. 영국에서는 Brexit을 계기로 병렬 경로가 도입되었지만 상호 승인으로 대부분공급 경로가 유지되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 폐암의 유병률 증가

- 공해와 흡연률 상승

- 면역종양학과 표적요법의 급속한 보급

- 확대하는 헬스케어 보험 적용 범위

- 정밀의료에 의한 바이오마커 검사의 보급

- 세포·RNA 기반의 새로운 치료 파이프라인

- 시장 성장 억제요인

- 높은 치료비와 가격압력

- 심각한 면역 관련 부작용

- 블록버스터 의약품에 육박하는 특허의 절벽

- 저자원 환경에서의 생검 접근 제한

- 가치/공급망 분석

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 질환 유형별

- 비소세포폐암(NSCLC)

- 소세포폐암(SCLC)

- 기타

- 치료 방식별

- 화학요법

- 면역요법

- 표적 치료

- 약물 종류별

- 저분자 약물

- 생물학적 제제 및 바이오시밀러

- 유통 채널별

- 병원 약국

- 소매 약국

- 온라인 약국

- 치료 단계별

- 1차 치료

- 2차 치료

- 3차 및 그 이상의 치료

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- F. Hoffman La Roche Ltd.

- AstraZeneca

- Merck & Co.

- Bristol-Myers Squibb

- Pfizer

- Boehringer Ingelheim

- Eli Lilly

- Novartis

- Johnson & Johnson(Janssen)

- AbbVie

- Amgen

- Sanofi

- Takeda

- Daiichi Sankyo

- BeiGene

- Exelixis

- Innovent Biologics

- Clovis Oncology

- Blueprint Medicines

제7장 시장 기회와 향후 전망

KTH 25.11.12The lung cancer therapeutics market size stood at USD 27.89 billion in 2025 and is forecast to reach USD 50.34 billion by 2030, translating into a 12.54% CAGR.

Rapid gains stem from immuno-oncology breakthroughs, bispecific antibodies, and wider global reimbursement adoption that collectively lift treatment volumes. Regulatory agencies expedited 11 new non-small cell approvals after 2024, underscoring an innovation cycle that compresses development timelines and intensifies competition. Precision biomarker testing has moved from specialist to mainstream practice, enabling mutation-matched drug selection and pushing response rates higher for previously hard-to-treat patients. Wider insurance coverage across Asia-Pacific and Latin America improves affordability, while price pressure in mature markets continues to nudge manufacturers toward value-based agreements. Strategic consolidation around combination platforms is accelerating as companies seek to defend positions before major patent cliffs arrive.

Global Lung Cancer Therapeutics Market Trends and Insights

Rapid Adoption of Immuno-Oncology & Targeted Therapies

Checkpoint inhibitors combined with novel targets lift survival beyond legacy chemotherapy. Bispecific T-cell engagers such as tarlatamab post 40% objective responses in heavily pre-treated small-cell cases, while antibody-drug conjugates like datopotamab deruxtecan reach 45% responses in EGFR-mutated non-small-cell disease . Thirteen lung cancer indications cleared the FDA's accelerated pathway during 2024 alone, compressing launch cycles and intensifying rivalry . Combination regimens dominate pipelines as developers marry immune activation with mutation-specific blockade to blunt escape mechanisms. Biomarker-driven selection now guides most first-line decisions, enabling higher response depths and longer progression-free intervals. As new modalities gain first-line status, chemotherapy shifts toward a backbone role within multi-agent protocols rather than standalone therapy.

Precision-Medicine Biomarker Testing Uptake

Comprehensive molecular profiling is replacing histology-based selection. Next-generation sequencing panels, supported by FDA-cleared diagnostics such as the Oncomine Dx Express Test, are becoming standard for community oncologists . Actionable alterations cover EGFR, ALK, ROS1, KRAS, HER2, MET, and BRAF, now informing choices for more than 60% of non-small-cell cases. Liquid biopsy expands real-time resistance monitoring, allowing therapy switches before clinical progression. Declining sequencing costs, along with payer reimbursement, embed biomarker testing into routine care across higher-income Asia-Pacific markets. Wider panels create additional commercial niches for targeted agents, reinforcing a virtuous cycle of test adoption and drug development.

High Therapy Costs & Pricing Pressures

Annual courses often exceed USD 200,000, straining payers and patients. Durvalumab's acquisition price slowed global uptake despite survival benefit, with cost-effectiveness analyses finding unfavorable ratios in resource-constrained regions. Biosimilar pipelines for pembrolizumab and nivolumab are expected to erode pricing power, forcing originators into value-based deals. Combination regimens compound cost, and multi-year therapy durations magnify budget impact. Reference pricing frameworks in Europe and Latin America intensify discount expectations. Manufacturers respond by offering outcome guarantees and tiered pricing, yet access gaps persist in low-income countries.

Other drivers and restraints analyzed in the detailed report include:

- Emerging Cell & RNA-Based Therapy Pipeline

- Expanding Healthcare Reimbursement Coverage

- Looming Patent Cliffs for Blockbuster Drugs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Non-small cell disease generated 77.23% of 2024 revenue within the lung cancer therapeutics market share, benefiting from broad biomarker-driven options and high incidence. The small-cell segment holds a smaller base yet is forecast to outpace at 13.21% CAGR through 2030, fueled by the first-in-class bispecific tarlatamab and checkpoint additions. The lung cancer therapeutics market size for small-cell therapy is therefore projected to climb swiftly from a low anchor point. Precision approaches in NSCLC, such as EGFR and KRAS inhibitors, keep that segment sizeable, but pipeline momentum is visibly shifting SCLC from neglect to opportunity.

