|

시장보고서

상품코드

1851273

컨테이너형 데이터센터 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Containerized Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

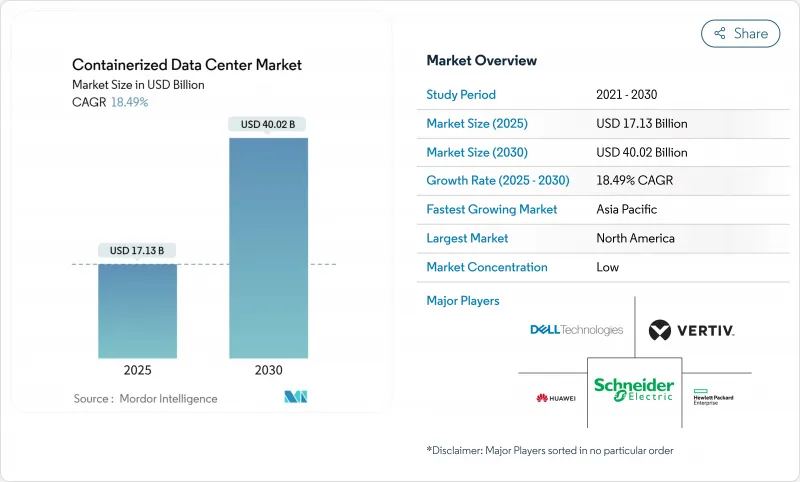

컨테이너형 데이터센터 시장은 2025년에 171억 3,000만 달러에 이르고, 2030년에는 400억 2,000만 달러에 달할 것으로 예상되며, CAGR은 18.49%를 나타낼 전망입니다.

5G 배포, 엣지 컴퓨팅, 보다 엄격한 지속가능성 의무화로 신속한 배포 용량에 대한 수요가 급증하고 주문장부의 장기화가 계속되고 있습니다. 하이퍼스케일 운영자는 수년간의 건설 지연을 채우기 위해 컨테이너 모듈을 사용하고 기업은 데이터 주권 규칙을 충족하기 위해 컨테이너 모듈을 도입합니다. 조립식의 효율성은 전력 사용 효율(PUE) 마진을 단축하고 총 소유 비용을 낮추고 이동성을 경쟁 차별화 요인으로 만듭니다. 공급업체는 액체 냉각, 열 회수, 원자력 또는 수소 마이크로그리드를 결합하여 잉여 전력을 회수하고 컨테이너형 데이터센터 시장을 지속적인 2자리 확장을 위해 배치하고 있습니다.

세계의 컨테이너형 데이터센터 시장 동향과 인사이트

엣지/5G 구축으로 마이크로 사이트가 가속

통신 캐리어는 초저지연 서비스를 지원하기 위해 수천 개의 마이크로 에지 노드를 배포하고 있으며 주문부터 '켜짐'까지 몇 주 내에 완료되는 모듈형 유닛을 선택합니다. 2024년 5월 ANSI/TIA-942-C 업데이트를 통해 A형과 B형 마이크로 에지 등급을 작성하여 운영자는 통합된 컴플라이언스 경로를 확보하여 조달 주기를 가속화했습니다. 컨테이너 폼 팩터를 통해 공급자는 커버리지 맵의 진화에 맞게 용량을 재배치할 수 있어, 밀집한 도시의 중심에서도 지역 간극에서도 컨테이너형 데이터센터 시장의 존재를 강화할 수 있습니다. 수요는 자율주행차, 산업용 IoT, AR/VR 및 이들 모두 네트워크 에지에서 일관된 10밀리초 이하의 레이턴시를 필요로 합니다. 공급업체는 현재 5G 라디오, MEC 서버 및 배터리 스토리지를 단일 리프트 유닛으로 번들하여 배포 타임라인과 자본 위험을 압축합니다. 5G의 고밀도화가 2026년에 피크를 맞이하는 가운데, 민간 네트워크 프로젝트의 제2파가 마이크로사이트의 파이프라인을 활성화시킬 것으로 보입니다.

Tier 1 허브 용량 부족

버지니아 북부, 실리콘 밸리, 런던의 토지, 전력 및 허가 병목 현상으로 인해 새로운 하이퍼스케일 프로젝트는 2028년 커미셔닝 창으로 몰려 들었으며, 사업자는 8 - 12 주 동안 생산할 수있는 잠정적 인 모듈 형 용량을 임대해야합니다. 따라서 컨테이너형 데이터센터 시장은 일시적인 오버플로에서 전략적 실적로 이동하여 클라우드 기업이 그리드 제약에도 불구하고 고객의 SLA를 유지할 수 있도록 합니다. 버지니아 주 부동산 투자자들은 변전소 업그레이드 근처에 위치한 모듈러 캠퍼스 입주 프리미엄이 20%를 초과했다고 보고했습니다. 기업은 모듈을 권리의 지연과 송전망 정지에 대한 보험으로 간주하고, 상설 홀이 온라인이 되면 많은 기업이 유닛의 재배치를 계획하고 있습니다.

제한된 랙 밀도와 하이퍼스케일 요구

ISO의 40피트 박스는 일반적으로 랙당 10-15kW를 지원하며, 단일 모듈에서 60-180kW의 IT 전력을 상한으로 하는 반면, 전용 하이퍼스케일 스위트는 20-40kW의 밀도를 가지며, 동등한 바닥 면적에서 300-500kW에 이릅니다. 따라서 랙당 수백 개의 GPU를 필요로 하는 AI 및 HPC 클러스터는 여러 컨테이너와 특수 액체 냉각을 개조해야 하며 MW당 자본 비용이 증가합니다. 도쿄와 프랑크푸르트와 같은 1제곱미터마다 비싼 부동산 시장에서는 밀도 차이가 더욱 커집니다. 벤더는 침지형 콜드 플레이트 설계로 이에 대응하고 있지만, 도입의 실증 포인트는 아직 한정되어 있습니다. 밀도가 동등해질 때까지 일부 하이퍼스케일 아키텍트는 컨테이너형 시스템을 주변기기나 과도적인 부하용으로 확보할 것으로 보입니다.

부문 분석

2024년 컨테이너형 데이터센터 시장 점유율의 78.2%는 구매 옵션이 차지하고 BFSI나 정부에 의한 자산 관리의 의무화가 그 요인이 되었습니다. 그러나 임대/「White-Space-as-a-Service」는 CAGR 20.1%를 나타낼 전망입니다. 조기 도입 기업은 번들 모니터링 및 새로 고침 서비스가 직원 부담을 줄이고 기술의 진부화 위험을 줄이는 데 주목하고 있습니다. 휴렛 팩커드 엔터프라이즈의 Facility-as-a-Service는 다년간의 성능 SLA를 보장하며 기존 벤더가 구독의 경제성을 받아들이고 있음을 보여줍니다.

임대는 중견 기업을 위한 고도의 용량을 민주화하고 2차 메트로 및 에지 이용 사례에서 컨테이너형 데이터센터 시장 실적를 확대합니다. 신흥 기업은 초기 투자를 피할 수 있으며 대기업은 잔존 가치 위험을 줄일 수 있습니다. 기간이 끝나면 모듈을 반환, 재배치 및 교체할 수 있는 유연성도 급변하는 AI 워크로드 프로파일에 적합합니다. 구매 모델은 보안 분류 및 맞춤 엔지니어링이 임대의 편의성을 초과하는 경우 지속될 것으로 보입니다.

ISO 40피트 쉘은 2024년 컨테이너형 데이터센터 시장 규모의 54.6%를 차지하며, 세계 화물 표준과 랙당 비용 절감의 이점을 누렸습니다. CAGR 19.7%로 성장하는 커스터마이즈/올인원 스키드는 랙 수 증가, 칩으로의 직접 냉각, 온보드 UPS를 통합하여 AI 및 분석 클러스터에 어필합니다. UL 2755 인증은 고정 설비와 동등한 안전성을 보장하고 기업의 조달 장애물을 완화합니다.

맞춤형 열 봉투에 대한 수요로 인해 공급업체는 30kW 이상의 랙과 열 재사용 루프를 비표준 실적에 설계하여 평균 판매 가격이 상승하면서 그린필드 홀에 비해 도입 기간이 단축됩니다. 2026년 이후 랙의 전력이 증가함에 따라 많은 하이퍼스케일 아키텍트는 재생에너지 공급 지점 근처에 GPU를 설치하는 유일한 현실적인 경로로 맞춤 스키드를 생각하고 있습니다. ISO 20 피트 박스는 틈새 시장이지만 텔레콤 에지 쉼터와 공간에 제약을 받는 도시 옥상에는 여전히 적합합니다.

컨테이너형 데이터센터 시장은 소유 유형(구매, 임대/"White-Space-As-A-Service"), 컨테이너 유형(ISO 20-Ft, ISO 40-Ft, 커스터마이즈/올인원 스키드), 전개 장소(코어/캠퍼스, 에지/마이크로, 원격/가혹한 환경), 최종 사용자 산업(IT 및 통신, BFSI 등), 지역 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 2024년 매출의 29.3%를 차지하며, 텍사스, 조지아, 앨버타에서 암호화 광산의 AI 캠퍼스로의 하이퍼스케일 전환이 그 주인이 되었습니다. 미국은 새로운 그리드 인터커넥트를 위해 몇 년 동안 기다리는 백로그를 피하기 위해 모듈을 흡수하고 캐나다는 타르 샌드 모니터링과 북극 광대역 게이트웨이에 견고한 포드를 채택했습니다. 멕시코의 니어 쇼어링 르네상스를 통해 마키라 도라 공장의 소유자는 미국의 물류 허브와 실시간 품질 데이터를 동기화하는 에지 포드를 도입했습니다. 이러한 추세로 인해 컨테이너형 데이터센터 시장은 대륙을 가로지르는 전략적 오버레이로 강화됩니다.

아시아태평양은 CAGR 18.5%로 가장 급성장하고 있는 지역으로 중국, 인도, ASEAN에서 5G의 매크로 구축과 스마트 시티의 시험 운용이 확대되고 있습니다. 각 국가는 컨테이너 클러스터를 앞뒤로 허용합니다. 인도의 데이터 현지화 룰북은 클라우드 제공업체가 시민 데이터를 소비 지역 근처로 둘러싸도록 하여 마이크로 지역 포드에 대한 수요를 높입니다. 일본과 호주는 철골 모듈 특유의 내진성과 사이클론 내성을 높이 평가했습니다. 이러한 다양한 요인이 이 지역의 주문 파이프라인을 견고하게 만듭니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 휴대성과 신속한 전개

- 엣지/5G의 구축이 마이크로 사이트를 가속

- Tier 1 허브의 데이터센터용량 부족

- 에너지 효율이 높은 프리팹이 TCO를 삭감

- SMR에 의한 마이크로그리드가 오프 그리드 DC를 가능

- 암호에서 AI로의 사이트 변환이 좌초 전력을 해방

- 시장 성장 억제요인

- 제한된 랙과 컴퓨팅 밀도 대 하이퍼스케일 요구

- 레거시 DC와의 통합 복잡성

- ISO 컨테이너공급망 병목

- 액냉의 레트로핏이 CAPEX를 상승

- 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 라이벌의 격렬함

- 시장의 거시경제 요인 평가

제5장 시장 규모와 성장 예측

- 소유 유형별

- 구매

- 임대/White-Space-as-a-Service

- 컨테이너 유형별

- ISO 20-ft

- ISO 40-ft

- 맞춤형/올인원 스키드

- 배포 지역별

- 코어/캠퍼스

- 엣지/마이크로

- 원격/가혹 환경

- 최종 사용자 업계별

- IT 및 통신

- BFSI

- 정부 및 방위

- 헬스케어

- 교육

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Vertiv

- Schneider Electric

- Huawei Technologies

- Dell Technologies

- Hewlett Packard Enterprise

- IBM Corporation

- Cisco Systems

- Rittal GmbH and Co. KG

- Delta Electronics

- Eaton Corporation

- Johnson Controls

- PCX Corporation

- BMarko Structures

- Baselayer Technology

- Flexenclosure(Xerxes)

- Cirrascale Cloud Services

- ZTE Corporation

- AST Modular(subs. of Schneider)

- Cannon Technologies

- EdgeMicro/EDJX

- Compass Datacenters

- EdgeConneX

- Vertiv(Emerson Network Power legacy)

- Stulz GmbH

제7장 시장 기회와 향후 전망

KTH 25.11.12The containerized data center market stood at USD 17.13 billion in 2025 and is forecast to reach USD 40.02 billion by 2030, advancing at an 18.49% CAGR.

Surging demand for rapid-deployment capacity, driven by 5G rollouts, edge computing, and stricter sustainability mandates, continues to lengthen order books. Hyperscale operators use container modules to bridge multi-year construction lags, while enterprises deploy them to meet data-sovereignty rules. Prefabricated efficiencies are tightening power usage effectiveness (PUE) margins and lowering total cost of ownership, making mobility a competitive differentiator. Vendors combine liquid cooling, heat-recovery, and nuclear or hydrogen micro-grids to unlock stranded power, positioning the containerized data center market for sustained double-digit expansion.

Global Containerized Data Center Market Trends and Insights

Edge/5G build-outs accelerate micro-sites

Telecom carriers are rolling out thousands of micro edge nodes to support ultra-low-latency services, choosing modular units that move from purchase order to "lights on" in weeks. The May 2024 ANSI/TIA-942-C update created Type A and Type B micro-edge ratings, giving operators a uniform compliance path and accelerating procurement cycles. Container form factors let providers relocate capacity as coverage maps evolve, strengthening the containerized data center market presence in dense urban cores and rural gaps alike. Demand spans autonomous vehicles, industrial IoT, and AR/VR, all of which require consistent sub-10 ms latency at the network edge. Vendors now bundle 5G radios, MEC servers, and battery storage into single-lift units, compressing deployment timelines and capital risk. As 5G densification peaks in 2026, a second wave of private-network projects will keep micro-site pipelines active.

Capacity shortages in Tier-1 hubs

Land, power, and permitting bottlenecks in Northern Virginia, Silicon Valley, and London have pushed new hyperscale projects into 2028 commissioning windows, forcing operators to lease interim modular capacity that can be live in 8-12 weeks. The containerized data center market thus shifts from temporary overflow to strategic footprint, enabling cloud firms to preserve customer SLAs despite grid constraints. Real-estate investors in Virginia report occupancy premiums topping 20% for modular campuses positioned near substation upgrades. Enterprises view the modules as insurance against entitlement delays and grid curtailments, and many plan to redeploy units once permanent halls come online.

Limited rack density vs hyperscale needs

ISO 40-foot boxes typically support 10-15 kW per rack, capping a single module at 60-180 kW IT power, whereas purpose-built hyperscale suites reach 20-40 kW densities and 300-500 kW in comparable floor area. AI and HPC clusters demanding hundreds of GPUs per rack therefore require multiple containers or specialized liquid-cooling retrofits, inflating capital cost per MW. The density gap is magnified in high-real-estate markets like Tokyo and Frankfurt, where every square meter carries a premium. Vendors answer with immersed cold-plate designs, yet deployment proof points remain limited. Until density parity closes, some hyperscale architects will reserve containerized systems for peripheral or transitional loads.

Other drivers and restraints analyzed in the detailed report include:

- Energy-efficient prefabrication lowers TCO

- SMR-powered micro-grids enable off-grid DCs

- Legacy estate integration complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Purchase option held 78.2% of containerized data center market share in 2024, fueled by BFSI and government mandates for asset control. However, Lease/"White-Space-as-a-Service" is growing at 20.1% CAGR as CFOs pivot to OpEx models that track utilization. Early adopters note that bundled monitoring and refresh services reduce staffing burdens and de-risk technology obsolescence. Hewlett Packard Enterprise's Facility-as-a-Service offering guarantees performance SLAs over multi-year terms, signaling that incumbent vendors embrace subscription economics.

Leasing democratizes high-spec capacity for mid-tier firms, swelling the containerized data center market footprint across secondary metros and edge use cases. Start-ups avoid upfront capital outlays, while large enterprises offload residual-value risk. The flexibility to return, relocate, or swap modules after the term also fits volatile AI workload profiles. Purchase models will persist where security classification or custom engineering outweigh leasing's convenience, yet the service curve is poised to steepen through 2030.

ISO 40-foot shells retained 54.6% of containerized data center market size in 2024, benefiting from global freight standards and lower per-rack cost. Customized/All-in-One Skids, advancing at 19.7% CAGR, integrate higher rack counts, direct-to-chip liquid cooling, and on-board UPS, appealing to AI and analytics clusters. UL 2755 certification assures safety parity with fixed facilities, easing enterprise procurement hurdles.

Demand for bespoke thermal envelopes pushes vendors to engineer 30 kW-plus racks and heat-reuse loops inside nonstandard footprints, lifting average selling price yet compressing deployment times compared with greenfield halls. As rack power escalates post-2026, many hyperscale architects view custom skids as the only pragmatic route to situate GPUs near renewable feed-in points. ISO 20-foot boxes, while niche, remain relevant for telecom edge shelters and space-constrained urban rooftops.

Containerized Data Center Market is Segmented by Ownership Type ( Purchase, Lease / "White-Space-As-A-Service"), Container Type (ISO 20-Ft, ISO 40-Ft, Customized/All-in-One Skids), Deployment Location ( Core / Campus, Edge / Micro, Remote / Harsh-Environment), End User Industry (IT and Telecommunications, BFSI and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 29.3% of 2024 revenue, anchored by hyperscale conversions of crypto mines into AI campuses across Texas, Georgia, and Alberta. The United States absorbs modules to circumvent multi-year queue backlogs for new grid interconnects, while Canada employs ruggedized pods for tar-sand monitoring and Arctic broadband gateways. Mexico's near-shoring renaissance drives maquiladora plant owners to install edge pods that sync real-time quality data with US logistics hubs. Together these trends reinforce the containerized data center market as a strategic overlay across the continent.

Asia-Pacific, the fastest-growing region at 18.5% CAGR, scales 5G macro builds and smart-city pilots across China, India, and ASEAN. Provinces grant accelerated permits for container clusters that can later shift sites as urban plans evolve. India's data-localization rulebook boosts demand for micro-regional pods, allowing cloud providers to ring-fence citizen data near consumption zones. Japan and Australia value seismic and cyclone resilience inherent in steel-framed modules. Collectively, diversified drivers keep the region's order pipeline robust.

- Vertiv

- Schneider Electric

- Huawei Technologies

- Dell Technologies

- Hewlett Packard Enterprise

- IBM Corporation

- Cisco Systems

- Rittal GmbH and Co. KG

- Delta Electronics

- Eaton Corporation

- Johnson Controls

- PCX Corporation

- BMarko Structures

- Baselayer Technology

- Flexenclosure (Xerxes)

- Cirrascale Cloud Services

- ZTE Corporation

- AST Modular (subs. of Schneider)

- Cannon Technologies

- EdgeMicro / EDJX

- Compass Datacenters

- EdgeConneX

- Vertiv (Emerson Network Power legacy)

- Stulz GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Portability and rapid deployment

- 4.2.2 Edge/5G build-outs accelerate micro-sites

- 4.2.3 Data-center capacity shortages in Tier-1 hubs

- 4.2.4 Energy-efficient prefabrication lowers TCO

- 4.2.5 SMR-powered micro-grids enable off-grid DCs

- 4.2.6 Crypto-to-AI site conversions unlock stranded power

- 4.3 Market Restraints

- 4.3.1 Limited rack and compute density vs hyperscale needs

- 4.3.2 Integration complexity with legacy DC estates

- 4.3.3 ISO-container supply-chain bottlenecks

- 4.3.4 Liquid-cooling retrofits raise CAPEX

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Ownership Type

- 5.1.1 Purchase

- 5.1.2 Lease / White-Space-as-a-Service

- 5.2 By Container Type

- 5.2.1 ISO 20-ft

- 5.2.2 ISO 40-ft

- 5.2.3 Customized/All-in-One Skids

- 5.3 By Deployment Location

- 5.3.1 Core / Campus

- 5.3.2 Edge / Micro

- 5.3.3 Remote / Harsh-Environment

- 5.4 By End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Government and Defense

- 5.4.4 Healthcare

- 5.4.5 Education

- 5.4.6 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Netherlands

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Vertiv

- 6.4.2 Schneider Electric

- 6.4.3 Huawei Technologies

- 6.4.4 Dell Technologies

- 6.4.5 Hewlett Packard Enterprise

- 6.4.6 IBM Corporation

- 6.4.7 Cisco Systems

- 6.4.8 Rittal GmbH and Co. KG

- 6.4.9 Delta Electronics

- 6.4.10 Eaton Corporation

- 6.4.11 Johnson Controls

- 6.4.12 PCX Corporation

- 6.4.13 BMarko Structures

- 6.4.14 Baselayer Technology

- 6.4.15 Flexenclosure (Xerxes)

- 6.4.16 Cirrascale Cloud Services

- 6.4.17 ZTE Corporation

- 6.4.18 AST Modular (subs. of Schneider)

- 6.4.19 Cannon Technologies

- 6.4.20 EdgeMicro / EDJX

- 6.4.21 Compass Datacenters

- 6.4.22 EdgeConneX

- 6.4.23 Vertiv (Emerson Network Power legacy)

- 6.4.24 Stulz GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment