|

시장보고서

상품코드

1851297

제스처 인식 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Gesture Recognition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

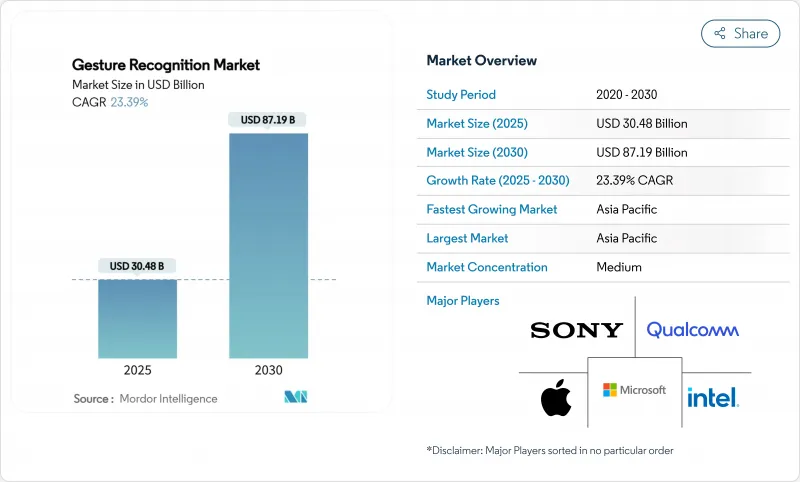

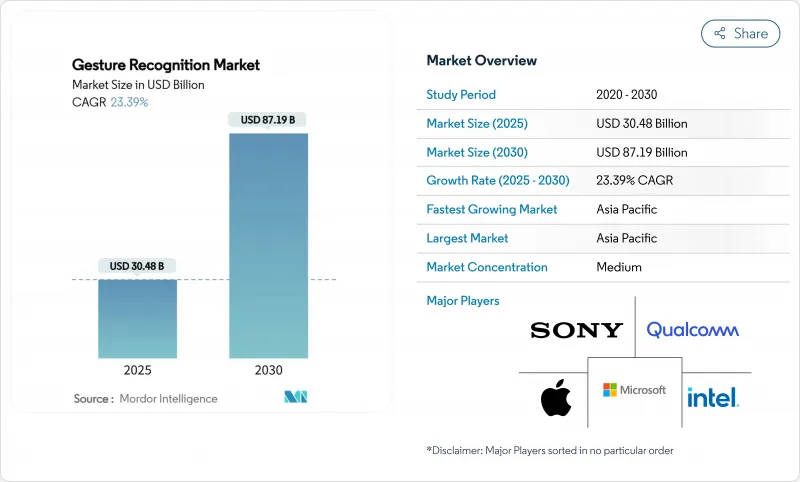

제스처 인식 시장 규모는 2025년 304억 8,000만 달러로 추정되고, 예측 기간(2025-2030년)의 CAGR은 23.39%로, 2030년에는 871억 9,000만 달러에 달할 것으로 예상됩니다.

이 지속적인 확장은 고급 mm파 레이더, 멀티존 ToF(Time-of-Flight) 센서, 에지 AI 알고리즘이 융합되어 스마트폰, 자동차, 의료기기, 산업기기에서 응답성이 높은 저지연의 휴먼 머신 인터페이스를 실현하고 있음을 반영합니다. 고급 휴대단말에 있어서 센서 출하의 가속, 자동차 안전 시스템에 대한 규제 압력, 헬스 케어에 있어서 감염 제어의 필요성 등이 더해져, 양적 수요를 자극하고 있습니다. 동시에, 제스처 인식 시장에서는 하드웨어 중심의 솔루션에서 상호작용을 개인화하고, 오감지를 줄이고, 디바이스 수명을 연장하는 소프트웨어와 AI 스택으로의 가치 전환을 볼 수 있습니다. 미국의 CHIPS 법과 유럽의 Chips 법으로 대표되는 지역적인 제조 장려책은 공급망을 재구축하고 현지 부품 제조에 새로운 비용 우위를 창출하고 있습니다. 이러한 요인이 수렴함에 따라 센서, 소프트웨어, 클라우드 오케스트레이션의 각 레이어를 수직 통합하는 업계 진출기업은 제스처 인식 시장에서 불균형한 리턴을 획득할 수 있는 입장에 있습니다.