Continued SCLC innovation narrows historic survival gaps. Tarlatamab reached 40% objective responses in heavily pre-treated cohorts, and durvalumab pushed median overall survival to 55.9 months in limited-stage settings. NSCLC pipelines add HER2 and MET inhibitors plus antibody-drug conjugates to re-intercept resistance, keeping volume leadership intact. Together, both segments illustrate a diversification that attracts specialized players while pushing incumbents to broaden portfolios.

Chemotherapy still accounted for 43.21% of 2024 revenue, yet immunotherapy is projected to climb at 13.24% CAGR, eroding monotherapy chemo reliance. Checkpoint inhibitors moved into first-line PD-L1-positive care, and bispecifics headline second-line SCLC protocols. The lung cancer therapeutics market size allocated to immunotherapy is forecast to double over the decade. Targeted agents add steady mid-single-digit growth by focusing on well-defined biomarkers.

Combination regimens are rising. Durvalumab plus chemotherapy extended survival in limited-stage SCLC, while chemo-IO combos dominate non-small cell first-line practice. As pipelines fill with T-cell engagers and antibody-drug conjugates, immunotherapy's reach broadens into biomarker-low populations, enlarging addressable demand while reshaping safety management norms.

The Lung Cancer Therapeutics Market Report is Segmented by Disease Type (Non-Small Cell Lung Cancer, Small Cell Lung Cancer, Others), Treatment Modality (Chemotherapy, and More), Drug Class (Small-Molecule Drugs, Biologics and Biosimilars), Distribution Channel (Hospital Pharmacies, and More), Line of Therapy (First-Line, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 39.19% of global revenue in 2024. Advanced trial infrastructure enables rapid translation from study to practice. Insurance systems fund high-cost regimens, though price negotiations tighten as biosimilars loom. Academic centers accelerate guideline updates, keeping adoption curves steep. Canada and Mexico participate through cross-border trials, widening patient access.

Asia-Pacific is the chief growth engine at 13.56% CAGR. China's reimbursement expansion and local innovation double-team to unlock suppressed demand. Japan's accelerated programs shorten review to 6 months for priority therapies, while Australia leverages expedited pathways for unmet-need cancers. India and Southeast Asia scale diagnostic capacity, installing NGS panels in tertiary hospitals. Economic development and urban pollution jointly increase lung burden, sustaining volume growth.

Europe exhibits steady mid-single-digit gains. Centralized EMA approvals speed simultaneous market launches, but reimbursement decisions remain country specific. Health technology assessment bodies focus on value thresholds, nudging manufacturers toward managed-entry agreements. Eastern European markets catch up through EU cohesion funding for oncology infrastructure. Brexit triggered parallel pathways in the United Kingdom, yet mutual recognition maintains most supply routes.

- Roche

- AstraZeneca

- Merck

- Bristol-Myers Squibb

- Pfizer

- Boehringer Ingelheim

- Eli Lilly and Company

- Novartis

- Johnson & Johnson

- Abbvie

- Amgen

- Sanofi

- Takeda Pharmaceuticals

- Daiichi Sankyo

- BeiGene

- Exelixis

- Innovent Biologics

- Clovis Oncology

- Blueprint Medicines

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing prevalence of lung cancer

- 4.2.2 Rising pollution & smoking rates

- 4.2.3 Rapid adoption of immuno-oncology & targeted therapies

- 4.2.4 Expanding healthcare reimbursement coverage

- 4.2.5 Precision-medicine driven biomarker testing uptake

- 4.2.6 Emerging cell & RNA-based therapies pipeline

- 4.3 Market Restraints

- 4.3.1 High therapy costs & pricing pressures

- 4.3.2 Severe immune-related adverse events

- 4.3.3 Looming patent cliffs for blockbuster drugs

- 4.3.4 Limited biopsy access in low-resource settings

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Disease Type

- 5.1.1 Non-Small Cell Lung Cancer (NSCLC)

- 5.1.2 Small Cell Lung Cancer (SCLC)

- 5.1.3 Others

- 5.2 By Treatment Modality

- 5.2.1 Chemotherapy

- 5.2.2 Immunotherapy

- 5.2.3 Targeted Therapy

- 5.3 By Drug Class

- 5.3.1 Small-Molecule Drugs

- 5.3.2 Biologics and Biosimilars

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.5 By Line of Therapy

- 5.5.1 First-Line

- 5.5.2 Second-Line

- 5.5.3 Third-Line and Beyond

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 F. Hoffman La Roche Ltd.

- 6.3.2 AstraZeneca

- 6.3.3 Merck & Co.

- 6.3.4 Bristol-Myers Squibb

- 6.3.5 Pfizer

- 6.3.6 Boehringer Ingelheim

- 6.3.7 Eli Lilly

- 6.3.8 Novartis

- 6.3.9 Johnson & Johnson (Janssen)

- 6.3.10 AbbVie

- 6.3.11 Amgen

- 6.3.12 Sanofi

- 6.3.13 Takeda

- 6.3.14 Daiichi Sankyo

- 6.3.15 BeiGene

- 6.3.16 Exelixis

- 6.3.17 Innovent Biologics

- 6.3.18 Clovis Oncology

- 6.3.19 Blueprint Medicines

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment