|

시장보고서

상품코드

1851253

구연산 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Citric Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

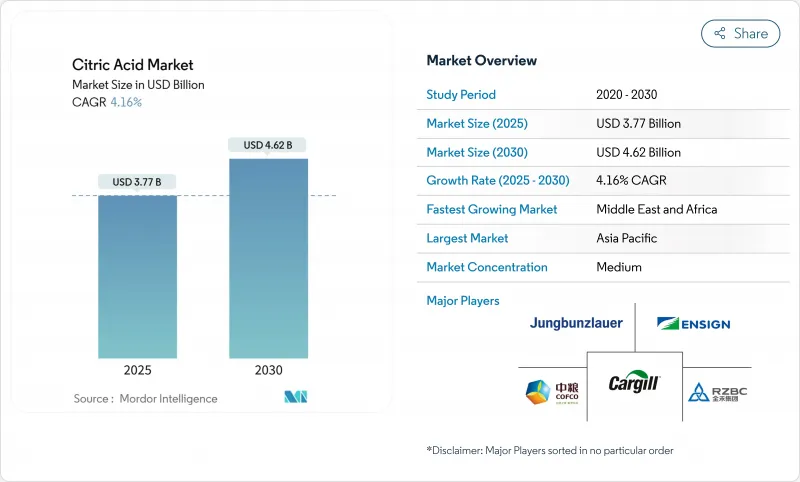

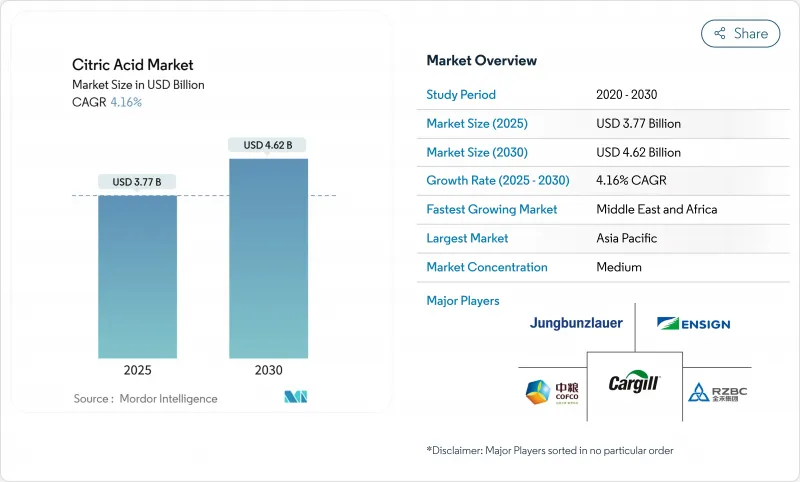

세계의 구연산 시장 규모는 2025년에는 37억 7,000만 달러로, 2030년에는 46억 2,000만 달러로 성장할 것으로 예측되고, CAGR은 4.16%로 견조하게 추이하고 있습니다.

클린 라벨 제품에 대한 소비자의 선호도 증가, 생명공학 프로세스의 진보, 음식, 의약품, 클리닝 제품 등의 산업에서의 다양화가 주로 이 성장을 추진하고 있습니다. 미국에서의 GRAS 상태와 유럽연합(EU)에서의 양자포화 승인을 포함한 규제의 명확화는 진입장벽을 계속 낮추고 시장 접근을 촉진하며 신규 진입기업 진입을 촉진하고 있습니다. 그러나 중국의 수입품에 대한 반덤핑 관세의 부과는 세계 조달 전략을 재구성하고 제조업체들에게 공급망 위험을 줄이기 위해 중국 이외의 지역에서 생산 능력 확대를 촉구하고 있습니다. 또한 공급망 전체의 수직 통합과 에너지 효율적인 발효 기술의 혁신으로 생산 효율과 비용 효율성이 향상되었습니다. 편의 음료, 생분해성 세척액, 발포성 의약품 및 기타 신흥 응용 분야에서 구연산 수요가 증가함에 따라 시장 범위가 더욱 확대되고 있습니다. 이러한 요인들로부터 구연산 시장의 잠재적인 성장력과 진화하는 규제, 기술, 소비자 주도의 동향에 대한 적응 능력이 뒷받침되고 있습니다.

세계 구연산 시장 동향과 통찰

탄산 음료에서 천연 산미료로 소비자 이동 증가

음료산업이 천연 산미료로 전환하는 동안 구연산은 클린 라벨 제품에 대한 노력에 힘입어 수요의 급증을 목격하고 있습니다. 구연산은 브라질에서 Normative Instruction 211/2023에 의해 첨가물로 승인되었습니다. 이 규칙은 0.1%에서 0.3% 사이에 설정된 음료에 대한 일반적인 첨가량을 규정하고 있으며 제조업체가 갈망했던 지침을 제공합니다. 이러한 규제의 명확화는 제형의 불확실성을 제거하는 것뿐만 아니라 브랜드가 자연 보존의 신용을 과시하는 힘을 제공합니다. 이 움직임은 성분표의 투명성과 단순화를 요구하는 소비자의 욕구 증가와 공명합니다. 구연산의 중요성은 천연 산미료로서의 주요 역할을 넘어섭니다. pH 조절제 및 방부제로서의 추가적인 기능을 통해 제조업체는 성분 배합을 간소화하면서 제품의 안정성을 높일 수 있습니다. 이 전략은 업계의 종합적인 목표인 규제 벤치마크 준수와 클린 라벨 제품에 대한 소비자의 요구와 일치합니다. 또한, 일류 음료 제조업체는 현재 의약품 등급 구연산에 기울고 있으며 일관된 품질과 시장 규정 준수의 중요성을 강조하고 있습니다. 인증된 고품질 구연산에 대한 이러한 수요 증가는 인증 공급업체에게 프리미엄 가격으로 가는 길을 열어줄 뿐만 아니라 시장에서의 경쟁과 혁신의 정신에 불을 붙인다.

즉시 섭취 음료에서 구연산 수요 증가

즉시 섭취 음료 시장은 강력한 성장을 이루고 있으며 다양한 용도로 구연산 수요를 크게 견인하고 있습니다. 구연산은 풍미 강화, 색 안정화, 보존 기간 연장 등 제품의 품질과 매력을 유지하기 위해 중요한 다기능 특성을 가지므로 중요한 성분이 되고 있습니다. 신흥 시장에서의 도시화의 진전은 편리성을 중시한 소비습관의 도입을 가속화하고, 즉시 섭취 음료에 큰 성장 기회를 가져오고 있습니다. 과일계 음료에서는 색조 보존제로서 구연산의 역할이 특히 중요하고, 시각적 어필, 소비자의 취향, 경쟁 시장에서의 브랜드 차별화에 직접 영향을 주기 때문입니다. 게다가 발효 기술의 진보는 생산 능력을 변화시켰습니다. 제조업체는 현재 아스페르길루스 니게르(Aspergillus niger)의 인공균주를 채용하여 174g/L을 초과하는 구연산 역가를 달성하고 있습니다. 이러한 혁신은 생산 효율성을 높이고 운영 비용을 절감하며 공급망의 신뢰성을 향상시킵니다. 그 결과 공급업체는 경쟁력 있는 가격 설정을 유지하면서 수요 증가에 대응할 수 있는 체제를 마련하고, 특히 가격에 민감한 신흥 부문에서 시장 확대를 촉진하고 있습니다.

신흥국의 원재료 가격 변동

원재료 비용의 변동은 구연산 공급 체인 전체에 큰 마진 압력이 되고 있으며, 옥수수, 사탕수수 당밀, 기타 탄수화물 공급원 등의 발효 기질이 특히 영향을 받고 있습니다. 이 변동은 신흥 시장에서 가장 두드러지며 농산물 가격은 예측 불가능한 날씨, 정책 개혁, 지정 긴장, 인프라 부족 등 외부 요인의 영향을 받기 쉽습니다. 투입비용 상승뿐만 아니라 제조업체는 환율변동과 물류비 증가에도 어려움을 겪고 있으며, 이로 인해 비용 관리가 더욱 복잡해지고 첨단 헤지 전략 채택이 필요합니다. 그러나 기질 이용 기술의 진보는 그것을 완화하는 유망한 길을 제공합니다. 최근 조사는 사탕수수 바가스, 치즈 유장, 기타 제품별 등 농업 폐기물의 흐름에서 구연산을 생산하는 데 성공했습니다. 이러한 혁신은 1차 제품 시장에 대한 의존도를 줄일 뿐만 아니라 지속가능성 목표에 부합하고 구연산 공급망의 강인성을 강화하는 비용 효율적이고 친환경적인 대안을 제공합니다.

부문 분석

2024년 무수 구연산은 55.35%의 점유율을 차지했으며, 계속 시장을 독점하고 있습니다. 탁월한 안정성, 보존 기간 연장, 다양한 최종 용도를 지원하는 확립된 공급망 인프라가 그 이유입니다. 그 결정 구조는 안정적인 품질을 보장하기 때문에 식품 제조 업체 및 제약 회사에 선호됩니다. 또한 산업 응용 분야에서는 예측 가능한 용해 속도와 제형화 공정에서 수분 관련 문제가 줄어들기 때문에 무수 형태가 선호됩니다. 그러나 가공 효율이 중요한 요소가 됨에 따라 시장은 점차 변화하고 있습니다. Jungbunzlauer의 CITROCOAT N과 같은 직접 압축 가능한 구연산은 의약품 정제화로 인기를 끌고 있습니다. 이러한 변종은 정제 경도 향상, 가공 시간 단축, 특정 용도의 성능 향상으로 업계 요구에 부응합니다.

액체 구연산 제제는 강력한 성장을 이루고 있으며, 2030년까지 CAGR은 6.82%로 예측되고 있습니다. 이 성장의 원동력이 되고 있는 것은 제조업체가 업무 효율과 비용의 최적화를 중시하게 되어 있는 것입니다. 액체 제제는 용해 공정이 필요 없기 때문에 자동화된 생산 시스템에서 정확한 투여 제어가 가능해져 제조 공정이 간소화됩니다. 이 동향은 특히 음료 산업에서 두드러지며, 액체 구연산은 시럽 제조 공정과 원활하게 통합되어 분말 취급과 관련된 오염 위험을 줄입니다. 또한 저장 및 운송 기술의 진보로 기존의 안정성에 대한 우려가 완화되어 액체 형태의 실현 가능성이 더욱 높아지고 있습니다. 이러한 개선에 의해 종래에는 무수 유형이 주류였던 용도에서의 액체 구연산의 채용이 확대되어, 예측 기간 중의 지속적인 성장이 기대되고 있습니다.

구연산 시장 보고서는 산업을 형태별(무수 및 액체), 용도별(식음료, 의약품, 퍼스널케어 및 화장품 등), 등급별(의약품 등급, 식품 등급, 산업 등급), 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류합니다. 각 부문에 대해 시장 세분화와 예측은 달러 기준입니다.

지역별 분석

2024년 아시아태평양 시장 점유율은 37.74%에 달했고, 이는 주로 중국의 견조한 생산 능력과 식품 가공 및 산업 분야에서의 국내 수요의 급증으로 인한 것입니다. 이 지역의 장점은 확립된 발효 인프라, 경쟁력 있는 생산 비용, 옥수수 및 사탕수수 유래와 같은 중요한 원료에 대한 근접 접근을 포함합니다. 그러나 무역 마찰과 안티 덤핑 조치가이 지역의 상황을 바꾸고 있습니다. 인도, 태국 및 기타 동남아시아 국가들은 국내 수요와 수출 수요 모두에 대응하기 때문에 생산 능력을 강화하고 있습니다. 일본의 정교한 의약품 및 식품 가공 부문은 유리한 시장 전망을 나타내고 호주의 급성장하는 음료 산업은 지역 소비를 뒷받침합니다.

중동 및 아프리카는 주목할 만한 지역으로 2030년까지 연평균 복합 성장률(CAGR)은 7.43%를 보일 것으로 예상됩니다. 이 성장의 주요 요인은 사우디아라비아 및 아랍에미리트(UAE)과 같은 국가에서 빠르게 성장하는 식품 가공 부문과 인프라 투자입니다. 식량 안보 강화 및 산업 다양화를 목표로 하는 이 지역 정부의 이니셔티브는 구연산의 새로운 수요 허브를 만들어 냅니다. NEOM이 Liberation Labs와 협력하여 정밀 발효 시설을 설립한 것은 이 지역의 고도 바이오 제조에 대한 의욕을 강조합니다. 한편, 북미와 유럽은 식품과 제약 부문이 정착하고 있으며, 시장 포화와 규제의 일관성에 의해 성장률이 억제되고 있는 것, 안정된 수요를 제공합니다.

식품, 음료, 퍼스널케어 분야 수요가 왕성한 유럽은 엄격한 품질 기준과 확립된 가공 시설에 지지되어 안정된 지위를 유지하고 있습니다. 북미는 즉시 섭취 음료, 편의점, 의약품의 급증에 견인되어 꾸준히 성장하고 있습니다. 이 지역의 소비자는 천연 보존제와 향미 조미료로 구연산을 사용하여 깨끗한 라벨의 원료에 점점 기울어지고 있습니다. 남미, 특히 브라질과 아르헨티나와 같은 국가에서는 식품 가공 부문의 확대와 포장 식품에 대한 선호도가 높아짐에 따라 성장하고 있습니다. 남미 제조업체는 구연산 생산을 위한 풍부한 농산물 원료라는 이중 이점을 누리고 있으며, 수입품에 대한 의존도도 낮아지고 있습니다. 유럽, 북미, 남미에서는 천연 첨가물을 우월하게 하는 규제 프레임워크가 구연산 시장의 가능성을 더욱 높여주고 있으며, 세계적인 대기업과 지역 기업 모두에게 기회를 제공합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 탄산음료에서 천연산미료에 대한 소비자 시프트의 고조

- 즉시 섭취 음료에서 구연산 수요 증가

- 발포성 의약품의 채용 증가

- 공업용 세정제에서 생분해성 킬레이트제에 대한 규제 증가

- 과자류에서 당질 삭감을 위한 개질 수요 고조

- 생산 공정의 혁신으로 수율 개선 및 비용 절감

- 시장 성장 억제요인

- 신흥국의 원재료 가격 변동

- 중국제 구연산에 대한 반덤핑 관세의 상승

- 대체 산미료와의 경쟁

- 감귤류의 가용성에 영향을 미치는 계절 변동

- 공급망 분석

- 규제 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 형태별

- 무수

- 액체

- 용도별

- 음식

- 베이커리

- 과자류

- 유제품

- 음료

- 세이보리 및 스낵

- 기타 음식

- 의약품

- 퍼스널케어 및 화장품

- 세제 및 가정용 클리너

- 기타

- 음식

- 등급별

- 의약품 등급

- 식품 등급

- 공업용 등급

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 칠레

- 페루

- 기타 남미

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 네덜란드

- 폴란드

- 벨기에

- 스웨덴

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 인도네시아

- 한국

- 태국

- 싱가포르

- 기타 아시아태평양

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 나이지리아

- 이집트

- 모로코

- 튀르키예

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 랭킹 분석

- 기업 프로파일

- Shandong Ensign Industry Co., Ltd.

- Jungbunzlauer Suisse AG

- COFCO Corporation

- RZBC Group Co., Ltd.

- TTCA Co., Ltd.

- Archer Daniels Midland Company

- Cargill, Incorporated

- Gadot Biochemical Industries Ltd.

- Foodchem International Corporation

- Merck KGaA

- Hawkins, Inc.

- Citrique Belge NV

- BBCA Group(Anhui BBCA)

- FUSO Chemical Co., Ltd.

- Wang Pharmaceuticals and Chemicals

- Hemadri Chemicals

- Vinipul Inorganics India Pvt. Ltd

- Arihant Chemicals

- Anmol Chemicals Private Limited

- Innova Corporate

제7장 시장 기회와 장래의 전망

JHS 25.11.21The Citric Acid market size is anticipated to be USD 3.77 billion in 2025, and is projected to grow to USD 4.62 billion by 2030, registering a steady CAGR of 4.16%.

The rising consumer preference for clean-label products, advancements in biotechnology processes, and the increasing diversification of applications across industries such as food and beverages, pharmaceuticals, and cleaning products primarily drive this growth. Regulatory clarity, including the GRAS status in the United States and quantum satis approval in the European Union, continues to lower entry barriers, fostering market accessibility and encouraging participation from new players. However, the imposition of anti-dumping duties on Chinese imports is reshaping global sourcing strategies, prompting manufacturers to expand production capacities in regions outside China to mitigate supply chain risks. Additionally, vertical integration across the supply chain and innovations in energy-efficient fermentation technologies are improving production efficiency and cost-effectiveness. The growing demand for citric acid in convenience beverages, biodegradable cleaning solutions, effervescent pharmaceuticals, and other emerging applications is further broadening its market scope. These factors collectively underscore the market's strong growth potential and its ability to adapt to evolving regulatory, technological, and consumer-driven trends.

Global Citric Acid Market Trends and Insights

Growing Consumer Shift to Natural Acidulants in Carbonated Soft Drinks

As the beverage industry pivots towards natural acidulants, citric acid is witnessing a surge in demand, largely fueled by a commitment to clean-label product reformulations. In Brazil, regulatory shifts have bolstered this momentum, with citric acid receiving the green light as an additive under Normative Instruction 211/2023. This regulation delineates typical dosages for beverages, set between 0.1% and 0.3%, offering manufacturers much-needed guidance. Such regulatory clarity not only dispels formulation uncertainties but also empowers brands to flaunt their natural preservation credentials. This move resonates with a growing consumer appetite for transparency and simplicity in ingredient lists. Citric acid's significance transcends its primary role as a natural acidulant. Its added functions as a pH regulator and preservative allow manufacturers to enhance product stability while streamlining ingredient formulations. This strategy dovetails with the industry's overarching objectives: adhering to regulatory benchmarks and aligning with consumer demands for clean-label offerings. Moreover, top-tier beverage manufacturers are now gravitating towards pharmaceutical-grade citric acid, underscoring the importance of consistent quality and market compliance. This heightened demand for certified, high-quality citric acid not only paves the way for premium pricing for certified suppliers but also ignites a spirit of competition and innovation in the market.

Increasing Demand for Citric Acid in Ready-to-drink Beverages

The ready-to-drink beverage market is experiencing robust growth, significantly driving the demand for citric acid across various applications. Citric acid is a key ingredient due to its multifunctional properties, including flavor enhancement, color stabilization, and shelf-life extension, which are critical for maintaining product quality and appeal. The increasing urbanization in emerging markets has accelerated the adoption of convenience-driven consumption habits, creating substantial growth opportunities for ready-to-drink beverages. In fruit-based beverages, citric acid's role as a color retention agent is particularly vital, as it directly influences visual appeal, consumer preferences, and brand differentiation in a competitive market. Additionally, advancements in fermentation technology have transformed production capabilities. Manufacturers are now employing engineered Aspergillus niger strains, achieving citric acid titers exceeding 174 g/L, a significant improvement over traditional methods. These innovations have enhanced production efficiency, reduced operational costs, and improved supply chain reliability. As a result, suppliers are well-positioned to meet the rising demand while maintaining competitive pricing, fostering market expansion, particularly in price-sensitive and emerging segments.

Price Volatility of Raw Materials in Emerging Countries

Fluctuations in raw material costs are exerting considerable margin pressures across the citric acid supply chain, with fermentation substrates such as corn, sugarcane molasses, and other carbohydrate sources being particularly impacted. This volatility is most evident in emerging markets, where agricultural commodity prices are highly susceptible to external factors, including unpredictable weather conditions, policy reforms, geopolitical tensions, and infrastructure deficiencies. Beyond the rising input costs, manufacturers are also grappling with currency fluctuations and increasing logistics expenses, which further complicate cost management and necessitate the adoption of sophisticated hedging strategies. However, advancements in substrate utilization technologies are providing a promising avenue for mitigation. Recent research highlights the successful production of citric acid from agricultural waste streams, such as sugarcane bagasse, cheese whey, and other by-products. These innovations not only reduce dependence on primary commodity markets but also align with sustainability goals, offering a cost-effective and environmentally friendly alternative that strengthens the resilience of the citric acid supply chain.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption in Effervescent Pharmaceuticals

- Rise in Regulatory Push for Biodegradable Chelating Agents in Industrial Cleaners

- Rise in Anti-dumping Duties on Chinese Citric Acid

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, anhydrous citric acid continues to dominate the market with a 55.35% share, attributed to its superior stability, extended shelf life, and well-established supply chain infrastructure supporting diverse end-use applications. Its crystalline structure ensures consistent quality, making it a preferred choice for food manufacturers and pharmaceutical companies. Industrial applications also favor anhydrous forms due to their predictable dissolution rates and reduced moisture-related challenges during formulation processes. However, the market is gradually shifting as processing efficiency becomes a critical factor. Direct compressible citric acid variants, such as Jungbunzlauer's CITROCOAT N, are gaining traction in pharmaceutical tableting. These variants address industry needs by offering improved tablet hardness, faster processing times, and enhanced performance in specific applications.

Liquid citric acid formulations are witnessing robust growth, with a projected CAGR of 6.82% through 2030. This growth is driven by manufacturers' increasing focus on operational efficiency and cost optimization. The liquid form eliminates the need for dissolution steps, enabling precise dosing control in automated production systems and streamlining manufacturing processes. This trend is particularly prominent in the beverage industry, where liquid citric acid integrates seamlessly with syrup preparation processes, reducing contamination risks associated with powder handling. Additionally, advancements in storage and transportation technologies have mitigated traditional stability concerns, further enhancing the viability of liquid forms. These improvements are expanding the adoption of liquid citric acid in applications that were previously dominated by anhydrous variants, positioning the segment for sustained growth in the forecast period.

The Citric Acid Market Report Segments the Industry by Form (Anhydrous and Liquid); by Application (Food and Beverage, Pharmaceuticals, Personal Care and Cosmetics, and More); by Grade (Pharmaceutical Grade, Food Grade, and Industrial Grade); and by Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). For Each Segment, The Market Sizing and Forecasts Have Been Based On Values in USD.

Geography Analysis

In 2024, Asia-Pacific commands a 37.74% market share, largely due to China's robust production capabilities and its surging domestic appetite in food processing and industrial sectors. The region's advantages include a well-established fermentation infrastructure, competitive production costs, and close access to vital raw materials like corn and sugarcane derivatives. Yet, trade tensions and anti-dumping measures are altering the regional landscape. Countries like India, Thailand, and other Southeast Asian nations are ramping up production capacities to cater to both local and export demands. Japan's sophisticated pharmaceutical and food processing sectors present lucrative market prospects, while Australia's burgeoning beverage industry bolsters regional consumption.

Middle East and Africa is the region to watch, boasting a 7.43% CAGR through 2030. This growth is largely attributed to the burgeoning food processing sectors and infrastructural investments in nations such as Saudi Arabia and the UAE. Government initiatives in the region, aimed at bolstering food security and diversifying industries, are birthing new demand hubs for citric acid. NEOM's collaboration with Liberation Labs to set up precision fermentation facilities underscores the region's ambition in advanced biomanufacturing. Meanwhile, North America and Europe, with their entrenched food and pharmaceutical sectors, offer stable demand, albeit with tempered growth rates due to market saturation and regulatory consistency.

Europe, with its robust demand from the food, beverage, and personal care sectors, remains a stable player, bolstered by stringent quality standards and established processing facilities. North America's growth is steady, driven by a surge in ready-to-drink beverages, convenience foods, and pharmaceuticals. Consumers here increasingly lean towards clean-label ingredients, using citric acid as a natural preservative and flavor enhancer. South America, particularly in nations like Brazil and Argentina, is on the rise, thanks to its expanding food processing sectors and a growing appetite for packaged foods. South American manufacturers enjoy the dual advantage of abundant agricultural feedstocks for citric acid production and a reduced reliance on imports. Across Europe, North America, and South America, regulatory frameworks that favor natural additives further enhance citric acid's market potential, presenting opportunities for both global giants and local players.

- Shandong Ensign Industry Co., Ltd.

- Jungbunzlauer Suisse AG

- COFCO Corporation

- RZBC Group Co., Ltd.

- TTCA Co., Ltd.

- Archer Daniels Midland Company

- Cargill, Incorporated

- Gadot Biochemical Industries Ltd.

- Foodchem International Corporation

- Merck KGaA

- Hawkins, Inc.

- Citrique Belge NV

- BBCA Group (Anhui BBCA)

- FUSO Chemical Co., Ltd.

- Wang Pharmaceuticals and Chemicals

- Hemadri Chemicals

- Vinipul Inorganics India Pvt. Ltd

- Arihant Chemicals

- Anmol Chemicals Private Limited

- Innova Corporate

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing consumer shift to natural acidulants in carbonated soft drinks

- 4.2.2 Increasing demand for citric acid in ready-to-drink beverages

- 4.2.3 Rising adoption in effervescent pharmaceuticals

- 4.2.4 Rise in regulatory push for biodegradable chelating agents in industrial cleaners

- 4.2.5 Increasing need for sugar-reduction reformulation in confectionery

- 4.2.6 Innovations in production processes are improving yield and reducing costs.

- 4.3 Market Restraints

- 4.3.1 Price volatility of raw materials in emerging countries

- 4.3.2 Rise in anti-dumping duties on chinese citric acid

- 4.3.3 Competition from alternative acidulants.

- 4.3.4 Seasonal variations impacting citrus fruit availability.

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Form

- 5.1.1 Anhydrous

- 5.1.2 Liquid

- 5.2 By Application

- 5.2.1 Food and Beverage

- 5.2.1.1 Bakery

- 5.2.1.2 Confectionery

- 5.2.1.3 Dairy

- 5.2.1.4 Beverages

- 5.2.1.5 Savory and Snacks

- 5.2.1.6 Other Foods and Beverages

- 5.2.2 Pharmaceuticals

- 5.2.3 Personal Care and Cosmetics

- 5.2.4 Detergents and Household Cleaners

- 5.2.5 Others

- 5.2.1 Food and Beverage

- 5.3 By Grade

- 5.3.1 Pharmaceutical Grade

- 5.3.2 Food Grade

- 5.3.3 Industrial Grade

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Colombia

- 5.4.2.4 Chile

- 5.4.2.5 Peru

- 5.4.2.6 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Netherlands

- 5.4.3.6 Poland

- 5.4.3.7 Belgium

- 5.4.3.8 Sweden

- 5.4.3.9 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 Indonesia

- 5.4.4.6 South Korea

- 5.4.4.7 Thailand

- 5.4.4.8 Singapore

- 5.4.4.9 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Shandong Ensign Industry Co., Ltd.

- 6.4.2 Jungbunzlauer Suisse AG

- 6.4.3 COFCO Corporation

- 6.4.4 RZBC Group Co., Ltd.

- 6.4.5 TTCA Co., Ltd.

- 6.4.6 Archer Daniels Midland Company

- 6.4.7 Cargill, Incorporated

- 6.4.8 Gadot Biochemical Industries Ltd.

- 6.4.9 Foodchem International Corporation

- 6.4.10 Merck KGaA

- 6.4.11 Hawkins, Inc.

- 6.4.12 Citrique Belge NV

- 6.4.13 BBCA Group (Anhui BBCA)

- 6.4.14 FUSO Chemical Co., Ltd.

- 6.4.15 Wang Pharmaceuticals and Chemicals

- 6.4.16 Hemadri Chemicals

- 6.4.17 Vinipul Inorganics India Pvt. Ltd

- 6.4.18 Arihant Chemicals

- 6.4.19 Anmol Chemicals Private Limited

- 6.4.20 Innova Corporate