세계의 제스처 인식 시장 동향과 인사이트

아시아의 플래그십 스마트폰에 mm파 센서와 ToF 센서가 보급

아시아에 기반을 둔 휴대폰 OEM은 현재 ST 마이크로 일렉트로닉스의 VL53L7CX와 같은 멀티존 ToF 모듈을 통합하여 주변광의 제약 없이 mm 레벨의 깊이 정밀도를 실현하여 엄격한 조명 하에서도 신뢰성 높은 공중 명령 입력을 가능하게 하고 있습니다. Ceva의 MotionEngine Hex 펌웨어는 관성 데이터와 레이더 데이터를 통합하여 사용자 인터페이스의 공간 제어를 실현합니다. ToF 칩셋 비용이 대량 로트 단위당 1달러 미만으로 떨어지면서 제스처 컨트롤은 제스처 인식 시장에서 프리미엄 차별화 요인에서 기본 기능으로 전환하고 있습니다.

자동차 제조업체에 의한 차내 제스처 HUD의 채용이 유로 NCAP의 의무에 적합에

2024년 7월 첨단 운전자 주의력 산만 경고 규제로 OEM은 인지 부하를 줄여야 하며 유럽 모델에 카메라 기반 제스처 허브를 신속하게 통합하고 있습니다. BMW의 7시리즈에서 레벨 2/3 인증은 상업적 준비 태세를 나타내며, 아우디의 3차원 조종석 인터페이스는 콘솔 상단의 손 스윕을 사용한 멀티모달 인포테인먼트 선택을 보여줍니다. 150ms 이하의 응답 시간과 3% 미만의 오감지율을 보장할 수 있는 공급업체는 프로그램 상을 수상할 수 있어 제스처 인식 시장의 성장 궤도를 강화하고 있습니다.

열대 지역의 비전 기반 시스템에서 태양광 하에서 높은 오 검출율

카메라 중심의 알고리즘은 고휘도 배경에 대한 손 윤곽의 해상에 고전하고, 야외 키오스크나 라이드 헤일링 차량에서 에러가 급증. 조사에 따르면 레이더 기반 대체 시스템은 조명에 관계없이 90% 이상의 정확도를 유지하므로 시스템 설계자는 제스처 인식 시장에서 멀티 센서 퓨전을 채택해야 합니다.

부문 분석

터치리스 솔루션은 2024년 매출의 58.2%를 차지하며 엔드 시장이 위생, 운전자 안전, 몰입형 엔터테인먼트를 중시하고 있음을 반영했습니다. 터치리스 하위 부문은 2030년까지 24.4%를 나타내 ToF, mm파 레이더, 초음파 어레이의 재료비 삭감에 의해 보다 넓은 제스처 인식 시장을 상회합니다. 이와는 대조적으로 커패시턴스 터치 컨트롤은 비용에 민감한 소비자 디바이스에서 중요성을 유지하지만 CAGR은 한 자리에 머물러 있습니다. 교세라의 깊이 센서는 10cm 이내에 100μm의 해상도를 나타내며 수술 수준의 정확도가 요구되는 로봇의 픽앤플레이스 및 정형외과의 정렬 도구를 가능하게 합니다. 주변과의 상호 작용으로의 꾸준한 전환은 터치리스 모달리티가 궁극적으로 접촉에 의존하는 선행 제품보다 큰 점유율을 차지한다는 것을 시사합니다.

터치리스의 확대는 공급자의 힘 다이어그램에 변화를 가져옵니다. 지금까지 실리콘을 상품화해 온 센서 벤더는 현재 AI 펌웨어, 데이터 모델, 개발자 포털을 번들해 하드웨어 마진에 더해 정기적인 라이선스료를 획득하고 있습니다. 이러한 재번들은 현장 업그레이드가 가능한 무선에서의 성능 향상을 요구하는 OEM의 우선순위와 일치하며, 제스처 인식 시장에서 터치리스의 대량 도입에 필요한 확장 가능한 경제성을 지원하고 있습니다.

2024년 제스처 인식 시장 규모의 71.5%는 하드웨어가 차지하고 있어 렌즈, 레이더 프론트엔드, MCU의 고유 비용이 그 요인이 되었습니다. 그러나 컨텍스트 인식, 사용자 적응, 연계 학습을 실현하는 소프트웨어 플랫폼은 CAGR 23.7%를 나타낼 것으로 예측되고 있으며 하드웨어 성장률을 350bps 이상 웃돌고 있습니다. 인피니언의 DEEPCRAFT Ready Models는 일반적인 제스처를 위해 사전 훈련된 신경망을 제공하여 통합 시간을 40% 단축하고, 가치 곡선이 높은 위치에 회사를 재배치합니다. 한편, Imagimob의 시각 그래프 기반 ML 툴은 모델 개발 사이클을 몇 시간으로 압축하고 중견 OEM의 AI 최적화를 민주화합니다.

수익 구성의 변화로 인해 예측 유지보수, 클라우드 기반 분석, 제스처를 통한 디지털 구매를 통한 인앱 돈 관리 등 서비스 번들링 기회가 생깁니다. 실리콘, 펌웨어 및 라이프사이클 서비스를 오케스트레이션할 수 있는 공급업체는 총 소유 비용(TCO)이 부품 가격(Component Price)을 능가함에 따라 제스처 인식 시장에서 로열티를 획득하는 태세를 갖추고 있습니다.

지역 분석

아시아태평양의 이점은 수직 통합 공급망, 정부 지원 자금, 조기 어댑터의 방대한 설치 기반으로 이루어져 있습니다. 각 지역의 휴대전화 브랜드는 10-12개월마다 새로운 플래그쉽 모델을 발표하고 있으며, 그 때마다 고해상도 ToF 어레이가 내장되어 있기 때문에 센서 벤더에게는 제스처 인식 시장 규모가 확대되고 있습니다. 일본의 콩그로말리트는 자동차 용접 및 반도체 리소그래피에 XR 기반의 기술 이전 플랫폼을 채용하여 고정밀 제스처 모델 수요를 강화하고 있습니다. 한국의 웨이퍼 생산 능력은 구성 요소의 연속성을 확보하고, 인도 스마트 TV의 확대는 터치리스 리모컨을 중간 소득 가구에 도입하여 수익 피라미드를 넓힙니다.

북미에서는 수술실과 진단센터에서 헬스케어의 지출력을 활용하여 유닛당 프리미엄 수익을 창출하고 있습니다. 현장 디스플레이를 채택한 병원에서는 교차 오염 사고의 상당한 감소가 보고되고 재입원 벌금이 감소하고 제스처 인터페이스의 ROI가 강화됩니다. 자동차 OEM은 주의 산만 운전에 관한 2024년 이후의 연방 가이드라인을 준수하기 위해 제스처 기반의 드라이버 모니터링을 통합하고 센서 장착률을 밀어 올렸습니다.

유럽은 규제의 페이스 세터 역할을 합니다. 유로 NCAP 지령은 와키미 운전 경감 기술을 의무화해, 고급차와 대중차의 양 클래스에의 전개를 가속시키고 있습니다. 독일공급업체는 국내 자동차 제조업체와 제스처 모듈을 공동 개발하여 하드웨어 조달이 세계화되고 있음에도 불구하고 지역적 가치 획득을 확고히 하고 있습니다. 한편, GCC 국가들은 터치리스 UI를 갖춘 공공 서비스 키오스크에 자금을 제공하는 AI 주권 이니셔티브를 추진하고 있으며, 중동은 현재의 기반에 비해 돌출된 성장 프로파일을 갖게 됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 아시아 전역에서 플래그십 스마트폰에 mm파 센서와 ToF 센서가 보급

- 유로 NCAP 주의 산만 방지 규정 충족을 위해 자동차 제조업체의 실내 제스처 HUD 도입

- 수술실의 HAI 위험 감소를 위해 터치프리 HMI에 대한 병원 수요(미국과 독일)

- XR 웨어러블에의 통합에 의해 산업 트레이닝용 6-DoF 제어가 가능(일본)

- 스마트 TV 벤더가 에어 제스처 리모컨을 번들해 가격 급락 시장에서의 차별화를 도모

- 정부의 스마트 시티 보조금이 공공 키오스크 제스처 UI 전개를 촉진(GCC)

- 시장 성장 억제요인

- 열대지역에서의 비전 기반 시스템의 태양광 하에서 높은 위양성률

- 개방적인 상호 운용성 표준의 부재가 OEM의 통합 비용 상승 촉진

- 10nm 이하의 모바일 SoC로 배터리를 소모하는 "항상 온"제스처 웨이크워드

- GDPR(EU 개인정보보호규정) 하의 차내 비디오 해석에 있어서 데이터 프라이버시 준수의 허들

- 규제 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 기술별

- 터치 기반 제스처 인식

- 2D 멀티 터치 패널

- 정전식 및 저항식 센서

- 터치리스 제스처 인식

- 2D 카메라 기반

- 3차원 깊이 및 ToF

- 초음파 및 mm파 레이더

- 터치 기반 제스처 인식

- 구성 요소별

- 하드웨어(센서, 컨트롤러, SoC)

- 소프트웨어(ML 알고리즘, SDK, 미들웨어)

- 제스처 유형별

- 온라인 동적 제스처

- 오프라인 정적 제스처

- 인증별

- 생체 인식(얼굴, 홍채, 손바닥 정맥)

- 비생체 인식(동작, 자세)

- 최종 사용자 업계별

- 소비자 가전

- 스마트폰 및 태블릿

- 스마트 TV 및 셋톱박스

- AR/VR 및 웨어러블

- 자동차

- 운전자 모니터링 및 인포테인먼트

- 항공우주 및 방위

- 헬스케어

- 수술실 및 진단실

- 게임 및 엔터테인먼트

- 산업 및 로봇공학

- 기타 산업

- 소비자 가전

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 뉴질랜드, 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC(사우디아라비아, 아랍 에미리트, 카타르)

- 튀르키예

- 남아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Intel Corporation

- Qualcomm Technologies Inc.

- Apple Inc.

- Microsoft Corp.

- Sony Group Corp.

- Google LLC

- Meta Platforms Inc.

- Ultraleap Ltd.

- Microchip Technology Inc.

- Infineon Technologies AG

- Synaptics Inc.

- Elliptic Laboratories AS

- GestureTek Inc.

- Cognitec Systems GmbH

- Eyesight Technologies Ltd.

- PointGrab Ltd.

- Omron Corporation

- Jabil Inc.

- Leap Motion

제7장 시장 기회와 향후 전망

KTH 25.11.12The Gesture Recognition Market size is estimated at USD 30.48 billion in 2025, and is expected to reach USD 87.19 billion by 2030, at a CAGR of 23.39% during the forecast period (2025-2030).

This sustained expansion reflects the convergence of advanced millimeter-wave radar, multizone Time-of-Flight (ToF) sensors, and edge-AI algorithms that together enable responsive, low-latency human-machine interfaces across smartphones, vehicles, medical devices, and industrial equipment. Accelerating sensor shipments in premium handsets, regulatory pressure on automotive safety systems, and infection-control imperatives in healthcare are jointly stimulating volume demand. At the same time, the gesture recognition market is witnessing a value shift from hardware-centric solutions toward software and AI stacks that personalize interactions, reduce false positives, and extend device longevity. Regional manufacturing incentives most notably the CHIPS Act in the United States and the European Chips Act are reshaping supply chains and creating new cost advantages for local component production. As these drivers converge, industry participants that integrate vertically across sensor, software, and cloud orchestration layers are positioned to capture disproportionate returns within the gesture recognition market.

Global Gesture Recognition Market Trends and Insights

Proliferation of mm-wave and ToF sensors in flagship smartphones across Asia

Asia-based handset OEMs now embed multizone ToF modules such as STMicroelectronics' VL53L7CX to deliver millimeter-level depth accuracy without ambient-light restrictions, enabling reliable mid-air command input even under harsh illumination. The deployment extends to smart-TV handsets through Ceva's MotionEngine Hex firmware, which integrates inertial and radar data to deliver spatial control of user interfaces. As the cost of ToF chipsets falls below USD 1 per unit in volume lots, gesture control is transitioning from a premium differentiator to a default feature in the gesture recognition market.

Automaker adoption of in-cabin gesture HUDs to meet Euro NCAP mandates

The July 2024 Advanced Driver Distraction Warning regulation obliges OEMs to mitigate cognitive load, propelling rapid integration of camera-based gesture hubs in European models. BMW's Level 2/3 certification on the 7 Series demonstrates commercial readiness, while Audi's 3-D cockpit interface showcases multi-modal infotainment selection using above-console hand sweeps. Suppliers that can guarantee sub-150 ms response times and <3% false-trigger rates stand to win program awards, reinforcing the growth trajectory of the gesture recognition market.

High false-positive rates in sunlight for vision-based systems in tropical regions

Camera-centric algorithms struggle to resolve hand contours against high-lux backgrounds, driving error spikes in outdoor kiosks and ride-hailing vehicles. Research indicates radar-based alternatives maintain >90% precision independent of illumination, prompting system designers to adopt multi-sensor fusion in the gesture recognition market.

Other drivers and restraints analyzed in the detailed report include:

- Hospital demand for touch-free HMI to cut HAI risks in surgical suites

- Integration into XR wearables to unlock 6-DoF control for industrial training

- Absence of open interoperability standards inflating OEM integration cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Touchless solutions generated 58.2% of 2024 revenue, reflecting end-market emphasis on hygiene, driver safety, and immersive entertainment. The touchless sub-segment will compound at 24.4% through 2030, outpacing the broader gesture recognition market as ToF, mm-wave radar, and ultrasonic arrays reduce bill-of-materials cost. In contrast, capacitive touch-based controls retain relevance in cost-sensitive consumer devices, yet their CAGR trails at single-digits. Kyocera's depth sensor demonstrates 100 µm resolution within 10 cm, enabling robotic pick-and-place and orthopedic alignment tools that demand surgical-grade accuracy. The steady migration toward ambient interaction implies touchless modalities will ultimately hold a greater gesture recognition market share than their contact-dependent predecessors.

Touchless expansion is altering supplier power dynamics. Sensor vendors that historically commoditized silicon are now bundling AI firmware, data models, and developer portals, capturing recurring license fees on top of hardware margins. This re-bundling aligns with OEM priorities for field-upgradable over-the-air performance improvements and supports the scalable economics required for high-volume touchless adoption within the gesture recognition market.

Hardware contributed 71.5% of gesture recognition market size in 2024, driven by the intrinsic cost of lenses, radar front-ends, and MCUs. However, software platforms that deliver contextual awareness, user adaptation, and federated learning are forecast at a 23.7% CAGR-more than 350 bps above hardware growth. Infineon's DEEPCRAFT Ready Models supply pre-trained neural networks for common gestures, cutting integration time by 40% and repositioning the firm higher on the value curve. Meanwhile, Imagimob's visual graph-based ML tooling compresses model-development cycles to hours, democratizing AI optimization for mid-tier OEMs.

The revenue mix shift creates opportunities for service bundling: predictive maintenance, cloud-based analytics, and in-app monetization through gesture-initiated digital purchases. Suppliers able to orchestrate silicon, firmware, and lifecycle services are poised to command loyalty in the gesture recognition market as total cost of ownership eclipses component price considerations.

Gesture Recognition Market Report is Segmented by Technology (Touch-Based Gesture Recognition, Touchless Gesture Recognition), Component (Hardware, Software), Gesture Type (Online Dynamic Gestures, Offline Static Gestures), Authentication (Biometric, Non-Biometric), End-User Industry (Consumer Electronics, Automotive, Aerospace and Defense and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific's dominance rests on vertically integrated supply chains, supportive government funding, and an immense installed base of early-adopter consumers. Regional handset brands release new flagship lines every 10-12 months, each iteration embedding higher-resolution ToF arrays, thereby expanding the gesture recognition market size for sensor vendors. Japanese conglomerates employ XR-based skill-transfer platforms in automotive welding and semiconductor lithography, reinforcing demand for high-precision gesture models. South Korea's wafer capacity secures component continuity, while India's smart-TV expansion introduces touchless remotes into middle-income households, broadening the revenue pyramid.

North America leverages healthcare spending power for surgical suites and diagnostic centers, generating premium revenue per unit. Hospitals adopting mid-air displays report significant reductions in cross-contamination incidents, translating into lower readmission penalties and bolstering ROI for gesture interfaces. Automotive OEMs integrate gesture-based driver monitoring to comply with post-2024 federal guidelines on distracted driving, pushing incremental sensor attach rates.

Europe acts as a regulatory pacesetter. Euro NCAP directives mandate distraction-mitigation technologies, accelerating deployment across both luxury and mass-market vehicle classes. German suppliers co-develop gesture modules with domestic automakers, cementing regional value capture despite globalized hardware sourcing. Meanwhile, GCC nations pursue AI sovereignty initiatives that fund public-service kiosks with touchless UIs, giving the Middle East an outsized growth profile relative to its current base.

- Intel Corporation

- Qualcomm Technologies Inc.

- Apple Inc.

- Microsoft Corp.

- Sony Group Corp.

- Google LLC

- Meta Platforms Inc.

- Ultraleap Ltd.

- Microchip Technology Inc.

- Infineon Technologies AG

- Synaptics Inc.

- Elliptic Laboratories AS

- GestureTek Inc.

- Cognitec Systems GmbH

- Eyesight Technologies Ltd.

- PointGrab Ltd.

- Omron Corporation

- Jabil Inc.

- Leap Motion

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of mm-wave and ToF sensors in flagship smartphones across Asia

- 4.2.2 Automaker adoption of in-cabin gesture HUDs to meet Euro NCAP distraction mandates

- 4.2.3 Hospital demand for touch-free HMI to cut HAI risks in surgical suites (US and Germany)

- 4.2.4 Integration into XR wearables to unlock 6-DoF control for industrial training (Japan)

- 4.2.5 Smart-TV vendors bundling air-gesture remotes to differentiate in price-eroding market

- 4.2.6 Government smart-city grants driving public-kiosk gesture UI roll-outs (GCC)

- 4.3 Market Restraints

- 4.3.1 High false-positive rates in sunlight for vision-based systems in tropical regions

- 4.3.2 Absence of open interoperability standards inflating OEM integration cost

- 4.3.3 "Always-on" gesture wake-word draining battery in sub-10 nm mobile SoCs

- 4.3.4 Data-privacy compliance hurdles for in-cabin video analytics under GDPR

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Touch-based Gesture Recognition

- 5.1.1.1 2-D Multi-touch Panels

- 5.1.1.2 Capacitive and Resistive Sensors

- 5.1.2 Touchless Gesture Recognition

- 5.1.2.1 2-D Camera-based

- 5.1.2.2 3-D Depth and ToF

- 5.1.2.3 Ultrasonic and mm-wave Radar

- 5.1.1 Touch-based Gesture Recognition

- 5.2 By Component

- 5.2.1 Hardware (Sensors, Controllers, SoCs)

- 5.2.2 Software (ML Algorithms, SDKs, Middleware)

- 5.3 By Gesture Type

- 5.3.1 Online Dynamic Gestures

- 5.3.2 Offline Static Gestures

- 5.4 By Authentication

- 5.4.1 Biometric (Face, Iris, Palm-vein)

- 5.4.2 Non-biometric (Motion, Pose)

- 5.5 By End-user Industry

- 5.5.1 Consumer Electronics

- 5.5.1.1 Smartphones and Tablets

- 5.5.1.2 Smart-TV and Set-top Boxes

- 5.5.1.3 AR/VR and Wearables

- 5.5.2 Automotive

- 5.5.2.1 Driver Monitoring and Infotainment

- 5.5.3 Aerospace and Defense

- 5.5.4 Healthcare

- 5.5.4.1 Surgical and Diagnostic Rooms

- 5.5.5 Gaming and Entertainment

- 5.5.6 Industrial and Robotics

- 5.5.7 Other Industries

- 5.5.1 Consumer Electronics

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 New Zealand and Australia

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 GCC (Saudi Arabia, UAE, Qatar)

- 5.6.5.2 Turkey

- 5.6.5.3 South Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Intel Corporation

- 6.4.2 Qualcomm Technologies Inc.

- 6.4.3 Apple Inc.

- 6.4.4 Microsoft Corp.

- 6.4.5 Sony Group Corp.

- 6.4.6 Google LLC

- 6.4.7 Meta Platforms Inc.

- 6.4.8 Ultraleap Ltd.

- 6.4.9 Microchip Technology Inc.

- 6.4.10 Infineon Technologies AG

- 6.4.11 Synaptics Inc.

- 6.4.12 Elliptic Laboratories AS

- 6.4.13 GestureTek Inc.

- 6.4.14 Cognitec Systems GmbH

- 6.4.15 Eyesight Technologies Ltd.

- 6.4.16 PointGrab Ltd.

- 6.4.17 Omron Corporation

- 6.4.18 Jabil Inc.

- 6.4.19 Leap Motion

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment